Europe Medical Clothing Market

Market Size in USD Billion

USD

42.94 Billion

USD

80.67 Billion

2025

2033

USD

42.94 Billion

USD

80.67 Billion

2025

2033

| 2026 - 2033 | |

| USD 42.94 Billion | |

| USD 80.67 Billion | |

| % | |

|

Europe Medical Clothing Market Overview

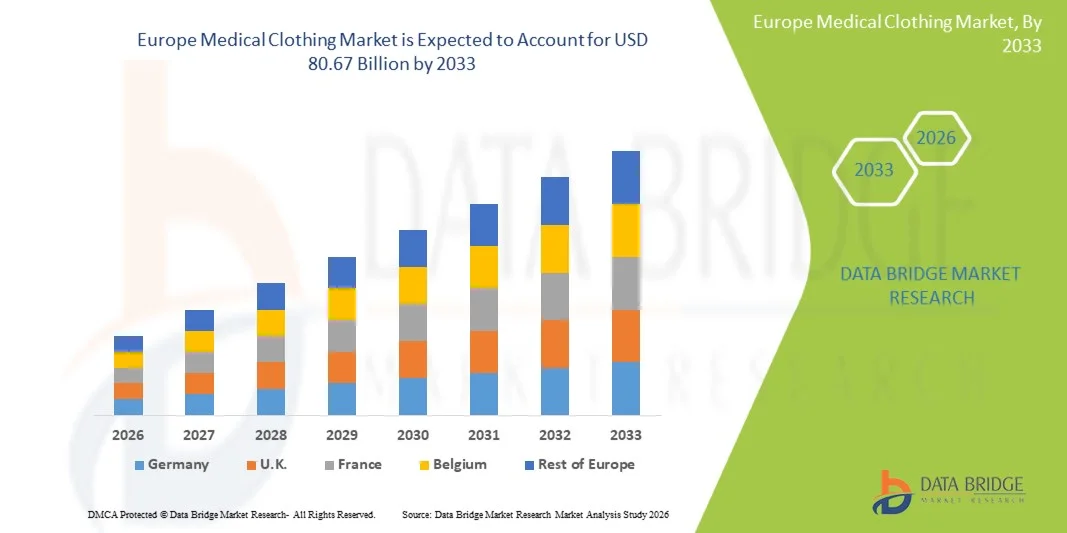

The Europe medical clothing market was valued at USD 42.94 billion in 2025 and is projected to reach USD 80.67 billion by 2033, growing at a CAGR of 8.20% from 2026 to 2033. Market growth is supported by increasing healthcare expenditures across European nations, rising emphasis on infection control and hospital hygiene protocols, and growing demand for high-quality protective apparel among healthcare professionals and patients.

The heightened awareness of hospital-acquired infections (HAIs) following the COVID-19 pandemic has accelerated adoption of medical clothing across hospitals, specialty clinics, and ambulatory care settings. According to the European Centre for Disease Prevention and Control (ECDC), approximately 8.9 million HAIs occur annually in European hospitals and long-term care facilities, driving stringent infection prevention measures and increased procurement of protective medical apparel. Ongoing regulatory developments, including the EU Medical Device Regulation (MDR), are catalyzing innovation and ensuring compliance with safety standards, which is crucial for market expansion.

Technological advancements in textile engineering, including antimicrobial fabrics, fluid-resistant coatings, and sustainable materials, are expanding the clinical applicability of medical clothing across diverse healthcare settings. In addition, the growing emphasis on sustainability and eco-friendly medical textiles is reshaping procurement strategies among European healthcare institutions. Collaborative efforts among manufacturers and healthcare providers are enhancing product offerings and market reach, positioning Europe as a key contributor to the global medical clothing industry.

Key Market Trends & Insights

- Germany dominated the Europe medical clothing market with the largest revenue share of 22.8% in 2025, supported by advanced healthcare infrastructure, high surgical volumes, and the presence of leading medical textile manufacturers.

- The U.K. is expected to be the fastest-growing country at a CAGR of 9.45% from 2026 to 2033, driven by expanding NHS infection control initiatives, growing private healthcare investments, and rising adoption of sustainable medical apparel.

