Europe Non Metallic Enclosure Market

Market Size in USD Billion

USD

1.13 Billion

USD

2.03 Billion

2025

2033

USD

1.13 Billion

USD

2.03 Billion

2025

2033

| 2026 - 2033 | |

| USD 1.13 Billion | |

| USD 2.03 Billion | |

| % | |

|

Non-Metallic Enclosure Market Size

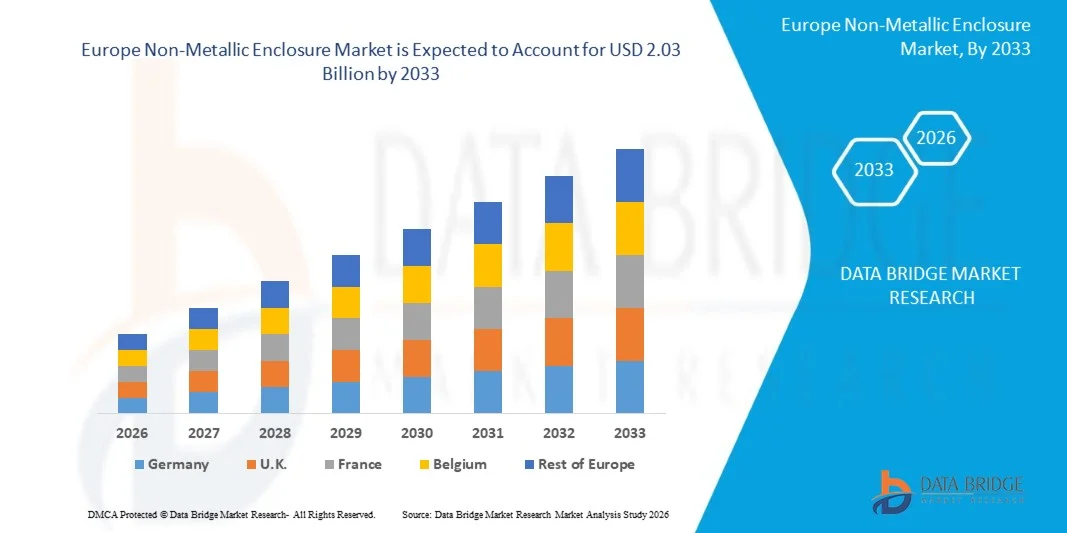

- The Europe non-metallic enclosure market size was valued at USD 1.13 Billion in 2025and is expected to reach USD 2.03 Billion by 2033, at a CAGR of 7.9% during the forecast period

- The market growth is primarily driven by the increasing demand for durable, lightweight, and corrosion-resistant enclosure solutions across industrial automation, energy & power, telecommunications, and commercial infrastructure sectors, along with the rising need for enhanced electrical safety and equipment protection in harsh operating environments.

- Furthermore, rapid industrialization, expansion of renewable energy installations, growing adoption of smart manufacturing and automation systems, and stricter safety regulations promoting non-conductive and weather-resistant enclosures are accelerating product adoption, thereby significantly supporting the overall expansion of the non-metallic enclosure market.

Non-Metallic Enclosure Market Analysis

- Non-metallic enclosures, including polymer, fiberglass, and polycarbonate-based housings, are increasingly essential across electrical distribution, industrial automation, renewable energy, telecommunications, and commercial infrastructure applications due to their lightweight structure, corrosion resistance, electrical insulation properties, and suitability for harsh operating environments.

- The growing demand for non-metallic enclosures is primarily driven by rapid industrial automation, expansion of renewable energy projects, increasing deployment of outdoor electrical systems, and rising emphasis on safety-compliant and low-maintenance protective solutions across industries.

- Germany dominated the non-metallic enclosure market with the largest revenue share of 25.05% in 2025, supported by strong industrial infrastructure, high adoption of advanced electrical protection systems, strict safety regulations, and significant investments in smart grid and automation technologies.

- Germany is expected to be the fastest-growing with the CAGR of 9.2%region during the forecast period, driven by accelerating industrialization, expanding construction and energy sectors, rapid urban development, and increasing investments in power distribution and manufacturing facilities across China, India, and Southeast Asia.

- The Polymer & Plastic Enclosures segment dominated the market, accounting for 64.52% market share in 2025, owing to advantages such as corrosion resistance, cost efficiency, ease of installation, weather durability, and growing preference for non-conductive enclosure solutions across industrial and commercial applications.

Report Scope and Non-Metallic Enclosure Market Segmentation

|

Attributes |

Non-Metallic Enclosure Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Europe · Germany · U.K. · France · Italy · Spain · Rest of Europe |

|

Key Market Players |

· Schneider Electric (France) · ABB Ltd. (Switzerland) · Eaton Corporation (Ireland) · Rittal GmbH & Co. KG (Germany) · Legrand SA (France) · TE Connectivity (Switzerland) · Phoenix Contact (Germany) · CHINT Group (China) · Delixi Electric (China) · Gustav Hensel GmbH & Co. KG (Germany) · Allied Moulded Products (U.S.) · Bopla Gehäuse Systeme GmbH (Germany) · OKW Gehäusesysteme GmbH (Germany) · Bud Industries Inc. (U.S.) · Polycase Inc. (U.S.) · Hylec-APL Ltd (U.K.) · Stahlin Enclosures (U.S.) · Saginaw Control and Engineering (U.S.) · BCH Electric Limited (India) · Arlington Industries, Inc. (U.S.) · Engineered Products Company (EPCO) (U.S.) · B&R Enclosures Pty Ltd (Australia) · Hammond Manufacturing (Canada) · Takachi Electronics Enclosure Co., Ltd. (Japan) · OKW Enclosures Ltd (METCASE) (U.S.) · Unibox Enclosures (Finland) · Saipwell (China) · Allbro (South Africa) · Leotech (Taiwan) · VSM Plast (India) |

|

Market Opportunities |

· Growth in renewable energy applications · Development of smart cities and IoT infrastructure · Advancements in material science |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, geographically represented company-wise production and capacity, network layouts of distributors and partners, detailed and updated price trend analysis and deficit analysis of supply chain and demand. |

Non-Metallic Enclosure Market Trends

“The Growing Adoption of Industrial Automation, Smart Manufacturing, and Digital Infrastructure”

- The rapid adoption of industrial automation across manufacturing facilities is increasing the deployment of control panels, sensors, and electrical systems that require reliable protection from dust, moisture, chemicals, and physical damage, thereby driving demand for durable non-metallic enclosures.

