Europe Neurosurgery Market

Market Size in USD Billion

USD

4.08 Billion

USD

11.47 Billion

2025

2033

USD

4.08 Billion

USD

11.47 Billion

2025

2033

| 2026 - 2033 | |

| USD 4.08 Billion | |

| USD 11.47 Billion | |

| % | |

|

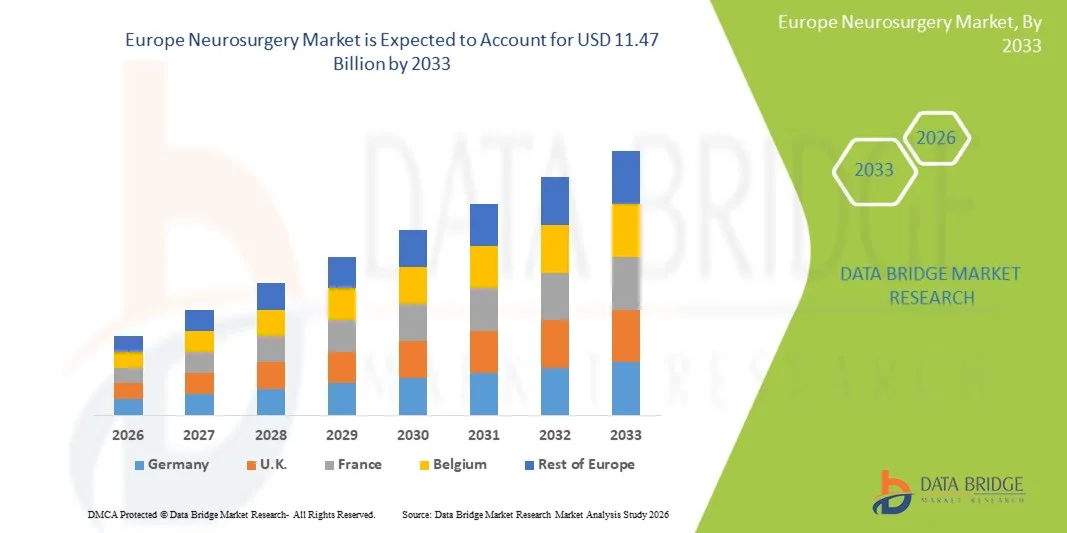

Europe Neurosurgery Market Size

- The Europe Neurosurgery Market size was valued at USD 4.08 billion in 2025 and is expected to reach USD 11.47 billion by 2033, at a CAGR of 13.80% during the forecast period

- The market growth is largely fueled by the increasing prevalence of neurological disorders such as brain tumors, epilepsy, Parkinson’s disease, and trauma-related injuries, along with rising demand for advanced surgical interventions, leading to greater adoption of neurosurgery procedures across hospitals and specialty centers

- Furthermore, continuous advancements in neurosurgical technologies such as minimally invasive surgery, robotic-assisted procedures, neuronavigation systems, and improved imaging techniques are enhancing surgical precision and patient outcomes. Growing investments in healthcare infrastructure and rising awareness regarding early diagnosis and treatment of neurological conditions are establishing neurosurgery as a critical component of modern healthcare delivery. These converging factors are accelerating the uptake of neurosurgery solutions, thereby significantly boosting the industry’s growth

Europe Neurosurgery Market Analysis

- Neurosurgery, involving complex surgical procedures for disorders of the brain, spine, and peripheral nerves, is a critical field of medical care supported by advanced technologies such as neuronavigation systems, microsurgical instruments, and minimally invasive surgical techniques, enabling improved precision, reduced complications, and better patient outcomes across hospitals and specialty neurology centers

- The escalating demand for neurosurgery is primarily driven by the rising prevalence of neurological disorders, increasing geriatric population, growing incidence of traumatic brain injuries, and expanding awareness regarding early diagnosis and advanced surgical treatment options, along with continuous innovation in neurotechnology and surgical techniques

- The U.K. dominated the Europe Neurosurgery Market with the largest revenue share of 35.6% in 2025, supported by a well-established healthcare system, strong neurosurgical expertise, high adoption of advanced surgical technologies, and significant government and private investments in neurological care infrastructure

