Europe Minimally Invasive Medical Robotics Imaging Visualization Systems Surgical Instruments Market

Market Size in USD Billion

USD

22.34 Billion

USD

39.40 Billion

2025

2033

USD

22.34 Billion

USD

39.40 Billion

2025

2033

| 2026 - 2033 | |

| USD 22.34 Billion | |

| USD 39.40 Billion | |

| % | |

|

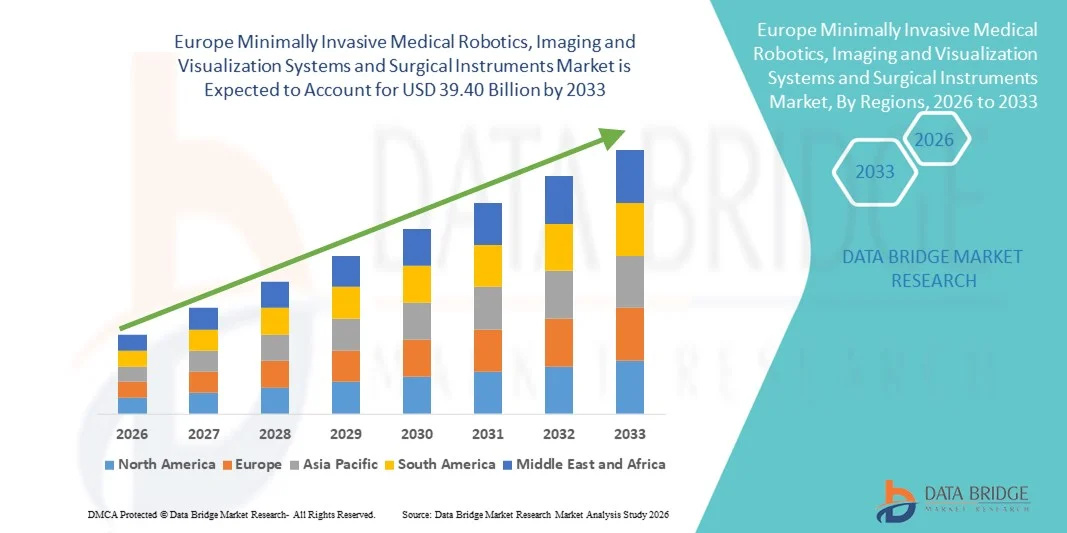

Europe Minimally Invasive Medical Robotics, Imaging and Visualization Systems and Surgical Instruments Market Size

- The Europe minimally invasive medical robotics, imaging and visualization systems and surgical instruments market size was valued at USD 22.34 billion in 2025 and is expected to reach USD 39.40 billion by 2033, at a CAGR of 7.35% during the forecast period

- The market growth is largely driven by the increasing adoption of minimally invasive surgical (MIS) procedures, continuous technological advancements in robotic-assisted systems, high-definition imaging, and real-time visualization platforms, along with the modernization of healthcare infrastructure across major European countries

- Furthermore, rising demand for precision-based surgeries, shorter hospital stays, reduced post-operative complications, and faster patient recovery is positioning minimally invasive robotics and advanced surgical instruments as essential components of next-generation operating rooms. These converging factors are accelerating technology integration across hospitals and specialty clinics, thereby significantly boosting the market’s expansion in Europe

Europe Minimally Invasive Medical Robotics, Imaging and Visualization Systems and Surgical Instruments Market Analysis

- Minimally invasive medical robotics, imaging and visualization systems, and advanced surgical instruments are increasingly becoming integral components of modern operating rooms across Europe, as healthcare providers prioritize precision, reduced surgical trauma, enhanced visualization, and improved patient outcomes across both public and private healthcare facilities

- The escalating demand for these systems is primarily fueled by the rising burden of chronic diseases, expanding geriatric population, growing preference for minimally invasive procedures, and continuous technological advancements in surgical devices, imaging and visualization systems, electrosurgical devices, and medical robotics

- Germany dominated the Europe minimally invasive medical robotics, imaging and visualization systems, and surgical instruments market with a revenue share of 26.4% in 2025, supported by its advanced hospital infrastructure, strong reimbursement framework, high surgical volumes, and early adoption of medical robotics and imaging devices technology across leading university and specialty hospitals

