Europe Minimally Invasive Spine Technologies Market

Market Size in USD Million

USD

835.80 Million

USD

2,129.29 Million

2024

2032

USD

835.80 Million

USD

2,129.29 Million

2024

2032

| 2025 - 2032 | |

| USD 835.80 Million | |

| USD 2,129.29 Million | |

| % | |

|

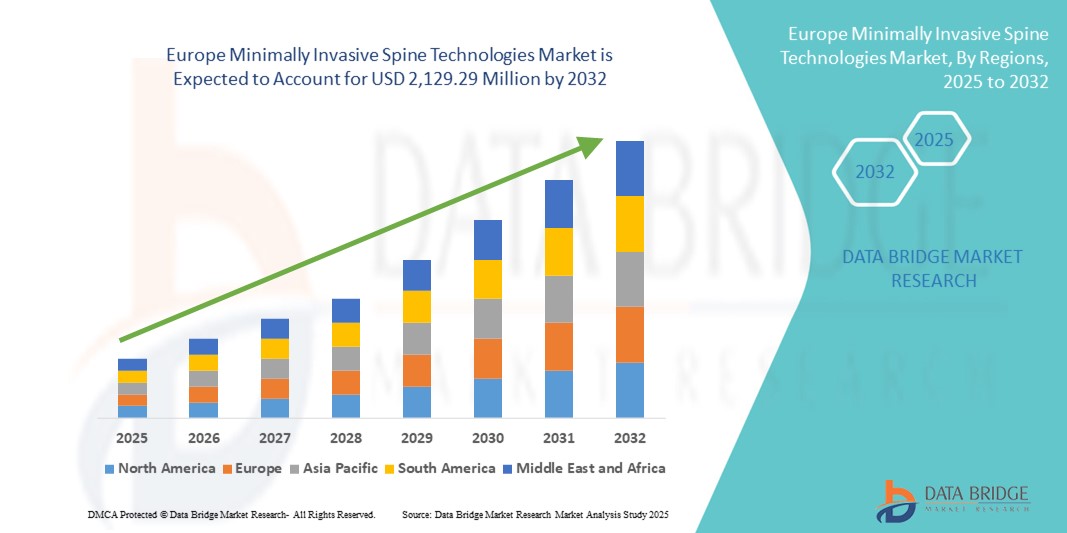

Europe Minimally Invasive Spine Technologies Market Size

- The Europe minimally invasive spine technologies market size was valued at USD 835.80 million in 2024 and is expected to reach USD 2,129.29 million by 2032, at a CAGR of 12.40% during the forecast period

- The market growth is primarily driven by the increasing prevalence of spinal disorders, aging population, and patient preference for procedures offering reduced recovery time, minimal scarring, and lower postoperative complications

- In addition, advancements in imaging technologies, navigation systems, and surgical instruments are enabling greater precision and outcomes in spine surgeries. These innovations, combined with rising demand for outpatient procedures and cost-effective solutions, are fostering rapid adoption across the region, propelling market expansion

Europe Minimally Invasive Spine Technologies Market Analysis

- Minimally invasive spine technologies, enabling surgical treatment of spinal disorders through smaller incisions and advanced imaging, are becoming increasingly integral in European healthcare settings due to their reduced recovery time, lower infection risks, and improved patient satisfaction

- The growing adoption of these technologies is primarily driven by an aging population, rising cases of degenerative spine conditions, and increasing demand for outpatient spinal procedures with minimal disruption to daily life

- Germany dominated the Europe minimally invasive spine technologies market with the largest revenue share of 32.1% in 2024, supported by robust healthcare infrastructure, early adoption of surgical innovations, and strong presence of medical technology companies

- Poland is expected to be the fastest-growing country in the Europe minimally invasive spine technologies market during the forecast period, owing to expanding healthcare investments, better access to specialized care, and increasing awareness of minimally invasive surgical solutions

- Implants segment dominated the Europe minimally invasive spine technologies market with a market share of 49.1% in 2024, due to their widespread application in spinal stabilization and fusion procedures using minimally invasive techniques

Report Scope and Europe Minimally Invasive Spine Technologies Market Segmentation

|

Attributes |

Europe Minimally Invasive Spine Technologies Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Europe

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Europe Minimally Invasive Spine Technologies Market Trends

