Europe Micro Invasive Glaucoma Surgery Migs Devices Market

Market Size in USD Million

USD

365.12 Million

USD

2,923.93 Million

2024

2032

USD

365.12 Million

USD

2,923.93 Million

2024

2032

| 2025 - 2032 | |

| USD 365.12 Million | |

| USD 2,923.93 Million | |

| % | |

|

Europe Micro Invasive Glaucoma Surgery (MIGS) Devices Market Size

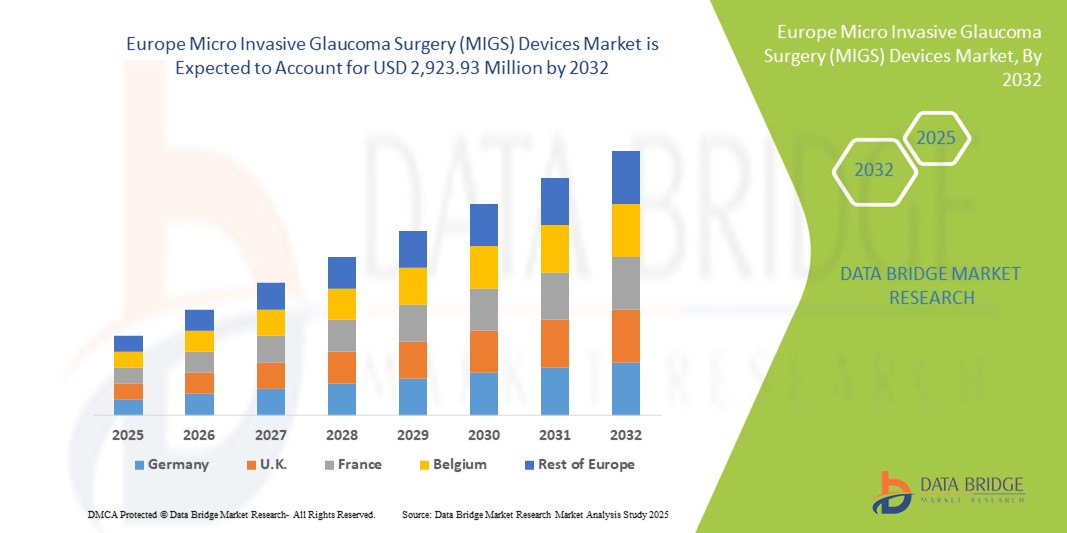

- The Europe micro invasive glaucoma surgery (MIGS) devices market size was valued at USD 365.12 million in 2024 and is expected to reach USD 2,923.93 million by 2032, at a CAGR of 29.7% during the forecast period

- The market growth is largely driven by increasing prevalence of glaucoma, rising awareness of early diagnosis and minimally invasive treatment options, and continuous technological advancements in MIGS devices across European countries

- Furthermore, growing preference for safer, faster, and outpatient-friendly surgical procedures, combined with supportive healthcare infrastructure and reimbursement policies, is positioning MIGS devices as the preferred choice for glaucoma management. These factors are collectively accelerating market adoption, thereby significantly enhancing industry growth

Europe Micro Invasive Glaucoma Surgery (MIGS) Devices Market Analysis

- Micro Invasive Glaucoma Surgery (MIGS) devices, offering minimally invasive solutions to reduce intraocular pressure, are increasingly vital components of modern glaucoma management in both hospital and outpatient settings due to their improved safety profile, faster recovery times, and compatibility with existing ophthalmic surgical procedures

- The escalating demand for MIGS devices is primarily fueled by the rising prevalence of glaucoma in Europe, growing awareness of early intervention benefits, and continuous technological advancements in MIGS device design and efficacy

- Germany dominated the Europe micro invasive glaucoma surgery (MIGS) devices market with the largest revenue share of 43% in 2024, characterized by advanced healthcare infrastructure, high patient awareness, and a strong presence of key ophthalmic device manufacturers, with France and the U.K. also experiencing substantial adoption of MIGS procedures in both private and public healthcare facilities

