Europe Mri Scanner Market

Market Size in USD Billion

USD

1.72 Billion

USD

2.90 Billion

2025

2033

USD

1.72 Billion

USD

2.90 Billion

2025

2033

| 2026 - 2033 | |

| USD 1.72 Billion | |

| USD 2.90 Billion | |

| % | |

|

Europe MRI Scanner Market Size

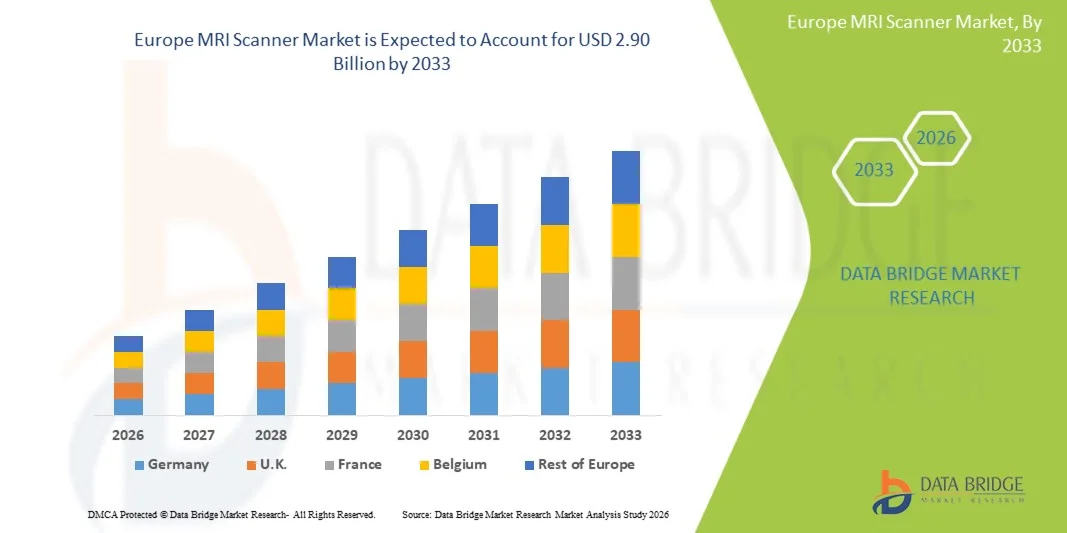

- The Europe MRI Scanner Market size was valued at USD 1.72 billion in 2025 and is expected to reach USD 2.90 billion by 2033, at a CAGR of 6.76% during the forecast period

- The market growth is largely fueled by the growing adoption of advanced diagnostic imaging technologies, rising prevalence of chronic and neurological diseases, and continuous modernization of healthcare infrastructure across hospitals and diagnostic centers

- Furthermore, increasing demand for accurate, non-invasive diagnostic tools and the expansion of medical imaging facilities is establishing MRI scanners as essential equipment in modern clinical practice. These converging factors are accelerating the uptake of MRI Scanner solutions, thereby significantly boosting the industry's growth

Europe MRI Scanner Market Analysis

- MRI scanners, offering high-resolution, non-invasive diagnostic imaging, are increasingly vital components of modern healthcare systems in both hospitals and diagnostic centers due to their ability to detect a wide range of neurological, musculoskeletal, cardiovascular, and oncological conditions

- The escalating demand for MRI scanners is primarily fueled by rising prevalence of chronic and neurological diseases, increasing investments in healthcare infrastructure, and growing focus on early and accurate diagnosis

- The U.K. dominated the Europe MRI Scanner Market with the largest revenue share of 29.4% in 2025, supported by a well-established healthcare system, widespread availability of MRI scanners across NHS hospitals and private diagnostic centers, and strong adoption of advanced imaging technologies. Increasing MRI scan volumes, government funding for diagnostic capacity expansion, and ongoing replacement of aging MRI equipment with high-field and AI-enabled systems continue to reinforce the U.K.’s market leadership