Technological Advancements Driving Precision and Recovery Outcomes

- A significant and accelerating trend in the Europe minimally invasive spine technologies market is the increasing integration of advanced surgical technologies such as robotic-assisted systems, real-time intraoperative navigation, and 3D imaging. These innovations are enhancing surgical accuracy, reducing operative time, and significantly improving patient recovery outcomes

- For instance, Medtronic’s Mazor X Stealth Edition robotic guidance system is being widely adopted across European surgical centers, offering spine surgeons enhanced visualization and precision during minimally invasive procedures. Similarly, Brainlab’s Curve Navigation system supports improved planning and execution of spinal surgeries with minimal tissue disruption

- Robotic and navigation-assisted surgeries reduce risks of complications and improve implant placement accuracy, while patients benefit from smaller incisions, reduced blood loss, and faster discharge from hospitals. The combination of these technologies allows for a more predictable and efficient surgical process

- Leading hospitals in Germany, France, and the Netherlands are increasingly investing in these systems to stay at the forefront of surgical innovation. The adoption of 3D-printed patient-specific implants and preoperative planning tools is also gaining traction across Europe, improving outcomes in complex spinal cases

- This trend toward technology-enabled, minimally invasive spine care is reshaping expectations among both surgeons and patients. As a result, key players such as Globus Medical, NuVasive, and DePuy Synthes are expanding their European portfolios with AI-powered navigation platforms, expandable cages, and robotic-assisted solutions

- The demand for precision-driven, less invasive spinal procedures is growing rapidly across Europe’s healthcare systems, supported by increasing R&D investment and supportive reimbursement policies that prioritize patient-centric outcomes

Europe Minimally Invasive Spine Technologies Market Dynamics

Driver

Rising Prevalence of Spine Disorders and Preference for Outpatient Procedures

- The growing incidence of spinal disorders such as herniated discs, spinal stenosis, and degenerative disc disease, especially among Europe’s aging population, is a major driver of the minimally invasive spine technologies market

- For instance, more than 20% of the European population was aged 65 or older in 2024 (Eurostat), contributing to a significant rise in demand for spine surgeries that prioritize reduced trauma and faster recovery

- Patients and healthcare providers asuch as are favoring minimally invasive approaches due to their clinical benefits, including lower infection rates, reduced postoperative pain, and faster return to normal activities. These procedures also support a shift toward outpatient and day-care surgery models

- In addition, healthcare systems across Europe are emphasizing cost-efficiency and resource optimization, making MIS technologies more desirable due to shorter hospital stays and faster patient throughput

- As device manufacturers continue to introduce specialized MIS implants, imaging systems, and navigation tools tailored for European hospitals, adoption is accelerating in key markets such as Germany, France, and Italy

Restraint/Challenge

High Equipment Costs and Learning Curve Among Surgeons

- The high cost of acquiring and maintaining advanced MIS systems including robotic platforms, navigation equipment, and 3D imaging tools poses a significant challenge to broader adoption across Europe

- For instance, robotic-assisted spine surgery requires specialized training to ensure accuracy and safety, which can delay adoption in hospitals with limited training infrastructure or staffing resources

- Many small and mid-sized hospitals, especially in Eastern and Southern Europe, face budget constraints that limit their ability to invest in these technologies, despite growing demand for minimally invasive procedures

- Moreover, the complexity of MIS procedures presents a steep learning curve for surgeons, requiring dedicated training and practice. Transitioning from traditional open techniques to MIS often demands new skill sets, longer training periods, and adjustments in surgical workflow

- Addressing this challenge requires collaborative efforts between medical device companies and healthcare institutions to provide training programs, cost-effective technology solutions, and awareness campaigns that highlight the long-term benefits of MIS adoption. Broader reimbursement support and regional funding initiatives may also help reduce financial barriers to entry

Europe Minimally Invasive Spine Technologies Market Scope

The market is segmented on the basis of product type, condition, and end user.

- By Product Type

On the basis of product type, the Europe minimally invasive spine technologies market is segmented into implants, instruments, and software. The implants segment dominated the market with the largest revenue share of 49.1% in 2024, owing to the growing use of advanced interbody cages, pedicle screw systems, and fusion devices designed specifically for minimally invasive procedures. These implants enable spine stabilization with minimal disruption to surrounding tissues, making them essential in modern spine surgeries. In addition, innovations in biomaterials and 3D-printed implants are expanding the utility and efficiency of implant-based solutions, especially in degenerative disc repair and spinal fusion cases.