- Poland is expected to be the fastest-growing country in the Europe micro invasive glaucoma surgery (MIGS) devices market during the forecast period due to improving healthcare access, increasing ophthalmologist expertise, and rising investments in modern surgical technologies

- Trabecular Meshwork segment dominated the Europe micro invasive glaucoma surgery (MIGS) devices market with a market share of 45.5% in 2024, driven by its efficacy and safety of MIGS procedures targeting the trabecular meshwork, particularly through devices such as the iStent, which facilitate enhanced aqueous humor outflow and are increasingly preferred in clinical settings

Report Scope and Europe Micro Invasive Glaucoma Surgery (MIGS) Devices Market Segmentation

|

Attributes |

Europe Micro Invasive Glaucoma Surgery (MIGS) Devices Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Europe

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Europe Micro Invasive Glaucoma Surgery (MIGS) Devices Market Trends

Minimally Invasive Techniques Enhancing Patient Outcomes

- A significant and accelerating trend in the European MIGS devices market is the adoption of minimally invasive techniques that reduce intraocular pressure while minimizing complications and recovery time. This approach is improving patient comfort and expanding the scope of glaucoma management in both hospital and outpatient settings

- For instance, the iStent inject W system allows surgeons to perform trabecular bypass with reduced surgical trauma, promoting faster post-operative recovery and lowering the risk of adverse events. Similarly, the Hydrus Microstent provides precise implantation into the Schlemm’s canal for improved aqueous humor outflow

- Advanced device designs, including micro-stents and micro-implants, are enabling surgeons to achieve predictable and effective pressure reduction with smaller incisions and reduced operative time. Furthermore, these innovations are fostering broader acceptance of MIGS procedures among ophthalmologists and patients asuch as

- The integration of MIGS devices with cataract surgery procedures facilitates simultaneous treatment of two conditions, enhancing overall clinical efficiency and patient satisfaction. Centralized surgical platforms and refined delivery systems are contributing to more accurate and less invasive glaucoma interventions

- This trend towards safer, faster, and more precise surgical options is reshaping expectations for glaucoma care. Consequently, companies such as Glaukos are developing next-generation MIGS devices with features such as enhanced biocompatibility, precise microstent delivery, and compatibility with multiple surgical techniques

- The demand for MIGS devices that offer predictable outcomes, minimal invasiveness, and compatibility with combined procedures is growing rapidly across European hospitals, outpatient departments, and ophthalmology clinics, as healthcare providers prioritize efficiency and patient safety

Europe Micro Invasive Glaucoma Surgery (MIGS) Devices Market Dynamics

Driver

Rising Glaucoma Prevalence and Awareness of Early Intervention

- The increasing prevalence of glaucoma among the aging European population, coupled with growing awareness of early diagnosis and treatment options, is a significant driver for the heightened adoption of MIGS devices

- For instance, in 2024, hospitals in Germany and France reported higher MIGS procedure volumes due to proactive glaucoma screening programs aimed at preserving vision and preventing disease progression. Such strategies by key healthcare providers are expected to drive market growth in the forecast period

- As ophthalmologists seek safer alternatives to traditional glaucoma surgery, MIGS devices offer predictable intraocular pressure reduction, shorter recovery times, and lower complication rates, providing a compelling advantage over conventional procedures

- Furthermore, increasing awareness campaigns by healthcare associations and patient advocacy groups are educating patients about minimally invasive glaucoma treatment options, further promoting device adoption

- The convenience of outpatient procedures, reduced hospitalization, and enhanced post-operative care are key factors propelling MIGS device adoption in hospitals, ophthalmology clinics, and ambulatory surgery centers. Early detection and proactive intervention strategies also contribute to sustained market growth

Restraint/Challenge

High Device Costs and Regulatory Compliance Hurdles

- Concerns surrounding the relatively high cost of MIGS devices, along with stringent European regulatory requirements, pose a significant challenge to broader market penetration. As MIGS procedures require specialized equipment and training, adoption may be limited in cost-sensitive facilities

