Europe Magnetic Resonance Imaging Devices Market

Market Size in USD Billion

USD

3.04 Billion

USD

4.12 Billion

2024

2032

USD

3.04 Billion

USD

4.12 Billion

2024

2032

| 2025 - 2032 | |

| USD 3.04 Billion | |

| USD 4.12 Billion | |

| % | |

|

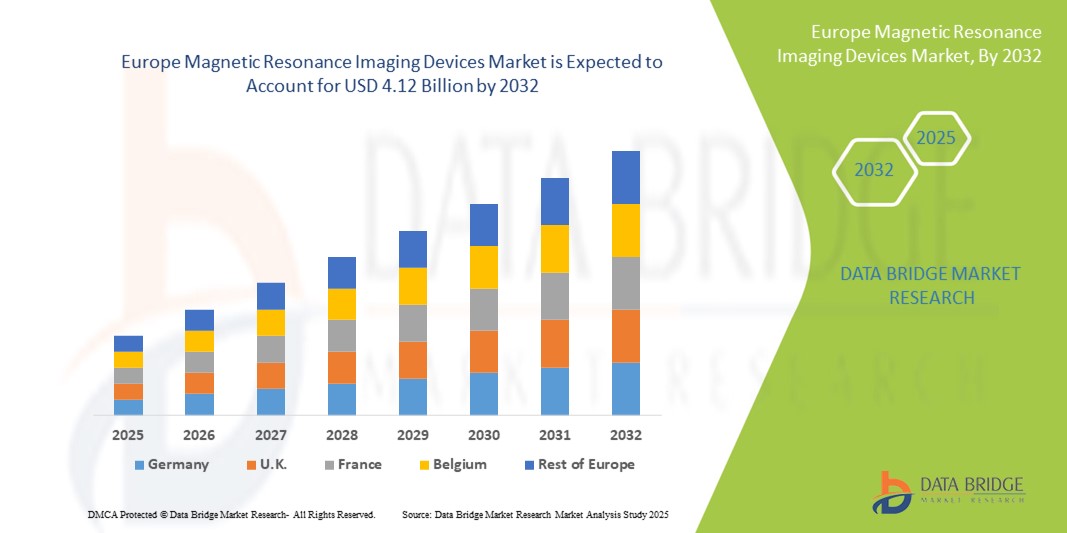

Europe Magnetic Resonance Imaging Devices Market Size

- The Europe magnetic resonance imaging devices market size was valued at USD 3.04 billion in 2024 and is expected to reach USD 4.12 billion by 2032, at a CAGR of 3.90% during the forecast period

- The market growth is largely fueled by the increasing prevalence of chronic diseases, an aging population, and technological advancements in imaging systems, leading to enhanced diagnostic capabilities and improved patient outcomes

- Furthermore, supportive healthcare policies, rising demand for early and accurate diagnosis, and growing adoption of advanced MRI systems in hospitals and diagnostic centers are establishing MRI devices as a critical tool in modern healthcare. These converging factors are accelerating the uptake of MRI solutions, thereby significantly boosting the industry's growth

Europe Magnetic Resonance Imaging Devices Market Analysis

- MRI devices, providing non-invasive imaging for detailed visualization of internal organs and tissues, are increasingly vital components of modern diagnostic and clinical workflows in both hospitals and diagnostic centers due to their accuracy, safety, and ability to detect a wide range of medical conditions

- The escalating demand for MRI devices is primarily fueled by the rising prevalence of chronic diseases, an aging population, and technological advancements in imaging systems, including hybrid and high-resolution MRI scanners

- Germany dominated the Europe magnetic resonance imaging devices market with the largest revenue share of 55% in 2024, characterized by advanced healthcare infrastructure, high adoption of cutting-edge technologies, and a strong presence of key industry players, with the country experiencing substantial growth in MRI installations driven by innovations in faster imaging techniques and improved patient comfort

- The U.K. is expected to be the fastest-growing country in the Europe magnetic resonance imaging devices market in Europe during the forecast period due to increasing healthcare expenditure, expanding diagnostic facilities, and government initiatives to enhance early disease detection