- The expansion of smart manufacturing and Industry 4.0 technologies has led to higher integration of connected devices, PLCs, and communication equipment, creating the need for electrically insulated and lightweight enclosure solutions that ensure operational safety and system reliability.

- The continuous growth of digital infrastructure, including data centers, telecom networks, and intelligent building systems, is further accelerating the requirement for non-conductive enclosures capable of protecting sensitive electronic components in both indoor and outdoor environments.

- For instance, automated production lines in automotive and electronics manufacturing plants increasingly utilize polymer-based enclosures to safeguard automation controllers and wiring systems from corrosion and environmental exposure.

- Overall, the increasing digitalization and automation of industrial operations are strengthening the adoption of advanced enclosure solutions that support efficient, safe, and uninterrupted system performance.

- As industries continue transitioning toward connected and intelligent operations, non-metallic enclosures are expected to play a critical role in enabling scalable, low-maintenance, and future-ready electrical protection infrastructure.

Non-Metallic Enclosure Market Dynamics

Driver

“Increasing Demand for Corrosion-Resistant Solutions”

- The increasing demand for corrosion-resistant solutions is a key driver accelerating the growth of the Europe non-metallic enclosure market. In industries such as chemical processing, wastewater treatment, marine, and oil & gas, equipment is frequently exposed to moisture, salts, and aggressive chemicals that cause rapid degradation of traditional metallic enclosures.

- Corrosion not only reduces the lifespan of enclosures but also leads to equipment failure, safety risks, and significant maintenance costs. As a result, industries are increasingly prioritizing materials that can withstand such harsh conditions while ensuring long-term operational reliability.

- Non-metallic enclosures, particularly those made from fiberglass-reinforced polymers and polycarbonate, offer inherent resistance to corrosion, chemicals, and environmental stressors. These materials are immune to rust and provide superior performance in corrosive environments such as coastal areas and industrial plants. Their ability to maintain structural integrity and reduce maintenance frequency makes them a cost-effective alternative to metal enclosures, especially in applications where durability and lifecycle performance are critical

- For instance, In January 2026, Eabel published an industry article highlighting those non-metallic enclosures are increasingly used in chemical plants, coastal infrastructure, and outdoor installations due to their strong resistance to moisture, chemicals, and harsh environmental conditions. The article emphasized their reliability in corrosive environments where metal enclosures degrade quickly. This demonstrates growing industry preference for corrosion-resistant non-metallic solutions, directly driving market demand

- In conclusion, the rising need to protect critical equipment from corrosion-related damage is significantly boosting the adoption of non-metallic enclosures worldwide. As industries continue to operate in increasingly harsh and demanding environments, the shift toward corrosion-resistant materials is becoming a strategic necessity rather than a preference. This trend is expected to remain a strong and sustained driver for the Europe non-metallic enclosure market.

Restraint/Challenge

“Intense Competition from Metallic Enclosures”

- While non-metallic enclosures offer significant benefits such as corrosion resistance, lightweight design, and energy efficiency, they face strong competition from traditional metallic enclosures. Metal enclosures, typically made from steel, aluminum, or stainless steel, have been widely used for decades in electrical, telecom, and industrial applications due to their robustness, durability, and ability to handle high thermal loads. In many sectors, metallic enclosures are perceived as more reliable for heavy-duty industrial use, high-voltage applications, and environments with extreme temperature fluctuations.

- Additionally, the well-established supply chains, long-standing manufacturer reputations, and cost competitiveness of metallic enclosures make it difficult for non-metallic alternatives to fully penetrate certain segments. Industries that prioritize mechanical strength or require shielding from electromagnetic interference (EMI) often continue to prefer metal enclosures, limiting the growth potential of non-metallic solutions in those applications. This competition creates a significant restraint for the non-metallic enclosure market, especially in regions where cost sensitivity or industrial standards favor traditional metallic options.

- For instance, In July 2025, KDM Steel published an article titled “Metallic Vs Non‑Metallic Electrical Enclosures: Key Differences, Benefits, and Best Applications”, explaining that metallic enclosures (e.g., steel and aluminum) are built to withstand high mechanical stress, provide strong EMI shielding, and perform reliably in high-temperature and industrial environments. The guide highlights those metals are preferred for applications requiring greater durability and protection where non‑metallic materials may not be ideal. This indicates that mechanical strength, EMI shielding, and thermal performance requirements restrain the growth of non‑metallic enclosures in industrial sectors.

- The longstanding adoption, superior mechanical strength, thermal tolerance, and EMI shielding capabilities of metallic enclosures pose a significant restraint on the non-metallic enclosure market. While non-metallic options provide corrosion resistance and lightweight advantages, industries with high-performance requirements, cost sensitivity, or legacy infrastructure continue to rely on metallic solutions. This intense competition limits market penetration and slows adoption rates in several industrial and utility sectors

Non-Metallic Enclosure Market Scope

The Europe non-metallic enclosure market is segmented into five notable segments based on product type, application, form factor, material type, and distribution channel.

- By Product Type

On the basis of product type, the Europe non-metallic enclosure market is segmented into polymer & plastic enclosures, composite enclosures, thermoplastic elastomer enclosures, and other specialty polymers. The Polymer & Plastic Enclosures segment is expected to dominate the market with share of 64.46% market share in 2026, due to their widespread usage across electrical, industrial, and telecommunications applications. These enclosures offer advantages such as lightweight structure, corrosion resistance, cost-effectiveness, and ease of manufacturing, making them highly suitable for indoor and outdoor installations. Composite enclosures, particularly fiberglass-reinforced materials, are gaining traction in harsh industrial and utility environments due to their superior strength, chemical resistance, and durability.