- For instance, smaller ophthalmology clinics in Eastern Europe may hesitate to adopt advanced MIGS devices due to budget constraints and the need for device certification under EU medical device regulations

- Addressing these cost and regulatory barriers through reimbursement support, training programs, and compliance assistance is crucial for building adoption across the region. Leading companies such as Glaukos and Ivantis emphasize support programs and clinical training to facilitate device uptake

- In addition, differences in healthcare infrastructure and reimbursement policies across European countries can slow uniform adoption of MIGS devices, making regulatory navigation a critical consideration for market players

- While prices are gradually stabilizing and more cost-effective devices are entering the market, the perceived premium for advanced MIGS technology can still hinder widespread adoption, especially in smaller hospitals or outpatient centers

- Overcoming these challenges through device cost optimization, regulatory guidance, and healthcare provider education will be vital for sustained market growth in Europe

Europe Micro Invasive Glaucoma Surgery (MIGS) Devices Market Scope

The market is segmented on the basis of product type, target, surgery type, glaucoma type, end user, and distribution channel.

- By Product Type

On the basis of product type, the micro invasive glaucoma surgery (MIGS) devices market is segmented into MIGS Shunt, MIGS Stent, Trabectome, Kahook Dual Blade, Tube Shunt, Micro-Implants, Micro Catheters, and Others. The MIGS Stent segment dominated the market with the largest market revenue share in 2024, driven by its minimally invasive approach and high clinical adoption. These stents, such as the iStent and Hydrus Microstent, provide effective intraocular pressure reduction with reduced surgical complications, making them preferred among ophthalmologists. Their compatibility with combined cataract procedures further enhances their appeal. In addition, MIGS stents benefit from strong clinical evidence supporting safety and long-term efficacy, boosting their adoption in hospitals and outpatient departments. The growing patient preference for faster recovery and less invasive surgery also contributes to their market dominance. The presence of multiple FDA-approved and CE-marked stent devices in Europe ensures consistent availability and drives surgeon confidence in these products.

The Trabectome segment is anticipated to witness the fastest growth rate from 2025 to 2032 due to increasing awareness of minimally invasive glaucoma surgeries in Eastern Europe. Trabectome allows precise ablation of trabecular meshwork tissue, offering safe and effective pressure reduction while preserving eye structure. Its adoption is accelerating as ophthalmologists seek cost-effective and versatile devices suitable for standalone glaucoma procedures. Improved surgical outcomes, shorter operative times, and minimal post-operative complications make Trabectome highly attractive for clinics and hospitals aiming to expand their MIGS offerings. Growing clinical training programs and awareness campaigns are further supporting this rapid adoption.

- By Target

On the basis of target, the micro invasive glaucoma surgery (MIGS) devices market is segmented into trabecular meshwork, suprachoroidal space, subconjunctival filtration, reducing aqueous production, and others. The Trabecular Meshwork segment dominated the market with the largest share of 45.5% in 2024, attributed to its effectiveness in enhancing aqueous humor outflow and lowering intraocular pressure. Devices targeting this area, such as micro-stents, are widely used due to predictable clinical outcomes and established long-term safety profiles. Trabecular meshwork procedures are often performed in combination with cataract surgery, making them convenient for both surgeons and patients. Their high adoption in Germany, France, and the U.K. is driven by advanced healthcare infrastructure and patient demand for minimally invasive interventions. Clinical training programs and strong procedural familiarity among ophthalmologists also support their dominant position. The increasing prevalence of open-angle glaucoma ensures a continued and growing patient base for this segment.

The Suprachoroidal Space segment is expected to witness the fastest growth from 2025 to 2032 due to its innovative approach to intraocular pressure reduction. Devices targeting this space, such as the iStent Supra, facilitate pressure reduction by creating an alternative drainage pathway while minimizing tissue disruption. Growing clinical evidence of efficacy and expanding surgeon expertise are driving adoption. Moreover, rising interest in safer, less invasive options for patients who cannot tolerate trabecular meshwork procedures contributes to this segment’s rapid growth. Continuous product innovations and increased training programs will further accelerate adoption in European clinics and hospitals.