- Conventional MRI systems dominated the Europe magnetic resonance imaging devices market with a market share of 60.2% in 2024, driven by their widespread use across oncology, neurology, cardiology, and musculoskeletal applications, and their established reliability in routine diagnostic imaging

Report Scope and Europe Magnetic Resonance Imaging Devices Market Segmentation

|

Attributes |

Europe Magnetic Resonance Imaging Devices Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Europe

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Europe Magnetic Resonance Imaging Devices Market Trends

Advancements in AI-Enhanced Imaging and Workflow Automation

- A significant and accelerating trend in the European MRI devices market is the integration of artificial intelligence (AI) into imaging systems, improving diagnostic accuracy, workflow efficiency, and patient throughput

- For instance, AI-powered MRI scanners can automatically segment tissues, highlight anomalies, and reduce scan times, assisting radiologists in faster and more precise diagnosis

- AI integration in MRI devices enables predictive analytics, image reconstruction, and optimization of scan protocols based on patient-specific factors, enhancing operational efficiency and reducing errors. Furthermore, some Siemens and Philips MRI systems utilize AI to improve image clarity and automatically detect abnormalities in real time

- The seamless integration of MRI systems with hospital information systems (HIS) and radiology information systems (RIS) allows centralized management of imaging workflows, patient records, and reporting, creating a more coordinated clinical environment

- This trend toward intelligent, automated, and interconnected imaging systems is reshaping expectations for diagnostic precision. Consequently, companies such as GE Healthcare are developing AI-enabled MRI devices with automated image analysis and enhanced workflow management capabilities

- The demand for MRI systems that offer AI-powered imaging and workflow integration is growing rapidly across hospitals and diagnostic centers, as healthcare providers increasingly prioritize efficiency, accuracy, and patient-centric care

Europe Magnetic Resonance Imaging Devices Market Dynamics

Driver

Rising Demand Due to Aging Population and Chronic Disease Prevalence

- The increasing prevalence of chronic diseases, coupled with the growing elderly population in Europe, is a significant driver for the heightened demand for MRI devices

- For instance, in 2024, the adoption of high-field MRI systems in German hospitals increased to support early detection of neurological and cardiovascular conditions, reflecting the rising need for advanced imaging solutions

- As the burden of cancer, cardiovascular disorders, and neurological diseases grows, MRI devices offer non-invasive, high-resolution imaging, providing a critical diagnostic advantage over other modalities

- Furthermore, government initiatives to expand healthcare coverage and improve diagnostic infrastructure are encouraging the installation of MRI devices across hospitals and diagnostic centers

- The combination of rising healthcare awareness, preventive diagnostics, and investment in imaging infrastructure is propelling the adoption of MRI systems in Europe, particularly in countries with well-developed healthcare facilities

Restraint/Challenge

High Equipment Cost and Complex Regulatory Compliance

- The substantial initial cost of MRI systems, along with the expenses associated with installation, maintenance, and training, poses a significant challenge to market expansion

- For instance, smaller diagnostic centers in Eastern Europe face budget constraints when procuring high-field MRI scanners, limiting widespread adoption

- Compliance with stringent regulatory standards and safety certifications across European countries adds complexity to product launches and operational approvals, potentially delaying market entry

- Furthermore, variations in reimbursement policies, budget allocations, and hospital procurement cycles can affect purchasing decisions, particularly for high-end MRI systems with advanced features

- Addressing these challenges through cost-effective solutions, modular MRI systems, and standardized regulatory processes will be essential for sustained market growth and broader adoption across diverse healthcare settings

Europe Magnetic Resonance Imaging Devices Market Scope

The market is segmented on the basis of type, process, field strength, modality, architecture, application, end user, and distribution channel.

- By Type

On the basis of type, the Europe magnetic resonance imaging devices market is segmented into conventional and bio-based MRI systems. The conventional MRI segment dominated the market with the largest revenue share of 60.2% in 2024, owing to its widespread adoption across hospitals and diagnostic centers. Conventional systems are preferred for their proven reliability, high-quality imaging for various clinical applications such as oncology and neurology, and compatibility with existing hospital infrastructure. They provide consistent image resolution, support multiple examination types, and are backed by established service networks. Hospitals benefit from standardized workflows and broad clinician familiarity, which reinforce market dominance. The availability of replacement parts and maintenance services further strengthens their position.

