Europe Medical Equipment Maintenance Market

Market Size in USD Billion

CAGR :

%

USD

73.22 Billion

USD

153.56 Billion

2025

2033

USD

73.22 Billion

USD

153.56 Billion

2025

2033

| 2026 –2033 | |

| USD 73.22 Billion | |

| USD 153.56 Billion | |

| % | |

|

Europe Medical Equipment Maintenance Market Size

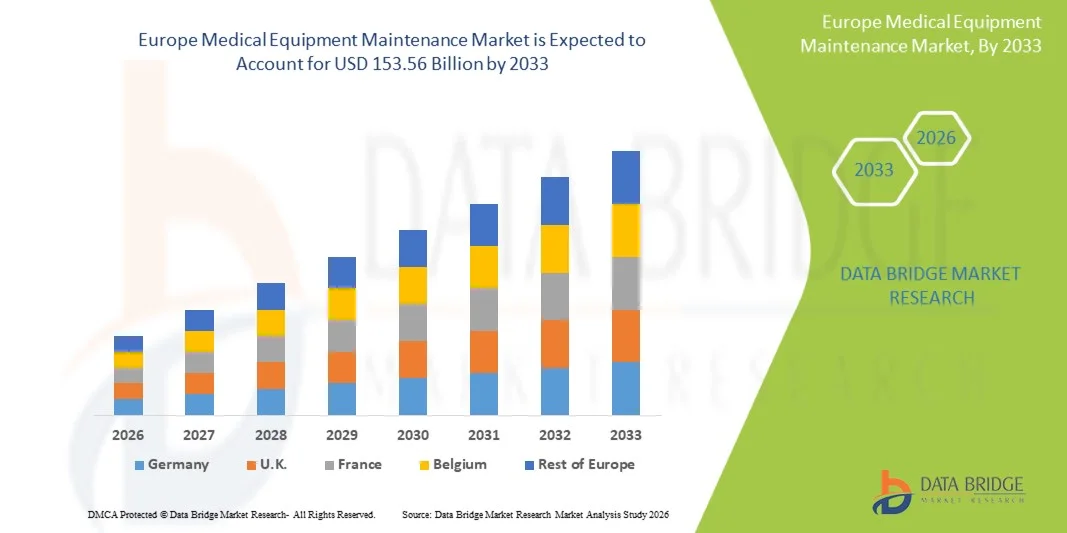

- The Europe medical equipment maintenance market size was valued at USD 73.22 billion in 2025 and is expected to reach USD 153.56 billion by 2033, at a CAGR of 9.70% during the forecast period

- The market growth is largely fueled by the increasing installation of advanced medical devices in hospitals and diagnostic centers, along with the rising need to ensure equipment reliability, regulatory compliance, and patient safety across healthcare facilities

- Furthermore, the growing emphasis on preventive maintenance services, equipment lifecycle management, and outsourcing of technical support by healthcare providers is establishing professional maintenance solutions as a critical component of modern healthcare infrastructure. These converging factors are accelerating the adoption of medical equipment maintenance services, thereby significantly boosting the industry's growth

Europe Medical Equipment Maintenance Market Analysis

- Medical equipment maintenance services, which include inspection, calibration, repair, and preventive servicing of diagnostic and therapeutic devices, are increasingly essential for healthcare systems across Europe to ensure operational efficiency, regulatory compliance, and patient safety in hospitals, laboratories, and specialty clinics

- The escalating demand for medical equipment maintenance is primarily fueled by the growing installation of technologically advanced medical devices, increasing pressure on healthcare providers to minimize equipment downtime, and the rising need to extend the operational lifespan of costly healthcare assets

- Germany dominated the Europe medical equipment maintenance market with the largest revenue share of 38.7% in 2025, characterized by its strong healthcare infrastructure, high medical device adoption rates, and the presence of leading medical technology companies, with hospitals and diagnostic centers increasingly outsourcing maintenance services to specialized providers to improve efficiency and reduce operational costs

- The United Kingdom is expected to be one of the fastest growing markets in the Europe medical equipment maintenance sector during the forecast period due to increasing investments in healthcare infrastructure, expanding diagnostic services, and the growing focus on preventive equipment servicing to maintain compliance with strict healthcare regulations

- Preventive segment dominated the Europe medical equipment maintenance market with a market share of 45.3% in 2025, driven by the increasing focus of healthcare facilities on routine inspection, early fault detection, and scheduled servicing to reduce equipment downtime and ensure uninterrupted operation of critical medical devices

