Europe Instrument Cluster Market

Market Size in USD Billion

USD

3.07 Billion

USD

4.64 Billion

2025

2033

USD

3.07 Billion

USD

4.64 Billion

2025

2033

| 2026 - 2033 | |

| USD 3.07 Billion | |

| USD 4.64 Billion | |

| % | |

|

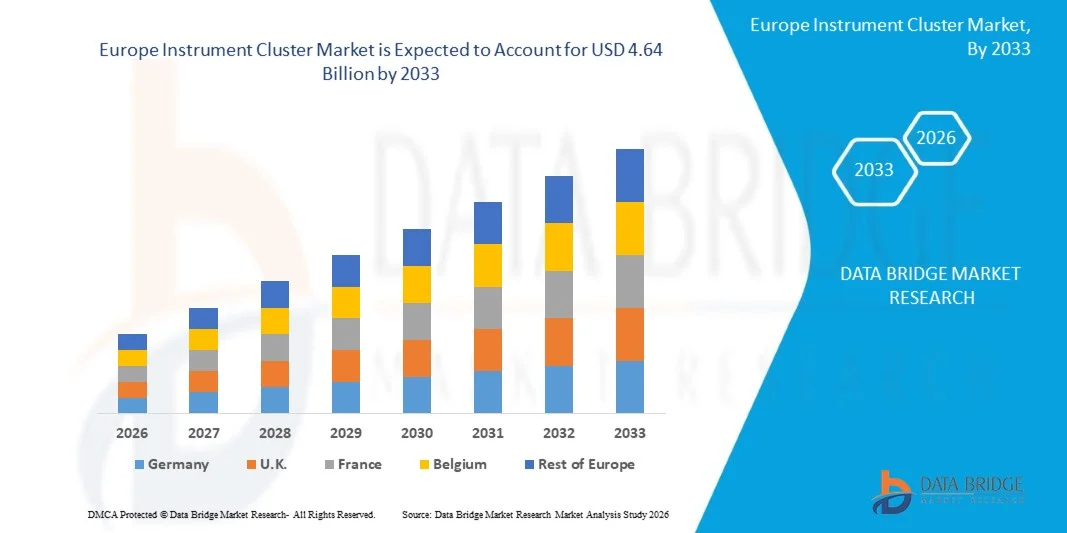

Europe Instrument Cluster Market Size

- The Europe Instrument Cluster Market size was valued at USD 3.07 billion in 2025 and is expected to reach USD 4.64 billion by 2033, at a CAGR of 5.3% during the forecast period

- The market growth is largely fueled by the increasing adoption of connected and software-defined vehicles, along with rapid advancements in digital display technologies, leading to enhanced driver interaction and real-time vehicle data visualization across passenger and commercial vehicles

- Furthermore, rising consumer demand for advanced in-vehicle experiences, improved safety features, and seamless integration with infotainment and navigation systems is positioning instrument clusters as a critical component of modern automotive cockpits. These converging factors are accelerating the transition from analog to fully digital clusters, thereby significantly boosting the industry's growth

Europe Instrument Cluster Market Analysis

- Instrument clusters are integrated display systems in vehicles that provide critical information such as speed, fuel level, engine performance, and navigation through analog, hybrid, or fully digital interfaces. These systems are increasingly evolving into intelligent human-machine interfaces that enhance driving safety, convenience, and overall user experience

- The escalating demand for instrument clusters is primarily driven by the rapid electrification of vehicles, increasing integration of advanced driver assistance systems, and growing preference for customizable and high-resolution digital displays that support connected and data-driven mobility solutions

- Germany dominated the Europe Instrument Cluster Market in 2025, due to its strong automotive manufacturing base, advanced engineering capabilities, and rapid adoption of digital cockpit technologies across premium and mass-market vehicles

- U.K. is expected to be the fastest growing country in the Europe Instrument Cluster Market during the forecast period due to rising investments in electric vehicle manufacturing, increasing adoption of connected mobility solutions, and strong demand for advanced in-vehicle digital interfaces