The Composite Enclosures segment is anticipated to witness the fastest CAGR of 8.3% from 2026 to 2033, fueled by the increasing demand for high-performance enclosure solutions that offer superior strength, corrosion resistance, and long service life compared to traditional materials. Composite enclosures, typically made from fiberglass-reinforced polymers and advanced resin systems, provide excellent resistance to harsh environmental conditions, including moisture, chemicals, UV exposure, and extreme temperatures, making them highly suitable for outdoor and industrial applications. Additionally, the growing expansion of renewable energy installations, smart grid infrastructure, telecommunications networks, and industrial automation systems is accelerating their adoption due to their lightweight design, electrical insulation properties, and reduced maintenance requirements, thereby supporting strong market growth during the forecast period.

- By Application

On the basis of application, the Europe non-metallic enclosure market is segmented into electrical & electronics, industrial automation, energy & utilities, telecommunications, transportation, consumer electronics, medical & healthcare, and defense & aerospace. The Electrical & Electronics segment is anticipated to dominate the market share of 28.93% share in 2026, due to increasing demand for protective enclosures in power distribution systems, control panels, and circuit protection applications. Industrial Automation and Energy & Utilities are also key contributors, driven by increasing deployment of control systems, renewable energy infrastructure, and smart grid technologies. Telecommunications is witnessing strong growth due to rising demand for outdoor network enclosures and fiber infrastructure protection.

The Energy & Utilities segment is expected to witness the fastest CAGR of 8.6% from 2026 to 2033, driven by the rapid expansion of renewable energy projects, modernization of power transmission and distribution networks, and increasing investments in smart grid infrastructure worldwide. The growing deployment of solar and wind energy systems requires durable, weather-resistant, and electrically insulated enclosure solutions to protect control panels, monitoring devices, and power distribution components in outdoor and harsh environments. Additionally, rising electrification initiatives, grid reliability improvements, and the integration of advanced monitoring and automation technologies across utility operations are further accelerating the adoption of non-metallic enclosures, supporting sustained growth of the segment during the forecast period.

- By Form Factor

On the basis of form factor, the Europe non-metallic enclosure market is segmented into box enclosures, cabinet & rack-mount, DIN-Rail enclosures, custom & modular enclosures, hinged cover enclosures, and sealed / gasketed enclosures. Box Enclosures are expected to dominate the market with market share of 40.72% in 2026, due to their extensive use in small-scale electrical installations, junction boxes, and instrumentation protection. Sealed / Gasketed enclosures are witnessing increasing demand in outdoor and harsh environments where protection against dust, moisture, and contaminants is critical. Custom & Modular enclosures are also gaining popularity due to growing demand for application-specific designs.

The Custom & Modular Enclosures segment is anticipated to witness the fastest CAGR of 8.6% from 2026 to 2033, driven by the increasing demand for flexible and application-specific enclosure solutions across industrial automation, telecommunications, renewable energy, and commercial infrastructure sectors. As industries adopt advanced electrical and electronic systems, there is a growing need for enclosures that can be easily modified, expanded, or integrated with additional components without requiring complete system replacement. Modular designs enable faster installation, improved space optimization, and simplified maintenance, while customization supports unique operational requirements, environmental conditions, and safety standards. Furthermore, the rising adoption of smart manufacturing and IoT-enabled equipment is encouraging manufacturers to prefer scalable enclosure systems, thereby accelerating the growth of the custom and modular enclosures segment during the forecast period.

- By Material Type

On the basis of material type, the Europe non-metallic enclosure market is segmented into thermoplastics, thermoset composites, elastomers, and others. The Thermoplastics segment is expected to dominate the market share with 67.08% in 2026, owing to their versatility, cost efficiency, and ease of processing. Materials such as polycarbonate and ABS are widely used due to their impact resistance, UV stability, and electrical insulation properties. Thermoset composites, including fiberglass-reinforced polyester, are preferred in demanding industrial and outdoor environments due to their superior mechanical strength and resistance to heat and chemicals.

The Thermoset Composites segment is expected to witness the fastest CAGR of 8.3% from 2026 to 2033, fueled by the increasing demand for high-strength, lightweight, and corrosion-resistant enclosure materials across industrial, energy, and infrastructure applications. Thermoset composite enclosures offer superior mechanical durability, thermal stability, and resistance to chemicals, UV radiation, and extreme weather conditions, making them highly suitable for outdoor and harsh environments. Additionally, the growing deployment of renewable energy systems, industrial automation equipment, and electrical distribution networks is accelerating the adoption of thermoset-based solutions due to their long service life and low maintenance requirements. Rising emphasis on safety standards, electrical insulation performance, and cost-effective lifecycle solutions further supports the expanding use of thermoset composites in modern non-metallic enclosure applications.

- By Distribution Channel

On the basis of distribution channel, the Europe non-metallic enclosure market is segmented into OEM direct sales, distributors / value-added resellers, system integrators & panel builders, online industrial marketplaces, and retail. OEM Direct Sales are expected to dominate the market with share of 31.82% share in 2026, as manufacturers directly supply enclosures to industrial OEMs, utilities, and infrastructure projects, ensuring customization, bulk procurement, and long-term contracts. Distributors and value-added resellers play a critical role in expanding market reach, particularly for small and medium enterprises. Meanwhile, online industrial marketplaces are emerging as a growing channel due to increasing digital procurement and ease of product comparison.

The Online Industrial Marketplaces segment is expected to witness the fastest CAGR of 8.7% from 2026 to 2033, fueled by the increasing digitalization of industrial procurement processes and the growing preference for convenient, transparent, and cost-efficient purchasing platforms. Companies are increasingly adopting online marketplaces to streamline sourcing, compare product specifications and pricing in real time, and reduce procurement cycle times. Additionally, the rising penetration of e-commerce in the industrial sector, improved logistics networks, and the availability of a wide range of suppliers and customized products on single platforms are encouraging businesses, particularly small and medium enterprises, to shift toward digital purchasing channels. This transition is further supported by advancements in cloud-based platforms, secure payment systems, and data-driven procurement solutions, which collectively enhance operational efficiency and accelerate the growth of online industrial marketplaces.

Non-Metallic Enclosure Market Regional Analysis

- Germany dominated the non-metallic enclosure market with a revenue share of 25.05% in 2025, supported by advanced industrial infrastructure, strong investments in automation and energy systems, high adoption of electrical safety solutions, and widespread deployment of control and power distribution equipment.