Report Scope and Europe Medical Equipment Maintenance Market Segmentation

|

Attributes |

Europe Medical Equipment Maintenance Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Europe

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Europe Medical Equipment Maintenance Market Trends

“Adoption of IoT and Predictive Maintenance Technologies”

- A significant and accelerating trend in the Europe medical equipment maintenance market is the increasing adoption of IoT-enabled devices and predictive maintenance platforms, which allow continuous monitoring of equipment performance and early detection of potential malfunctions

- For instance, GE Healthcare’s IoT-enabled imaging systems provide real-time alerts for calibration and component wear, allowing hospitals to schedule maintenance proactively and minimize downtime

- Predictive analytics integration enables maintenance providers to optimize service schedules, reduce unexpected failures, and extend equipment lifespan, while also providing actionable insights on usage patterns and device efficiency

- The seamless integration of maintenance platforms with hospital information systems facilitates centralized tracking of multiple devices across departments, ensuring compliance with regulatory standards and enhancing operational efficiency

- The growing use of cloud-based maintenance solutions allows remote access to equipment data, enabling centralized monitoring and quicker response times for corrective actions

- Collaboration between device manufacturers and third-party maintenance providers is increasing, offering bundled solutions that include software updates, calibration, and on-site servicing, creating a more integrated service model

- This trend towards connected, data-driven, and predictive maintenance solutions is fundamentally transforming expectations for healthcare facility operations, driving providers to adopt smarter service models

- The demand for IoT-based predictive maintenance and AI-assisted monitoring is growing rapidly across hospitals, diagnostic labs, and specialty clinics, as healthcare administrators increasingly prioritize uninterrupted device functionality and cost-efficient servicing

Europe Medical Equipment Maintenance Market Dynamics

Driver

“Increasing Demand Due to Rising Equipment Complexity and Regulatory Standards”

- The growing complexity of medical devices, coupled with stringent regulatory requirements for operational reliability and patient safety, is a key driver for the increased demand for professional equipment maintenance services

- For instance, Siemens Healthineers reported expanding preventive maintenance programs for advanced imaging and laboratory equipment to meet EU medical device regulations and reduce operational risks

- As healthcare facilities invest in sophisticated diagnostic and therapeutic devices, the need to minimize downtime and ensure compliance with ISO and MDR standards compels hospitals to rely on specialized maintenance providers

- Furthermore, the rise in hospital infrastructure expansion and outpatient diagnostic centers across Europe is contributing to higher adoption of regular maintenance contracts for installed equipment

- The convenience of outsourced service agreements, including remote monitoring, calibration, and emergency repair, alongside cost optimization and extended device lifecycle, are key factors propelling market growth in both public and private healthcare facilities

- Increasing awareness among administrators about operational efficiency, patient safety, and regulatory compliance further supports the expansion of professional medical equipment maintenance services in Europe

- Rising investments in advanced healthcare infrastructure and digital hospital initiatives across Europe are further driving demand for reliable maintenance services to ensure uninterrupted clinical operations

- The trend of leasing high-end medical equipment rather than outright purchases is creating opportunities for maintenance providers, as service contracts are often included in leasing agreements, ensuring regular upkeep and minimizing downtime

Restraint/Challenge

“High Maintenance Costs and Skilled Workforce Shortage”

- The relatively high cost of specialized maintenance services for advanced medical devices poses a challenge to broader adoption, particularly for smaller clinics and budget-constrained healthcare facilities

- For instance, high-end MRI or CT scanner maintenance contracts from Philips or Canon can require significant annual expenditure, limiting uptake among mid-sized hospitals

- In addition, a shortage of skilled biomedical engineers and certified technicians in Europe restricts the timely delivery of preventive and corrective maintenance, potentially increasing equipment downtime

- Ensuring adherence to strict regulatory standards such as ISO 13485 and EU MDR while delivering timely maintenance services adds operational complexity and can deter some healthcare providers from outsourcing services

- While some cost-effective and training-focused solutions are emerging, the perception of high service charges and limited availability of qualified personnel continues to hinder widespread adoption, especially in less urbanized regions

- Overcoming these challenges through workforce development, cost optimization, and technology-enabled service solutions will be vital for sustained growth of the Europe medical equipment maintenance market

- Variability in maintenance standards and service quality across different providers can create inconsistencies and reduce trust among healthcare facilities, limiting market expansion

- Budgetary constraints and delayed government reimbursements for public hospitals may restrict spending on comprehensive maintenance services, slowing adoption rates in certain European regions

Europe Medical Equipment Maintenance Market Scope

The market is segmented on the basis of service type, service providers, device type, level of maintenance, and end user.

