Europe Laryngoscopes Market

Market Size in USD Million

USD

718.10 Million

USD

1,473.41 Million

2024

2032

USD

718.10 Million

USD

1,473.41 Million

2024

2032

| 2025 - 2032 | |

| USD 718.10 Million | |

| USD 1,473.41 Million | |

| % | |

|

Europe Laryngoscopes Market Size

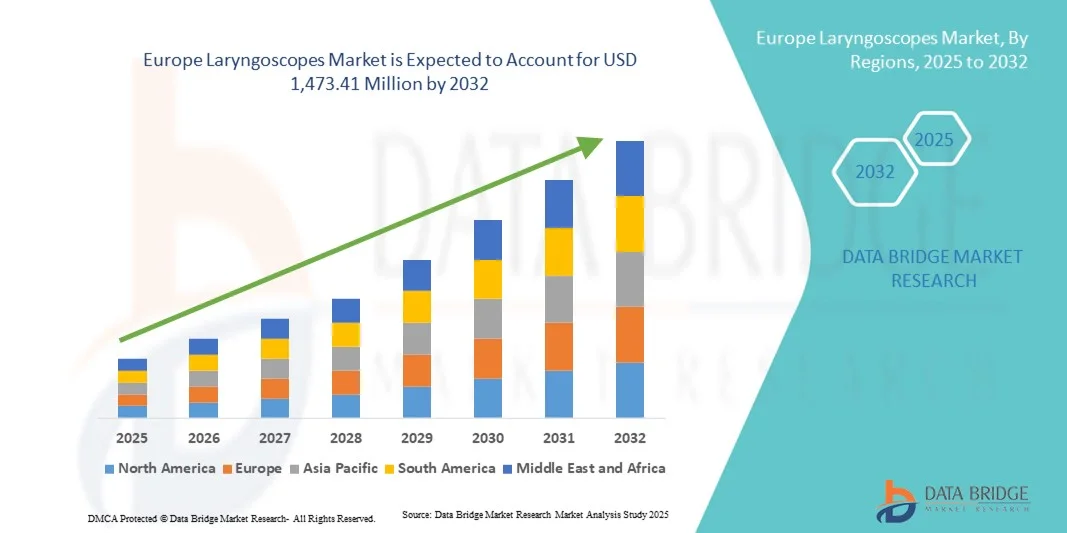

- The Europe laryngoscopes market size was valued at USD 718.10 million in 2024 and is expected to reach USD 1,473.41 million by 2032, at a CAGR of 9.4% during the forecast period

- This growth is primarily driven by advancements in medical technology, increasing demand for minimally invasive procedures, and the rising prevalence of respiratory disorders

- In addition, the adoption of video laryngoscopes, known for enhanced visualization and improved patient outcomes, is contributing significantly to market expansion

Europe Laryngoscopes Market Analysis

- Laryngoscopes are used for airway management and intubation procedures in hospitals and clinics, are increasingly vital in European healthcare settings due to their role in anesthesiology, emergency medicine, and intensive care

- The escalating demand for laryngoscopes is primarily fueled by increasing prevalence of respiratory disorders, technological advancements such as video and fiberoptic laryngoscopes, and a growing focus on patient safety during intubation procedures

- Germany dominated the European laryngoscopes market with the largest revenue share of 29% in 2024, characterized by a strong healthcare infrastructure, high adoption of advanced medical devices, and a strong presence of key industry players, while France and other Western European countries also contributed significantly to market growth.

- The United Kingdom is expected to be the fastest-growing country in the European laryngoscopes market during the forecast period due to rapid adoption of advanced airway management devices, expanding healthcare infrastructure, and increasing investments in digital and video laryngoscopy technologies

- Rigid laryngoscopes dominated the market in 2024 with a market share of 52.8%, driven by their established reliability, wide availability, and compatibility with existing hospital protocols

Report Scope and Europe Laryngoscopes Market Segmentation

|

Attributes |

Europe Laryngoscopes Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Europe

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Europe Laryngoscopes Market Trends

Enhanced Convenience Through AI and Voice Integration

- A significant and accelerating trend in the European laryngoscopes market is the deepening integration with artificial intelligence (AI) and voice-controlled systems in operating rooms. This fusion of technologies is enhancing procedural accuracy, workflow efficiency, and patient safety

- For instance, AI algorithms in video laryngoscopes assist in glottic opening detection, improving intubation accuracy, while voice-controlled laryngoscopes enable hands-free operation, maintaining sterility in surgeries

- AI integration enables features such as predictive guidance during difficult intubations and intelligent alerts for procedural deviations. Some advanced models also learn user patterns to suggest workflow optimizations. Voice control further allows clinicians to adjust settings or capture images without touching the device