- Germany is expected to be the fastest-growing market in the MRI Scanner industry during the forecast period, registering a CAGR of 7.9%, driven by rising healthcare expenditure, rapid technological advancements in MRI systems, and growing demand for high-quality diagnostic imaging. Expansion of hospital infrastructure, strong clinical research activity, and increasing adoption of high-field and specialized MRI scanners for oncology, neurology, and cardiovascular applications are accelerating market growth across the country

- The closed MRI systems segment accounted for the largest market revenue share of 62.7% in 2025, owing to its superior imaging performance and high magnetic field strength

Report Scope and Europe MRI Scanner Market Segmentation

|

Attributes |

MRI Scanner Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Europe

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Europe MRI Scanner Market Trends

“Global Shift Toward High-Field, Specialized, and Patient-Centric MRI Systems”

- A prominent global trend in the Europe MRI Scanner Market is the accelerating adoption of high-field MRI systems, particularly 3T scanners, across developed and emerging healthcare systems

- These systems offer superior image resolution, faster scan times, and enhanced diagnostic confidence, making them increasingly preferred for neurological, musculoskeletal, cardiovascular, and oncological imaging worldwide

- Healthcare providers globally are also moving toward specialized MRI systems designed for specific clinical applications such as breast MRI, cardiac MRI, and pediatric imaging. This specialization is enabling hospitals and diagnostic centers to improve diagnostic accuracy while optimizing workflow efficiency

- For instance, large hospital networks in North America and Europe are expanding their MRI fleets with dedicated cardiac and neuro MRI systems to support advanced disease management and research programs. At the same time, emerging markets in Europe and Latin America are rapidly adopting mid- to high-field MRI scanners to expand access to advanced diagnostics

- Another notable trend is the global emphasis on patient-centric MRI design, including wider bores, shorter tunnels, quieter scanning technologies, and faster imaging protocols. These features significantly reduce patient discomfort, claustrophobia, and motion artifacts, improving overall scan success rates

- Furthermore, healthcare systems worldwide are increasingly prioritizing operational efficiency and throughput, leading to the adoption of MRI scanners capable of high patient volumes without compromising image quality. This is particularly evident in high-demand diagnostic hubs in urban regions

- Overall, this global shift toward advanced, specialized, and patient-friendly MRI solutions is reshaping procurement strategies and influencing long-term investments across public and private healthcare providers

Europe MRI Scanner Market Dynamics

Driver

“Rising Global Burden of Chronic Diseases and Expanding Diagnostic Infrastructure”

- The growing prevalence of chronic diseases such as cancer, cardiovascular disorders, neurological conditions, and musculoskeletal ailments is a primary driver of the global Europe MRI Scanner Market. MRI remains a critical diagnostic tool due to its non-invasive nature and superior soft-tissue contrast

- Worldwide increases in aging populations, particularly in North America, Europe, Japan, and China, are significantly driving demand for frequent and advanced imaging procedures, including MRI scans for age-related conditions

- Governments across regions are investing heavily in healthcare infrastructure to strengthen early disease detection and reduce long-term treatment costs

- For instance, multiple national healthcare modernization programs launched between 2022 and 2024 in Europe and the Middle East included funding for advanced diagnostic imaging equipment such as MRI scanner

- The expansion of private diagnostic imaging centers globally is another major growth driver. These centers are increasingly adopting advanced MRI scanners to differentiate their services, reduce waiting times, and attract high patient volumes

- In addition, the growing penetration of health insurance coverage and reimbursement policies for advanced diagnostic imaging in both developed and developing economies is improving patient access to MRI services, further supporting market growth

- The increasing emphasis on preventive healthcare, early diagnosis, and precision medicine worldwide continues to reinforce the critical role of MRI scanners in modern healthcare delivery systems

Restraint/Challenge

“High Capital Costs, Operational Complexity, and Infrastructure Limitations”

