Europe Mobile C Arm Equipment Market

Market Size in USD Billion

USD

1.80 Billion

USD

2.70 Billion

2025

2033

USD

1.80 Billion

USD

2.70 Billion

2025

2033

| 2026 - 2033 | |

| USD 1.80 Billion | |

| USD 2.70 Billion | |

| % | |

|

Europe Mobile C-Arm Equipment Market Overview

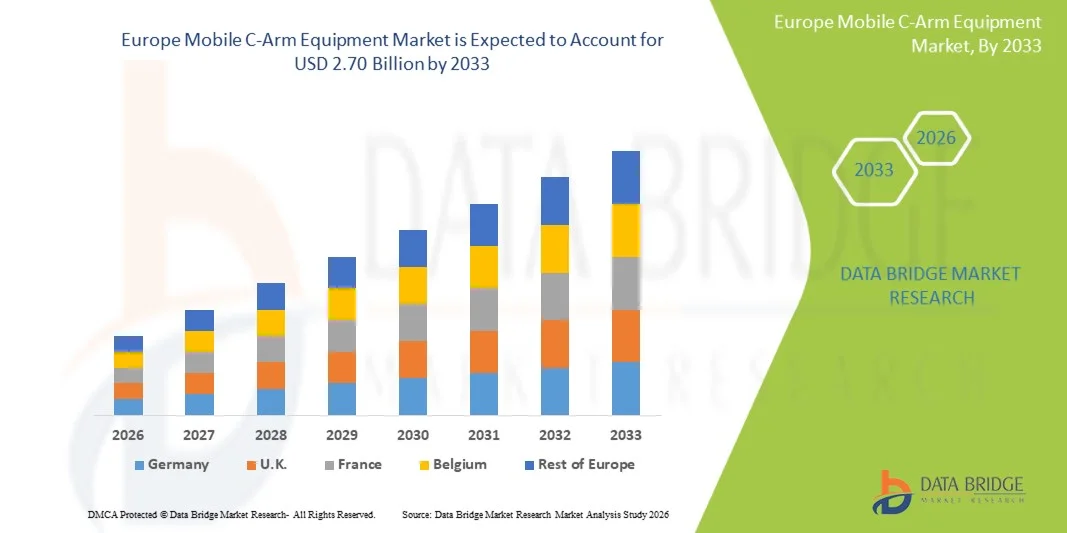

The Europe mobile C-arm equipment market was valued at USD 1.80 billion in 2025 and is projected to reach USD 2.70 billion by 2033, growing at a CAGR of 5.2% from 2026 to 2033. The market is experiencing steady growth driven by the rising volume of minimally invasive surgical procedures, increasing demand for real-time intraoperative imaging, and continuous technological advancements in mobile fluoroscopy systems across hospitals and ambulatory surgical centers.

The growing prevalence of orthopedic disorders, cardiovascular diseases, and trauma-related injuries across Europe, combined with an aging population and expanding healthcare infrastructure, is accelerating the adoption of advanced mobile C-arm systems. Healthcare providers are increasingly investing in flat-panel detector technology, low-dose imaging solutions, and AI-enhanced visualization capabilities to improve procedural accuracy and patient outcomes. In addition, the shift toward outpatient surgeries and image-guided interventions is further strengthening demand for mobile C-arm equipment throughout the region.

Key Market Trends & Insights

- Germany dominated the Europe mobile C-arm equipment market in 2025 with the largest revenue share of 28.6%, supported by a highly advanced hospital network, strong adoption of image-guided surgical systems, and continuous investments in medical imaging technologies.

- The Full-Size C-Arms segment led the market with a 54.2% share in 2025, driven by its widespread use in complex surgical procedures requiring high-resolution imaging and greater anatomical coverage.

- Poland is expected to be the fastest-growing country from 2026 to 2033, expanding at a CAGR of 6.1%, fueled by increasing healthcare modernization programs, rising hospital infrastructure investments, and expanding access to advanced surgical imaging systems.

- 3D Mobile C-Arms are the fastest-growing type, projected to register a CAGR of 6.8%, reflecting the surge in demand for high-precision imaging in complex minimally invasive surgeries.

- The Image Intensifier segment dominated the technology category with a 61.3% revenue share in 2025, led by its widespread installed base and relatively lower acquisition cost compared to newer technologies.

- Orthopedic and Trauma Surgery accounted for 39.8% of the market, preferred by the high incidence of fractures, musculoskeletal disorders, and sports-related injuries across Europe.

