Europe Middle East And Africa Fleet Management Market

Market Size in USD Billion

USD

10.09 Billion

USD

21.64 Billion

2024

2032

USD

10.09 Billion

USD

21.64 Billion

2024

2032

| 2025 - 2032 | |

| USD 10.09 Billion | |

| USD 21.64 Billion | |

| % | |

|

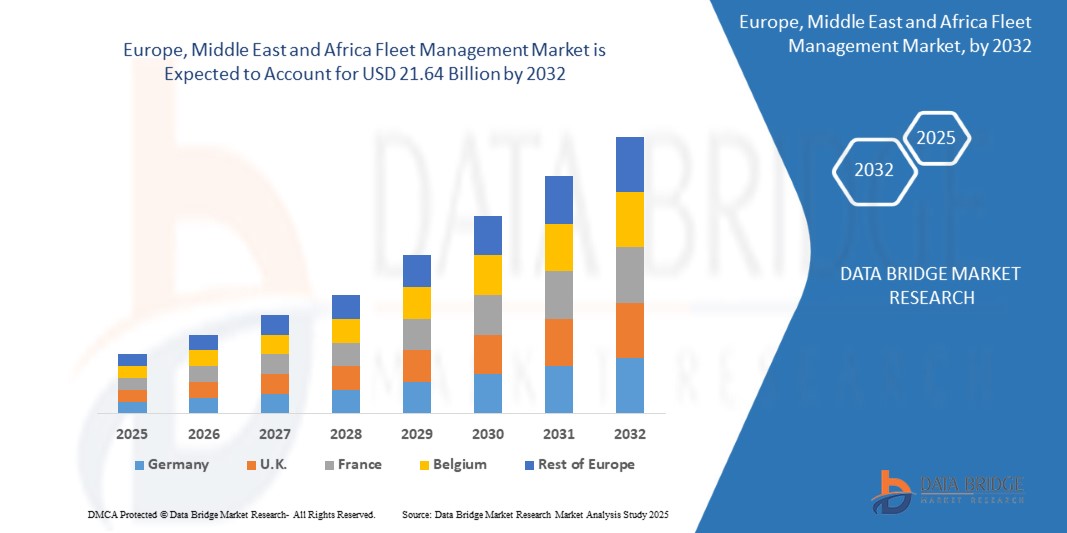

Europe, Middle East and Africa Fleet Management Market Size

- The Europe, Middle East and Africa fleet management market size was valued at USD 10.09 billion in 2024 and is expected to reach USD 21.64 billion by 2032, at a CAGR of 10.00% during the forecast period

- The market growth is largely fuelled by the increasing adoption of connected vehicle technologies, rising demand for operational efficiency, regulatory compliance requirements, and the growing need for real-time fleet tracking and management solutions

- In addition, other contributing factors include the expansion of e-commerce and logistics sectors, rising fuel costs driving efficiency measures, and increasing government initiatives to modernize transport infrastructure

Europe, Middle East and Africa Fleet Management Market Analysis

- The market is witnessing strong growth due to technological advancements in telematics, GPS tracking, and IoT-enabled fleet solutions

- There is a shift towards cloud-based and software-as-a-service (SaaS) fleet management solutions to reduce upfront investment and improve scalability

- Europe dominates the Europe, Middle East and Africa fleet management market, fuelled by widespread adoption of telematics, GPS tracking, and cloud-based fleet solutions across commercial, government, and private fleets

- Germany is expected to dominate the Europe, Middle East and Africa fleet management market, driven by its well-established transportation infrastructure, strict regulatory compliance, and high adoption of advanced fleet management technologies

- The solutions segment held the largest market revenue share in 2024 driven by widespread adoption of telematics, GPS tracking, and fleet management software. These solutions help operators optimize routes, monitor fuel usage, and enhance driver safety across large fleets. Cloud integration and mobile apps provide real-time insights, improving operational efficiency

Report Scope and Europe, Middle East and Africa Fleet Management Market Segmentation

|

Attributes |

Europe, Middle East and Africa Fleet Management Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Europe

Middle East and Africa

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the market insights such as market value, growth rate, market segments, geographical coverage, market players, and market scenario, the market report curated by the Data Bridge Market Research team includes in-depth expert analysis, import/export analysis, pricing analysis, production consumption analysis, and pestle analysis. |