- The region benefits from a technologically advanced industrial base, stringent safety and regulatory standards, and the presence of leading enclosure manufacturers, which collectively encourage the adoption of high-performance non-metallic enclosures across manufacturing, utilities, and commercial applications.

- Germany is expected to witness the fastest growth during the forecast period, driven by rapid industrialization, expanding construction and renewable energy sectors, increasing electrification projects, and rising investments in smart manufacturing and infrastructure development.

U.K. Non-Metallic Enclosure Market Insight

The U.K. non-metallic enclosure market is driven by strong adoption of industrial automation, expanding renewable energy installations, and increasing demand for durable electrical protection solutions across manufacturing and commercial sectors. Strict safety regulations, modernization of power infrastructure, and growing investments in smart grid and digital systems further support steady market growth.

France Non-Metallic Enclosure Market Insight

The France Non-Metallic Enclosure Market is driven by strong industrial automation adoption, strict electrical safety regulations, and increasing investments in renewable energy and smart infrastructure projects. Growing demand for corrosion-resistant and lightweight enclosure solutions across manufacturing, energy, and transportation sectors further supports steady regional market growth.

Non-Metallic Enclosure Market Share

The Non-Metallic Enclosure industry is primarily led by well-established companies, including:

- Schneider Electric (France)

- ABB Ltd. (Switzerland)

- Eaton Corporation (Ireland)

- Rittal GmbH & Co. KG (Germany)

- Legrand SA (France)

- TE Connectivity (Switzerland)

- Phoenix Contact (Germany)

- CHINT Group (China)

- Delixi Electric (China)

- Gustav Hensel GmbH & Co. KG (Germany)

- Allied Moulded Products (U.S.)

- Bopla Gehäuse Systeme GmbH (Germany)

- OKW Gehäusesysteme GmbH (Germany)

- Bud Industries Inc. (U.S.)

- Polycase Inc. (U.S.)

- Hylec-APL Ltd (U.K.)

- Stahlin Enclosures (U.S.)

- Saginaw Control and Engineering (U.S.)

- BCH Electric Limited (India)

- Arlington Industries, Inc. (U.S.)

- Engineered Products Company (EPCO) (U.S.)

- B&R Enclosures Pty Ltd (Australia)

- Hammond Manufacturing (Canada)

- Takachi Electronics Enclosure Co., Ltd. (Japan)

- OKW Enclosures Ltd (METCASE) (U.S.)

- Unibox Enclosures (Finland)

- Saipwell (China)

- Allbro (South Africa)

- Leotech (Taiwan)

- VSM Plast (India)

Latest Developments in Europe Non-Metallic Enclosure Market

- In January 2026, Schneider Electric announced an investment of approximately $66.8 million USD to expand its manufacturing facilities in Telangana, India, aimed at increasing production capacity for electrical safety and power management solutions. The expansion is intended to support rising demand for electrification, industrial automation, and energy infrastructure across domestic and international markets. By strengthening localized manufacturing and supply chain capabilities, the company plans to improve production efficiency and ensure faster product availability, including enclosure-based electrical systems used in industrial and commercial applications.

- In June 2025, ABB Electrification Canada Inc. completed the acquisition of Bel Products Inc., a leading Canadian manufacturer of commercial, industrial, and custom‑built enclosures, housings and panels. This strategic acquisition strengthens ABB’s enclosures portfolio and expands its manufacturing and supply footprint in global to meet growing demand from commercial and industrial sectors.

- In May 2025, Lenze and Rittal signed a technology partnership to work together to shape the future of power distribution and drive technology. The combination of RiLineX, as the new standard platform for busbar systems, and Lenze’s market-leading compact inverters provides the basis.