- The Neuro Surgery segment is the fastest-growing application category, with a CAGR of 6.9%, driven by the increasing demand for precision imaging in complex brain and spine procedures.

Market Size & Forecast

- Global Market Value (2025): USD 1.80 Billion

- Expected Market Value (2033): USD 2.70 Billion

- Forecast CAGR (2026–2033): 5.2%

- Leading Country in 2025: Germany

- Fastest Growing Country: Poland

Report Scope and Global Europe Mobile C-Arm Equipment Market Segmentation

|

Attributes |

Europe Mobile C-Arm Equipment Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe |

|

Key Market Players |

· Siemens Healthineers AG (Germany) · Koninklijke Philips N.V. (Netherlands) · GE HealthCare (U.S.) · Ziehm Imaging GmbH (Germany) · CANON MEDICAL SYSTEMS CORPORATION (Japan) · Shimadzu Corporation (Japan) · Hologic, Inc. (U.S.) · Orthoscan, Inc. (U.S.) · Eurocolumbus S.r.l. (Italy) · INTERMEDICAL S.r.l. (Italy) · Genoray Co., Ltd. (South Korea) · ECORAY Co., Ltd. (South Korea) · Perlong Medical Equipment Co., Ltd. (China) · Wandong Medical Technology Co., Ltd. (China) · Comermy S.r.l. (Italy) · ITALRAY S.r.l. (Italy) · MS Westfalia GmbH (Germany) · Allengers Medical Systems Limited (India) · DMS Imaging (France) · Villa Sistemi Medicali S.p.A. (Italy) |

|

Market Opportunities |

· Growing adoption of mobile C-arms in ambulatory surgical centers · Rising demand for intraoperative 3D imaging and navigation-assisted surgery · Expanding healthcare infrastructure in emerging economies |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Europe Mobile C-Arm Equipment Market Trends

Trend: Expansion of Image-Guided Minimally Invasive Surgery Adoption

Hospitals across Europe are increasingly integrating mobile C-arm systems into minimally invasive orthopedic, cardiovascular, neurological, and trauma procedures to achieve higher precision and better clinical outcomes. The shift toward image-guided interventions is being driven by the need to reduce surgical complications, shorten hospital stays, and improve procedural efficiency. Advanced flat-panel detector C-arms are replacing older image intensifier systems due to superior resolution, faster imaging, and lower radiation exposure. Surgeons are also leveraging real-time fluoroscopy to make intraoperative decisions with greater accuracy, especially in complex fracture fixation and spinal correction procedures. For instance, major tertiary care hospitals in Germany are deploying hybrid operating rooms equipped with high-end mobile C-arms to support multi-specialty surgical workflows.

Europe Mobile C-Arm Equipment Market Dynamics

Key Market Driver: Rising Burden of Orthopedic and Chronic Diseases

The increasing prevalence of musculoskeletal disorders, osteoporosis, cardiovascular diseases, and age-related degenerative conditions is significantly boosting demand for mobile C-arm systems across Europe. The region’s rapidly aging population is leading to a higher number of surgical interventions, particularly in orthopedic and trauma care. In addition, the growing incidence of sports injuries and road accidents is further expanding the need for real-time intraoperative imaging solutions. Healthcare providers are investing in advanced mobile imaging systems to improve diagnostic accuracy and support complex surgical procedures with minimal invasiveness. For instance, orthopedic hospitals in France and Italy are increasingly using C-arm systems for joint replacement, spinal surgeries, and fracture management procedures.

Key Restraint/Challenge: High Equipment Cost and Maintenance Burden

Despite strong demand, the market faces a significant challenge due to the high upfront cost of advanced mobile C-arm systems, particularly those equipped with flat-panel detectors, 3D imaging capabilities, and AI-enabled functionalities. In addition to procurement costs, hospitals must also bear expenses related to installation, calibration, radiation shielding compliance, and regular maintenance. Software licensing, periodic upgrades, and training requirements further increase the total cost of ownership, making it difficult for smaller healthcare facilities to adopt the latest systems. Budget limitations in public healthcare systems across several European countries also delay equipment replacement cycles. For instance, smaller regional hospitals in Spain and Portugal often continue using older fluoroscopy systems due to capital constraints.

