Europe Medical Device Regulatory Affairs Outsourcing Market

Market Size in USD Billion

USD

8.31 Billion

USD

21.78 Billion

2025

2033

USD

8.31 Billion

USD

21.78 Billion

2025

2033

| 2026 - 2033 | |

| USD 8.31 Billion | |

| USD 21.78 Billion | |

| % | |

|

Europe Medical Device Regulatory Affairs Outsourcing Market Size

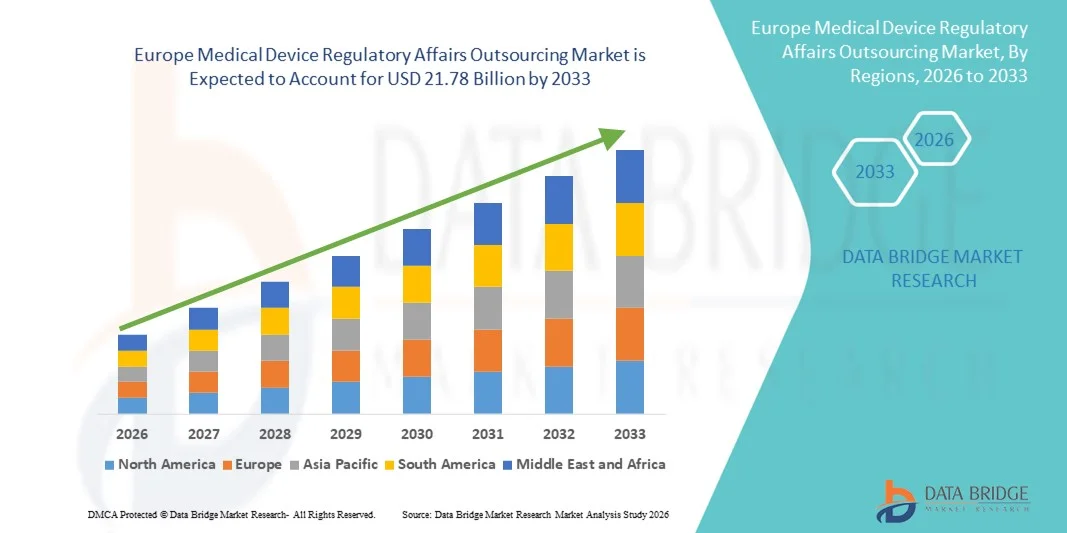

- The Europe Medical Device Regulatory Affairs Outsourcing market size was valued at USD 8.31 billion in 2025 and is expected to reach USD 21.78 billion by 2033, at a CAGR of 12.80% during the forecast period

- The market growth is largely fueled by the increasing complexity of regulatory requirements across the pharmaceutical, biotechnology, and medical device industries, prompting companies to seek specialized outsourcing services for compliance management

- Furthermore, rising demand for cost-effective, efficient, and timely regulatory submissions is driving the adoption of regulatory affairs outsourcing solutions. These converging factors are accelerating the uptake of Regulatory Affairs Outsourcing services, thereby significantly boosting the industry's growth globally

Europe Medical Device Regulatory Affairs Outsourcing Market Analysis

- Medical Device Regulatory Affairs Outsourcing market which involves delegating regulatory strategy, compliance documentation, product registration, and post-market surveillance activities to specialized service providers, is becoming increasingly important for medical device companies operating under complex and evolving regulatory frameworks across the Middle East

- The growing stringency of medical device regulations, increasing demand for faster approvals, and the need for localized regulatory expertise are key factors driving the adoption of Medical Device Regulatory Affairs Outsourcing services. Companies are leveraging outsourcing partners to minimize compliance risks, streamline approval timelines, and focus on core product development and commercialization activities

- The U.K. dominated the medical device regulatory affairs outsourcing market with the largest revenue share of approximately 38.7% in 2025, driven by a well-established healthcare and biopharmaceutical ecosystem, strong government support for medical device regulation, high procedure volumes, and the presence of leading regulatory consulting firms. The country’s emphasis on regulatory compliance and early adoption of advanced outsourcing services has significantly boosted demand for specialized regulatory affairs solutions