- Poland is expected to witness the fastest growth during the forecast period due to increasing government healthcare investments, modernization of hospital infrastructure, expanding access to minimally invasive surgical technologies, and rising demand for orthopedic, urological, and gastrointestinal procedures

- Surgical devices segment dominated the market with a share of 38.7% in 2025, driven by their extensive use across applications such as orthopedic surgery, gynaecological surgery, cardio-thoracic surgery, and oncology surgery, supported by continuous product innovations enhancing precision, safety, and procedural efficiency

Report Scope and Europe Minimally Invasive Medical Robotics, Imaging and Visualization Systems and Surgical Instruments Market Segmentation

|

Attributes |

Europe Minimally Invasive Medical Robotics, Imaging and Visualization Systems and Surgical Instruments Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Europe

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Europe Minimally Invasive Medical Robotics, Imaging and Visualization Systems and Surgical Instruments Market Trends

Rising Integration of Robotics with Advanced Imaging and Real-Time Visualization

- A significant and accelerating trend in the Europe minimally invasive medical robotics, imaging and visualization systems and surgical instruments market is the deepening integration of robotic-assisted platforms with high-definition imaging, 3D visualization, and real-time navigation systems. This convergence of technologies is significantly enhancing surgical precision and intraoperative decision-making across complex procedures

- For instance, leading hospitals in Germany and France are increasingly deploying integrated robotic systems combined with advanced imaging and fluorescence-guided visualization technologies to improve accuracy in urological and oncological surgeries. Similarly, next-generation imaging platforms are being incorporated into hybrid operating rooms to enable seamless surgical workflows

- Technology integration in minimally invasive systems enables features such as enhanced depth perception, AI-assisted image analysis, motion stabilization, and improved instrument articulation, supporting surgeons in performing highly precise interventions. For instance, advanced visualization systems can provide real-time tissue differentiation and augmented overlays during neurological and gastrointestinal procedures

- The seamless interoperability between medical robotics, electrosurgical devices, and imaging devices technology facilitates centralized control within digitally connected operating rooms. Through unified surgical platforms, clinicians can manage robotic arms, visualization feeds, and energy devices simultaneously, creating a synchronized and efficient procedural environment

- This trend toward more intelligent, data-driven, and ergonomically advanced surgical ecosystems is fundamentally reshaping surgical standards across Europe. Consequently, manufacturers are developing compact robotic systems and integrated visualization solutions tailored to multispecialty applications and mid-sized hospital settings

- The demand for technologically advanced, minimally invasive surgical solutions with integrated imaging and robotic precision is growing rapidly across European healthcare systems, as providers increasingly prioritize improved clinical outcomes, shorter recovery times, and optimized operating room efficiency

- In addition, the incorporation of AI-driven analytics and data recording capabilities within surgical systems is enabling performance tracking, surgical planning optimization, and enhanced post-operative assessment across complex procedures

Europe Minimally Invasive Medical Robotics, Imaging and Visualization Systems and Surgical Instruments Market Dynamics

Driver

Increasing Surgical Volumes and Preference for Minimally Invasive Procedures

- The rising prevalence of chronic diseases, growing geriatric population, and increasing number of complex surgical interventions across Europe are significant drivers for the heightened demand for minimally invasive medical robotics and advanced surgical instruments

- For instance, in 2025, several tertiary care centers across Italy and the U.K. expanded their robotic-assisted surgery programs to address growing demand for orthopedic and urological procedures, reflecting strategic investments in advanced minimally invasive technologies

- As patients and healthcare providers increasingly favor minimally invasive approaches due to reduced postoperative pain, lower complication rates, and shorter hospital stays, hospitals are investing in imaging and visualization systems that enhance procedural accuracy and patient safety

- Furthermore, supportive reimbursement frameworks in countries such as Germany and France and ongoing modernization of hospital infrastructure are accelerating the adoption of robotic systems, electrosurgical devices, and advanced imaging platforms

- The ability to perform highly precise surgeries with improved ergonomics for surgeons, reduced blood loss, and faster patient recovery is propelling adoption across applications including cardio-thoracic, gynecological, neurological, and orthopedic surgeries. Continuous clinical evidence supporting improved outcomes further strengthens market expansion