- Despite strong demand, the global Europe MRI Scanner Market faces significant challenges related to the high capital investment required for system acquisition, installation, and maintenance. Advanced MRI scanners involve substantial upfront costs, making them less accessible for small hospitals, rural healthcare facilities, and budget-constrained regions

- In many developing and underdeveloped markets, limited healthcare infrastructure, including inadequate power supply, space constraints, and cooling requirements, restrict the deployment of MRI scanners. This limits market penetration outside major urban centers

- Operational challenges, including the need for highly trained radiologists, MRI technologists, and service engineers, further hinder adoption. Several regions, particularly in parts of Africa, Southeast Asia, and Latin America, continue to face shortages of skilled personnel capable of operating and maintaining advanced MRI systems

- For instance, healthcare providers in emerging economies often report underutilization of MRI scanners due to workforce constraints and high operational expenses, despite rising patient demand

- In addition, ongoing costs related to system upgrades, software maintenance, and compliance with regulatory standards add to the financial burden for healthcare providers globally

- Addressing these challenges will require collaborative efforts among manufacturers, governments, and healthcare institutions, including flexible financing models, workforce training initiatives, and the development of cost-effective MRI solutions tailored for diverse global healthcare settings

Europe MRI Scanner Market Scope

The market is segmented on the basis of type, product, application, end user, and distribution channel.

• By Type

On the basis of type, the Europe MRI Scanner Market is segmented into portable type and desktop type. The desktop type segment dominated the largest market revenue share of 58.4% in 2025, driven by its extensive adoption across hospitals and large diagnostic imaging centers. Desktop MRI scanners provide higher magnetic field strength, enabling superior image clarity and diagnostic accuracy for complex clinical conditions. These systems are widely used for neurology, oncology, and musculoskeletal imaging where precision is critical. Their ability to support advanced imaging sequences such as functional MRI and diffusion imaging further strengthens demand. Desktop MRI systems are compatible with both closed and open configurations, enhancing flexibility. High patient throughput capability supports their use in high-volume healthcare facilities. Long operational lifespan and strong manufacturer support also contribute to dominance. Continuous technological upgrades in gradient and RF systems improve performance. Integration with hospital IT and PACS systems ensures workflow efficiency. Availability of skilled operators favors deployment in tertiary hospitals. Strong reimbursement coverage in developed markets further supports adoption. Collectively, these factors sustain the dominance of desktop MRI scanners globally.

The portable type segment is expected to witness the fastest CAGR of 19.2% from 2026 to 2033, driven by the growing demand for point-of-care diagnostics and mobile healthcare solutions. Portable MRI scanners offer compact design and ease of mobility, allowing imaging in ICUs, emergency rooms, and remote locations. They reduce patient transfer risks, particularly for critically ill and pediatric patients. Lower installation and infrastructure costs make them attractive to small healthcare facilities. Rising adoption in rural and underserved regions supports growth. Technological advancements are improving image quality despite smaller size. Increasing use in neurological emergencies such as stroke diagnosis boosts demand. Military and disaster-response applications further expand usage. Government initiatives supporting mobile healthcare strengthen adoption. Growing focus on decentralized healthcare models fuels market expansion. Increasing acceptance among clinicians enhances credibility. These combined factors drive rapid growth of portable MRI scanners.

• By Product

On the basis of product, the Europe MRI Scanner Market is segmented into closed MRI systems and open MRI systems. The closed MRI systems segment accounted for the largest market revenue share of 62.7% in 2025, owing to its superior imaging performance and high magnetic field strength. Closed MRI systems deliver exceptional signal-to-noise ratio, enabling accurate detection of tumors, neurological disorders, and cardiovascular abnormalities. They are widely preferred in tertiary hospitals and research institutions. Compatibility with advanced imaging protocols supports complex diagnostic procedures. These systems are essential for oncology staging and neurological assessments. High reliability and standardized performance enhance clinical confidence. Strong manufacturer presence ensures consistent upgrades and maintenance. Closed MRI systems support high patient throughput. Reimbursement policies favor their use in advanced diagnostics. Availability of skilled radiologists supports adoption. Continuous innovation in gradient strength and cooling systems enhances efficiency. These factors collectively maintain dominance in the global market.