- Germany is expected to be the fastest-growing market, registering a CAGR of around 10.2% during the forecast period, supported by rising investments in advanced healthcare infrastructure, increasing presence of international medical device manufacturers, and evolving regulatory frameworks. Strong collaboration between industry and regulatory authorities, along with growing awareness of efficient outsourcing solutions, is further driving market growth in the country

- The Finished Goods segment held the largest market revenue share of 52.1% in 2025, as final medical devices are subjected to rigorous premarket approvals and post-market surveillance requirements

Report Scope and Medical Device Regulatory Affairs Outsourcing Market Segmentation

|

Attributes |

Medical Device Regulatory Affairs Outsourcing Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Europe

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Europe Medical Device Regulatory Affairs Outsourcing Market Trends

Increasing Complexity of Medical Device Regulations Across Regions

- A significant and accelerating trend in the Medical Device Regulatory Affairs Outsourcing market is the growing complexity and continual evolution of regulatory frameworks governing medical devices. Countries across the region are strengthening approval processes, post-market surveillance requirements, and compliance standards to align more closely with international benchmarks

- For instance, regulatory authorities in the Gulf Cooperation Council (GCC) countries and South Africa have introduced more structured medical device registration systems, prompting manufacturers to rely on specialized regulatory affairs outsourcing partners to navigate local submission procedures and documentation requirements efficiently

- The increasing adoption of international standards, such as ISO 13485 and risk-based classification systems, is driving demand for external expertise to manage regulatory filings, technical documentation, and quality compliance activities. Outsourcing partners provide region-specific knowledge that helps reduce approval timelines and regulatory risks

- In addition, the expansion of multinational medical device companies into Middle Eastern and African markets is encouraging the use of outsourced regulatory services to manage multi-country registrations through a centralized and cost-effective approach

- This trend toward professional regulatory support services is reshaping how manufacturers approach market entry and compliance, with outsourcing becoming a strategic necessity rather than an optional service across the region

- As regulatory scrutiny increases, demand for specialized regulatory affairs service providers with regional expertise continues to grow among both global and local medical device manufacturers

Europe Medical Device Regulatory Affairs Outsourcing Market Dynamics

Driver

Rising Medical Device Market Expansion and Regulatory Stringency

- The rapid expansion of the medical device sector across the globe, driven by increasing healthcare investments, population growth, and rising prevalence of chronic diseases, is a major driver for regulatory affairs outsourcing services

- For instance, growing healthcare infrastructure development in countries such as Saudi Arabia, the UAE, and South Africa has led to higher demand for medical devices, thereby increasing the regulatory workload for manufacturers seeking timely market approvals

- As regulatory authorities introduce more stringent compliance requirements, manufacturers are increasingly outsourcing regulatory activities to specialized firms to ensure accuracy, consistency, and faster product approvals

- Furthermore, small and mid-sized medical device companies often lack in-house regulatory expertise for diverse regional regulations, making outsourcing a practical solution to manage costs and reduce compliance risks

- The need to maintain regulatory compliance throughout the product lifecycle, including renewals, variations, and post-market surveillance, continues to support sustained demand for outsourcing services in the region

Restraint/Challenge

Limited Regulatory Harmonization and Shortage of Skilled Professionals

- A key challenge in the medical device regulatory affairs outsourcing market is the lack of harmonized regulatory frameworks across countries, which increases complexity and resource requirements for service providers and manufacturers alike

- For instance, varying submission formats, approval timelines, and regulatory expectations across African and Middle Eastern markets can lead to delays and increased operational costs, even when outsourcing regulatory activities

- Another significant restraint is the limited availability of highly skilled regulatory professionals with in-depth knowledge of both local regulations and international standards, particularly in emerging African markets

- In addition, concerns related to data confidentiality, communication gaps, and dependency on third-party service providers may cause some manufacturers to hesitate before fully outsourcing regulatory functions

- Overcoming these challenges through regulatory capacity building, regional harmonization initiatives, and investment in skilled workforce development will be critical for the long-term growth and effectiveness of the Medical Device Regulatory Affairs Outsourcing market in the Middle East and Africa

Europe Medical Device Regulatory Affairs Outsourcing Market Scope

The market is segmented on the basis of services, product, device type, application, and end user.