- Germany is expected to be the fastest-growing region in the Europe Neurosurgery Market during the forecast period, driven by increasing healthcare expenditure, rapid adoption of minimally invasive and robotic-assisted neurosurgical procedures, and strong presence of leading medical device and neurosurgical equipment manufacturers

- The neurosurgery devices segment dominated the largest market revenue share of approximately 58.7% in 2025, driven by the increasing demand for advanced surgical tools used in complex brain and spine procedures

Report Scope and Europe Neurosurgery Market Segmentation

|

Attributes |

Neurosurgery Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Europe

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Europe Neurosurgery Market Trends

“Advancements in Minimally Invasive Surgical Techniques and Neuro-navigation Systems”

- A significant and accelerating trend in the global Europe Neurosurgery Market is the rapid advancement of minimally invasive surgical techniques and the increasing use of neuro-navigation systems, which are improving surgical precision and patient outcomes

- For instance, minimally invasive neurosurgical procedures are increasingly being adopted for brain tumor removal and spinal surgeries, enabling smaller incisions, reduced trauma, and faster patient recovery

- The integration of advanced imaging technologies such as intraoperative MRI and CT scanning is enhancing real-time visualization, allowing surgeons to perform highly accurate interventions

- Furthermore, neuro-navigation systems are providing 3D guidance during complex procedures, improving accuracy in targeting deep-seated brain lesions and reducing surgical risks

- The growing use of robotic-assisted neurosurgery is also contributing to improved precision, reduced human error, and better postoperative outcomes

- This trend toward high-precision, technology-driven surgical approaches is significantly transforming neurosurgical practice and improving patient safety and recovery rates

Europe Neurosurgery Market Dynamics

Driver

“Rising Prevalence of Neurological Disorders and Growing Aging Population”

- The increasing prevalence of neurological disorders such as brain tumors, epilepsy, Parkinson’s disease, and stroke is a major driver for the Europe Neurosurgery Market

- For instance, the global rise in stroke incidence and neurodegenerative diseases has significantly increased the demand for surgical and interventional neurosurgical procedures

- The rapidly aging population is further contributing to market growth, as elderly individuals are more susceptible to neurological conditions requiring surgical intervention

- Furthermore, improvements in diagnostic capabilities are enabling earlier detection of neurological disorders, leading to timely surgical treatment

- The expansion of specialized neurosurgical centers and improved healthcare infrastructure is also supporting market growth across developed and emerging regions

- Increasing awareness among patients and healthcare providers regarding advanced treatment options is further boosting the adoption of neurosurgical procedures

Restraint/Challenge

“High Surgical Complexity and Limited Access to Advanced Neurosurgical Care”

- Neurosurgery procedures are highly complex and require specialized expertise, which limits the availability of skilled neurosurgeons in many regions

- For instance, in several developing and rural areas, patients often need to travel to major metropolitan hospitals to access advanced neurosurgical treatment, leading to delays in care

- In addition, the high cost associated with neurosurgical procedures, including hospitalization, advanced imaging, and postoperative care, can be a significant financial burden for patients

- The risk of complications and long recovery periods also makes neurosurgical interventions less accessible for some patient populations

- Shortage of advanced neurosurgical infrastructure and equipment in underdeveloped healthcare systems further restricts market expansion

- Addressing these challenges requires increased investment in healthcare facilities, training of specialized professionals, and improved access to advanced surgical technologies

- While technological progress is ongoing, disparities in access and affordability continue to limit the overall growth potential of the Europe Neurosurgery Market

Europe Neurosurgery Market Scope

The market is segmented on the basis of product type, application, age group, end user, and distribution channel.