The software segment is projected to experience the fastest growth rate from 2025 to 2032, driven by increasing adoption of surgical planning tools, intraoperative navigation platforms, and robotic integration systems. Software solutions improve surgical precision, enable preoperative simulation, and enhance intraoperative decision-making. Growing investments in AI-based platforms and real-time 3D visualization are further propelling demand for software-driven tools in MIS procedures.

- By Condition

On the basis of condition, the Europe minimally invasive spine technologies market is segmented into degenerative disc disease, spinal stenosis, scoliosis, spinal infection, and others. The degenerative disc disease segment held the largest market revenue share of 39.4% in 2024, supported by a high prevalence among the aging European population. As the leading cause of chronic back pain and mobility issues, degenerative disc disease is driving demand for minimally invasive procedures such as microdiscectomy and MIS spinal fusion. Patient preference for reduced pain, faster recovery, and limited tissue disruption makes MIS the preferred treatment method in this condition.

The spinal stenosis segment is anticipated to grow at the fastest rate from 2025 to 2032, fueled by a growing number of older adults experiencing narrowing of the spinal canal. Technological advancements in decompression tools and targeted implant systems optimized for MIS techniques are expanding treatment accessibility and improving patient outcomes in spinal stenosis cases.

- By End User

On the basis of end user, the Europe minimally invasive spine technologies market is segmented into hospitals, clinics, and others. The hospitals segment dominated the market with the largest share of 62.1% in 2024, as most complex and advanced spine procedures are performed in hospital settings equipped with specialized surgical infrastructure. European hospitals are early adopters of robotics, real-time navigation, and AI-assisted technologies that facilitate minimally invasive spine surgeries, particularly in Germany, France, and the UK.

The clinics segment is expected to witness the fastest growth from 2025 to 2032, due to increasing demand for outpatient care, same-day discharge capabilities, and lower treatment costs. Clinics offering minimally invasive procedures for less severe spine conditions are attracting patients seeking quick recovery and reduced hospital stays. Expansion of specialized spine centers and growing surgeon expertise in MIS techniques are further contributing to this trend.

Europe Minimally Invasive Spine Technologies Market Regional Analysis

- Germany dominated the Europe minimally invasive spine technologies market with the largest revenue share of 32.1% in 2024, supported by robust healthcare infrastructure, early adoption of surgical innovations, and strong presence of medical technology companies

- Patients and healthcare providers in Germany prioritize procedures that offer faster recovery, reduced postoperative complications, and improved long-term outcomes, making minimally invasive techniques a preferred choice for spinal treatments

- This widespread adoption is further supported by government initiatives to modernize surgical care, a high concentration of skilled spine surgeons, and significant investments in robotic systems, navigation platforms, and specialized spinal implants, positioning Germany as a regional leader in minimally invasive spine solutions

Germany Minimally Invasive Spine Technologies Market Insight

The Germany minimally invasive spine technologies market captured the largest revenue share in Europe in 2024, fueled by the country’s advanced medical infrastructure, early adoption of robotic and navigation-assisted systems, and strong presence of global medtech companies. German healthcare institutions prioritize innovative solutions that improve surgical precision and patient recovery, leading to widespread implementation of minimally invasive procedures in both academic and private hospitals. The government's emphasis on value-based care and digital health integration further supports the expansion of the market.

U.K. Minimally Invasive Spine Technologies Market Insight

The U.K. minimally invasive spine technologies market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by rising demand for outpatient surgical procedures and patient preference for less invasive treatment options. A strong focus on healthcare efficiency, combined with increased NHS investments in surgical technology and training, is accelerating adoption. In addition, the country’s commitment to reducing hospital stays and improving surgical outcomes is prompting both public and private hospitals to integrate MIS solutions into standard spinal care practices.

France Minimally Invasive Spine Technologies Market Insight

The France minimally invasive spine technologies market is expected to expand at a steady CAGR through the forecast period, supported by robust health coverage, a high prevalence of spinal disorders, and increasing adoption of robotic and navigation systems in surgical centers. French healthcare providers are focusing on improving patient quality of life through technologically advanced, less invasive interventions. National research collaborations and medical training initiatives are further fostering innovation and market penetration of MIS procedures.