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Table of Content

1 INTRODUCTION

1.1 OBJECTIVES OF THE STUDY

1.2 MARKET DEFINITION

1.3 OVERVIEW OF EUROPE NON-METALLIC ENCLOSURE MARKET

1.4 CURRENCY AND PRICING

1.5 LIMITATIONS

1.6 MARKETS COVERED

2 MARKET SEGMENTATION

2.1 MARKETS COVERED

2.2 GEOGRAPHICAL SCOPE

2.3 YEARS CONSIDERED FOR THE STUDY

2.4 DBMR TRIPOD DATA VALIDATION MODEL

2.5 PRIMARY INTERVIEWS WITH KEY OPINION LEADERS

2.6 DBMR MARKET POSITION GRID

2.7 VENDOR SHARE ANALYSIS

2.8 MULTIVARIATE MODELING

2.9 PRODUCT TYPE TIMELINE CURVE

2.1 MARKET APPLICATION COVERAGE GRID

2.11 SECONDARY SOURCES

2.12 ASSUMPTIONS

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

4.1 PORTER’S FIVE FORCES ANALYSIS

4.1.1 THREAT OF NEW ENTRANTS

4.1.1.1 ECONOMIES OF SCALE AND CAPITAL REQUIREMENTS:

4.1.1.2 BRAND IDENTITY, REPUTATION, AND TRUST BARRIERS

4.1.1.3 TECHNOLOGICAL & REGULATORY BARRIERS

4.1.2 BARGAINING POWER OF SUPPLIERS

4.1.2.1 SUPPLIER CONCENTRATION AND RAW MATERIAL DEPENDENCY

4.1.2.2 MATERIAL SPECIALIZATION AND NICHE CHEMICAL INPUTS

4.1.2.3 IMPACT OF GEOPOLITICAL AND MACRO SUPPLY DISRUPTIONS

4.1.3 BARGAINING POWER OF BUYERS

4.1.3.1 BUYER CONCENTRATION AND SCALE

4.1.3.2 PRODUCT STANDARDIZATION AND COMMODITIZATION

4.1.4 THREAT OF SUBSTITUTE PRODUCTS

4.1.4.1 EMERGING MATERIALS AND ADVANCED MANUFACTURING TECHNOLOGIES

4.1.4.2 LIFECYCLE‑LEVEL SUBSTITUTES: MODULAR AND RECONFIGURABLE CONCEPTS

4.1.5 INDUSTRY RIVALRY

4.1.5.1 NUMBER AND DIVERSITY OF COMPETITORS

4.1.5.2 CAPACITY AND UTILIZATION

4.1.5.3 INNOVATION AND R&D

4.2 INDUSTRY ANALYSIS & FUTURISTIC SCENARIO

4.2.1 OVERVIEW

4.2.2 INDUSTRY ANALYSIS

4.2.3 FUTURE ANALYSIS

4.2.4 CONCLUSION

4.3 PENETRATION AND GROWTH PROSPECT MAPPING

4.4 NEW BUSINESS AND EMERGING BUSINESS'S REVENUE OPPORTUNITIES

4.5 COMPANY COMPARATIVE ANALYSIS

4.6 VALUE CHAIN ANALYSIS

4.6.1 OVERVIEW

4.6.2 UPSTREAM: RAW MATERIALS & INPUT SUPPLY

4.6.3 MIDSTREAM: MANUFACTURING & PROCESSING

4.6.4 OEM INTEGRATION & SYSTEM ASSEMBLY

4.6.5 DISTRIBUTION & SALES CHANNELS

4.6.6 DOWNSTREAM: END-USE INDUSTRIES

4.6.7 AFTERMARKET SERVICES & LIFECYCLE SUPPORT

4.6.8 CONCLUSION

4.7 VENDOR SELECTION CRITERIA

4.7.1 MATERIAL QUALITY AND COMPLIANCE

4.7.2 MANUFACTURING CAPABILITY AND TECHNOLOGY

4.7.3 CUSTOMIZATION AND DESIGN SUPPORT

4.7.4 SUPPLY RELIABILITY AND LOGISTICS

4.7.5 AFTER-SALES SUPPORT AND LIFECYCLE SERVICES

4.7.6 COST AND TOTAL VALUE

4.7.7 REPUTATION AND INDUSTRY EXPERIENCE

4.8 INNOVATION TRACKER AND STRATEGIC ANALYSIS

4.8.1 MAJOR DEALS AND STRATEGIC ALLIANCES ANALYSIS

4.8.2 PRODUCTS DEVELOPMENT

4.8.3 STAGE OF DEVELOPMENT

4.8.4 TIMELINES AND MILESTONES

4.8.5 INNOVATION STRATEGIES AND METHODOLOGIES

4.8.6 RISK ASSESSMENT AND MITIGATION

4.8.6.1 MARKET & DEMAND RISKS:

4.8.6.2 SUPPLY CHAIN & RAW MATERIAL RISKS:

4.8.6.3 REGULATORY & COMPLIANCE RISKS:

4.8.6.4 COMPETITIVE & TECHNOLOGICAL RISKS:

4.8.6.5 FINANCIAL & CURRENCY RISKS:

4.8.6.6 OPERATIONAL & QUALITY RISKS:

4.8.6.7 ENVIRONMENTAL & SUSTAINABILITY RISKS:

4.8.6.8 CYBERSECURITY & DIGITAL RISKS:

4.8.7 FUTURE OUTLOOK

4.9 CONSUMER BUYING BEHAVIOR

4.9.1 INTRODUCTION

4.9.2 BUYING PATTERN

4.9.3 USES ANALYSIS

4.9.4 CONCLUSION

4.1 TECHNOLOGY ANALYSIS

4.10.1 INTRODUCTION

4.10.2 KEY TECHNOLOGIES

4.10.3 COMPLEMENTARY TECHNOLOGIES

4.10.4 ADJACENT TECHNOLOGIES

4.10.5 CONCLUSION

4.11 CHALLENGES

4.11.1 OVERVIEW

4.11.2 VOLATILITY IN RAW MATERIAL PRICES AND SUPPLY CHAINS

4.11.3 PERFORMANCE LIMITATIONS COMPARED TO METALLIC ALTERNATIVES

4.11.4 STRINGENT REGULATORY AND COMPLIANCE REQUIREMENTS

4.11.5 ENVIRONMENTAL AND SUSTAINABILITY CHALLENGES

4.11.6 HIGH INITIAL TOOLING AND MANUFACTURING COSTS

4.11.7 LIMITED AWARENESS AND ADOPTION IN EMERGING MARKETS

5.8.1 TECHNOLOGICAL INTEGRATION CHALLENGES

4.11.8 CONCLUSION

4.12 TECHNOLOGICAL ADVANCEMENTS

4.12.1 ADVANCED POLYMER BLENDS AND HIGH‑PERFORMANCE PLASTICS