Key Market Opportunity: Integration of AI-Driven Imaging and Workflow Optimization

The integration of artificial intelligence and advanced software algorithms into mobile C-arm systems presents a major opportunity to transform intraoperative imaging workflows. AI-enabled systems can enhance image reconstruction, automatically optimize radiation dose, and assist surgeons in real-time anatomical visualization during complex procedures. These technologies also support predictive analytics, improving surgical planning and reducing procedural risks. Furthermore, integration with hospital information systems and surgical navigation platforms is improving overall workflow efficiency and reducing operation time. For instance, leading medical centers in the Netherlands and Sweden are adopting AI-assisted C-arm solutions to support precision-driven spinal and neurovascular procedures, enhancing both safety and surgical accuracy.

Europe Mobile C-Arm Equipment Market Scope

The Europe mobile C-arm equipment market is segmented on the basis of type, technology, application, end user, and distribution channel.

- By Type

On the basis of type, the Europe mobile C-arm equipment market is segmented into mini C-arms, full-size C-arms, 2D mobile C-arms, 3D mobile C-arms, and hybrid mobile C-arms. The Full-Size C-Arms segment dominated the market with a 54.2% share in 2025, owing to its widespread use in complex surgical procedures requiring high-resolution imaging and greater anatomical coverage. These systems are extensively deployed in orthopedic, cardiovascular, and trauma surgeries where precision imaging is critical for procedural success. Hospitals prefer full-size systems due to their versatility across multiple departments and compatibility with advanced imaging software. Continuous improvements in image quality, mobility, and radiation dose reduction are further strengthening adoption. Increasing surgical volumes across Europe are also reinforcing demand for these systems. Their ability to support both routine and complex interventions makes them the most widely used type segment.

The 3D Mobile C-Arms segment is expected to witness the fastest growth at a CAGR of 6.8% from 2026 to 2033, driven by rising demand for high-precision imaging in complex minimally invasive surgeries. These systems provide volumetric imaging capabilities, enabling surgeons to visualize anatomical structures in greater detail during procedures. Their adoption is increasing in spine surgery, neurovascular interventions, and advanced orthopedic procedures. Technological advancements in reconstruction algorithms and imaging speed are improving clinical efficiency. Growing preference for real-time intraoperative 3D visualization is further supporting growth. Expanding use in hybrid operating rooms is also accelerating market penetration.

- By Technology

On the basis of technology, the Europe mobile C-arm equipment market is segmented into image intensifiers and flat panel detector systems. The Image Intensifier segment dominated the market with a 61.3% share in 2025, due to its widespread installed base and relatively lower acquisition cost compared to newer technologies. These systems have been traditionally used across hospitals for routine imaging and general surgical procedures. Their reliability and familiarity among medical professionals continue to support steady demand. Maintenance costs are relatively lower in existing infrastructure, making them a preferred option in budget-constrained healthcare settings. However, gradual replacement by advanced systems is occurring in major hospitals. Despite technological limitations, they remain widely used in secondary care centers.

The Flat Panel Detector segment is expected to witness the fastest growth at a CAGR of 7.1% from 2026 to 2033, driven by superior image quality, lower radiation exposure, and faster image processing capabilities. These systems provide enhanced contrast resolution, making them ideal for minimally invasive and high-precision surgeries. Increasing adoption in advanced hospitals and specialty surgical centers is accelerating growth. Continuous technological improvements are reducing system costs and improving accessibility. Integration with AI-based imaging and navigation systems is further enhancing clinical utility. Growing focus on patient safety and diagnostic accuracy is strongly supporting adoption.

- By Application

On the basis of application, the Europe mobile C-arm equipment market is segmented into orthopedic and trauma surgeries, cardiovascular surgeries, neuro surgeries, gastrointestinal surgeries, pain management, general surgery, urology, and others. The Orthopedic and Trauma Surgery segment dominated the market with a 39.8% share in 2025, due to the high incidence of fractures, musculoskeletal disorders, and sports-related injuries across Europe. Mobile C-arms are extensively used for fracture fixation, joint replacement, and spinal correction procedures. The aging population further increases demand for orthopedic interventions. High procedural volume and routine use of intraoperative imaging support this segment’s dominance. Hospitals rely heavily on C-arms for real-time surgical guidance. Continuous advancements in orthopedic surgical techniques are further strengthening demand.

The Neuro Surgery segment is expected to witness the fastest growth at a CAGR of 6.9% from 2026 to 2033, driven by increasing demand for precision imaging in complex brain and spine procedures. Mobile C-arms are increasingly used in minimally invasive neurosurgical interventions requiring high spatial accuracy. Growing adoption of image-guided surgery and hybrid operating rooms is accelerating usage. Rising prevalence of neurological disorders and spinal conditions is further supporting growth. Technological advancements in 3D imaging and navigation integration are enhancing surgical outcomes. Expanding investments in neurosurgical infrastructure across Europe are also boosting adoption.