- By Services

On the basis of services, the Medical Device Regulatory Affairs Outsourcing market is segmented into Regulatory Affairs Services, Quality Consulting, and Medical Writing. The Regulatory Affairs Services segment dominated the largest market revenue share of 46.8% in 2025, due to the increasing complexity of medical device regulations across major regions such as North America, Europe, and Asia-Pacific. Companies rely on outsourced regulatory services for premarket submissions, technical documentation, and post-market compliance management. Growing regulatory requirements for Class II and Class III devices drive demand. Globalization of medical device operations and cross-border product registrations also fuel the segment. Regulatory affairs outsourcing reduces operational costs while ensuring compliance with FDA, EU MDR, and IVDR guidelines. The segment benefits from increasing regulatory audits and frequent updates in documentation standards. Lifecycle management of devices, vigilance reporting, and risk mitigation are critical drivers. Companies increasingly prioritize outsourcing to enhance speed-to-market while reducing internal resource burden. Rising adoption of advanced medical devices, and rapid product innovation, further support dominance. Expansion into emerging markets creates sustained demand for regulatory affairs services.

The Medical Writing segment is expected to witness the fastest CAGR of 11.4% from 2026 to 2033, driven by rising global demand for high-quality clinical evaluation reports, technical files, and regulatory documentation. Small and mid-sized medical device companies are increasingly dependent on outsourced medical writers. Regulatory authorities require precise and compliant documentation for device approvals, fueling growth. Adoption of electronic submission platforms accelerates outsourcing. Growth in clinical trials, real-world evidence collection, and post-market data reporting enhances demand. Digitalization and AI-assisted medical writing tools contribute to faster document preparation. Companies seek flexible outsourcing contracts to reduce internal workforce burden. Expansion of therapeutic areas, including cardiology, orthopedics, and IVD devices, further drives growth. Increasing international regulatory harmonization supports cross-border outsourcing needs. Overall, the segment benefits from rising regulatory complexity and the growing importance of accurate medical documentation.

- By Product

On the basis of product, the Medical Device Regulatory Affairs Outsourcing market is segmented into Finished Goods, Electronics, and Raw Material. The Finished Goods segment held the largest market revenue share of 52.1% in 2025, as final medical devices are subjected to rigorous premarket approvals and post-market surveillance requirements. Companies outsource regulatory processes to ensure smooth compliance with FDA, EU MDR, and other regional regulations. Finished goods include devices across cardiology, orthopedics, IVD, and ophthalmology. Outsourcing helps reduce internal workload while ensuring adherence to quality and safety standards. Manufacturers seek expert support for labeling, documentation, validation, and clinical evidence preparation. Increased scrutiny for combination products, software-integrated devices, and connected medical devices supports market dominance. The global expansion of medical device operations drives long-term outsourcing contracts. Outsourcing mitigates risks associated with audits and non-compliance penalties. Companies prioritize speed-to-market without compromising compliance. Post-market vigilance and adverse event reporting are additional drivers. Manufacturers aim to optimize resource allocation and cost-efficiency through outsourcing.