- The seamless integration of laryngoscopes with hospital digital systems facilitates centralized control over surgical tools, patient monitoring, and data recording, enhancing the overall efficiency of operating rooms

- This trend towards more intelligent, intuitive, and interconnected devices is reshaping expectations for medical equipment. Consequently, companies such as Ambu and Verathon are developing AI-enabled laryngoscopes with features such as automatic visualization assistance and voice-command functionality

- The demand for laryngoscopes with AI and voice control integration is growing rapidly across hospitals and clinics in Europe, as medical professionals prioritize efficiency, patient safety, and advanced procedural guidance

Europe Laryngoscopes Market Dynamics

Driver

Growing Need Due to Increasing Healthcare Complexity and Aging Population

- The rising prevalence of respiratory and airway-related conditions, alongside increasing complexity in medical procedures, is a key driver of the European laryngoscopes market

- For instance, hospitals are adopting video and AI-enabled laryngoscopes to improve procedural success rates in critical care and surgical interventions

- As the European population ages, demand for airway management devices rises due to higher incidences of respiratory complications and surgeries

- Furthermore, hospitals and surgical centers are increasingly integrating advanced laryngoscopes with digital healthcare ecosystems, enabling centralized monitoring and efficient patient management

- The convenience of improved visualization, predictive guidance, and hands-free operation through AI and voice control are key factors propelling adoption among healthcare providers

- The trend towards upgrading standard devices to smart laryngoscopes and the growing number of training programs for advanced airway management further support market growth

Restraint/Challenge

Cybersecurity Issues and Regulatory Compliance Hurdles

- Concerns surrounding cybersecurity vulnerabilities in AI-enabled and connected medical devices, including laryngoscopes, pose a significant challenge for market adoption

- For instance, EU Medical Device Regulations (MDR) require manufacturers to ensure compliance with stringent cybersecurity, risk management, and patient data protection standards

- Manufacturers must regularly update software, monitor vulnerabilities, and provide secure authentication protocols to build trust among healthcare providers

- In addition, the relatively high initial cost of AI and video-enabled laryngoscopes compared to traditional devices can deter adoption, particularly in smaller clinics or budget-constrained hospitals

- While prices are gradually decreasing, the perceived premium for technologically advanced devices can still hinder widespread adoption, especially where basic laryngoscopy suffices

- Overcoming these challenges through robust cybersecurity measures, regulatory compliance, and the development of cost-effective AI-enabled laryngoscopes is vital for sustained market growth

Europe Laryngoscopes Market Scope

The market is segmented on the basis of type, visualization system, accessories, application, and end user.

- By Type

On the basis of type, the Europe laryngoscopes market is segmented into flexible and rigid laryngoscopes. Rigid laryngoscopes dominated the market in 2024 with a market share of 52.8%, driven by their stability, precision, and widespread adoption in surgical and critical care settings. They are preferred for procedures requiring direct airway visualization, ensuring high patient safety and procedural accuracy. Technological advancements, including LED illumination, fiber-optic integration, and ergonomic designs, further strengthen their dominance. Hospitals and surgical centers favor reusable and durable rigid laryngoscopes for long-term cost-effectiveness. The increasing prevalence of complex surgeries and high-risk procedures across Europe contributes to sustained demand. Continuous professional training and awareness programs among clinicians also promote reliance on rigid devices in clinical practice.

The flexible laryngoscopes segment is anticipated to witness the fastest growth from 2025 to 2032, fueled by innovations in imaging, maneuverability, and integration with video systems. They are particularly effective in managing difficult airways, pediatric cases, and patients with anatomical variations. The rising demand for minimally invasive procedures, combined with the versatility of flexible laryngoscopes across emergency, ICU, and surgical settings, accelerates adoption. Portability and patient comfort further support rapid growth. Technological improvements in visualization, recording, and workflow integration also enhance their appeal. Professional training programs and growing adoption in specialty clinics contribute to the segment’s rapid expansion.

- By Visualization System

On the basis of visualization system, the market is segmented into video laryngoscopes, standard laryngoscopes, and fiber laryngoscopes. The video laryngoscopes segment dominated the market in 2024, owing to its superior imaging capabilities, high success rate in intubation procedures, and the ability to record and review procedures for training purposes. Hospitals and surgical centers prefer video laryngoscopes for difficult airway management, enhancing patient safety and procedural efficiency. Integration with digital platforms allows real-time data sharing and workflow optimization. The growing emphasis on evidence-based healthcare practices drives the continued adoption of video laryngoscopes. Furthermore, ongoing technological advancements and software updates increase procedural accuracy. The ability to train medical staff efficiently with video feedback also strengthens their market position.