- By Surgery Type

On the basis of surgery type, the micro invasive glaucoma surgery (MIGS) devices market is segmented into Glaucoma in Conjunction with Cataract and Stand-Alone Glaucoma procedures. The Glaucoma in Conjunction with Cataract segment dominated the market in 2024 due to the convenience of treating two conditions simultaneously, improving surgical efficiency and patient outcomes. Combining procedures reduces operative time, accelerates recovery, and is preferred by both surgeons and patients. Hospitals and outpatient clinics favor this approach as it enhances workflow efficiency and reduces overall healthcare costs. Clinical evidence supporting safety and effectiveness further reinforces its adoption. Patient preference for fewer surgical interventions also strengthens this segment’s dominance. Strong insurance coverage and reimbursement policies in Western Europe further support uptake.

The Stand-Alone Glaucoma segment is expected to witness the fastest growth during 2025–2032 due to increasing awareness of early glaucoma intervention and rising adoption in regions with growing outpatient surgical infrastructure. Stand-alone MIGS procedures provide flexible treatment options for patients with mild to moderate glaucoma and are increasingly performed in ambulatory surgery centers. Technological improvements in device design and delivery systems enhance precision and safety, fueling adoption. Rising prevalence of patients unsuitable for combined cataract procedures further drives this segment’s growth. Targeted marketing and clinical education initiatives are also accelerating adoption.

- By Glaucoma Type

On the basis of glaucoma type, the micro invasive glaucoma surgery (MIGS) devices market is segmented into open angle glaucoma, acute angle-closure glaucoma, normal-tension glaucoma, secondary glaucoma, pigmentary glaucoma, and congenital glaucoma. The Open Angle Glaucoma segment dominated the market in 2024 due to its high prevalence in Europe and the suitability of MIGS devices for this condition. MIGS procedures effectively lower intraocular pressure with minimal invasiveness, making them the preferred treatment for open-angle patients. Healthcare facilities, especially in Germany, France, and the U.K., have standardized MIGS protocols for this type. Established clinical outcomes and widespread surgeon familiarity further contribute to market dominance. Patient preference for outpatient and less invasive interventions ensures sustained growth. Training programs and educational campaigns by device manufacturers support broader adoption.

The Secondary Glaucoma segment is expected to witness the fastest growth during forecast period, due to the need for targeted interventions in complex cases. Rising awareness of MIGS as a viable solution for secondary glaucoma and improvements in device versatility are fueling adoption. Expanding clinical trials and evidence of safety and efficacy in secondary glaucoma cases are also supporting this segment’s rapid growth. Growing hospital and clinic adoption for complex glaucoma cases contributes to increasing revenue share.

- By End User

On the basis of end user, the micro invasive glaucoma surgery (MIGS) devices market is segmented into Hospitals’ Outpatient Departments (HOPD), Ophthalmology Clinics, Ambulatory Surgery Centers (ASCs), and Others. The Hospitals’ Outpatient Departments (HOPD) segment dominated the market in 2024 due to access to advanced surgical facilities, experienced surgeons, and higher patient volumes. HOPDs offer optimal conditions for MIGS procedures, including sterilized surgical theaters and post-operative care, making them preferred for hospitals and clinics performing multiple interventions. Strong insurance coverage and reimbursement policies in Western Europe further support adoption. Established training programs for ophthalmologists in hospitals enhance procedural confidence and uptake. The ability to combine MIGS with cataract surgery efficiently contributes to dominance. The segment’s scale and resources make it ideal for high-volume MIGS procedures.

The Ambulatory Surgery Centers (ASCs) segment is expected to witness the fastest growth during forecast period, as healthcare systems shift toward cost-effective, outpatient-focused procedures. ASCs provide patients with convenient scheduling, reduced hospitalization, and lower treatment costs. Growing investments in surgical infrastructure and adoption of minimally invasive techniques support rapid growth. Increasing patient preference for shorter recovery times and outpatient care drives ASC adoption. Device manufacturers are increasingly targeting ASCs with specialized product offerings. The flexibility and efficiency of ASCs make them attractive for expanding MIGS services.