- Increasing cross-border collaborations between European medical institutions and technology providers are further accelerating innovation and clinical validation of advanced minimally invasive platforms

- Rising patient awareness regarding faster recovery and minimally invasive treatment options is also contributing to higher procedural volumes and greater hospital investments in robotic and imaging technologies

Restraint/Challenge

High Capital Investment and Regulatory Compliance Complexity

- The substantial upfront capital investment required for medical robotics, imaging and visualization systems, and advanced surgical instruments poses a significant challenge to broader market penetration, particularly for small and mid-sized hospitals

- For instance, procurement of robotic-assisted surgical systems involves high acquisition, maintenance, and training costs, which can limit adoption in budget-constrained healthcare facilities despite demonstrated clinical benefits

- Addressing financial constraints through flexible financing models, leasing options, and value-based procurement strategies is crucial for expanding accessibility. In addition, stringent European regulatory requirements under evolving medical device regulations increase compliance complexity and time-to-market for manufacturers

- The need for extensive surgeon training, certification, and integration of new systems into existing hospital workflows further adds operational challenges. Variability in reimbursement policies across European countries can also impact return on investment for healthcare providers

- While technological advancements continue to improve system efficiency and reduce procedural costs over time, the perceived financial burden and regulatory hurdles can still delay purchasing decisions, particularly in emerging European healthcare markets

- Complex procurement processes within public healthcare systems can prolong purchasing cycles and delay technology deployment across hospitals

- Limited availability of highly trained robotic surgeons and technical specialists in certain European countries may further restrict optimal utilization of advanced minimally invasive systems

Europe Minimally Invasive Medical Robotics, Imaging and Visualization Systems and Surgical Instruments Market Scope

The market is segmented on the basis of product, technology, and application.

- By Product

On the basis of product, the Europe minimally invasive medical robotics, imaging and visualization systems and surgical instruments market is segmented into surgical devices, imaging and visualization systems, electrosurgical devices, and medical robotics. The surgical devices segment dominated the market with the largest revenue share of 38.7% in 2025, driven by their extensive utilization across a broad range of minimally invasive procedures including orthopedic, gastrointestinal, gynecological, and cardiovascular surgeries. Surgical devices such as trocars, forceps, graspers, and staplers are fundamental components of laparoscopic and endoscopic interventions, ensuring consistent demand across hospitals. Their relatively lower cost compared to robotic platforms makes them widely accessible across both large tertiary centers and mid-sized healthcare facilities. Continuous product innovations focused on improved ergonomics, enhanced precision, and disposable variants further support segment leadership. In addition, the increasing procedural volume of minimally invasive surgeries across Germany, France, and Italy strengthens recurring demand. The versatility of surgical devices across multiple specialties firmly positions this segment as the primary revenue contributor.

The medical robotics segment is anticipated to witness the fastest growth rate from 2026 to 2033, fueled by rising adoption of robotic-assisted surgery across urology, gynecology, and oncology applications. Increasing clinical evidence supporting improved precision, reduced blood loss, and shorter recovery times is accelerating hospital investments in robotic platforms. European healthcare providers are progressively expanding robotic programs to enhance surgical outcomes and attract skilled surgeons. Technological advancements including compact robotic systems and improved instrument articulation are making these platforms more accessible. Growing training initiatives and surgeon familiarity with robotic systems further contribute to adoption. As capital investments rise and system costs gradually optimize, medical robotics is expected to register the highest growth momentum during the forecast period.

- By Technology

On the basis of technology, the market is segmented into surgical devices technology and imaging devices technology. The surgical devices technology segment dominated the market in 2025 due to its established role in enabling minimally invasive procedures through advanced laparoscopic and endoscopic instrumentation. Continuous improvements in materials, miniaturization, and electrosurgical integration have enhanced procedural efficiency and patient safety. These technologies are widely implemented across European hospitals because of their reliability and cost-effectiveness. The broad clinical applicability of surgical devices technology across multiple specialties supports its strong adoption. Furthermore, consistent upgrades in energy-based and precision-driven instruments contribute to recurring procurement cycles. Its critical role in both routine and complex surgeries ensures sustained market leadership.