- ICE vehicle segment dominated the market with a market share of 65.5% in 2025, due to its extensive global fleet presence and established manufacturing ecosystem. Traditional vehicles continue to require robust instrument clusters for monitoring engine parameters and diagnostics. The widespread adoption across developing regions sustains demand for conventional cluster systems

Report Scope and Europe Instrument Cluster Market Segmentation

|

Attributes |

Instrument Cluster Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Europe

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, geographically represented company-wise production and capacity, network layouts of distributors and partners, detailed and updated price trend analysis and deficit analysis of supply chain and demand. |

Europe Instrument Cluster Market Trends

“Integration of Digital and Fully Virtual Displays in Automotive Cockpits”

- A significant trend in the Europe Instrument Cluster Market is the growing shift toward fully digital and virtual display systems integrated into modern automotive cockpits, replacing traditional analog dashboards with high-resolution, customizable interfaces. This transition is being driven by the need for enhanced driver experience, real-time vehicle data visualization, and seamless connectivity across infotainment and driving assistance systems

- For instance, Mercedes-Benz has implemented the MBUX Hyperscreen in its EQS series, which integrates a fully digital instrument cluster with AI-driven interface capabilities, offering a unified and immersive cockpit experience. Such developments enhance driver interaction, improve accessibility of critical information, and elevate overall vehicle usability through advanced visualization systems

- The adoption of reconfigurable digital clusters is increasing as automotive manufacturers prioritize personalization, allowing drivers to customize layouts, themes, and displayed driving information. This is enabling greater flexibility in vehicle interfaces and supporting the broader shift toward software-defined vehicle architectures

- Luxury and premium vehicle segments are leading the deployment of high-definition OLED and TFT-based instrument clusters, where clarity, responsiveness, and aesthetic design play a critical role in differentiating vehicle offerings. This is strengthening the demand for advanced display technologies that enhance both functionality and visual appeal

- The integration of advanced driver assistance system (ADAS) feedback into instrument clusters is expanding as real-time alerts, navigation prompts, and safety warnings are directly projected onto digital displays. This is improving situational awareness and supporting safer driving experiences across modern vehicle platforms

- The market is witnessing continued evolution toward fully connected digital cockpits where instrument clusters function as central information hubs linked with infotainment, telematics, and vehicle control systems. This is reinforcing the role of digital clusters as essential components in next-generation automotive ecosystems

Europe Instrument Cluster Market Dynamics

Driver

“Rising Adoption of Connected and Electric Vehicles”

- The increasing global adoption of connected vehicles and electric vehicles is significantly driving demand for advanced instrument clusters that can support real-time data monitoring, energy efficiency metrics, and integrated connectivity features. These vehicles require highly intelligent digital dashboards capable of displaying battery status, range estimation, navigation data, and system diagnostics in real time

- For instance, Tesla integrates fully digital instrument cluster systems within its Model 3 and Model Y vehicles, offering centralized display interfaces that provide live vehicle performance data, autonomous driving updates, and connectivity-based functionalities. Such implementations highlight the growing reliance on advanced clusters to support software-driven vehicle ecosystems and enhance user interaction

- The expansion of electric vehicle adoption is increasing the need for instrument clusters capable of managing complex energy consumption data and regenerative braking insights, which are essential for optimizing vehicle efficiency. This is driving innovation in display systems that can process and present large volumes of real-time vehicle information clearly and effectively

- Connected vehicle platforms are enabling continuous data exchange between vehicles and external networks, increasing the importance of clusters that can integrate cloud-based updates, navigation services, and predictive maintenance alerts. This is strengthening the role of instrument clusters as central digital communication hubs within modern vehicles

- The growing consumer preference for technologically advanced and feature-rich vehicles continues to reinforce this driver, as instrument clusters evolve into essential interfaces for managing connected mobility experiences. This sustained demand is supporting long-term growth in the market

Restraint/Challenge

“High Development Cost and Complex Integration of Advanced Display Technologies”

- The Europe Instrument Cluster Market faces significant challenges due to the high development cost associated with advanced display technologies such as OLED, TFT, and fully digital cockpit systems, which require substantial investment in research, design, and manufacturing processes. These technologies demand precision engineering and continuous innovation to meet automotive safety and performance standards