4.12.2 SMART SENSOR INTEGRATION (IOT‑ENABLED ENCLOSURES)

4.12.3 MODULAR AND CONFIGURABLE DESIGNS

4.12.4 THERMAL MANAGEMENT AND PASSIVE COOLING INNOVATIONS

4.12.5 ADDITIVE MANUFACTURING (3D PRINTING) FOR CUSTOMIZATION

4.12.6 CONCLUSION

5 TARIFFS & IMPACT ON THE GLOBAL, U.S., AND INDIA NON-METALLIC ENCLOSURE MARKET

5.1 OVERVIEW

5.2 TARIFF STRUCTURES

5.2.1 UNITED STATES (HTSUS)

5.2.2 EUROPEAN UNION (EU – TARIC)

5.2.3 INDIA (ITC‑HS / HSN‑BASED SYSTEM)

5.2.4 CHINA CUSTOMS (PRC IMPORT DUTY)

5.2.5 OTHER REGIONS

5.2.6 EMERGING MARKETS: CHALLENGES IN TARIFF IMPLEMENTATION

5.3 INCREASED COSTS

5.4 SUPPLY CHAIN DISRUPTIONS

5.5 UNCERTAINTY AND INVESTMENT

5.6 IMPACT ON INNOVATION

5.7 COMPETITION AND MARKET DYNAMICS

5.8 EFFECT ON SMALL AND MEDIUM ENTERPRISES (SMES)

5.9 DEPLOYMENT OF TELECOMMUNICATION INFRASTRUCTURE

5.1 STRATEGIC RESPONSES AND INDUSTRY OUTLOOK

5.11 DIVERSIFICATION OF SUPPLY CHAINS

5.12 LEVERAGING ADVANCED LOGISTICS

5.13 ADVOCACY FOR POLICY ADJUSTMENTS

6 REGULATION COVERAGE

6.1 INTRODUCTION

6.2 INTERNATIONAL STANDARDIZATION FRAMEWORK

6.2.1 ROLE OF EUROPE STANDARDS ORGANIZATIONS

6.2.2 NORTH AMERICAN CERTIFICATION ECOSYSTEM

6.2.3 NEMA CLASSIFICATION SYSTEM

6.3 ENVIRONMENTAL AND CHEMICAL COMPLIANCE REGULATIONS

6.3.1 HAZARDOUS SUBSTANCE RESTRICTIONS

6.3.2 WASTE MANAGEMENT AND LIFECYCLE COMPLIANCE

6.4 REGIONAL REGULATORY DYNAMICS

6.4.1 UNITED STATES AND CANADA

6.4.2 EUROPEAN UNION

6.4.3 ASIA-PACIFIC

6.5 INGRESS PROTECTION AND ENVIRONMENTAL TESTING

6.6 FIRE SAFETY AND MATERIAL PERFORMANCE

6.7 CERTIFICATION, TESTING, AND COMPLIANCE INFRASTRUCTURE

6.7.1 THIRD-PARTY VALIDATION

6.7.2 DOCUMENTATION AND AUDIT REQUIREMENTS

6.8 EMERGING REGULATORY TRENDS

6.8.1 SUSTAINABILITY AND CIRCULAR ECONOMY

6.8.2 INTEGRATION OF SMART TECHNOLOGIES

6.8.3 CONVERGENCE OF EUROPE STANDARDS

6.9 CONCLUSION

7 MARKET OVERVIEW

7.1 DRIVERS

7.1.1 INCREASING DEMAND FOR CORROSION-RESISTANT SOLUTIONS

7.1.2 EXPANSION OF ELECTRICAL, TELECOMMUNICATIONS, AND ELECTRONICS SECTORS

7.1.3 EMPHASIS ON SUSTAINABILITY AND ENERGY EFFICIENCY

7.1.4 RAPID INDUSTRIALIZATION AND INFRASTRUCTURE DEVELOPMENT

7.2 RESTRAINTS

7.2.1 INTENSE COMPETITION FROM METALLIC ENCLOSURES

7.2.2 LOW AWARENESS AND PERCEPTION CHALLENGES

7.3 OPPORTUNITIES

7.3.1 GROWTH IN RENEWABLE ENERGY APPLICATIONS

7.3.2 DEVELOPMENT OF SMART CITIES AND IOT INFRASTRUCTURE

7.3.3 ADVANCEMENTS IN MATERIAL SCIENCE

7.4 CHALLENGES

7.4.1 THERMAL MANAGEMENT LIMITATIONS

7.4.2 INTENSE COMPETITION FROM TRADITIONAL AND ALTERNATIVE FOODS

8 EUROPE NON-METALLIC ENCLOSURE MARKET, BY PRODUCT TYPE

8.1 OVERVIEW

8.2 EUROPE NON-METALLIC ENCLOSURE MARKET, BY PRODUCT TYPE, 2018-2033 (USD THOUSAND)

8.2.1 POLYMER & PLASTIC ENCLOSURES

8.2.2 COMPOSITE ENCLOSURES

8.2.3 THERMOPLASTIC ELASTOMER ENCLOSURES

8.2.4 OTHER SPECIALTY POLYMERS

8.3 EUROPE POLYMER & PLASTIC ENCLOSURES IN NON-METALLIC ENCLOSURE MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

8.3.1 POLYCARBONATE ENCLOSURES

8.3.2 ABS ENCLOSURES

8.3.3 PVC ENCLOSURES

8.3.4 POLYPROPYLENE ENCLOSURES

8.3.5 HDPE/LDPE ENCLOSURES

8.3.6 ACETAL (POM) ENCLOSURES

8.4 EUROPE POLYMER & PLASTIC ENCLOSURES IN NON-METALLIC ENCLOSURE MARKET, BY REGION, 2018-2033 (USD THOUSAND)

8.4.1 NORTH AMERICA

8.4.2 EUROPE

8.4.3 ASIA-PACIFIC

8.4.4 SOUTH AMERICA

8.4.5 MIDDLE EAST & AFRICA

8.5 EUROPE COMPOSITE ENCLOSURES IN NON-METALLIC ENCLOSURE MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

8.5.1 GLASS FIBER REINFORCED POLYESTER (GRP)

8.5.2 GLASS REINFORCED PLASTIC (FRP)

8.5.3 OTHERS

8.6 EUROPE COMPOSITE ENCLOSURES IN NON-METALLIC ENCLOSURE MARKET, BY REGION, 2018-2033 (USD THOUSAND)

8.6.1 NORTH AMERICA

8.6.2 EUROPE

8.6.3 ASIA-PACIFIC

8.6.4 SOUTH AMERICA

8.6.5 MIDDLE EAST & AFRICA

8.7 EUROPE THERMOPLASTIC ELASTOMER ENCLOSURES IN NON-METALLIC ENCLOSURE MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