The Electronics segment is anticipated to witness the fastest CAGR of 10.7% from 2026 to 2033, due to the increasing integration of software and digital components in medical devices. Regulatory compliance for software, firmware, and connected device cybersecurity is complex and evolving. Outsourcing is preferred to ensure regulatory readiness and faster approvals. Growth in wearable devices, remote monitoring systems, and digital health solutions supports the segment. Startups and SMEs increasingly rely on expert regulatory partners for electronics-heavy devices. Adoption of AI and machine learning in medical devices increases documentation and testing requirements. Cross-border commercialization drives demand for standardized regulatory documentation. The trend of connected health solutions accelerates outsourcing of compliance activities. Companies aim to reduce internal operational burden while adhering to global regulatory standards. Expansion of telemedicine devices and IoT-enabled medical devices further supports growth.

- By Device Type

On the basis of device type, the Medical Device Regulatory Affairs Outsourcing market is segmented into Class I, Class II, and Class III devices. The Class II devices segment dominated the market with a revenue share of 41.6% in 2025, owing to a high volume of moderately regulated devices entering the market. Regulatory submissions for Class II devices involve documentation, technical files, and compliance with FDA 510(k) or CE marking guidelines. Outsourcing helps manufacturers streamline approvals and reduce internal workload. Orthopedic, diagnostic, and monitoring devices constitute a major part of Class II products. Companies leverage outsourced expertise to manage product lifecycle, post-market surveillance, and regulatory audits. Globalization of device operations and increasing innovation further drive demand. Cost reduction, efficiency, and timely market entry are key advantages. Regulatory complexity across multiple regions strengthens reliance on outsourcing. Lifecycle management activities, including device modifications, updates, and reporting, fuel the segment. Increasing adoption of medical devices in emerging markets contributes to dominance. Class II devices account for a balance of innovation and regulatory complexity, making outsourcing essential.

The Class III devices segment is projected to grow at the fastest CAGR of 12.8% from 2026 to 2033, driven by increasing development of implantable, life-supporting, and high-risk devices. These devices require extensive clinical evidence, validation studies, and regulatory approvals. Outsourcing regulatory affairs minimizes approval delays and ensures compliance with global standards. High-risk device scrutiny, including cardiac implants and neuromodulation devices, fuels market growth. Manufacturers rely on regulatory partners for documentation, clinical evaluation reports, and technical files. The growing trend of combination products increases outsourcing demand. Continuous post-market surveillance and adverse event reporting requirements further support expansion. Regulatory updates under MDR and IVDR enhance segment growth. Small and medium-sized companies increasingly outsource Class III device compliance due to complexity. Innovation in biocompatible materials and smart implants supports segment acceleration. The segment’s high-value products and regulatory risk drive sustained outsourcing demand.

- By Application

On the basis of application, the Medical Device Regulatory Affairs Outsourcing market is segmented into Cardiology, Diagnostic Imaging, Orthopedic, IVD, Ophthalmic, General and Plastic Surgery, Drug Delivery, Dental, Endoscopy, Diabetes Care, and Others. The IVD segment accounted for the largest market revenue share of 30.2% in 2025, driven by growing demand for diagnostic testing and personalized medicine. Outsourcing is critical due to stringent EU IVDR and FDA compliance requirements. Manufacturers depend on regulatory experts for device approvals, validation, labeling, and post-market surveillance. Expansion of diagnostic centers, clinical laboratories, and molecular diagnostic facilities supports growth. Increasing chronic disease prevalence boosts demand for accurate diagnostic devices. Companies aim to reduce operational costs and mitigate regulatory risks. Globalization of IVD device distribution further strengthens outsourcing requirements. Rapid product innovation requires timely regulatory support. Risk-based classification of IVDs drives reliance on outsourcing. Regulatory audits, CE marking, and FDA clearances increase market activity. The segment benefits from rising investments in early disease detection and precision medicine.