- For instance, Continental AG develops advanced digital instrument clusters integrated with multi-display cockpit systems that require complex hardware-software synchronization and extensive validation testing. This complexity increases production costs and extends development cycles, making large-scale adoption more resource-intensive

- Integrating advanced instrument clusters into modern vehicle architectures requires compatibility with multiple electronic control units, infotainment systems, and ADAS platforms, which adds to system complexity. This creates challenges for automakers in ensuring seamless communication and functional stability across interconnected systems

- The need for high-resolution displays, durable components, and automotive-grade reliability increases material and production expenses, particularly in premium and electric vehicle segments. This cost burden limits adoption in cost-sensitive markets and entry-level vehicle categories

- The market continues to experience constraints related to balancing advanced functionality with cost efficiency and scalable production. These challenges collectively impact profitability and slow down widespread deployment of next-generation instrument cluster systems across all vehicle segments

Europe Instrument Cluster Market Scope

The market is segmented on the basis of utility, vehicle type, technology, enterprise size, and end-user.

• By Utility

On the basis of utility, the Europe Instrument Cluster Market is segmented into speedometer, odometer, tachometer, coolant temperature gauge, oil pressure gauge, and others. The speedometer segment dominated the largest market revenue share in 2025, driven by its fundamental role in vehicle operation and regulatory compliance across all vehicle categories. It remains a critical component as it provides real-time speed monitoring, ensuring driver safety and adherence to traffic norms. Increasing integration of digital displays has enhanced speedometer functionality with navigation overlays and alerts. Automakers prioritize advanced speedometer interfaces to improve user experience and driving efficiency. The demand is further supported by its universal requirement across conventional and electric vehicles.

The tachometer segment is anticipated to witness the fastest growth rate from 2026 to 2033, fueled by rising demand for performance monitoring and efficient engine management. Modern vehicles increasingly incorporate advanced tachometers to optimize fuel efficiency and engine lifespan. Growing adoption in electric and hybrid vehicles for power output visualization is accelerating segment expansion. Enhanced graphical interfaces in digital clusters are improving readability and driver engagement. The focus on performance analytics in premium and sports vehicles is also contributing to its rapid growth trajectory.

• By Vehicle Type

On the basis of vehicle type, the Europe Instrument Cluster Market is segmented into ICE vehicle, battery electric vehicle (BEV), plug-in hybrid electric vehicle (PHEV), hybrid electric vehicle (HEV), and fuel cell electric vehicle (FCEV). The ICE vehicle segment dominated the largest market revenue share of 65.5% in 2025, driven by its extensive global fleet presence and established manufacturing ecosystem. Traditional vehicles continue to require robust instrument clusters for monitoring engine parameters and diagnostics. The widespread adoption across developing regions sustains demand for conventional cluster systems. Incremental upgrades in semi-digital clusters are further supporting growth in this segment. Cost efficiency and compatibility with existing vehicle architectures reinforce its dominance.

The battery electric vehicle (BEV) segment is expected to witness the fastest CAGR from 2026 to 2033, driven by accelerating electrification trends and government incentives promoting zero-emission mobility. BEVs require advanced digital clusters to display battery status, range, and energy consumption insights. Increasing consumer preference for connected and tech-enabled vehicles is boosting adoption. Automakers are investing heavily in futuristic display technologies tailored for EV platforms. The shift toward software-defined vehicles is further strengthening demand in this segment.

• By Technology

On the basis of technology, the Europe Instrument Cluster Market is segmented into hybrid, analog, and digital. The analog segment dominated the largest market revenue share in 2025, driven by its cost-effectiveness and widespread use in entry-level and mid-range vehicles. Analog clusters are preferred for their simplicity, reliability, and ease of maintenance. Many manufacturers continue to deploy analog systems in price-sensitive markets to maintain affordability. The familiarity of traditional gauges also supports consumer acceptance. Continued demand from developing regions sustains the segment’s leading position.