The bio-based MRI segment is anticipated to witness the fastest growth during the forecast period, driven by increasing research in contrast agents and biologically enhanced imaging techniques. These systems provide improved tissue characterization, functional imaging capabilities, and advanced diagnostic features for early disease detection. Research hospitals and academic centers are increasingly adopting bio-based MRI for precision medicine initiatives. Innovations in molecular imaging and targeted diagnostics are accelerating demand. The growing emphasis on personalized healthcare and patient-specific imaging supports rapid adoption.

- By Field Strength

On the basis of field strength, the Europe magnetic resonance imaging devices market is segmented into low-to-mid-field (<1.5T), high-field (1.5T to 3T), and very-high-field (4T and above) MRI systems. High-field MRI systems dominated the market in 2024 due to their optimal balance of image resolution, scan speed, and patient comfort. Hospitals widely prefer 1.5T–3T systems for routine imaging in neurology, cardiology, and musculoskeletal applications. They offer reproducible diagnostic results and are supported by extensive clinical data. The versatility of high-field systems allows integration into multi-departmental imaging workflows. Strong manufacturer support and widespread clinician familiarity reinforce their adoption.

Very-high-field MRI systems are expected to witness the fastest growth from 2025 to 2032, driven by their enhanced imaging capabilities for research, advanced neurology, and oncology applications. These systems provide ultra-high-resolution imaging, advanced spectroscopy, and superior tissue contrast for early detection. Research hospitals and academic centers are key adopters of very-high-field systems. The growing focus on functional and molecular imaging is boosting demand. Increasing investments in advanced imaging infrastructure further support this segment’s growth.

- By Modality

On the basis of modality, the Europe magnetic resonance imaging devices market is segmented into stationary, portable/mobile, and point-of-care (POC) systems. The stationary MRI segment dominated the market in 2024 due to robust imaging capabilities and suitability for high-volume hospitals. These systems handle a wide range of patient examinations and support multiple clinical specialties. They offer high reliability, standardized workflows, and consistent image quality. Large hospitals and diagnostic centers favor stationary systems for their capacity and advanced functionalities. Integration with hospital information systems enhances operational efficiency and patient management.

Portable/mobile MRI systems are expected to witness the fastest growth during the forecast period, driven by demand for decentralized imaging solutions in ambulatory centers, emergency care, and remote locations. Portable MRI allows rapid bedside diagnostics and reduced infrastructure costs. They provide flexible deployment for smaller hospitals and outpatient clinics. Advances in compact magnet design and software improvements enhance image quality. Point-of-care imaging is expanding in community hospitals, supporting segment growth.

- By Architecture

On the basis of architecture, the Europe magnetic resonance imaging devices market is segmented into closed, standard bore, wide-bore, and open MRI systems. Closed MRI systems dominated the market in 2024 due to superior magnetic field homogeneity and higher resolution imaging. Hospitals prefer closed systems for oncology, neurology, and musculoskeletal imaging due to precise and reproducible results. They are widely adopted in high-volume clinical settings. The robust performance and extensive clinical validation reinforce market leadership. Closed systems support complex imaging protocols and advanced applications. Established service networks and clinician familiarity further drive adoption.

Open MRI systems are anticipated to witness the fastest growth during the forecast period, driven by patient comfort, reduced claustrophobia, and suitability for pediatric and bariatric patients. Outpatient centers and hospitals increasingly adopt open MRI to improve patient experience. Technological advancements in magnet design and image quality enhance their capabilities. Open systems facilitate flexible positioning and easier accessibility. Rising awareness of patient-centric care supports adoption in both hospitals and diagnostic centers.

- By Application

On the basis of application, the Europe magnetic resonance imaging devices market is segmented into oncology, neurology, cardiology, gastroenterology, musculoskeletal, mammography, pelvic and abdominal, gynecology, urology, dental, and other applications. The oncology segment dominated the market in 2024 due to MRI’s critical role in tumor detection, treatment planning, and therapy monitoring. Cancer centers and hospitals rely on MRI for early detection and precise imaging. The versatility of MRI across multiple tumor types reinforces its leadership. Integration with treatment planning software enhances clinical workflows. Availability of high-field MRI systems supports advanced oncology applications. Clinical research also drives adoption in oncology-focused institutions.