Italy Minimally Invasive Spine Technologies Market Insight

The Italy minimally invasive spine technologies market is gaining momentum due to growing demand for cost-effective and efficient surgical care. Increasing public-private healthcare collaboration, coupled with a shift towards outpatient surgery, is boosting MIS adoption. Italian hospitals are also integrating digital tools for surgical planning and execution, supported by favorable reimbursement structures and regional funding initiatives aimed at modernizing operating rooms and expanding access to spine care.

Poland Minimally Invasive Spine Technologies Market Insight

The Poland minimally invasive spine technologies market is expected to grow at the fastest CAGR in Europe during the forecast period, driven by rising healthcare investments, improved access to specialized care, and increasing surgeon training in MIS techniques. The country's focus on upgrading surgical infrastructure and expanding regional spine centers is creating a favorable environment for minimally invasive technologies. Growing awareness among patients about the benefits of less invasive spinal procedures is also contributing to strong market momentum in Poland.

Europe Minimally Invasive Spine Technologies Market Share

The Europe minimally invasive spine technologies industry is primarily led by well-established companies, including:

- Medtronic (Ireland)

- DePuy Synthes, Inc. (U.S.)

- NuVasive, Inc. (U.S.)

- Zimmer Biomet (U.S.)

- Globus Medical, Inc. (U.S.)

- Stryker (U.S.)

- B. Braun SE (Germany)

- Smith+Nephew (U.K.)

- Spineart SA (Switzerland)

- Brainlab AG (Germany)

- Joimax GmbH (Germany)

- Alphatec Spine, Inc. (U.S.)

- RTI Surgical, Inc. (U.S.)

- KARL STORZ SE & Co. KG (Germany)

- RIWOspine GmbH (Germany)

- Medacta International SA (Switzerland)

- Ulrich Medical (Germany)

- Xtant Medical Holdings, Inc. (U.S.)

- SPINEWAY (France)

- Zavation Medical Products, LLC (U.S.)

What are the Recent Developments in Europe Minimally Invasive Spine Technologies Market?

- In April 2023, Medtronic plc expanded its minimally invasive spine surgery capabilities in Europe by launching the Mazor X Stealth Edition in multiple leading hospitals across Germany and France. This advanced robotic guidance system combines real-time 3D navigation with robotic precision, enhancing surgical accuracy and reducing patient recovery time. The initiative reflects Medtronic's continued investment in expanding its European footprint and its commitment to offering state-of-the-art MIS solutions for complex spinal procedures

- In March 2023, Globus Medical, Inc. partnered with prominent surgical training institutions in the United Kingdom to introduce hands-on educational programs focused on minimally invasive spine technologies. The initiative includes training on expandable implants and navigation-assisted procedures, aiming to address the learning curve and promote safer, more effective MIS adoption among European spine surgeons. This strategic move demonstrates Globus Medical's emphasis on surgeon empowerment and clinical excellence in key European markets

- In March 2023, Brainlab AG, a Germany-based digital surgery technology provider, launched its upgraded Loop-X Mobile Imaging Robot in several European hospitals. This imaging system enhances intraoperative visualization, enabling higher precision in minimally invasive spine surgeries. The deployment of Loop-X underscores Brainlab’s role in pushing the boundaries of real-time navigation and imaging in European surgical environments

- In February 2023, NuVasive, Inc. announced the expansion of its X360 System across multiple surgical centers in Italy and Spain. This comprehensive approach to lateral spine surgery allows for a minimally invasive, single-position procedure that enhances efficiency and patient safety. The rollout is part of NuVasive’s strategic plan to grow its MIS portfolio and offer streamlined, advanced spine solutions to European healthcare providers

- In January 2023, DePuy Synthes, the orthopaedics company of Johnson & Johnson, collaborated with several hospitals in France to pilot its AI-assisted VELYS Navigation System for minimally invasive spine procedures. This system provides surgeons with real-time data and analytics to optimize surgical planning and execution. The project highlights DePuy Synthes’ dedication to delivering intelligent MIS technologies that align with Europe’s growing emphasis on precision medicine and improved patient outcomes

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.