Europe, Middle East and Africa Fleet Management Market Trends

Rise of Telematics and IoT-Enabled Fleet Management Solutions

- The increasing adoption of telematics and IoT-based fleet management solutions is reshaping fleet operations by providing real-time vehicle tracking, predictive maintenance, and driver behavior monitoring. These technologies allow fleet operators to make faster, data-driven decisions, reduce downtime, and optimize routes, ultimately improving operational efficiency

- The growing emphasis on fuel efficiency and cost reduction is driving demand for connected fleet solutions. Organizations are increasingly deploying GPS tracking, fuel sensors, and performance analytics to reduce operational expenses, minimize emissions, and enhance sustainability across large vehicle fleets

- Cloud-based fleet management platforms are becoming popular due to their scalability and ease of integration with existing systems. Operators benefit from remote monitoring, automated reporting, and real-time alerts, which simplifies fleet oversight and improves compliance with regulatory requirements

- For instance, in 2023, several logistics companies in the UAE integrated IoT-enabled fleet platforms, resulting in a 15% reduction in fuel costs and improved on-time delivery performance. These platforms allowed centralized control over multiple depots while reducing operational inefficiencies

- While telematics adoption is accelerating efficiency and sustainability, its effectiveness depends on continuous innovation, cybersecurity, and workforce training. Providers must develop localized, cost-effective solutions to maximize adoption across diverse fleets in the EMEA region

Europe, Middle East and Africa Fleet Management Market Dynamics

Driver

Rising Need for Operational Efficiency and Regulatory Compliance

- The increasing complexity of fleet operations, especially in logistics, delivery, and public transport, is pushing organizations to adopt advanced fleet management solutions. Companies aim to optimize routes, reduce fuel consumption, and enhance driver safety, driving demand for automated systems. This also helps fleets achieve better resource allocation, reduce idle times, and improve customer service levels across multiple locations

- Regulatory requirements across EMEA countries, including emission standards and driver hours monitoring, are incentivizing fleet operators to implement compliant and trackable fleet management solutions. This has accelerated investments in digital fleet platforms and reporting tools. Compliance-driven adoption also reduces legal penalties, enhances operational transparency, and strengthens trust with stakeholders and clients

- Organizations are also focusing on minimizing operational risks and reducing vehicle downtime. Predictive maintenance and real-time monitoring enable early detection of mechanical issues, lowering repair costs and preventing service disruptions. These strategies also extend vehicle lifespans, improve fleet reliability, and ensure uninterrupted service delivery in competitive markets

- For instance, in 2022, several European transport firms adopted GPS and telematics-based monitoring to comply with the EU’s digital tachograph regulations, improving both safety and operational transparency. The integration of telematics also enabled data-driven decision-making, better driver performance tracking, and more efficient fuel management

- While operational efficiency and compliance are key growth drivers, challenges remain in integrating legacy vehicles with modern systems and ensuring employee adoption of new technologies. Organizations must invest in training programs, change management initiatives, and phased technology rollouts to achieve maximum operational benefits

Restraint/Challenge

High Implementation Costs and Limited Infrastructure in Some Regions

- Advanced fleet management solutions, including telematics, IoT devices, and predictive analytics platforms, often involve high upfront costs, making them less accessible for small and medium fleet operators. This limits adoption in cost-sensitive markets and may result in unequal technology deployment across regions. High setup costs also affect ROI calculations and slow down investment decisions for smaller operators

- In some regions of the Middle East and Africa, infrastructure gaps such as inconsistent internet connectivity and lack of GPS coverage restrict real-time tracking and system reliability. These barriers hinder widespread deployment of connected fleet technologies and limit the effectiveness of digital monitoring systems. Poor connectivity also affects data collection, fleet reporting, and timely decision-making

- Maintenance of hardware and software systems requires skilled personnel, which may be scarce in remote areas. This complicates fleet monitoring and increases reliance on manual processes, reducing the potential benefits of automated solutions. Organizations may face additional costs for training, technical support, and outsourced maintenance, further increasing operational burdens

- For instance, in 2023, fleet operators in parts of Sub-Saharan Africa reported delays in system adoption due to equipment costs and limited digital infrastructure, slowing overall market penetration. The delays also impacted operational efficiency, route optimization, and compliance monitoring, reducing competitive advantage in these regions

- While technology continues to advance, reducing costs, improving network coverage, and providing training remain critical for enabling broader adoption and realizing long-term growth in the EMEA fleet management market. Strategic partnerships, government incentives, and localized solutions are essential to overcome these barriers and foster sustainable market development

Europe, Middle East and Africa Fleet Management Market Scope

The market is segmented on the basis of offering, lease type, hardware, fleet size, communication range, deployment model, technology, function, operation, business type, vehicle type, mode of transport, and end user.