• By Product Type

On the basis of product type, the Europe Neurosurgery Market is segmented into neurosurgery devices, neurosurgery software, and consumables. The neurosurgery devices segment dominated the largest market revenue share of approximately 58.7% in 2025, driven by the increasing demand for advanced surgical tools used in complex brain and spine procedures. These devices include surgical microscopes, neuroendoscopes, and stereotactic systems that enhance precision and surgical outcomes. Rising prevalence of neurological disorders such as brain tumors, epilepsy, and Parkinson’s disease significantly boosts demand. Continuous technological advancements, including minimally invasive and robot-assisted systems, further strengthen this segment. Hospitals and specialized neurosurgery centers heavily invest in advanced devices to improve success rates. Growing healthcare infrastructure in emerging economies supports adoption. Increasing number of neurosurgical procedures globally also contributes to dominance. Favorable reimbursement policies in developed regions further enhance market penetration. In addition, rising geriatric population increases neurological disease burden. Continuous R&D investments by key players drive innovation and expansion.

The neurosurgery software segment is expected to witness the fastest CAGR of 10.2% from 2026 to 2033, driven by increasing adoption of AI-based surgical planning and navigation systems. Advanced software solutions assist in preoperative planning, intraoperative guidance, and postoperative analysis. Growing integration of artificial intelligence and machine learning enhances surgical precision. Rising demand for image-guided surgery systems supports segment growth. In addition, cloud-based neurosurgical platforms are improving data accessibility and collaboration. Increasing focus on personalized medicine further boosts software adoption. Hospitals are increasingly investing in digital operating rooms. Expansion of minimally invasive surgeries also drives demand for advanced software tools. Continuous innovation in neuroimaging and simulation technologies supports growth. The segment is expected to expand rapidly with the digital transformation of healthcare.

• By Application

On the basis of application, the market is segmented into aneurysms, arteriovenous malformation (AVM), brain tumors, carotid artery blockage/stenosis, cerebrovascular surgery, cortical mapping, epilepsy, functional neurosurgery, intraoperative angiography, Parkinson’s disease and tremors, peripheral nerve surgery, pituitary tumors, radiosurgery, skull base surgery, spine surgery, stereotactic neurosurgery, trauma surgery, trigeminal neuralgia, and others. The brain tumors segment dominated the market with a revenue share of approximately 21.5% in 2025, driven by the rising global incidence of primary and metastatic brain tumors. Increasing exposure to risk factors such as radiation and genetic mutations contributes to disease prevalence. Advancements in imaging technologies enable early detection and accurate diagnosis. Surgical intervention remains the primary treatment method, boosting demand for neurosurgical procedures. Hospitals and oncology centers increasingly invest in advanced neurosurgical systems. Rising geriatric population further increases tumor incidence rates. Continuous R&D in oncology and neurosurgery improves treatment outcomes. Growing awareness about early diagnosis also supports segment growth. In addition, improved healthcare access in developing countries enhances treatment rates.

The Parkinson’s disease and tremors segment is expected to witness the fastest CAGR of 11.4% from 2026 to 2033, driven by the rising global prevalence of neurodegenerative disorders. Increasing aging population is a major contributing factor. Growing adoption of deep brain stimulation (DBS) and functional neurosurgery techniques supports segment growth. Technological advancements in neurostimulation devices improve treatment effectiveness. Rising awareness about movement disorder treatments further boosts demand. Increasing healthcare expenditure supports access to advanced therapies. Continuous clinical research into neurological disorders enhances treatment options. Expansion of specialized neurology centers contributes to growth. Improved diagnostic capabilities enable early intervention. The segment is expected to expand rapidly due to rising neurological disease burden worldwide.

• By Age Group

On the basis of age group, the market is segmented into pediatric, adult, and geriatric. The adult segment dominated the market with a share of approximately 56.8% in 2025, driven by the high prevalence of neurological disorders in the working-age population. Adults are more exposed to lifestyle-related risk factors such as stress, hypertension, and trauma. Increasing incidence of brain injuries and tumors also contributes to demand. Advanced neurosurgical procedures are widely performed in adult patients. Hospitals prioritize treatment for this large patient base. Rising awareness about neurological health further supports segment growth. Increasing healthcare access improves treatment rates. In addition, technological advancements enhance surgical success rates.