The digital segment is anticipated to witness the fastest growth rate from 2026 to 2033, fueled by increasing demand for advanced user interfaces and connected vehicle features. Digital clusters offer customizable displays, enhanced graphics, and integration with infotainment and navigation systems. Automakers are focusing on high-resolution screens to improve driver interaction and safety. Rising adoption in premium and electric vehicles is accelerating growth. Continuous advancements in display technologies are further expanding its application scope.

• By Enterprise Size

On the basis of enterprise size, the Europe Instrument Cluster Market is segmented into small-scale organization, semi-urban mid-scale organization, and large scale organizations. The large scale organizations segment dominated the largest market revenue share in 2025, driven by their strong manufacturing capabilities and extensive distribution networks. These organizations invest significantly in research and development to integrate advanced technologies into instrument clusters. Their ability to cater to automotive OEMs strengthens market presence. High production volumes enable cost optimization and scalability. Strategic partnerships with technology providers further reinforce their dominance.

The semi-urban mid-scale organization segment is expected to witness the fastest CAGR from 2026 to 2033, driven by increasing participation in regional automotive supply chains. These organizations are rapidly adopting modern manufacturing techniques to stay competitive. Growing demand from emerging markets is creating new growth opportunities. Their flexibility in customization and cost management is attracting OEM collaborations. Expansion into digital cluster production is further accelerating segment growth.

• By End-User

On the basis of end-user, the Europe Instrument Cluster Market is segmented into passenger cars, commercial vehicles, two-wheelers, off-highway vehicle, agriculture vehicle, and others. The passenger cars segment dominated the largest market revenue share in 2025, driven by high production volumes and increasing consumer demand for advanced in-vehicle technologies. Instrument clusters in passenger cars are evolving with enhanced digital interfaces and connectivity features. Rising disposable income and preference for premium driving experiences support segment growth. Automakers are integrating multifunctional displays to improve safety and convenience. Continuous innovation in user interface design further strengthens its leading position.

The two-wheelers segment is anticipated to witness the fastest growth rate from 2026 to 2033, fueled by increasing adoption of smart and connected motorcycles and scooters. Rising urbanization and demand for efficient mobility solutions are driving segment expansion. Digital instrument clusters in two-wheelers are gaining traction due to features such as navigation and smartphone connectivity. Manufacturers are focusing on compact and cost-effective display solutions. Growing electrification in two-wheelers is further accelerating demand for advanced cluster systems.

Europe Instrument Cluster Market Regional Analysis

- Germany dominated the Europe Instrument Cluster Market with the largest revenue share in 2025, driven by its strong automotive manufacturing base, advanced engineering capabilities, and rapid adoption of digital cockpit technologies across premium and mass-market vehicles

- The presence of leading automotive OEMs such as BMW, Mercedes-Benz Group AG, and Volkswagen Group strengthens the demand for advanced digital instrument clusters featuring fully integrated infotainment and driver assistance interfaces. These manufacturers consistently invest in next-generation cockpit architectures that enhance driver experience and support software-defined vehicle development

- Increasing innovation in display technologies, expansion of electric vehicle production, and strong focus on autonomous driving systems further reinforce Germany’s dominant position in the Europe Instrument Cluster Market

U.K. Europe Instrument Cluster Market Insight

The U.K. is projected to register the fastest CAGR in the Europe Instrument Cluster Market during the forecast period, supported by rising investments in electric vehicle manufacturing, increasing adoption of connected mobility solutions, and strong demand for advanced in-vehicle digital interfaces. The country’s shift toward smart mobility and electrification is driving rapid integration of next-generation instrument cluster technologies. Automotive manufacturers such as Jaguar Land Rover are advancing digital cockpit platforms by integrating high-resolution instrument clusters with connected infotainment and real-time vehicle data systems across their vehicle lineup. Expanding EV production initiatives, growing focus on autonomous driving technologies, and increasing collaboration between automotive OEMs and technology providers are positioning the U.K. as the fastest-growing market in Europe.