- By Service Type

On the basis of service type, the Europe medical equipment maintenance market is segmented into preventive, corrective, and performance/operational maintenance. The preventive maintenance segment dominated the market with the largest share of 45.3% in 2025, driven by the growing emphasis on scheduled inspections, calibration, and early fault detection to minimize equipment downtime. Hospitals and diagnostic centers prioritize preventive maintenance to comply with regulatory standards and ensure uninterrupted operation of critical devices such as MRI and CT scanners. Preventive maintenance also extends the lifecycle of expensive medical equipment and reduces the risk of sudden failures, making it a preferred choice among large healthcare facilities. In addition, predictive maintenance technologies, including IoT-enabled monitoring, are increasingly being integrated within preventive services, further enhancing their adoption. The segment’s growth is supported by both public and private healthcare institutions seeking cost-efficient and reliable maintenance strategies.

The corrective maintenance segment is expected to witness the fastest growth during 2026–2033, driven by the rising adoption of complex and high-tech medical devices that require rapid repair services to minimize operational disruption. Corrective maintenance addresses unexpected equipment failures and ensures that hospitals maintain continuity in patient care. With increasing reliance on advanced imaging and surgical equipment, timely corrective services are critical to prevent clinical delays. Growth is further fueled by the outsourcing of repair services to specialized providers and the adoption of service contracts that include emergency support. Healthcare facilities in fast-developing regions are particularly adopting corrective maintenance due to increasing device complexity and operational pressure.

- By Service Providers

On the basis of service providers, the market is segmented into in-house service providers and external service providers. The external service providers segment dominated the Europe medical equipment maintenance market with the largest revenue share in 2025, owing to hospitals and clinics increasingly outsourcing maintenance to specialized third-party companies. Outsourcing ensures access to certified technicians, compliance with regulatory standards, and timely service for high-value medical devices without the burden of hiring and training in-house staff. External providers often offer comprehensive contracts covering preventive, corrective, and performance maintenance, along with software updates and calibration services. The growing complexity of medical devices and the rise in IoT-enabled equipment are further encouraging hospitals to rely on external expertise. In addition, outsourcing allows healthcare facilities to optimize operational costs while ensuring minimal equipment downtime.

The in-house service providers segment is anticipated to witness the fastest growth over the forecast period, driven by large hospitals and healthcare chains aiming to reduce dependency on external vendors and retain control over critical equipment servicing. In-house teams allow rapid response to equipment issues, improve turnaround time for maintenance requests, and ensure closer monitoring of device performance. Growth is supported by the increasing availability of training programs for biomedical engineers and technicians within Europe. Hospitals in Germany, France, and the UK are investing in internal maintenance capabilities for key devices, particularly imaging and surgical equipment, to enhance operational reliability and compliance with strict medical regulations.

- By Device Type

On the basis of device type, the Europe medical equipment maintenance market is segmented into imaging equipment, endoscopic devices, electromedical equipment, surgical instruments, and other medical equipment. The imaging equipment segment dominated the market in 2025, owing to the high cost, complexity, and critical nature of devices such as MRI, CT, and X-ray machines. Maintenance of imaging equipment is essential for accurate diagnostics, patient safety, and regulatory compliance. Hospitals and diagnostic centers prioritize preventive and corrective maintenance contracts to minimize downtime, reduce repair costs, and extend equipment lifespan. The growing adoption of high-tech imaging systems across Europe, combined with predictive maintenance technologies, further drives market dominance. In addition, equipment manufacturers and service providers offer integrated maintenance packages, ensuring continuous device performance.

The surgical instruments segment is expected to witness the fastest growth during 2026–2033, driven by the rising number of minimally invasive surgeries and adoption of advanced robotic-assisted surgical systems. Surgical instruments require frequent inspection, calibration, and sterilization to ensure precision and patient safety, making maintenance services increasingly critical. Growth is further fueled by the expanding number of surgical procedures and the need for highly specialized maintenance providers. The integration of smart monitoring and IoT-based tracking for surgical tools is also contributing to rapid adoption. Healthcare facilities in countries such as the UK, France, and the Nordics are increasingly investing in professional maintenance services for surgical instruments to enhance procedural efficiency and reduce operational risks.