The geriatric segment is expected to witness the fastest CAGR of 9.6% from 2026 to 2033, driven by the rapidly aging global population. Elderly individuals are highly susceptible to neurological disorders such as Alzheimer’s, Parkinson’s, and brain tumors. Increasing life expectancy further contributes to segment growth. Rising demand for minimally invasive neurosurgical procedures supports adoption. Growing healthcare expenditure on elderly care enhances treatment access. Expansion of geriatric healthcare services boosts market growth. Continuous advancements in neurosurgical technologies improve outcomes in older patients. The segment is expected to expand significantly due to demographic shifts worldwide.

• By End User

On the basis of end user, the market is segmented into hospitals, neurosurgery centers, research centers, ambulatory surgical centers, and others. The hospitals segment dominated the market with a revenue share of approximately 62.3% in 2025, driven by the availability of advanced neurosurgical infrastructure and skilled professionals. Hospitals handle the majority of complex neurosurgery cases, including tumors and trauma. Increasing patient inflow supports segment dominance. Availability of multidisciplinary care enhances treatment outcomes. Government funding and healthcare investments further strengthen hospitals. Continuous technological upgrades improve surgical capabilities. Rising number of neurology departments globally also supports growth.

The ambulatory surgical centers (ASCs) segment is expected to witness the fastest CAGR of 10.1% from 2026 to 2033, driven by the increasing shift toward minimally invasive and cost-effective surgeries. ASCs offer shorter hospital stays and reduced healthcare costs. Advancements in outpatient neurosurgical procedures support growth. Increasing patient preference for convenient care settings boosts adoption. Expansion of healthcare infrastructure in emerging economies further supports demand. The segment is expected to grow rapidly due to efficiency and affordability advantages.

• By Distribution Channel

On the basis of distribution channel, the market is segmented into direct tender, third-party distributors, and others. The direct tender segment dominated the market with a share of approximately 48.9% in 2025, driven by bulk procurement of neurosurgical equipment by hospitals and government healthcare institutions. Direct purchasing ensures cost efficiency and quality assurance. Increasing government investments in healthcare infrastructure support this segment. Hospitals prefer direct sourcing for advanced neurosurgical devices. Strong relationships between manufacturers and healthcare providers further enhance adoption.

The third-party distributors segment is expected to witness the fastest CAGR of 9.8% from 2026 to 2033, driven by expanding access to neurosurgical equipment in emerging markets. Distributors help bridge supply chain gaps and improve product availability. Increasing demand from smaller hospitals and clinics supports growth. In addition, growing international expansion of medical device companies boosts distributor networks. The segment is expected to grow steadily with rising global healthcare penetration. Furthermore, distributors provide localized support services and faster delivery, improving overall operational efficiency. Rising partnerships between manufacturers and regional distributors are also strengthening market reach and accessibility.

Europe Neurosurgery Market Regional Analysis

- The Europe Neurosurgery Market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by the increasing prevalence of neurological disorders, advancements in neurosurgical technologies, and strong healthcare infrastructure across the region

- Rising investments in hospital modernization, growing adoption of minimally invasive neurosurgical procedures, and continuous innovation in surgical imaging and navigation systems are further supporting market growth

- In addition, the presence of highly skilled neurosurgeons and well-established neuro care facilities is enhancing the overall treatment landscape in Europe

U.K. Europe Neurosurgery Market Insight

The U.K. Europe Neurosurgery Market dominated the Europe region with the largest revenue share of 35.6% in 2025, supported by a well-established healthcare system, strong neurosurgical expertise, high adoption of advanced surgical technologies, and significant government and private investments in neurological care infrastructure. The country benefits from advanced hospital networks and early adoption of cutting-edge neurosurgical techniques, including image-guided and minimally invasive procedures. Furthermore, increasing cases of neurological disorders and continuous improvements in neurocritical care are driving sustained market growth in the U.K.