France Europe Instrument Cluster Market Insight

France is expected to witness steady growth in the Europe Instrument Cluster Market during the forecast period, driven by increasing integration of digital dashboards in passenger vehicles, rising electric vehicle adoption, and strong emphasis on automotive safety and regulatory compliance. The country’s automotive sector is gradually transitioning toward connected and electrified vehicle platforms supported by digital instrumentation systems. Leading automotive manufacturers such as Renault Group and Stellantis are contributing to the development and deployment of advanced instrument cluster systems featuring digital displays, real-time navigation, and driver assistance integration. Growing focus on sustainable mobility, expansion of electric vehicle infrastructure, and continuous advancements in automotive electronics are reinforcing France’s position as a stable and steadily expanding market in the Europe instrument cluster industry.

Europe Instrument Cluster Market Share

The instrument cluster industry is primarily led by well-established companies, including:

- Visteon Corporation (U.S.)

- Continental AG (Germany)

- Parker Hannifin Corp (U.S.)

- Robert Bosch GmbH (Germany)

- Infineon Technologies AG (Germany)

- HARMAN International (U.S.)

- Aptiv PLC (Ireland)

- YAZAKI Corporation (Japan)

- Nippon Seiki Co., Ltd. (Japan)

- DENSO Corporation (Japan)

- Renesas Electronics Corporation (Japan)

- IAC Group (U.S.)

- Luxoft, A DXC Technology Company (Switzerland)

- Spark Minda (India)

- ALPS ALPINE CO., LTD (Japan)

- Panasonic Corporation (Japan)

- Simco Ltd (U.K.)

- Texas Instruments Incorporated (U.S.)

- Mini Meters Manufacturing Co. Pvt. Ltd. (India)

- Embitel (India)

Latest Developments in Europe Instrument Cluster Market

- In March 2025, Visteon Corporation introduced its next-generation fully digital instrument cluster platform integrated with AI-driven personalization features, enabling real-time data visualization and adaptive user interfaces. This development is strengthening the transition toward software-defined cockpits by enhancing user experience and enabling automakers to offer differentiated in-vehicle digital environments. It is also accelerating the adoption of high-performance computing platforms within instrument clusters, supporting scalability across vehicle segments and boosting overall market demand for intelligent display systems

- In September 2024, Denso Corporation expanded its development of augmented reality-based instrument clusters integrated with head-up display systems to improve driver awareness and safety. This advancement is driving the adoption of immersive visualization technologies that overlay critical driving information directly within the driver’s field of vision. It is further encouraging OEMs to invest in advanced human-machine interface solutions, thereby increasing the penetration of premium and technologically advanced instrument cluster systems across modern vehicles

- In May 2023, Nippon Seiki Co., Ltd. launched a high-resolution TFT digital instrument cluster specifically designed for electric vehicles with enhanced battery monitoring and energy efficiency insights. This innovation is supporting the growing electrification trend by providing EV users with more precise and actionable vehicle data. It is also enabling automakers to deliver customized digital interfaces for electric mobility, thereby expanding the role of instrument clusters beyond traditional displays and strengthening market growth in EV-focused applications

- In November 2021, Robert Bosch GmbH announced its Engineering Centre in Sofia focused on developing technologies for vehicle electrification, connectivity solutions, displays, instrument clusters, and driver monitoring systems. This expansion is enhancing Bosch’s R&D capabilities and accelerating innovation in integrated cockpit systems that combine multiple vehicle functions into a unified interface. It is also contributing to the development of scalable and modular cluster solutions, supporting the increasing demand for connected and intelligent automotive systems across global markets

- In January 2021, Continental AG collaborated with Leia Inc. to develop a 3D display based on natural Lightfield Technology designed to reduce weight, optimize space, and enhance in-vehicle digital interaction. This collaboration is advancing next-generation display capabilities by enabling glasses-free 3D visualization within instrument clusters and infotainment systems. It is also supporting automakers in differentiating their vehicle offerings through innovative display technologies, thereby driving competitive advancements and expanding the application scope of digital instrument clusters in connected vehicles

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Europe Instrument Cluster Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Europe Instrument Cluster Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Europe Instrument Cluster Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.