- By Level of Maintenance

On the basis of level of maintenance, the market is segmented into Level 3 (Specialized), Level 2 (Technician), and Level 1 (User or First-line). The Level 3 (Specialized) segment dominated the market with the largest share in 2025, driven by the need for highly trained engineers to service complex medical devices such as MRI, CT scanners, and robotic surgical systems. Specialized maintenance ensures regulatory compliance, precise calibration, and timely repairs for high-value equipment, reducing operational risks in critical care settings. Providers of Level 3 services often offer bundled preventive and corrective maintenance contracts, which are preferred by large hospitals and diagnostic chains. The segment’s growth is further supported by the increasing reliance on advanced equipment with sophisticated software and electronic components that require expert handling.

The Level 1 (User or First-line) segment is expected to witness the fastest growth during 2026–2033, due to rising adoption of user-friendly monitoring tools and self-service maintenance protocols for basic medical devices. Hospitals and clinics are encouraging first-line personnel to perform routine inspections, cleaning, and minor troubleshooting to reduce dependency on specialized engineers and improve response time. Growth is further accelerated by the development of smart IoT-enabled devices that provide automated alerts, enabling non-specialists to perform initial maintenance actions effectively. This trend is particularly prominent in outpatient clinics, laboratory setups, and smaller healthcare centers.

- By End User

On the basis of end user, the market is segmented into hospitals, clinics, laboratories, and other healthcare centers. The hospitals segment dominated the Europe medical equipment maintenance market in 2025, accounting for the largest revenue share due to the high concentration of advanced diagnostic, imaging, and surgical equipment. Hospitals require comprehensive maintenance services, including preventive, corrective, and performance maintenance, to ensure uninterrupted clinical operations and patient safety. The high cost and complexity of medical devices, combined with strict regulatory compliance requirements, make hospitals the primary consumers of professional maintenance services. Large hospital chains are increasingly adopting service contracts with external providers and integrating predictive maintenance technologies to minimize downtime and optimize operational efficiency.

The clinics segment is anticipated to witness the fastest growth during 2026–2033, driven by the expansion of outpatient diagnostic centers, specialty clinics, and smaller healthcare facilities across Europe. Clinics increasingly rely on advanced medical devices such as ultrasound, endoscopic, and laboratory equipment, which require regular maintenance to ensure performance and safety. Growth is further supported by the outsourcing of maintenance services and adoption of IoT-enabled monitoring systems that facilitate remote equipment tracking. Rapid urbanization, rising patient volumes, and increased investment in private healthcare facilities are accelerating the uptake of maintenance services in this segment.

Europe Medical Equipment Maintenance Market Regional Analysis

- Germany dominated the Europe medical equipment maintenance market with the largest revenue share of 38.7% in 2025, characterized by its strong healthcare infrastructure, high medical device adoption rates, and the presence of leading medical technology companies

- Healthcare providers in Germany highly prioritize reliable maintenance services to ensure uninterrupted operation of critical equipment such as MRI, CT scanners, surgical instruments, and laboratory devices, which are essential for patient safety and clinical efficiency

- This dominance is further supported by the presence of leading medical technology companies, increasing outsourcing of maintenance services to specialized providers, and rising investments in hospital modernization, establishing professional medical equipment maintenance as the preferred solution for both public and private healthcare facilities

The Germany Medical Equipment Maintenance Market Insight

The Germany medical equipment maintenance market dominated Europe with the largest revenue share of 38.7% in 2025, driven by the country’s advanced healthcare infrastructure, high adoption of sophisticated medical devices, and strict regulatory standards. Hospitals and diagnostic centers prioritize uninterrupted operation of critical devices such as MRI, CT scanners, surgical instruments, and laboratory equipment to ensure patient safety and compliance. The market is further supported by outsourcing of maintenance services to specialized providers, integration of predictive maintenance solutions, and increasing investments in hospital modernization. German healthcare providers also emphasize operational efficiency, regulatory adherence, and high-quality service contracts, fueling strong demand for preventive, corrective, and performance maintenance services. The preference for professional, privacy-focused, and technologically advanced maintenance solutions aligns with local expectations, establishing Germany as the key market within Europe.