The fiber laryngoscopes segment is expected to witness the fastest growth from 2025 to 2032, driven by their flexibility, compact design, and portability for use in emergency and ICU settings. They are particularly effective in navigating complex airway anatomies and pediatric patients. Advancements in fiber-optic technology have improved the imaging quality, durability, and ease of maintenance of these devices. The rise of minimally invasive procedures, along with professional training programs promoting fiber-laryngoscope skills, accelerates market growth. Increasing demand for precision airway management in outpatient and specialty clinics contributes to rapid adoption. In addition, lower risk of complications and improved patient comfort enhance acceptance.

- By Accessories

On the basis of accessories, the market is segmented into handles, blades, fiber bundles, shell and caps, sets and kits, cytology brushes, bulbs, battery holders, bags, and others. The blades segment dominated the market in 2024, as they are essential for airway access and visualization. The availability of pediatric and adult blades, disposable options to reduce infection risk, and advanced ergonomic designs support widespread adoption. Blade versatility across different clinical scenarios, along with integration with modern laryngoscopes, reinforces their position as the leading accessory. Hospitals and surgical centers prioritize high-quality blades to ensure procedural accuracy and patient safety. Moreover, the long lifespan and reusability of premium blades contribute to their dominance in the market.

The LED handles segment is anticipated to witness the fastest growth from 2025 to 2032, driven by energy-efficient lighting, improved visibility, ergonomic designs, and integration with rechargeable batteries. Hospitals and surgical centers increasingly prefer LED handles to enhance procedural accuracy and reduce operator fatigue. Sustainable and cost-effective designs further accelerate adoption. Growing demand for improved illumination and consistency in complex surgeries supports the segment’s growth. The trend toward environmentally friendly and low-maintenance devices is also encouraging usage. In addition, the enhanced portability of LED handles makes them suitable for emergency and outpatient settings.

- By Application

On the basis of application, the market is segmented into diagnostic and surgical uses. The surgical segment dominated the market in 2024, as airway management is critical in various surgical interventions under general anesthesia. Advanced laryngoscopes with video integration and AI-assisted guidance improve procedural precision and patient safety. Hospitals and surgical centers remain the primary end-users, driven by complex procedures and the need for minimally invasive techniques. Increasing healthcare infrastructure investments and training initiatives also support the dominance of the surgical segment. The growing frequency of elective and emergency surgeries in Europe drives demand further. Technological advancements in imaging, illumination, and ergonomics reinforce this trend.

The diagnostic segment is expected to witness the fastest growth from 2025 to 2032, fueled by the use of laryngoscopes in outpatient clinics, specialty centers, and ENT diagnostic procedures. High-definition imaging, portability, and ease of use improve early detection of laryngeal disorders. Rising awareness of voice-related health issues and preventive care drives demand. Integration with video and recording systems enhances clinical documentation and patient evaluation. Increasing adoption in ambulatory care settings and smaller hospitals contributes to rapid growth. Professional training programs also encourage clinicians to use diagnostic laryngoscopes more frequently.

- By End User

On the basis of end user, the market is segmented into hospitals, specialty clinics, ambulatory centers, surgical centers, and others. The hospitals segment dominated the market in 2024, driven by the need for airway management across multiple departments including anesthesiology, emergency medicine, and intensive care. Hospitals invest in advanced and durable laryngoscopic equipment, including video and fiber-optic systems, to ensure procedural efficiency and patient safety. Integration with hospital information systems allows streamlined workflow and enhanced patient outcomes. Hospitals’ ability to fund high-cost equipment and preference for reusable devices further strengthens dominance. Large-scale surgical procedures and critical care requirements maintain consistent demand. Continuous professional training in hospitals promotes adoption of advanced devices.

The ambulatory surgical centers (ASCs) segment is anticipated to witness the fastest growth from 2025 to 2032, fueled by the rising preference for outpatient procedures that offer cost efficiency and patient convenience. Portable, single-use, and battery-operated laryngoscopes meet ASC operational needs, enabling rapid procedure turnover. Increasing procedural volumes and emphasis on patient satisfaction drive rapid adoption of advanced laryngoscopes. Investments in modern ASC infrastructure and staff training further support growth. Technological advancements such as wireless and AI-assisted laryngoscopes are rapidly deployed in ASCs. The expansion of ASCs across Europe and rising outpatient surgeries accelerate segment growth.