The neurology segment is expected to witness the fastest growth during forecast period, driven by rising prevalence of neurological disorders such as Alzheimer’s, Parkinson’s, and stroke. Advanced MRI techniques such as functional MRI and diffusion tensor imaging are increasingly utilized for early detection and mapping. Hospitals and research centers adopt neurology-focused MRI solutions to improve patient outcomes. The demand for early intervention and precise diagnostics fuels segment growth. Technological advancements in high-resolution imaging further accelerate adoption. Increasing government and private investments in neurological healthcare infrastructure support expansion.

- By End User

On the basis of end users, the Europe magnetic resonance imaging devices market is segmented into hospitals, imaging centers, ambulatory surgical centers, and others. Hospitals dominated the market in 2024 due to large-scale imaging infrastructure, multi-specialty departments, and capacity to invest in high-end MRI systems. Hospitals require comprehensive diagnostic imaging for oncology, cardiology, neurology, and orthopedics. The ability to perform high patient volumes reinforces market dominance. Established maintenance and service networks support sustained adoption. Multi-departmental integration enhances workflow efficiency. Hospitals’ preference for high-field and closed MRI systems drives revenue share.

Imaging centers are expected to witness the fastest growth from 2025 to 2032, fueled by the increasing number of outpatient diagnostic facilities. Smaller centers seek cost-effective, accessible MRI solutions to meet local demand. Adoption of portable and mid-field MRI systems facilitates market penetration. Expanding private imaging chains contribute to rapid segment growth. Flexible financing and leasing models support procurement by imaging centers. Advanced software and AI integration enhance clinical capabilities.

- By Distribution Channel

On the basis of distribution channel, the Europe magnetic resonance imaging devices market is segmented into direct tender and retail sales. The direct tender segment dominated the market in 2024 due to bulk procurement by hospitals, government projects, and large diagnostic chains. Long-term service contracts and maintenance support are typically included in tender agreements. Hospitals prefer direct tender to secure favorable pricing and comprehensive service. Large-scale buyers benefit from volume discounts and vendor support. Direct procurement ensures timely delivery and regulatory compliance. The segment is reinforced by established manufacturer relationships.

Retail sales are expected to witness the fastest growth during forecast period, driven by smaller clinics, imaging centers, and specialty hospitals procuring MRI devices independently. Financing options, leasing models, and online procurement platforms support adoption. Retail channels enable faster deployment of mid- and low-field MRI systems. Demand from outpatient and community healthcare facilities fuels growth. Retail sales provide flexibility in model selection and feature customization. Increasing awareness and accessibility of MRI technology further drive adoption in this segment.

Europe Magnetic Resonance Imaging Devices Market Regional Analysis

- Germany dominated the Europe magnetic resonance imaging devices market with the largest revenue share of 55% in 2024, characterized by advanced healthcare infrastructure, high adoption of cutting-edge technologies, and a strong presence of key industry players, with the country experiencing substantial growth in MRI installations driven by innovations in faster imaging techniques and improved patient comfort

- Healthcare providers in the region highly value the accuracy, reliability, and versatility offered by MRI devices for applications in oncology, neurology, cardiology, and musculoskeletal imaging

- This widespread adoption is further supported by government healthcare initiatives, strong research and development activities, and the presence of leading MRI device manufacturers, establishing MRI systems as a critical diagnostic tool across hospitals, imaging centers, and research facilities

The Germany MRI Devices Market Insight

The Germany magnetic resonance imaging devices market dominated the market with the largest revenue share of 55% in 2024, driven by advanced healthcare infrastructure, high adoption of cutting-edge imaging technologies, and increasing demand for diagnostic procedures across hospitals and specialty centers. Healthcare providers highly value MRI systems for oncology, neurology, cardiology, and musculoskeletal applications due to their accuracy, reliability, and versatility. Government initiatives, strong R&D activities, and the presence of leading MRI manufacturers further propel adoption. Integration with hospital information systems and advanced imaging software enhances workflow efficiency. Hospitals prioritize high-field and very-high-field MRI systems for both routine diagnostics and research purposes. The combination of technological innovation, clinician familiarity, and patient-centric solutions reinforces Germany’s market dominance.