8.7.1 TPE CASING

8.7.2 TPU PROTECTIVE HOUSINGS

8.8 EUROPE THERMOPLASTIC ELASTOMER ENCLOSURES IN NON-METALLIC ENCLOSURE MARKET, BY REGION, 2018-2033 (USD THOUSAND)

8.8.1 NORTH AMERICA

8.8.2 EUROPE

8.8.3 ASIA-PACIFIC

8.8.4 SOUTH AMERICA

8.8.5 MIDDLE EAST & AFRICA

8.9 EUROPE OTHER SPECIALTY POLYMERS IN NON-METALLIC ENCLOSURE MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

8.9.1 NYLON / PA66

8.9.2 PTFE & FLUOROPOLYMERS

8.9.3 PPS (POLYPHENYLENE SULFIDE)

8.1 EUROPE OTHER SPECIALTY POLYMERS IN NON-METALLIC ENCLOSURE MARKET, BY REGION, 2018-2033 (USD THOUSAND)

8.10.1 NORTH AMERICA

8.10.2 EUROPE

8.10.3 ASIA-PACIFIC

8.10.4 SOUTH AMERICA

8.10.5 MIDDLE EAST & AFRICA

9 EUROPE NON-METALLIC ENCLOSURE MARKET, BY APPLICATION

9.1 OVERVIEW

9.2 ELECTRICAL & ELECTRONICS

9.3 INDUSTRIAL AUTOMATION

9.4 ENERGY & UTILITIES

9.5 TELECOMMUNICATIONS

9.6 TRANSPORTATION

9.7 CONSUMER ELECTRONICS

9.8 MEDICAL & HEALTHCARE

9.9 DEFENSE & AEROSPACE

9.1 EUROPE ELECTRICAL & ELECTRONICS IN NON-METALLIC ENCLOSURE MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

9.10.1 JUNCTION BOXES

9.10.2 INDUSTRIAL CONTROL CABINETS

9.10.3 SWITCHGEAR ENCLOSURES

9.10.4 TERMINAL BOXES

9.10.5 PCB MOUNTING BOXES

9.11 EUROPE ELECTRICAL & ELECTRONICS IN NON-METALLIC ENCLOSURE MARKET, BY REGION, 2018-2033 (USD THOUSAND)

9.11.1 NORTH AMERICA

9.11.2 EUROPE

9.11.3 ASIA-PACIFIC

9.11.4 SOUTH AMERICA

9.11.5 MIDDLE EAST & AFRICA

9.12 EUROPE INDUSTRIAL AUTOMATION IN NON-METALLIC ENCLOSURE MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

9.12.1 MACHINE CONTROL ENCLOSURES

9.12.2 PANEL MOUNT CASINGS

9.12.3 SENSOR HOUSINGS

9.13 EUROPE INDUSTRIAL AUTOMATION IN NON-METALLIC ENCLOSURE MARKET, BY REGION, 2018-2033 (USD THOUSAND)

9.13.1 NORTH AMERICA

9.13.2 EUROPE

9.13.3 ASIA-PACIFIC

9.13.4 SOUTH AMERICA

9.13.5 MIDDLE EAST & AFRICA

9.14 EUROPE ENERGY & UTILITIES IN NON-METALLIC ENCLOSURE MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

9.14.1 METER ENCLOSURES

9.14.2 SOLAR INVERTER ENCLOSURES

9.14.3 WIND TURBINE COMPONENT HOUSINGS

9.15 EUROPE ENERGY & UTILITIES IN NON-METALLIC ENCLOSURE MARKET, BY REGION, 2018-2033 (USD THOUSAND)

9.15.1 NORTH AMERICA

9.15.2 EUROPE

9.15.3 ASIA-PACIFIC

9.15.4 SOUTH AMERICA

9.15.5 MIDDLE EAST & AFRICA

9.16 EUROPE TELECOMMUNICATIONS IN NON-METALLIC ENCLOSURE MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

9.16.1 OUTDOOR COMMUNICATION ENCLOSURES

9.16.2 FIBER OPTIC JUNCTION BOXES

9.16.3 TELECOM POLE BOXES

9.17 EUROPE TELECOMMUNICATIONS IN NON-METALLIC ENCLOSURE MARKET, BY REGION, 2018-2033 (USD THOUSAND)

9.17.1 NORTH AMERICA

9.17.2 EUROPE

9.17.3 ASIA-PACIFIC

9.17.4 SOUTH AMERICA

9.17.5 MIDDLE EAST & AFRICA

9.18 EUROPE TRANSPORTATION IN NON-METALLIC ENCLOSURE MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

9.18.1 AUTOMOTIVE EV CONTROL BOXES

9.18.2 RAILWAY SIGNALING ENCLOSURES

9.18.3 MARINE & OFFSHORE RATED BOXES

9.19 EUROPE TRANSPORTATION IN NON-METALLIC ENCLOSURE MARKET, BY REGION, 2018-2033 (USD THOUSAND)

9.19.1 NORTH AMERICA

9.19.2 EUROPE

9.19.3 ASIA-PACIFIC

9.19.4 SOUTH AMERICA

9.19.5 MIDDLE EAST & AFRICA

9.2 EUROPE CONSUMER ELECTRONICS IN NON-METALLIC ENCLOSURE MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

9.20.1 SMART HOME DEVICE CASES

9.20.2 WEARABLE ENCLOSURE BODIES

9.21 EUROPE CONSUMER ELECTRONICS IN NON-METALLIC ENCLOSURE MARKET, BY REGION, 2018-2033 (USD THOUSAND)

9.21.1 NORTH AMERICA

9.21.2 EUROPE

9.21.3 ASIA-PACIFIC

9.21.4 SOUTH AMERICA

9.21.5 MIDDLE EAST & AFRICA

9.22 EUROPE MEDICAL & HEALTHCARE IN NON-METALLIC ENCLOSURE MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

9.22.1 MEDICAL DEVICE HOUSINGS

9.22.2 LABORATORY INSTRUMENT ENCLOSURES

9.23 EUROPE MEDICAL & HEALTHCARE IN NON-METALLIC ENCLOSURE MARKET, BY REGION, 2018-2033 (USD THOUSAND)

9.23.1 NORTH AMERICA

9.23.2 EUROPE

9.23.3 ASIA-PACIFIC

9.23.4 SOUTH AMERICA

9.23.5 MIDDLE EAST & AFRICA

9.24 EUROPE DEFENSE & AEROSPACE IN NON-METALLIC ENCLOSURE MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