The imaging devices technology segment is projected to witness the fastest growth from 2026 to 2033, driven by increasing demand for high-definition visualization, 3D imaging, and real-time intraoperative guidance. Advanced imaging enhances surgical accuracy and supports better clinical decision-making during complex neurological and oncology procedures. The expansion of hybrid operating rooms across Western Europe is accelerating adoption of integrated imaging platforms. Growing interest in fluorescence imaging and AI-assisted visualization further strengthens growth prospects. Hospitals are prioritizing advanced imaging investments to improve outcomes and reduce complications. As minimally invasive techniques become more sophisticated, demand for next-generation imaging technologies is expected to rise rapidly.

- By Application

On the basis of application, the market is segmented into cardio-thoracic surgery, vascular surgery, neurological surgery, ENT/respiratory surgery, cosmetic surgery, gastrointestinal surgery, gynaecological surgery, urological surgery, orthopedic surgery, oncology surgery, and dental surgery. The orthopedic surgery segment dominated the market in 2025 due to the high prevalence of musculoskeletal disorders and rising joint replacement procedures across Europe. Minimally invasive orthopedic techniques supported by advanced surgical devices and robotics are increasingly preferred for reduced recovery time and improved implant precision. Aging populations in countries such as Germany and Italy contribute to rising orthopedic procedure volumes. Robotic-assisted systems are gaining traction in knee and hip replacement surgeries, enhancing surgical alignment accuracy. Hospitals are investing in advanced visualization and navigation systems to optimize orthopedic outcomes. The high procedural frequency and technological integration support the segment’s dominant position.

The oncology surgery segment is expected to witness the fastest growth from 2026 to 2033, driven by increasing cancer incidence and the growing preference for minimally invasive tumor resection procedures. Advanced imaging and robotic-assisted systems enable higher precision in complex oncological interventions. Surgeons increasingly rely on real-time visualization and navigation technologies to improve margin accuracy and reduce complications. Expansion of cancer treatment centers across Europe is further accelerating adoption of minimally invasive platforms. Technological advancements in fluorescence imaging and AI-supported diagnostics are enhancing procedural success rates. As cancer care modernization intensifies, oncology surgery is projected to register the highest growth rate during the forecast period.

Europe Minimally Invasive Medical Robotics, Imaging and Visualization Systems and Surgical Instruments Market Regional Analysis

- Germany dominated the Europe minimally invasive medical robotics, imaging and visualization systems, and surgical instruments market with a revenue share of 26.4% in 2025, supported by its advanced hospital infrastructure, strong reimbursement framework, high surgical volumes, and early adoption of medical robotics and imaging devices technology across leading university and specialty hospitals

- Healthcare providers in the country highly prioritize precision-based minimally invasive procedures, advanced visualization platforms, and integrated robotic systems to enhance clinical outcomes across orthopedic, urological, and oncological surgeries

- This widespread adoption is further supported by favorable reimbursement frameworks, substantial healthcare expenditure, a strong presence of leading medical technology manufacturers, and continuous hospital modernization initiatives, establishing advanced minimally invasive surgical systems as a preferred solution across major German healthcare institutions

The Germany Minimally Invasive Medical Robotics, Imaging and Visualization Systems and Surgical Instruments Market Insight

Germany captured the largest revenue share within Europe in 2025, fueled by its advanced healthcare infrastructure, high surgical procedure volumes, and early adoption of robotic-assisted and high-definition imaging technologies. Hospitals and university medical centers are increasingly prioritizing minimally invasive surgical platforms to enhance precision and reduce patient recovery times. Strong reimbursement mechanisms and consistent capital investments in hybrid operating rooms further support market expansion. Moreover, the presence of leading medical device manufacturers and a strong focus on surgical innovation significantly contribute to the country’s market leadership.

France Minimally Invasive Medical Robotics, Imaging and Visualization Systems and Surgical Instruments Market Insight

The France market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by increasing modernization of public hospitals and growing preference for minimally invasive surgical techniques. Rising demand for advanced imaging and visualization systems in oncology and cardiovascular procedures is fostering adoption. Government-backed healthcare investments and structured reimbursement policies are further accelerating procurement of robotic-assisted platforms. The integration of advanced surgical technologies into academic and tertiary care centers is strengthening the country’s growth trajectory.