- By End User

On the basis of end user, the Europe mobile C-arm equipment market is segmented into hospitals, diagnostic centers, specialty clinics, and others. The Hospitals segment dominated the market with a 62.5% share in 2025, owing to high patient inflow, availability of advanced surgical infrastructure, and presence of multi-specialty departments. Hospitals conduct a large number of complex surgeries requiring intraoperative imaging support. Continuous investment in advanced imaging technologies strengthens their dominance. Availability of trained medical professionals further supports equipment utilization. Government funding and healthcare modernization programs also drive procurement. Hospitals remain the primary adoption point for high-end mobile C-arm systems.

The Specialty Clinics segment is expected to witness the fastest growth at a CAGR of 6.6% from 2026 to 2033, driven by increasing shift toward outpatient surgical procedures and minimally invasive treatments. These clinics are adopting mobile C-arms to support orthopedic, pain management, and urology procedures. Lower operational costs and faster patient turnover make them attractive for advanced imaging adoption. Technological advancements are making compact systems more suitable for smaller facilities. Rising preference for day-care surgeries is further accelerating demand. Expansion of private healthcare infrastructure across Europe is also supporting growth.

- By Distribution Channel

On the basis of distribution channel, the Europe mobile C-arm equipment market is segmented into direct tender and retail sales. The Direct Tender segment dominated the market with a 68.4% share in 2025, due to large-scale procurement by public hospitals and government healthcare systems. Bulk purchasing agreements ensure cost efficiency and standardized equipment deployment across facilities. Hospitals prefer direct procurement from manufacturers for better pricing and long-term service agreements. Government-funded healthcare modernization programs further support this channel. High-value imaging systems are predominantly acquired through tender processes. Strong manufacturer-hospital relationships reinforce this segment’s dominance.

The Retail Sales segment is expected to witness the fastest growth at a CAGR of 6.3% from 2026 to 2033, driven by increasing adoption among private clinics and specialty diagnostic centers. Smaller healthcare providers prefer retail procurement due to flexibility and faster acquisition cycles. Growing number of private healthcare facilities is supporting demand. Financing options and leasing models are making high-cost equipment more accessible. Increasing demand for outpatient imaging services is further accelerating growth. Expansion of private healthcare networks across Europe is strengthening this channel.

Europe Mobile C-Arm Equipment Market Regional Analysis

Germany dominated the Europe mobile C-arm equipment market in 2025 with the largest revenue share of 28.6%, supported by a highly advanced hospital network, strong adoption of image-guided surgical systems, and continuous investments in medical imaging technologies. The country benefits from a high concentration of specialized surgical centers performing orthopedic, cardiovascular, and trauma procedures that require real-time intraoperative imaging. Continuous investments in hospital modernization, hybrid operating rooms, and digital imaging solutions are further strengthening market growth. Germany also hosts several leading medical device manufacturers and R&D facilities, supporting rapid technology adoption and innovation. Increasing demand for minimally invasive surgeries and precision-guided procedures continues to reinforce Germany’s leadership position in the European market.

The Germany Mobile C-Arm Equipment Market Insight

The Germany mobile C-arm equipment market is witnessing strong growth due to advanced healthcare infrastructure, high surgical volumes, and early adoption of image-guided surgical technologies. The country’s well-established hospital network and leading role in medical device innovation are driving demand for high-performance mobile C-arms. Increasing utilization in orthopedic, cardiovascular, and trauma procedures is further supporting market expansion. Growing investments in hybrid operating rooms and digital imaging systems are accelerating technology adoption. In addition, strong focus on precision surgery and patient safety is reinforcing consistent market growth across Germany.

France Mobile C-Arm Equipment Market Insight

The France mobile C-arm equipment market is experiencing steady growth, supported by rising healthcare modernization initiatives and increasing demand for minimally invasive surgical procedures. Hospitals are increasingly adopting advanced imaging systems to improve surgical accuracy and reduce patient recovery time. The presence of a strong public healthcare system is driving large-scale procurement of mobile C-arms. Expanding use in orthopedic and trauma surgeries is further strengthening market demand. Moreover, integration of digital imaging and AI-based surgical support tools is enhancing procedural efficiency across healthcare facilities.