- The Professional Apparel segment led the market with a 38.5% market share in 2025, reflecting strong demand for scrubs, lab coats, and surgical gowns among healthcare workers across European hospitals and clinics.

- The Specialty Apparel segment is anticipated to be the fastest-growing product category, driven by increasing prevalence of infectious diseases, expanding surgical procedure volumes, and technological advancements in protective fabric technologies.

- The Hospitals segment dominated the end-user category with a 45.2% market share in 2025, supported by high patient volumes, comprehensive infection control protocols, and centralized procurement of medical clothing.

- The Ambulatory Centres segment is expected to witness strong growth during the forecast period, driven by expanding outpatient surgical services, cost-effective care delivery models, and increasing adoption of disposable medical apparel.

Market Size & Forecast

- Europe Market Value (2025): USD 42.94 Billion

- Expected Market Value (2033): USD 80.67 Billion

- Forecast CAGR (2026–2033): 8.20%

Report Scope and Europe Medical Clothing Market Segmentation

|

Attributes |

Europe Medical Clothing Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe |

|

Key Market Players |

|

|

Market Opportunities |

· Expansion of sustainable and biodegradable medical textile production across European manufacturing facilities · Development of smart medical apparel integrating wearable sensors and antimicrobial technologies for enhanced infection control |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Europe Medical Clothing Market Trends

Trend: Sustainability and Eco-Friendly Medical Textiles Driving Innovation

The European medical clothing industry is witnessing a significant shift toward sustainable and eco-friendly materials as healthcare institutions prioritize environmental responsibility alongside infection control. Manufacturers are investing in recyclable, biodegradable, and organic cotton-based medical textiles to reduce the carbon footprint of hospital operations. The European Union's Green Deal and circular economy initiatives are accelerating adoption of sustainable procurement practices across public and private healthcare systems.

For instance,

Mölnlycke Health Care AB has expanded its portfolio of sustainable surgical drapes and gowns manufactured using recycled polyester and responsibly sourced materials, aligning with European healthcare institutions' sustainability targets and reducing environmental impact across the product lifecycle.

In addition, research demonstrates that adoption of reusable medical clothing systems in European hospitals reduces textile waste by up to 70% compared to single-use alternatives, supporting broader clinical adoption of sustainable medical apparel across general surgery, obstetrics, and critical care specialties. The growing emphasis on sustainability is expected to strengthen innovation and market competitiveness among European medical clothing manufacturers.

Europe Medical Clothing Market Dynamics

Key Market Driver: Rising Emphasis on Infection Prevention and Hospital Hygiene

The increasing focus on infection prevention and control within European healthcare settings is a primary driver of market growth. Medical clothing serves as a critical barrier against pathogen transmission, protecting healthcare workers and patients from hospital-acquired infections. Stringent regulatory frameworks, including the EU Medical Device Regulation and national infection control guidelines, are mandating higher standards for protective apparel quality and performance.

For instance,

A 2025 ECDC report highlighted that effective use of protective medical clothing, including gowns, masks, and gloves, reduced healthcare worker infection rates by 62% during respiratory disease outbreaks, demonstrating significant clinical advantages.

Rising regulatory pressure and awareness of infection risks are expected to strengthen adoption of medical clothing across European healthcare facilities.

Key Restraint/Challenge: Supply Chain Disruptions and Raw Material Cost Volatility

The European medical clothing market faces challenges related to supply chain disruptions and fluctuating raw material costs, particularly for specialized synthetic and antimicrobial fabrics. Dependence on imported raw materials and manufacturing components can lead to price volatility and procurement delays, affecting product availability and profit margins for manufacturers and healthcare institutions.

For instance,

European healthcare systems experienced significant supply shortages of disposable gowns and protective apparel during the COVID-19 pandemic, highlighting vulnerabilities in global supply chains and the need for regional manufacturing resilience.

Supply chain volatility may constrain market growth and increase procurement costs for budget-sensitive healthcare providers.

Key Market Opportunity: Integration of Smart Textiles and Wearable Technologies

The development of smart medical clothing integrating wearable sensors, antimicrobial nanotechnology, and real-time monitoring capabilities is creating opportunities for market differentiation and clinical innovation. European research institutions and medical textile manufacturers are collaborating to develop garments capable of tracking vital signs, detecting contamination, and alerting healthcare staff to infection risks.