The Diabetes Care segment is expected to witness the fastest CAGR of 13.3% from 2026 to 2033, fueled by the global rise in diabetes prevalence and adoption of connected glucose monitoring systems. Regulatory requirements for continuous glucose monitors and smart insulin delivery devices are complex, increasing outsourcing demand. Startups and mid-sized manufacturers rely on expert partners for documentation, technical files, and compliance. AI-integrated diabetes management devices require additional regulatory support. Growth in wearable devices and home care solutions supports segment expansion. Cross-border market entry demands harmonized regulatory submissions. Digital therapeutics and telemedicine integration drive outsourcing further. Post-market vigilance and risk management are critical factors. Governments and healthcare providers’ focus on diabetes management strengthens the market. Increasing venture funding in digital diabetes solutions accelerates growth. Small-scale manufacturers benefit from reduced internal compliance costs. Regulatory knowledge gap among new companies promotes high outsourcing adoption.

- By End User

On the basis of end user, the Medical Device Regulatory Affairs Outsourcing market is segmented into Small Medical Device Company, Medium Medical Device Company, and Large Medical Device Company. The Large Medical Device Company segment dominated the market with a revenue share of 44.9% in 2025, due to large product portfolios and global operations. Outsourcing supports regulatory submissions across multiple countries and ensures compliance with varying standards. Frequent product launches and lifecycle management activities demand expert support. Companies leverage outsourcing to optimize resource allocation and reduce internal compliance burden. Large players face high regulatory scrutiny for Class II and III devices, enhancing segment growth. Post-market surveillance, clinical evaluations, and technical documentation are outsourced to specialized firms. Regulatory audits, CE marking, and FDA 510(k) approvals increase outsourcing adoption. Risk mitigation, cost efficiency, and faster market entry drive dominance. Expansion into emerging markets necessitates outsourcing expertise. Integration of software and connected devices further enhances demand. Outsourcing allows large companies to focus on R&D while ensuring regulatory compliance.

The Small Medical Device Company segment is anticipated to grow at the fastest CAGR of 13.1% from 2026 to 2033, driven by limited in-house regulatory expertise. Startups and early-stage companies rely heavily on outsourced services to meet global compliance requirements. Outsourcing helps reduce approval timelines and operational costs. Increasing innovation in wearable, diagnostic, and home care devices supports growth. Complex documentation, clinical evaluation, and post-market requirements make outsourcing essential. Venture-funded companies seek cost-effective regulatory solutions. Global market expansion demands expertise in regional regulations. Rapidly evolving MDR and IVDR requirements accelerate outsourcing adoption. AI-assisted regulatory tools support small companies in efficient documentation. Compliance risk mitigation is a major driver for segment growth. Startups leverage outsourcing for faster time-to-market and reduced internal workload. Increasing partnerships with CROs and regulatory consultants strengthen growth prospects.

Europe Medical Device Regulatory Affairs Outsourcing Market Regional Analysis

- The Europe medical device regulatory affairs outsourcing market is projected to grow steadily over the forecast period, supported by strengthening regulatory frameworks, rising medical device approvals, and expanding healthcare and biopharmaceutical infrastructure across the region

- Governments are increasingly emphasizing regulatory compliance, product registration, and post-market surveillance to ensure patient safety and quality standards. As a result, medical device manufacturers are outsourcing regulatory affairs activities to specialized service providers to navigate complex and evolving regulations efficiently

- Growing investments in advanced medical technologies, coupled with the rising presence of international medical device manufacturers, are further accelerating demand for regulatory affairs outsourcing services across Europe

U.K. Medical Device Regulatory Affairs Outsourcing Market Insight

The U.K. medical device regulatory affairs outsourcing market dominated Europe, accounting for approximately 38.7% of the revenue share in 2025. This dominance is primarily driven by a well-established healthcare and biopharmaceutical ecosystem, strong government support for medical device regulation, high procedure volumes, and the presence of leading regulatory consulting firms. The country’s early adoption of advanced outsourcing services, combined with strict regulatory compliance requirements, has significantly boosted demand for specialized regulatory affairs solutions.

Germany Medical Device Regulatory Affairs Outsourcing Market Insight

The Germany medical device regulatory affairs outsourcing market is expected to register the fastest growth in Europe, with a projected CAGR of around 10.2% during the forecast period. This growth is supported by rising investments in advanced healthcare infrastructure, increasing presence of international medical device manufacturers, and evolving regulatory frameworks. Strong collaboration between industry and regulatory authorities, along with growing awareness of efficient outsourcing solutions, is further driving market expansion in the country.