Germany Europe Neurosurgery Market Insight

The Germany Europe Neurosurgery Market is expected to be the fastest-growing region during the forecast period, driven by increasing healthcare expenditure and rapid adoption of minimally invasive and robotic-assisted neurosurgical procedures. The country’s strong presence of leading medical device manufacturers and continuous technological innovation in surgical equipment are significantly enhancing treatment capabilities. In addition, Germany’s focus on precision medicine, high-quality healthcare standards, and expanding neurosurgical infrastructure is further accelerating market expansion.

Europe Neurosurgery Market Share

The Neurosurgery industry is primarily led by well-established companies, including:

- Medtronic plc (Ireland)

- Stryker Corporation (U.S.)

- Johnson & Johnson MedTech (U.S.)

- Siemens Healthineers AG (Germany)

- GE HealthCare Technologies Inc. (U.S.)

- Brainlab AG (Germany)

- Zimmer Biomet Holdings, Inc. (U.S.)

- Integra LifeSciences Holdings Corporation (U.S.)

- B. Braun SE (Germany)

- Abbott Laboratories (U.S.)

- Karl Storz SE & Co. KG (Germany)

- Olympus Corporation (Japan)

- Zimmer Biomet Neurosurgery (U.S.)

- Elekta AB (Sweden)

- Micromar Indústria e Comércio Ltda. (Brazil)

- Natus Medical Incorporated (U.S.)

- ClearPoint Neuro, Inc. (U.S.)

- Aleva Neurotherapeutics SA (Switzerland)

- RAUMEDIC AG (Germany)

- Synaptive Medical (Canada)

Latest Developments in Europe Neurosurgery Market

- In April 2021, the U.S. Food and Drug Administration (FDA) authorized the Neurolutions IpsiHand Upper Extremity Rehabilitation System, a brain–computer interface (BCI)-based neurorehabilitation device for stroke patients. The system enables neurosurgery-adjacent neuro-rehabilitation by translating brain signals into movement assistance for patients with motor impairment, marking a key advancement in neurotechnology-driven recovery solutions

- In June 2021, CMR Surgical, a UK-based surgical robotics company, reported increased adoption of its Versius Surgical Robotic System across neurosurgery-adjacent minimally invasive procedures, with hospitals integrating robotic assistance for complex cranial and endoscopic workflows. This expansion highlighted the growing shift toward robotic-assisted neurosurgical techniques to improve precision and reduce surgical trauma

- In May 2023, Neuralink, a neurotechnology company, received U.S. FDA approval to begin human clinical trials for its brain-computer interface implant after prior regulatory concerns were addressed. The approval enabled first-in-human testing in patients with severe paralysis, marking a major milestone in implantable neurosurgical neurotechnology development

- In September 2023, Zeta Surgical, a neurosurgical navigation technology company, received FDA 510(k) clearance for its ZETA platform for cranial surgical procedures. The system provides “GPS-like” navigation for neurosurgery with submillimeter accuracy, supporting brain biopsy and intracranial interventions and improving surgical precision and safety

- In February 2024, CMR Surgical, announced an upgrade to its Versius Surgical Robotic System introducing new imaging capabilities, including indocyanine green (ICG) fluorescence visualization. This advancement enhances intraoperative visualization and supports more precise tissue identification during minimally invasive surgical procedures, including neurosurgical-adjacent applications

- In April 2024, researchers published advancements in soft robotic systems for minimally invasive neurosurgery, highlighting new hybrid rigid–flexible robotic platforms designed for deep brain access and tumor biopsy procedures. These innovations aim to improve dexterity, safety, and precision in complex intracranial surgeries where traditional rigid instruments are limited

- In March 2024, Intuitive Surgical, the developer of the da Vinci robotic surgical system, reported continued expansion of robotic-assisted surgery adoption following FDA-cleared upgrades to its platform. These advancements strengthened minimally invasive surgical capabilities across complex procedures, contributing indirectly to neurosurgical technique evolution through improved robotic precision systems

- In December 2025, Medivis, a surgical intelligence company, received FDA 510(k) clearance for its Cranial Navigation augmented reality (AR) platform. The system is the first AR-based intraoperative guidance technology cleared for cranial neurosurgery, enabling real-time visualization of brain anatomy and improving surgical accuracy and workflow efficiency

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.