The open MRI systems segment is projected to witness the fastest CAGR of 18.5% from 2026 to 2033, driven by increasing emphasis on patient comfort and accessibility. Open MRI systems reduce claustrophobia, making them suitable for elderly, pediatric, and obese patients. Growing preference for patient-centric care models boosts adoption. Advancements in open MRI technology are improving image quality and scan speed. Increased use in outpatient clinics and diagnostic centers supports growth. Open systems allow easier positioning for musculoskeletal imaging. Rising awareness among patients enhances acceptance. Demand is strong in orthopedic and sports medicine applications. Lower anxiety improves scan completion rates. Expanding private diagnostic centers favor open MRI installations. Technological improvements reduce performance gaps with closed systems. These factors collectively drive rapid market growth.

• By Application

On the basis of application, the Europe MRI Scanner Market is segmented into oncology, neurology, cardiology, pelvic and abdominal, musculoskeletal, and other applications. The neurology segment dominated the largest market revenue share of 41.3% in 2025, driven by the rising prevalence of neurological disorders worldwide. MRI scanners are essential for diagnosing brain tumors, stroke, epilepsy, and multiple sclerosis. Growing aging population increases demand for neurological imaging. High accuracy and non-invasive nature support clinical preference. Functional MRI plays a critical role in brain mapping. Increased use in trauma and emergency care boosts demand. Neurology departments require frequent follow-up imaging. Technological advancements improve visualization of brain structures. Research activities further expand usage. Strong reimbursement policies support adoption. Hospitals prioritize MRI for neurological diagnostics. Collectively, these factors drive segment dominance.

The oncology segment is expected to register the fastest CAGR of 17.8% from 2026 to 2033, fueled by rising global cancer incidence. MRI scanners are increasingly used for tumor detection, staging, and treatment monitoring. Growing preference for radiation-free imaging supports demand. MRI plays a vital role in breast, prostate, and pelvic cancers. Advances in contrast-enhanced imaging improve tumor visualization. Cancer care centers invest heavily in advanced MRI systems. Rising adoption in personalized treatment planning supports growth. MRI is used for therapy response assessment. Increasing screening programs drive imaging demand. Technological innovation improves diagnostic accuracy. Expanding oncology infrastructure boosts adoption. These factors contribute to strong growth momentum.

• By End User

On the basis of end user, the Europe MRI Scanner Market is segmented into hospital, clinic, ambulatory surgical centres, scientific research, and others. The hospital segment held the largest market revenue share of 49.6% in 2025, driven by high patient volumes and advanced diagnostic infrastructure. Hospitals perform a wide range of MRI procedures across multiple specialties. Availability of skilled professionals supports complex imaging. Hospitals invest in high-field MRI scanners for accuracy. Emergency and inpatient imaging drives demand. Strong financial capacity enables procurement of advanced systems. Integration with hospital information systems enhances efficiency. Continuous patient inflow supports high utilization rates. Hospitals serve as referral centers for imaging. Government funding supports hospital MRI installations. Teaching hospitals drive research-based imaging. These factors sustain hospital dominance.

The ambulatory surgical centres segment is expected to witness the fastest CAGR of 16.9% from 2026 to 2033, driven by the shift toward outpatient care. These centers focus on cost-effective and efficient diagnostic services. MRI scanners support preoperative and postoperative imaging. Rising number of minimally invasive procedures boosts demand. Shorter patient stay enhances workflow efficiency. Increasing private investments support expansion. Lower operational costs encourage MRI adoption. Patient convenience supports outpatient imaging growth. Technological advancements enable compact MRI systems. Growing insurance coverage supports usage. Expansion of day-care surgeries fuels demand. These drivers accelerate growth in this segment.