United Kingdom Mobile C-Arm Equipment Market Insight

The United Kingdom mobile C-arm equipment market is growing steadily, driven by strong adoption of advanced surgical imaging technologies and increasing investment in healthcare infrastructure. The NHS and private healthcare providers are increasingly deploying mobile C-arms for orthopedic, vascular, and emergency surgeries. Rising demand for minimally invasive procedures is further supporting market expansion. Technological advancements such as flat-panel detectors and low-dose imaging systems are gaining traction. In addition, growing focus on surgical precision and workflow efficiency is boosting adoption across hospitals and specialty clinics.

Poland Mobile C-Arm Equipment Market Insight

The Poland mobile C-arm equipment market is witnessing rapid growth due to ongoing healthcare modernization and increasing investments in hospital infrastructure. Rising demand for advanced diagnostic and surgical imaging systems is driving adoption across public and private hospitals. The growing burden of orthopedic and trauma cases is further supporting market expansion. Mobile C-arms are increasingly being used to improve surgical precision and reduce procedure times. In addition, improving access to advanced medical technologies is positioning Poland as one of the fastest-growing markets in Europe.

Europe Mobile C-Arm Equipment Market Share

The Europe mobile C-arm equipment industry is primarily led by well-established companies, including:

- Siemens Healthineers AG (Germany)

- Koninklijke Philips N.V. (Netherlands)

- GE HealthCare (U.S.)

- Ziehm Imaging GmbH (Germany)

- CANON MEDICAL SYSTEMS CORPORATION (Japan)

- Shimadzu Corporation (Japan)

- Hologic, Inc. (U.S.)

- Orthoscan, Inc. (U.S.)

- Eurocolumbus S.r.l. (Italy)

- INTERMEDICAL S.r.l. (Italy)

- Genoray Co., Ltd. (South Korea)

- ECORAY Co., Ltd. (South Korea)

- Perlong Medical Equipment Co., Ltd. (China)

- Wandong Medical Technology Co., Ltd. (China)

- Comermy S.r.l. (Italy)

- ITALRAY S.r.l. (Italy)

- MS Westfalia GmbH (Germany)

- Allengers Medical Systems Limited (India)

- DMS Imaging (France)

- Villa Sistemi Medicali S.p.A. (Italy)

Latest Developments in Europe Mobile C-Arm Equipment Market

- In October 2025, Philips announced the 5,000th installation of its Zenition mobile C-arm system at Kolín Regional Hospital in the Czech Republic, marking a major milestone in intraoperative imaging adoption across Europe and globally. The Zenition platform has been widely used in minimally invasive surgeries, supporting more than 15 million patients annually across 170+ countries. This milestone highlights strong European demand for advanced mobile C-arm systems driven by efficiency needs in hybrid operating rooms and surgical precision requirements. It also reflects growing reliance on standardized imaging platforms for orthopedic and interventional procedures

- In March 2024, Siemens Healthineers received FDA clearance for its CIARTIC Move self-driving mobile C-arm system, which introduces automated positioning and workflow standardization for intraoperative imaging. Although cleared in the U.S., the innovation is highly relevant to Europe due to Siemens’ strong installed base across European hospitals. The system is designed for orthopedic, trauma, spine, and general surgery applications, improving imaging speed and consistency in operating rooms. It reduces manual handling and enhances surgical workflow efficiency

- In February 2024, Philips launched the Zenition 90 Motorized mobile C-arm system, designed to improve workflow automation and surgical imaging precision in complex procedures such as cardiovascular, urology, and orthopedic surgeries. The system introduced motorized control, advanced imaging quality, and automated positioning features that reduce dependence on manual operation inside operating rooms. This innovation is particularly relevant for Europe, where hospitals are increasingly adopting efficiency-driven surgical imaging solutions. The system also supports dose reduction and enhanced visualization in minimally invasive surgeries

- In September 2023, Philips expanded its mobile C-arm portfolio with the Zenition 30 system, aimed at improving access to high-quality intraoperative imaging for routine surgical procedures. The system introduced advanced imaging algorithms, ease-of-use features, and improved workflow personalization, making it suitable for hospitals facing staff shortages. It supports a wide range of applications including orthopedics, trauma, spine, and pain management procedures. In Europe, this system strengthened adoption in mid-sized hospitals seeking cost-effective but advanced imaging solutions

- In March 2023, Philips introduced the Zenition 10 mobile C-arm system, expanding its portfolio with a cost-effective flat-panel detector-based solution for routine surgeries. The system was designed to improve access to high-quality imaging in minimally invasive and general surgical procedures while reducing operational costs for hospitals. It strengthened adoption of mobile C-arms in Europe by addressing demand for affordable yet advanced imaging technologies. The system also contributed to improved patient outcomes through better imaging clarity and dose efficiency

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.