- By Distribution Channel

On the basis of distribution channel, the micro invasive glaucoma surgery (MIGS) devices market is segmented into direct tender, retail sales, and others. The Direct Tender segment dominated the market in 2024, driven by institutional procurement practices, particularly in hospitals and government healthcare facilities. Direct tendering ensures cost efficiency, bulk purchasing, and reliable product availability, making it the preferred distribution method for key MIGS devices. Long-term contracts with major ophthalmic device manufacturers guarantee steady supply, supporting consistent adoption across Europe. Regulatory compliance and institutional preference for certified devices reinforce dominance. Relationships between manufacturers and hospitals facilitate training and support, enhancing market share. The streamlined procurement process ensures widespread device availability.

The Retail Sales segment is expected to witness the fastest growth during forecast period, due to increasing accessibility of MIGS devices for smaller ophthalmology clinics and outpatient centers. Growing awareness of minimally invasive procedures, coupled with simplified device ordering processes, allows retail distribution to expand reach. Manufacturers are also offering device support and training through retail channels, boosting adoption. Rising interest from private clinics and smaller healthcare facilities contributes to rapid segment growth. Retail availability increases penetration in emerging markets. Easier purchasing options drive adoption among clinics with limited procurement capacity.

Europe Micro Invasive Glaucoma Surgery (MIGS) Devices Market Regional Analysis

- Germany dominated the micro invasive glaucoma surgery (MIGS) devices market with the largest revenue share of 43% in 2024, characterized by advanced healthcare infrastructure, high patient awareness, and a strong presence of key ophthalmic device manufacturers, with France and the U.K. also experiencing substantial adoption of MIGS procedures in both private and public healthcare facilities

- Ophthalmologists in the region prioritize MIGS devices due to their proven safety profile, effectiveness in lowering intraocular pressure, and compatibility with cataract surgeries, making them a preferred choice in both hospitals and outpatient departments

- The high adoption is further supported by well-established reimbursement policies, robust clinical training programs, and the presence of key device manufacturers in the country, which facilitates easy access to the latest MIGS technologies

The Germany MIGS Devices Market Insight

The Germany micro invasive glaucoma surgery (MIGS) devices market dominated the market with the largest revenue share in 2024, driven by advanced healthcare infrastructure, high patient awareness, and early adoption of minimally invasive glaucoma procedures. Hospitals and outpatient departments prefer MIGS devices due to their proven safety, effectiveness in lowering intraocular pressure, and compatibility with cataract surgeries. The country’s strong reimbursement policies, presence of key device manufacturers, and well-established clinical training programs further support adoption. Patients increasingly favor minimally invasive procedures for faster recovery and fewer complications, enhancing market penetration. Germany’s high prevalence of open-angle glaucoma and emphasis on early intervention continue to strengthen its market leadership. The integration of MIGS devices into standard ophthalmic practices ensures consistent demand across hospitals and clinics.

Poland MIGS Devices Market Insight

The Poland micro invasive glaucoma surgery (MIGS) devices market is expected to be the fastest-growing market in Europe during the forecast period, driven by rising awareness of glaucoma and increasing adoption of minimally invasive procedures. The growing healthcare infrastructure, combined with expanding ophthalmology centers and outpatient facilities, supports the rapid uptake of MIGS technologies. Patients and surgeons are increasingly adopting micro-stents, micro-implants, and trabecular meshwork-targeted devices due to their safety and faster recovery compared with conventional surgeries. Government initiatives promoting early glaucoma intervention and improved access to advanced surgical devices further stimulate growth. The increasing prevalence of open-angle glaucoma in the country and rising demand for outpatient procedures are key factors driving market expansion. Poland’s growing investments in clinical training and hospital equipment enhance the adoption of MIGS devices across the country.