U.K. Minimally Invasive Medical Robotics, Imaging and Visualization Systems and Surgical Instruments Market Insight

The U.K. market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by increasing surgical backlogs and the need for efficient, precision-based procedures within NHS hospitals. Growing adoption of robotic-assisted systems in urology and gynecology is enhancing procedural efficiency and patient outcomes. Investments in digital operating rooms and advanced intraoperative imaging systems are further stimulating market growth. In addition, expanding clinical training programs for robotic surgery are encouraging broader technology utilization across major healthcare institutions.

Poland Minimally Invasive Medical Robotics, Imaging and Visualization Systems and Surgical Instruments Market Insight

The Poland market is gaining momentum due to increasing government healthcare spending, expanding hospital infrastructure, and growing demand for advanced surgical technologies. The country is witnessing rising adoption of minimally invasive procedures across orthopedic and urological applications. Investments in modern imaging devices technology and robotic platforms are gradually increasing across tertiary hospitals. Moreover, ongoing healthcare system modernization initiatives are supporting long-term market development and technology penetration.

Europe Minimally Invasive Medical Robotics, Imaging and Visualization Systems and Surgical Instruments Market Share

The Europe Minimally Invasive Medical Robotics, Imaging and Visualization Systems and Surgical Instruments industry is primarily led by well-established companies, including:

- Medtronic (Ireland)

- Intuitive Surgical, Inc. (U.S.)

- Siemens Healthineers AG (Germany)

- Koninklijke Philips N.V. (Netherlands)

- Olympus Corporation (Japan)

- CANON MEDICAL SYSTEMS CORPORATION (Japan)

- Stryker (U.S.)

- Smith & Nephew (U.K.)

- Boston Scientific Corporation (U.S.)

- B. Braun SE (Germany)

- Zimmer Biomet (U.S.)

- Maquet GmbH (Germany)

- EOS imaging (France)

- Mauna Kea Technologies S.A. (France)

- Brainlab AG (Germany)

- CMR Surgical Ltd. (U.K.)

- Renishaw plc (U.K.)

- Medisafe International Ltd. (U.K.)

- ERGOSURG Mechatronics and Medical Solutions GmbH (Germany)

- VirtaMed AG (Switzerland)

What are the Recent Developments in Europe Minimally Invasive Medical Robotics, Imaging and Visualization Systems and Surgical Instruments Market?

- In November 2025, a collaborative team from KU Leuven and Balgrist University Hospital won the KUKA Innovation Award 2025 for a breakthrough robotic technique that enhances safety and accuracy in spinal surgery. The award-winning system integrates ultrasound-guided collaborative robots to improve pedicle screw placement accuracy, reduce surgical time, and minimize risk in spinal procedures

- In August 2025, Beijing Surgerii Robotics’ SHURUI® Single-Port Surgical Robot received CE certification in Europe. This marks a significant regulatory milestone, enabling the device’s clinical use in urologic, gynecologic, general laparoscopic and thoracic procedures across EU hospitals and establishing a new standard for single-port minimally invasive robotics

- In June 2025, MicroPort® MedBot’s CE-certified Toumai® Surgical Robot enabled the first-ever intra-EU telesurgery cases. Surgeries including a prostatectomy and hysterectomy were successfully performed remotely between Belgium and Belgium via its high-definition robotic system, demonstrating real-time remote robotic surgical capability within Europe

- In November 2024, the Toumai® Laparoscopic Surgical Robot performed a landmark combined adrenal tumor and gallbladder removal in Italy. This milestone surgery using a new robotic platform underscores the expanding clinical adoption and real-world application of minimally invasive robotic systems in European hospitals

- In May 2024, MicroPort® MedBot’s Toumai® Laparoscopic Surgical Robot received CE MDR certification from the EU. The approval broadens the robot’s official clinical indications across urologic, general, thoracic and gynecologic endoscopic surgeries, emphasizing regulatory progress in robotic minimally invasive systems in Europe

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.