• By Offering

On the basis of offering, the EMEA fleet management market is segmented into solutions and services. The solutions segment held the largest market revenue share in 2024 driven by widespread adoption of telematics, GPS tracking, and fleet management software. These solutions help operators optimize routes, monitor fuel usage, and enhance driver safety across large fleets. Cloud integration and mobile apps provide real-time insights, improving operational efficiency.

The services segment is expected to witness the fastest growth rate from 2025 to 2032, driven by rising demand for maintenance, support, and consulting services that complement fleet solutions.

• By Lease Type

On the basis of lease type, the market is segmented into on-lease and without lease. The on-lease segment held the largest market revenue share in 2024 due to reduced upfront costs and easy access to modern vehicles and telematics systems. On-lease options provide flexible payment plans, periodic vehicle upgrades, and replacement services, making them attractive for small and medium fleets.

The without lease segment is expected to witness the fastest growth rate from 2025 to 2032, driven by enterprises preferring full ownership for long-term cost control and asset management.

• By Hardware

On the basis of hardware, the market is segmented into GPS tracking devices, dash cameras, Bluetooth tracking tags, and data loggers. GPS tracking devices held the largest share in 2024 due to real-time vehicle location tracking, route optimization, and fuel management capabilities.

Dash cameras and Bluetooth tracking tags is expected to witness the fastest growth rate from 2025 to 2032, driven by growing demand for driver safety, vehicle monitoring, and fleet security. Data loggers are increasingly adopted for compliance reporting and performance analysis.

• By Fleet Size

On the basis of fleet size, the market is segmented into small fleets, medium fleets, and large & enterprise fleets. Large & enterprise fleets held the largest revenue share in 2024 due to high investment capacity and comprehensive fleet management needs.

Small and medium fleets is expected to witness the fastest growth rate from 2025 to 2032, driven by affordable cloud-based telematics and scalable software solutions. Growing awareness of operational efficiency and cost savings is boosting adoption among smaller operators.

• By Communication Range

On the basis of communication range, the market is segmented into short-range and long-range communication. Long-range communication held the largest market share in 2024 due to its ability to support real-time vehicle tracking and management over wide geographical areas.

Short-range communication is expected to witness the fastest growth rate from 2025 to 2032, driven by adoption in localized operations, warehouse fleets, and campus-based transport services. Increasing use of Bluetooth and Wi-Fi-enabled devices is supporting this growth.

• By Deployment Model

On the basis of deployment model, the market is segmented into on-premise, cloud, and hybrid. Cloud deployment held the largest share in 2024 due to remote accessibility, scalability, and reduced upfront costs.

Hybrid deployment is expected to witness the fastest growth rate from 2025 to 2032, driven by organizations seeking combined on-premise control with cloud-based flexibility. On-premise deployment is still preferred by companies with strict data security and compliance requirements.

• By Technology

On the basis of technology, the market is segmented into GNSS, cellular systems, EDI, remote sensing, computational methods & decision-making, and RFID. GNSS led the market in 2024 due to real-time vehicle tracking, navigation, and route optimization capabilities.

Cellular systems and computational methods is expected to witness the fastest growth rate from 2025 to 2032, driven by predictive analytics and advanced telematics solutions. RFID and EDI technologies are gaining adoption for asset management and logistics automation.

• By Function

On the basis of function, the market is segmented into asset management, route management, fuel consumption, real-time vehicle location, delivery schedule, accident prevention, mobile apps, driver behavior monitoring, vehicle maintenance updates, and ELD compliance. Real-time vehicle location and route management held the largest share in 2024 due to improved operational efficiency and reduced delays.

Driver behavior monitoring is expected to witness the fastest growth rate from 2025 to 2032, driven by safety regulations and insurance requirements. Fleet maintenance updates and mobile apps enhance decision-making and compliance monitoring.

• By Operation

On the basis of operation, the market is segmented into commercial and private. The commercial segment held the largest market share in 2024 due to adoption by logistics, transportation, and service fleets requiring operational efficiency.