France Micro Invasive Glaucoma Surgery (MIGS) Devices Market Insight

The France micro invasive glaucoma surgery (MIGS) devices market is gaining momentum due to the country’s increasing focus on patient-centered ophthalmic care and early glaucoma intervention. French hospitals and ophthalmology clinics are adopting minimally invasive surgical solutions to reduce complications and accelerate post-operative recovery. The preference for combining cataract and glaucoma procedures is strengthening market adoption. Moreover, strong clinical evidence supporting the safety and efficacy of MIGS devices is driving trust among surgeons. The availability of advanced surgical devices and training programs further encourages uptake in hospitals and outpatient facilities.

Italy Micro Invasive Glaucoma Surgery (MIGS) Devices Market Insight

The Italy micro invasive glaucoma surgery (MIGS) devices market accounted for significant market revenue in 2024, attributed to the country’s growing awareness of glaucoma treatment and demand for minimally invasive solutions. Italian ophthalmologists are increasingly performing MIGS procedures in hospitals and ambulatory surgical centers, driven by the desire for better patient outcomes and faster recovery. Rising prevalence of open-angle glaucoma, combined with the adoption of innovative devices such as micro-stents and trabecular meshwork implants, is propelling market growth. Government support, clinical training programs, and expanding ophthalmology infrastructure are key factors boosting adoption across Italy.

Europe Micro Invasive Glaucoma Surgery (MIGS) Devices Market Share

The Europe micro invasive glaucoma surgery (MIGS) devices industry is primarily led by well-established companies, including:

- Alcon Inc. (U.S.)

- Santen Pharmaceutical Co., Ltd. (Japan)

- OPHTEC BV (Netherlands)

- Lumenis Be Ltd. (Belgium)

- Lumibird Medical (Australia)

- Sight Sciences, Inc. (U.S.)

- Glaukos Corporation (U.S.)

- Ivantis Group, Inc. (U.S.)

- Katalyst Surgical, Inc. (U.S.)

- Bausch + Lomb (U.S.)

- Carl Zeiss AG (Germany)

- Topcon Corporation (Japan)

- Nidek Co., Ltd. (Japan)

- Hoya Corporation (Japan)

- Optos plc (U.K.)

- Johnson & Johnson and its affiliates (U.S.)

- Medtronic (Ireland)

- BVI (U.S.)

- Avedro, Inc. (U.S.)

What are the Recent Developments in Europe Micro Invasive Glaucoma Surgery (MIGS) Devices Market?

- In June 2025, Glaukos announced that it had secured European Union Medical Device Regulation (EU-MDR) certification for its iStent infinite and other leading MIGS therapies. This certification paves the way for commercial launches in the European market, addressing the growing demand for minimally invasive glaucoma treatments. The certification underscores Glaukos' commitment to expanding its presence in Europe and enhancing patient access to advanced glaucoma therapies

- In June 2025, Glaukos commenced the commercial launch of iDose TR, a first-of-its-kind, long-duration, intracameral procedural pharmaceutical designed to deliver continuous glaucoma drug therapy inside the eye for extended periods. This innovative device offers a new approach to glaucoma management, reducing the need for daily eye drops and enhancing patient compliance

- In April 2024, Carl Zeiss Meditec completed the acquisition of DORC, a leading provider of ophthalmic surgical equipment. This acquisition enhances Zeiss's portfolio in MIGS, particularly in the retina and cataract surgery segments, and strengthens its position in the European ophthalmic market

- In March 2024, ZEISS Medical Technology showcased its latest innovations in ophthalmic surgery at the American Society of Cataract and Refractive Surgery (ASCRS) conference. The company introduced advanced 3D visualization technologies and surgical tools designed to enhance the precision and safety of MIGS procedures. These innovations aim to improve patient outcomes and streamline surgical workflows in the treatment of glaucoma

- In February 2024, Glaukos announced a collaboration with Celanese to commercialize the iDose TR, a long-duration intracameral glaucoma drug delivery system. This partnership leverages Celanese's VITALE EVA technology to enable continuous drug release, aiming to improve patient compliance and reduce the need for daily eye drops

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.