• By Distribution Channel

On the basis of distribution channel, the Europe MRI Scanner Market is segmented into direct tender and retail sales. The direct tender segment dominated the largest market revenue share of 53.2% in 2025, driven by bulk procurement by hospitals and government institutions. Direct tenders enable cost-effective purchasing and long-term contracts. Large healthcare systems prefer tender-based procurement. Government-funded projects rely heavily on tenders. Service and maintenance agreements enhance value. Transparent pricing supports adoption. High-volume purchases reduce per-unit costs. Tenders ensure standardized equipment deployment. Public hospitals favor direct procurement. Long-term supplier relationships strengthen reliability. Vendor credibility plays a key role. These factors support dominance.

The retail sales segment is expected to grow at the fastest CAGR of 15.4% from 2026 to 2033, driven by expansion of private diagnostic centers. Retail sales offer flexible purchasing options. Smaller clinics prefer retail channels. Faster procurement supports quicker installation. Growing demand for portable and open MRI systems boosts retail sales. Private healthcare expansion supports growth. Financing options improve accessibility. Increased competition among vendors strengthens retail presence. Diagnostic chains favor decentralized procurement. Customizable solutions attract buyers. Rising healthcare privatization supports adoption. These factors collectively drive rapid growth.

Europe MRI Scanner Market Regional Analysis

- Europe is expected to be one of the fastest-growing Europe MRI Scanner Markets during the forecast period, with a projected CAGR of 7.6% from 2026 to 2033, driven by rising healthcare expenditure, aging populations, and increasing demand for advanced diagnostic imaging across hospitals and diagnostic centers. Continuous investments in healthcare infrastructure, replacement of aging MRI systems, and growing adoption of high-field and AI-enabled MRI scanners are supporting market expansion across the region

- Technological advancements, including high-field (3T and above) systems, AI-assisted imaging, and multi-channel MRI scanners, are accelerating adoption across Europe. Government funding programs, strong regulatory frameworks ensuring high diagnostic standards, and increasing focus on early disease detection—particularly for neurological, oncological, and cardiovascular conditions—are further strengthening regional growth

- While the U.K. leads in overall market share due to widespread MRI availability and high scan volumes, Germany is emerging as the fastest-growing country owing to rapid technology adoption and strong clinical research activity. Collectively, Europe remains a major hub for advanced MRI Scanner deployment and innovation

U.K. Europe MRI Scanner Market Insight

The U.K. Europe MRI Scanner Market dominated the European market with the largest revenue share of 29.4% in 2025, supported by a well-established healthcare system and extensive deployment of MRI scanners across NHS hospitals and private diagnostic centers. Increasing MRI scan volumes, driven by rising diagnostic demand for neurological, musculoskeletal, and oncological conditions, are fueling steady utilization of MRI systems. Government funding for diagnostic capacity expansion and structured programs aimed at reducing imaging backlogs are accelerating the replacement of aging MRI equipment with high-field and AI-enabled scanners. Strong adoption of advanced imaging technologies and centralized procurement within the NHS continue to reinforce the U.K.’s leadership position in the European Europe MRI Scanner Market.

Germany Europe MRI Scanner Market Insight

Germany Europe MRI Scanner Market is expected to be the fastest-growing market in the MRI Scanner industry in Europe, registering a CAGR of 7.9% during the forecast period. Growth is driven by rising healthcare expenditure, rapid technological advancements in MRI systems, and increasing demand for high-quality diagnostic imaging across hospitals and specialized diagnostic centers. Germany’s strong clinical research ecosystem, expanding hospital infrastructure, and emphasis on early disease detection are accelerating adoption of high-field, application-specific, and AI-integrated MRI scanners. Additionally, growing demand for advanced imaging in oncology, neurology, and cardiovascular applications, combined with precision medicine initiatives, is further supporting robust market growth across the country.

Europe MRI Scanner Market Share

The MRI Scanner industry is primarily led by well-established companies, including:

- GE HealthCare (U.S.)