The private segment is expected to witness the fastest growth rate from 2025 to 2032, driven by increasing adoption of connected vehicle solutions among corporate and personal fleets. Commercial adoption is driven by regulatory compliance, cost optimization, and efficiency demands.

• By Business Type

On the basis of business type, the market is segmented into large business and small business. Large business held the largest market share in 2024 due to high fleet volume and investment capacity.

Small business is expected to witness the fastest growth rate from 2025 to 2032, driven by affordable, scalable cloud-based fleet management solutions and pay-as-you-go service models. Large enterprises prioritize automation and analytics, while small businesses focus on cost-effective operational improvement.

• By Vehicle Type

On the basis of vehicle type, the market is segmented into internal combustion engine (ICE) and electric vehicles (EVs). ICE vehicles held the largest share in 2024 due to their majority presence in commercial fleets.

EVs is expected to witness the fastest growth rate from 2025 to 2032, driven by sustainability initiatives, government incentives, and adoption of green fleet policies. Fleet electrification is increasing across logistics, delivery, and public transport segments.

• By Mode of Transport

On the basis of mode of transport, the market is segmented into passenger cars, light commercial vehicles (LCVs), and heavy commercial vehicles (HCVs). HCVs held the largest market share in 2024 due to extensive use in long-haul logistics and supply chain operations.

LCVs is expected to witness the fastest growth rate from 2025 to 2032, driven by last-mile delivery and urban mobility growth. Increased e-commerce activity is further supporting adoption across LCVs and passenger fleets.

• By End User

On the basis of end user, the market is segmented into automotive, transportation & logistics, retail, manufacturing, food & beverages, energy & utilities, mining, government, healthcare, agriculture, construction, and other industries. Transportation & logistics held the largest share in 2024 due to high fleet volumes and operational requirements.

Manufacturing is expected to witness the fastest growth rate from 2025 to 2032, adoption is driven by cost savings, operational efficiency, and real-time monitoring needs.

Europe, Middle East and Africa Fleet Management Market Regional Analysis

The Europe fleet management market held the largest share in 2024, primarily driven by the rising need for operational efficiency, regulatory compliance, and cost optimization. Increasing adoption of telematics, GPS tracking, and cloud-based fleet solutions is fostering growth across logistics, transportation, and delivery sectors. Companies are also focusing on predictive maintenance and route optimization to reduce fuel consumption and vehicle downtime. The region is witnessing significant growth across commercial, government, and private fleet applications, with advanced fleet management solutions being integrated into both large enterprises and small to medium businesses

Europe, Middle East and Africa Fleet Management Market Share

The Europe, Middle East and Africa Fleet Management industry is primarily led by well-established companies, including:

- Ayvens Group (France)

- Arval (France)

- Alphabet (U.K.)

- TÜV SÜD (Germany)

- HERE Technologies (Netherlands)

- SAP SE (Germany)

- Webfleet Solutions Sales B.V. (Netherlands)

- STILL GmbH (Germany)

- Free2move (PSA) (France)

- Athlon (Netherlands)

- Zain (Kuwait)

- Fleet Africa (South Africa)

- Fleetroot (U.A.E.)

- Arabitra (U.A.E.)

- TENDERD (U.A.E.)

Latest Developments in Europe, Middle East and Africa Fleet Management Market

- In June 2024, according to an article published by Insightgeeks PVT LTD., fleet managers faced a significant challenge in managing the vast volumes of data generated by modern fleet management technologies. The integration of telematics and GPS tracking systems produced enormous amounts of data, including information on fuel consumption, driver behavior, and vehicle performance. While having access to such data can offer valuable insights, the real challenge lies in effectively analyzing and utilizing this information to make informed decisions. Properly leveraging this data required advanced analytical skills and tools to convert it into actionable insights, which significantly impacted the fleet efficiency and operational success

- In March 2024, according to an article published by Tourmaline Labs, Inc. managing the vast volume of data generated by modern fleet management systems posed a significant challenge for fleet managers. With the integration of telematics, AI, and other advanced technologies, fleets generated extensive data on vehicle performance, fuel consumption, driver behavior, and more. While this data provided valuable insights, the challenge lied in effectively analyzing and utilizing it to drive operational improvements. Fleet managers leveraged sophisticated analytical tools to transform this data into actionable strategies, optimizing efficiency and reducing costs, while managing the complexities and potential overload of information

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.