U.K. Medical Equipment Maintenance Market Insight

The U.K. medical equipment maintenance market is expected to grow at a noteworthy CAGR during the forecast period, driven by increasing focus on patient safety, regulatory compliance, and uninterrupted operation of medical devices in hospitals and clinics. Rising concerns over equipment downtime and high repair costs are encouraging adoption of preventive and corrective maintenance services. The country benefits from a strong presence of specialized service providers and outsourcing infrastructure, along with adoption of IoT-enabled monitoring systems for diagnostic and imaging equipment. Investments in digital healthcare initiatives, hospital modernization, and streamlined service contracts further stimulate market growth. U.K. healthcare providers increasingly rely on professional maintenance services to ensure efficiency, minimize downtime, and extend the lifecycle of critical medical devices.

France Medical Equipment Maintenance Market Insight

The France medical equipment maintenance market is projected to expand steadily during the forecast period, fueled by growing installation of advanced medical devices and increasing regulatory scrutiny across hospitals and clinics. French healthcare providers prioritize preventive maintenance and performance monitoring to maintain compliance and operational efficiency. Outsourcing of maintenance services to certified external providers is becoming prevalent, enabling timely calibration, repairs, and software updates for high-value equipment. Government initiatives supporting hospital infrastructure modernization, coupled with rising investments in diagnostic and imaging technologies, further boost demand. The market is also benefiting from adoption of predictive maintenance technologies and IoT-based monitoring, ensuring continuous device reliability and improved patient care.

Italy Medical Equipment Maintenance Market Insight

The Italy medical equipment maintenance market is expected to witness significant growth over the forecast period, driven by rising adoption of advanced imaging, surgical, and laboratory equipment across public and private healthcare facilities. Hospitals and diagnostic centers are emphasizing preventive maintenance and rapid corrective services to ensure uninterrupted operation and patient safety. The market is supported by specialized maintenance providers offering integrated service contracts covering calibration, repair, and performance optimization. Increasing awareness of regulatory compliance, operational efficiency, and equipment lifecycle management is propelling adoption. Furthermore, Italy is witnessing growing investments in hospital modernization and digital healthcare infrastructure, strengthening demand for professional maintenance services.

Europe Medical Equipment Maintenance Market Share

The Europe Medical Equipment Maintenance industry is primarily led by well-established companies, including:

- GE HealthCare (U.S.)

- Koninklijke Philips N.V. (Netherlands)

- Medtronic (Ireland)

- B. Braun SE (Germany)

- Drägerwerk AG & Co. KGaA (Germany)

- Metesa (Norway)

- Siemens Healthineers AG (Germany)

- Esaote SPA (Italy)

- Althea Group (Italy)

- Wisag (Germany)

- VI.TECH GmbH (Germany)

- Ergea Group (U.K.)

- EULEN Group (Spain)

- STERIS plc (U.S.)

- CANON MEDICAL SYSTEMS CORPORATION (Japan)

- Agfa-Gevaert Group (Belgium)

- Medisafe International (U.K.)

- Roeser Medical Group (Germany)

- Alldevice (Estonia)

- Nordic Service Group (Denmark)

What are the Recent Developments in Europe Medical Equipment Maintenance Market?

- In January 2026, the European Commission proposed major amendments to simplify and streamline medical device regulations impacting hospitals and manufacturers, a development expected to indirectly improve hospital compliance and equipment maintenance processes across Europe. The regulatory changes aim to reduce administrative burdens and improve device availability in clinical settings

- In December 2025, data showed a new safety concern as eight in ten NHS hospitals in England were found to be relying on outdated medical imaging and radiotherapy machines, prompting government commitments to upgrade equipment and accelerate maintenance and modernization efforts. MRI scanners and X‑ray machines over a decade old were still in use, raising risks of diagnostic errors and emphasizing the importance of effective maintenance and renewal programs

- In July 2025, the EU announced plans to strengthen strategic stockpiling of medical equipment and supplies as part of broader preparedness efforts for future health crises, potentially influencing maintenance and readiness strategies in national healthcare systems. This initiative reflects heightened focus on ensuring availability and operational reliability of critical medical devices across Europe

- In June 2025, Andhra Pradesh MedTech Zone (AMTZ) and the Universal Clinical Engineering Federation (UCEF) launched the International Biomed Cross (IBC) a global initiative to provide rapid support for medical device maintenance and repair during disasters and public health emergencies, signalling increased collaboration on equipment servicing infrastructure

- In June 2025, England’s NHS revealed thousands of patient harms and deaths linked to equipment malfunctions, highlighting serious maintenance and safety shortfalls in hospital medical devices across the country. Between 2022 and 2025, nearly 4,000 patients were harmed and 87 died due to malfunctions in critical equipment such as defibrillators and breathing devices, prompting calls for enhanced investment in infrastructure and modernization of maintenance practices

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.