- Siemens Healthineers (Germany)

- Philips Healthcare (Netherlands)

- Canon Medical Systems Corporation (Japan)

- Fujifilm Healthcare (Japan)

- United Imaging Healthcare (China)

- Hitachi Healthcare (Japan)

- Esaote S.p.A. (Italy)

- Neusoft Medical Systems (China)

- Mindray Medical International (China)

- Shimadzu Corporation (Japan)

- Bruker Corporation (U.S.)

- Aspect Imaging (Israel)

- Time Medical Systems (Hong Kong)

- IMRIS (Canada)

- AllTech Medical Systems (China)

- Aurora Imaging Technology (U.S.)

- Paramed Medical Systems (Italy)

- SternMed GmbH (Germany)

- MR Solutions Ltd. (U.K.)

Latest Developments in Europe MRI Scanner Market

- In March 2021, GE Healthcare, a leading global medical technology company, announced the launch of its SIGNA Voyager AIR Edition MRI system, designed to enhance patient comfort and workflow efficiency. The system incorporates lightweight AIR™ coils, advanced gradient performance, and automation features to improve image quality while reducing scan times, supporting a wide range of clinical applications including neurology, orthopedics, and oncology

- In June 2022, Siemens Healthineers, a global leader in medical imaging, introduced the MAGNETOM Free.Star 0.55T MRI scanner, developed to improve access to MRI imaging with lower installation and operating costs. The system uses a helium-light magnet and energy-efficient technology, enabling deployment in smaller hospitals and emerging markets while maintaining diagnostic image quality

- In November 2022, Canon Medical Systems announced the global launch of its Vantage Galan 3T / Supreme Edition MRI system, featuring advanced gradient technology and AI-driven workflow solutions. The system is designed to deliver high-resolution imaging with reduced acoustic noise and faster scan times, improving diagnostic confidence and patient experience across neurological and musculoskeletal imaging

- In April 2023, Philips Healthcare, a major provider of diagnostic imaging solutions, announced the expansion of its BlueSeal helium-free MRI portfolio, highlighting sustainability and operational efficiency. The BlueSeal MRI systems eliminate the need for helium refills and incorporate AI-enabled SmartSpeed technology to accelerate scan times while maintaining image quality, supporting hospitals in reducing environmental impact and operating costs

- In November 2023, GE Healthcare unveiled enhancements to its SIGNA™ Hero 3.0T MRI platform at RSNA 2023, integrating AI-powered image reconstruction and deep-learning-based automation. These upgrades improve image clarity, reduce motion artifacts, and enhance workflow productivity, enabling faster diagnosis in high-volume clinical environments

- In May 2024, United Imaging Healthcare announced new advancements in its MRI scanner portfolio at the International Society for Magnetic Resonance in Medicine (ISMRM) 2024 meeting. The company showcased ultra-high-performance gradient systems and native AI-enabled imaging technologies aimed at improving motion visualization and expanding MRI applications in neurology and cardiovascular imaging

- In December 2024, Siemens Healthineers launched the MAGNETOM Flow. Platform, a next-generation 1.5T MRI system designed for high efficiency and sustainability. The system features a wide-bore design, AI-assisted imaging workflows, and near-zero helium consumption, enabling improved patient throughput and reduced environmental footprint for healthcare providers

- In February 2025, Philips Healthcare announced the rollout of its SmartSpeed Precise dual-AI MRI technology across its MRI scanner portfolio. This innovation combines AI-driven image reconstruction and scan acceleration to significantly reduce examination times while enhancing image sharpness, supporting improved clinical decision-making and patient comfort

- In November 2025, Philips Healthcare unveiled BlueSeal Horizon, the world’s first helium-free 3.0T MRI scanner, at RSNA 2025. The system integrates advanced AI automation, real-time scan preview, and enhanced gradient performance to deliver high-resolution imaging for complex applications such as cardiac, oncology, and neurological diagnostics, reinforcing Philips’ leadership in sustainable MRI technology

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.