For instance,

The smart clothing market is projected to experience exponential growth by 2030, with healthcare representing one of its strongest verticals.

European manufacturers are well-positioned to capitalize on this opportunity through investment in advanced textile engineering and digital health integration.

Europe Medical Clothing Market Scope

The Europe medical clothing market is segmented on the basis of product, usage, end user, and distribution channel.

By Product

On the basis of product, the Europe medical clothing market is segmented into professional apparel, patient apparel, specialty apparel, first aid clothing, wraps and towels, and others. The professional apparel segment dominated the market with a 38.5% market share in 2025, reflecting strong demand for scrubs, lab coats, surgical gowns, and medical uniforms among healthcare workers across European hospitals, specialty clinics, and ambulatory care centers. The increasing healthcare workforce, combined with stringent hygiene standards and growing emphasis on professional appearance, has driven consistent procurement of high-quality professional medical apparel. European healthcare institutions prioritize comfort, durability, and antimicrobial properties in professional clothing, contributing to segment leadership.

The specialty apparel segment is expected to witness the fastest growth from 2026 to 2033, driven by rising incidence of infectious diseases, expanding surgical procedure volumes, and technological advancements in protective fabric technologies. Specialty apparel includes isolation gowns, coveralls, and chemotherapy-resistant garments designed for high-risk clinical environments. Growing awareness of occupational hazards and regulatory mandates for enhanced protection are expanding the eligible user base and driving innovation in specialty medical textiles.

By Usage

On the basis of usage, the Europe medical clothing market is segmented into reusable and disposable. The disposable segment dominated the market with a 58.4% market share in 2025, driven by stringent infection control protocols, convenience of single-use garments, and reduced risk of cross-contamination in high-acuity clinical settings. Disposable medical clothing, including surgical gowns, masks, and drapes, is widely adopted in hospitals and ambulatory surgical centers for procedures requiring sterile environments. The COVID-19 pandemic significantly accelerated adoption of disposable medical apparel across European healthcare systems.

The reusable segment is expected to witness strong growth during the forecast period, driven by sustainability initiatives, cost-effectiveness over extended use cycles, and technological advancements in laundering and sterilization processes. European healthcare institutions are increasingly adopting reusable medical clothing systems to reduce textile waste and align with environmental sustainability targets. Innovations in durable antimicrobial fabrics are supporting broader adoption of reusable apparel in non-critical care settings.

By End User

On the basis of end user, the Europe medical clothing market is segmented into hospitals, specialty clinics, ambulatory centres, home care settings, research & clinical laboratories, and others. The Hospitals segment dominated the market with a 45.2% market share in 2025, driven by high patient volumes, comprehensive infection control protocols, and centralized procurement of medical clothing. Hospitals serve as primary centers for surgical procedures, critical care, and emergency services requiring extensive use of professional apparel, patient gowns, and specialty protective garments. The concentration of multidisciplinary medical teams and regulatory compliance requirements within hospital systems contributes to high procurement volumes and equipment utilization.

The Ambulatory Centres segment is expected to witness the fastest growth from 2026 to 2033, driven by expanding outpatient surgical services, cost-effective care delivery models, and increasing adoption of disposable medical apparel. The shift toward same-day discharge procedures and minimally invasive surgeries is increasing demand for medical clothing in ambulatory settings. Growing payer acceptance of outpatient procedures and favorable reimbursement policies are supporting segment expansion across European markets.

By Distribution Channel

On the basis of distribution channel, the Europe medical clothing market is segmented into direct tender, retail sales, third party distributor, and others. The direct tender segment dominated the market with a 42.6% market share in 2025, reflecting the preference of large hospital systems and public healthcare institutions for centralized procurement through competitive bidding processes. Direct tender arrangements enable bulk purchasing, cost optimization, and quality assurance compliance with institutional standards. Government-funded healthcare systems in Germany, France, and the United Kingdom rely heavily on direct tender processes for medical clothing procurement.

The retail sales segment is expected to witness strong growth during the forecast period, driven by expanding e-commerce platforms, increasing procurement by small and medium-sized healthcare facilities, and growing demand among individual healthcare professionals for personalized medical apparel. Online retailers are offering a wide range of products with easy access and significant discounts, thus appealing to a larger customer base and supporting segment expansion.