Europe Medical Device Regulatory Affairs Outsourcing Market Share

The Medical Device Regulatory Affairs Outsourcing industry is primarily led by well-established companies, including:

- Accell Clinical Research, LLC (U.S.)

- Genpact (U.S.)

- CRITERIUM, INC. (U.S.)

- Promedica International (U.S.)

- WuXiAppTec (China)

- Medpace (U.S.)

- PPD Inc. (U.S.)

- Charles River Laboratories (U.S.)

- ICON plc (U.S.)

- Covance (U.S.)

- Parexel International Corporation (U.S.)

- Freyr

- Navitas Clinical Research, Inc. (U.S.)

- Medelis, Inc. (U.S.)

- Sciformix (U.S.)

- Tech Tammina (U.S.)

- Acorn Regulatory Consultancy Services Ltd. (Ireland)

- BIOMAPAS (Lithuania)

- REGULATORY PROFESSIONALS (Australia)

- CompareNetworks, Inc. (U.S.)

Latest Developments in Europe Medical Device Regulatory Affairs Outsourcing Market

- In January 2023, Medistri SA, a Switzerland‑based medtech service provider, introduced an integrated regulatory affairs and quality management consulting solution tailored for small and mid‑sized medical device manufacturers. This offering simplified pathways to compliance by providing cost‑effective support for CE marking, technical file preparation, and post‑market surveillance, addressing a key need for companies lacking full in‑house regulatory teams

- In March 2023, ICON plc launched a new Regulatory Intelligence platform designed to assist medical device companies in tracking evolving global regulations, managing submission strategies, and accessing compliance templates. The platform was aimed at improving regulatory strategy and operational efficiency for complex multi‑jurisdictional filings

- In March 2023, Freyr Solutions opened a new global regulatory services hub in the Asia‑Pacific region, expanding its capacity to support medical device companies with end‑to‑end compliance for country‑specific approvals. This enhanced regional service offering highlighted the rapid growth of regulatory outsourcing demand in emerging markets

- In April 2023, Parexel International Corporation expanded its global regulatory consulting services to better support medical device and combination product developers grappling with the increasingly complex requirements under the EU Medical Device Regulation (MDR) and In Vitro Diagnostic Regulation (IVDR). This strategic enhancement reflected heightened industry demand for specialized MDR/IVDR expertise

- In March 2024, Emergo by UL established a new regulatory consulting center in Singapore focused on serving the growing Asia‑Pacific medical device market, particularly supporting ASEAN regulatory harmonization initiatives and multi‑country approvals. This move underscored strong geographic expansion in outsourced regulatory services

- In July 2024, Parexel International launched its Digital Regulatory Platform, integrating artificial intelligence and machine learning to streamline medical device regulatory submissions, provide cloud‑based document management, and improve collaboration between sponsors and regulators

- In September 2024, IQVIA expanded its regulatory affairs capabilities through the acquisition of Pharm‑Olam’s regulatory consulting division, bolstering its global medical device regulatory expertise and enhancing services across Asia‑Pacific and Latin America—especially for emerging market regulatory strategies

- In January 2025, ProPharma Group partnered with MedTech Europe to develop specialized regulatory training programs for medical device regulatory professionals, addressing critical skills gaps following implementation of more stringent regulatory frameworks such as MDR

- In February 2025, IQVIA announced a strategic partnership with a European medical device manufacturer to support regulatory dossier preparation and clinical evaluation reporting under EU MDR, reinforcing industry reliance on outsourced expertise for complex compliance documentation

- In March 2025, market insights indicated ICON plc expanded its regulatory affairs outsourcing services in the Asia‑Pacific region, responding to increasing localized demand for regulatory consultation and clinical trial support in high‑growth markets such as China and India

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.