Europe Laryngoscopes Market Regional Analysis

- Germany dominated the Europe laryngoscopes market with the largest revenue share of 29% in 2024, characterized by a strong healthcare infrastructure, high adoption of advanced medical devices, and a strong presence of key industry players, while France and other Western European countries also contributed significantly to market growth

- Healthcare providers in Germany prioritize precision, patient safety, and the integration of advanced airway management tools such as video and fiber-optic laryngoscopes. Clinicians value features such as enhanced visualization, AI-assisted guidance, and ergonomic designs that improve procedural efficiency

- This widespread adoption is further supported by a technologically skilled workforce, high healthcare expenditure, and growing awareness of minimally invasive procedures, establishing advanced laryngoscopes as a standard solution in hospitals, specialty clinics, and ambulatory surgical centers across Germany

U.K. Laryngoscopes Market Insight

The U.K. laryngoscopes market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by the increasing focus on patient safety, minimally invasive procedures, and enhanced airway management in hospitals and specialty clinics. The rise in elective surgeries and ENT diagnostic procedures encourages the adoption of video and flexible laryngoscopes. In addition, the country’s well-developed healthcare infrastructure and awareness of advanced medical technologies stimulate market growth. The integration of modern laryngoscopes with hospital digital systems improves procedural efficiency and workflow management. Demand is further supported by training programs for medical professionals and government-led healthcare quality initiatives. The emphasis on modernizing hospital equipment for patient safety is also contributing to adoption.

France Laryngoscopes Market Insight

The France laryngoscopes market is expected to grow steadily during the forecast period, driven by the modernization of healthcare facilities and growing adoption of minimally invasive surgical techniques. Hospitals and surgical centers are increasingly investing in video and fiber-optic laryngoscopes to enhance procedural accuracy and patient outcomes. The prevalence of respiratory disorders and airway management challenges supports demand for advanced laryngoscopes. Training programs and professional awareness campaigns for anesthesiologists and ENT specialists further promote adoption. Integration with digital health systems and real-time imaging enhances efficiency and procedural documentation. Moreover, government policies supporting healthcare infrastructure upgrades provide additional momentum to the market.

Italy Laryngoscopes Market Insight

The Italy laryngoscopes market is projected to witness considerable growth during the forecast period, fueled by the rising demand for advanced airway management in hospitals, specialty clinics, and ambulatory surgical centers. The adoption of video and fiber-optic laryngoscopes is driven by increasing surgical volumes, focus on patient safety, and minimally invasive procedures. Italian healthcare providers are upgrading traditional devices to improve visualization, procedural efficiency, and diagnostic accuracy. Awareness programs and medical training further facilitate adoption. Government initiatives aimed at improving hospital infrastructure also support market expansion. Technological innovations, such as ergonomic designs and AI-assisted visualization, are contributing to the growth of the Italian market.

Europe Laryngoscopes Market Share

The Europe Laryngoscopes industry is primarily led by well-established companies, including:

- Verathon Inc. (U.S.)

- Ambu A/S (Denmark)

- Olympus Corporation (Japan)

- Hill-Rom Company, Inc. (U.S.)

- Friedrich-Alexander-Universität Erlangen-Nürnberg (Germany)

- KARL STORZ SE & Co. KG (Germany)

- Medtronic (Ireland)

- Smith & Nephew (U.K.)

- Stryker (U.S.)

- ConvaTec Group plc (U.K.)

- Johnson & Johnson Services, Inc. (U.S.)

- GE Healthcare (U.K.)

- Koninklijke Philips N.V., (Netherlands)

- Siemens Healthineers AG (Germany)

- FUJIFILM Holdings Corporation (Japan)

- CANON MEDICAL SYSTEMS CORPORATION (Japan)

- Hologic, Inc. (U.S.)

- Medline Industries, Inc. (U.S.)

- 3M (U.S.)

- Evident Scientific (Japan)

What are the Recent Developments in Europe Laryngoscopes Market?

- In August 2025, computer scientists at FAU Erlangen-Nürnberg developed a tool for automatically analyzing results of barium swallow tests, receiving €390,000 in funding for their project. This development aims to enhance diagnostic capabilities in swallowing disorders, potentially impacting laryngoscopic procedures

- In April 2025, KARL STORZ announced the global launch of the Slimline C-MAC® S, a single-use video laryngoscope designed for airway management. Engineered to meet the company’s high-quality standards, the Slimline C-MAC S blade offers clear visualization to support confident intubation, even in difficult scenarios. This launch underscores KARL STORZ's commitment to advancing airway management solutions

- In April 2025, Verathon expanded its GlideScope Spectrum QC line by introducing four new single-use video laryngoscopes tailored for neonatal and pediatric patients. The new blades—Miller 00, Miller 2, Mac 1, and Mac 2 are designed to meet the unique needs of younger patients, supporting better intubation outcomes and aligning with evolving guidelines that endorse video laryngoscopy for neonatal resuscitation

- In September 2023, Verathon introduced the GlideScope Go 2, a next-generation handheld video laryngoscope designed for urgent and critical situations. This device offers high-resolution imaging and a compact form factor, enhancing airway management in emergency settings

- In September 2023, Olympus launched the E-SteriScope, a single-use flexible video rhinolaryngoscope for diagnostic and therapeutic ENT procedures. The device offers portability and efficiency, aiming to improve procedural workflows and reduce cross-contamination risks

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.