U.K. MRI Devices Market Insight

The U.K. magnetic resonance imaging devices market is expected to grow at fastest rate during the forecast period, driven by rising demand for advanced imaging and increasing cases of neurological, oncological, and musculoskeletal disorders. Hospitals and imaging centers are investing in high-field and open MRI systems to enhance diagnostic accuracy. Government initiatives promoting modern medical imaging and patient-centric care support market expansion. Integration with PACS and hospital information systems improves operational efficiency. The adoption of AI-enabled MRI solutions is increasing in research and specialty hospitals. Expansion of outpatient imaging facilities further fuels growth.

France MRI Devices Market Insight

The France magnetic resonance imaging devices market is projected to grow at a moderate CAGR during the forecast period, driven by increasing healthcare expenditure and rising demand for early and precise diagnostics. Hospitals and diagnostic centers are modernizing MRI infrastructure to manage oncology, neurology, and musculoskeletal cases effectively. Government programs to improve access to advanced imaging technologies contribute to market growth. Integration with digital health records enhances workflow and patient management. Research hospitals and academic centers are adopting high-resolution and hybrid MRI systems. The emphasis on non-invasive, accurate imaging drives adoption in both public and private healthcare facilities.

Italy MRI Devices Market Insight

The Italy magnetic resonance imaging devices market is expected to witness steady growth, fueled by rising prevalence of chronic and lifestyle-related diseases and increasing investment in healthcare infrastructure. Hospitals are upgrading to high-field and open MRI systems for comprehensive diagnostic capabilities. Government initiatives supporting early diagnostics and modern imaging technologies aid market expansion. Integration with hospital networks and digital imaging platforms improves efficiency. The growing number of specialty imaging centers encourages MRI adoption. Patient awareness and preference for non-invasive diagnostic solutions further drive market growth.

Europe Magnetic Resonance Imaging Devices Market Share

The Europe magnetic resonance imaging devices industry is primarily led by well-established companies, including:

- Siemens Healthineers AG (Germany)

- Koninklijke Philips N.V. (Netherlands)

- GE HealthCare (U.S.)

- CANON MEDICAL SYSTEMS CORPORATION (Japan)

- Hitachi, Ltd. (Japan)

- FUJIFILM Corporation (Japan)

- Esaote S.p.A. (Italy)

- Neusoft Corporation (China)

- Mindray Bio-Medical Electronics Co., Ltd. (China)

- Samsung Medison Co., Ltd. (South Korea)

- United Imaging Healthcare Co., Ltd. (China)

- Hologic, Inc. (U.S.)

- Carestream Health, Inc. (U.S.)

- Agfa-Gevaert Group (Belgium)

- Konica Minolta, Inc. (Japan)

- Medtronic (Ireland)

- Toshiba Medical Systems Corporation (Japan)

What are the Recent Developments in Europe Magnetic Resonance Imaging Devices Market?

- In June 2025, the European Union announced restrictions on imports of Chinese medical devices, including MRI equipment, in response to alleged discrimination against foreign suppliers in China's public procurement. This move aims to ensure fair competition and protect European manufacturers

- In May 2025, GE Healthcare unveiled the SIGNA Voyager Premier Edition, a 1.5T wide-bore MRI scanner, in the UK. This system is designed to provide exceptional image quality and patient-friendly exams, balancing comfort and productivity. The introduction of this system reflects GE Healthcare's dedication to advancing MRI technology

- In November 2024, The Paris Brain Institute's Neuro@7T project, supported by France's SESAME Filières France 2030 initiative, aims to develop a hub of expertise in ultra-high-field MRI neuroimaging. This project seeks to identify innovative diagnostic markers for neurological and psychiatric disorders, demonstrating France's

- In June 2024, Siemens Healthineers and Dentsply Sirona collaborated to develop the first dental-dedicated MRI system, the MAGNETOM Free.Max Dental Edition. This system aims to provide high-quality imaging tailored for dental applications, marking a significant advancement in specialized MRI technology

- In November 2022, Philips launched the Ingenia Ambition X, a 1.5T MRI system, in France. This system incorporates AI-based imaging and real-time workflow optimization to improve diagnostic accuracy and patient throughput

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.