Europe Medical Clothing Market Regional Analysis

Europe represents a significant market for medical clothing, accounting for approximately 30% of the global market share in 2025. The region is experiencing growth driven by increasing healthcare expenditures, a rising elderly population, and a shift toward sustainable and eco-friendly medical textiles. Regulatory frameworks, such as the EU Medical Device Regulation, are catalyzing innovation and ensuring compliance with safety standards, which is crucial for market expansion.

Germany Medical Clothing Market Insight

The Germany medical clothing market dominated in the Europe with a revenue share of 22.8% in 2025, supported by advanced healthcare infrastructure, high surgical volumes, and the presence of leading medical textile manufacturers. The country's robust hospital network and strong emphasis on infection control have driven consistent demand for professional apparel, surgical drapes, and protective garments. Leading companies including PAUL HARTMANN AG and Mölnlycke Health Care AB maintain significant manufacturing and distribution operations within Germany, contributing to market leadership.

U.K. Medical Clothing Market Insight

The U.K. medical clothing market is expected to be the fastest-growing country at a CAGR of 9.45% from 2026 to 2033, driven by expanding NHS infection control initiatives, growing private healthcare investments, and rising adoption of sustainable medical apparel. Investment in medical clothing for surgical services, primary care, and community health settings is improving access to protective apparel and reducing infection transmission risks. The UK market is characterized by increasing collaboration between manufacturers and healthcare providers to enhance product offerings and procurement efficiency.

France Medical Clothing Market Insight

France represents a significant contributor to the Europe medical clothing market, driven by a well-developed public healthcare system, high surgical procedure volumes, and strong regulatory frameworks for medical textiles. French healthcare institutions are increasingly adopting sustainable medical apparel solutions aligned with national environmental objectives. The presence of leading international and domestic manufacturers supports product availability and market competitiveness.

Europe Medical Clothing Market Share

The Europe medical clothing industry is primarily led by well-established companies, including:

- Medline Industries, LP (U.S.)

- Cardinal Health, Inc. (U.S.)

- Mölnlycke Health Care AB (Sweden)

- PAUL HARTMANN AG (Germany)

- Halyard Health, Inc. (U.S.)

- ANSELL LTD. (Australia)

- 3M Company (U.S.)

- Kimberly-Clark Corporation (U.S.)

- Johnson & Johnson and its affiliates (U.S.)

- Superior Uniform Group, Inc. (U.S.)

- Barco Uniforms (U.S.)

- Landau Uniforms (U.S.)

Latest Developments in Europe Medical Clothing Market

- In March 2026, Mölnlycke Health Care AB announced the expansion of its sustainable surgical apparel production facility in Belgium, increasing manufacturing capacity for recyclable surgical gowns and drapes to meet growing European healthcare demand for eco-friendly medical textiles. The investment supports the company's commitment to reducing environmental impact across the product lifecycle.

- In January 2026, PAUL HARTMANN AG launched a new line of antimicrobial professional apparel designed for high-risk clinical environments, incorporating advanced silver-ion technology for enhanced infection protection. The product launch expands the company's portfolio of specialty medical clothing for European hospitals and ambulatory care centers.

- In November 2025, Cardinal Health, Inc. expanded its distribution partnership with major European hospital networks to improve supply chain resilience and ensure consistent availability of disposable medical apparel across critical care and surgical settings. The partnership addresses supply chain challenges experienced during recent public health emergencies.

- In September 2025, 3M Company introduced an advanced fluid-resistant surgical gown featuring breathable fabric technology and enhanced comfort for extended surgical procedures. The product launch supports the company's strategy to address healthcare worker demand for improved protective apparel performance.

- In June 2025, Medline Industries, LP announced a strategic collaboration with European healthcare sustainability initiatives to develop biodegradable patient apparel solutions aligned with circular economy principles. The collaboration demonstrates the company's commitment to environmental responsibility and innovation in medical textiles.

- In April 2025, Kimberly-Clark Corporation received CE marking approval for its next-generation surgical drapes incorporating enhanced barrier protection and reduced environmental impact. The regulatory milestone enables expanded distribution across European healthcare markets.

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.