9.24.1 RUGGEDIZED GRP HOUSINGS

9.24.2 AVIONIC CASINGS

9.25 EUROPE DEFENSE & AEROSPACE IN NON-METALLIC ENCLOSURE MARKET, BY REGION, 2018-2033 (USD THOUSAND)

9.25.1 NORTH AMERICA

9.25.2 EUROPE

9.25.3 ASIA-PACIFIC

9.25.4 SOUTH AMERICA

9.25.5 MIDDLE EAST & AFRICA

10 EUROPE NON-METALLIC ENCLOSURE MARKET, BY FORM FACTOR

10.1 OVERVIEW

10.2 BOX ENCLOSURES

10.3 CABINET & RACK-MOUNT

10.4 DIN-RAIL ENCLOSURES

10.5 CUSTOM & MODULAR ENCLOSURES

10.6 HINGED COVER ENCLOSURES

10.7 SEALED / GASKETED ENCLOSURES

10.8 EUROPE BOX ENCLOSURES IN NON-METALLIC ENCLOSURE MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

10.8.1 WALL-MOUNT

10.8.2 POLE-MOUNT

10.8.3 HANDHELD

10.8.4 TABLETOP

10.9 EUROPE BOX ENCLOSURES IN NON-METALLIC ENCLOSURE MARKET, BY REGION, 2018-2033 (USD THOUSAND)

10.9.1 NORTH AMERICA

10.9.2 EUROPE

10.9.3 ASIA-PACIFIC

10.9.4 SOUTH AMERICA

10.9.5 MIDDLE EAST & AFRICA

10.1 EUROPE CABINET & RACK-MOUNT IN NON-METALLIC ENCLOSURE MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

10.10.1 FLOOR STANDING CABINETS

10.10.2 19” RACK MOUNT POLYMER PANELS

10.11 EUROPE CABINET & RACK-MOUNT IN NON-METALLIC ENCLOSURE MARKET, BY REGION, 2018-2033 (USD THOUSAND)

10.11.1 NORTH AMERICA

10.11.2 EUROPE

10.11.3 ASIA-PACIFIC

10.11.4 SOUTH AMERICA

10.11.5 MIDDLE EAST & AFRICA

10.12 EUROPE DIN-RAIL ENCLOSURES IN NON-METALLIC ENCLOSURE MARKET, BY REGION, 2018-2033 (USD THOUSAND)

10.12.1 NORTH AMERICA

10.12.2 EUROPE

10.12.3 ASIA-PACIFIC

10.12.4 SOUTH AMERICA

10.12.5 MIDDLE EAST & AFRICA

10.13 EUROPE CUSTOM & MODULAR ENCLOSURES IN NON-METALLIC ENCLOSURE MARKET, BY REGION, 2018-2033 (USD THOUSAND)

10.13.1 NORTH AMERICA

10.13.2 EUROPE

10.13.3 ASIA-PACIFIC

10.13.4 SOUTH AMERICA

10.13.5 MIDDLE EAST & AFRICA

10.14 EUROPE HINGED COVER ENCLOSURES IN NON-METALLIC ENCLOSURE MARKET, BY REGION, 2018-2033 (USD THOUSAND)

10.14.1 NORTH AMERICA

10.14.2 EUROPE

10.14.3 ASIA-PACIFIC

10.14.4 SOUTH AMERICA

10.14.5 MIDDLE EAST & AFRICA

10.15 EUROPE SEALED / GASKETED ENCLOSURES IN NON-METALLIC ENCLOSURE MARKET, BY REGION, 2018-2033 (USD THOUSAND)

10.15.1 NORTH AMERICA

10.15.2 EUROPE

10.15.3 ASIA-PACIFIC

10.15.4 SOUTH AMERICA

10.15.5 MIDDLE EAST & AFRICA

11 EUROPE NON-METALLIC ENCLOSURE MARKET, BY MATERIAL TYPE

11.1 OVERVIEW

11.2 THERMOPLASTICS

11.3 THERMOSET COMPOSITES

11.4 ELASTOMERS

11.5 OTHERS

11.6 EUROPE THERMOPLASTICS IN NON-METALLIC ENCLOSURE MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

11.6.1 PC (POLYCARBONATE)

11.6.2 ABS

11.6.3 PVC

11.6.4 PP (POLYPROPYLENE)

11.6.5 PE (POLYETHYLENE)

11.6.6 NYLON

11.6.7 OTHERS

11.7 EUROPE THERMOPLASTICS IN NON-METALLIC ENCLOSURE MARKET, BY REGION, 2018-2033 (USD THOUSAND)

11.7.1 NORTH AMERICA

11.7.2 EUROPE

11.7.3 ASIA-PACIFIC

11.7.4 SOUTH AMERICA

11.7.5 MIDDLE EAST & AFRICA

11.8 EUROPE THERMOSET IN NON-METALLIC ENCLOSURE MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

11.8.1 GRP

11.8.2 FRP

11.8.3 OTHERS

11.9 EUROPE THERMOSET IN NON-METALLIC ENCLOSURE MARKET, BY REGION, 2018-2033 (USD THOUSAND)

11.9.1 NORTH AMERICA

11.9.2 EUROPE

11.9.3 ASIA-PACIFIC

11.9.4 SOUTH AMERICA

11.9.5 MIDDLE EAST & AFRICA

11.1 EUROPE ELASTOMERS IN NON-METALLIC ENCLOSURE MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

11.10.1 TPE

11.10.2 TPU

11.11 EUROPE ELASTOMERS IN NON-METALLIC ENCLOSURE MARKET, BY REGION, 2018-2033 (USD THOUSAND)

11.11.1 NORTH AMERICA

11.11.2 EUROPE

11.11.3 ASIA-PACIFIC

11.11.4 SOUTH AMERICA

11.11.5 MIDDLE EAST & AFRICA

11.12 EUROPE OTHERS IN NON-METALLIC ENCLOSURE MARKET, BY REGION, 2018-2033 (USD THOUSAND)

11.12.1 NORTH AMERICA

11.12.2 EUROPE

11.12.3 ASIA-PACIFIC

11.12.4 SOUTH AMERICA

11.12.5 MIDDLE EAST & AFRICA

12 EUROPE NON-METALLIC ENCLOSURE MARKET, BY DISTRIBUTION CHANNEL

12.1 OVERVIEW

12.2 OEM DIRECT SALES

12.3 DISTRIBUTORS / VALUE-ADDED RESELLERS

12.4 SYSTEM INTEGRATORS & PANEL BUILDERS

12.5 ONLINE INDUSTRIAL MARKETPLACES

12.6 RETAIL

12.7 EUROPE OEM DIRECT SALES IN NON-METALLIC ENCLOSURE MARKET, BY REGION, 2018-2033 (USD THOUSAND)

12.7.1 NORTH AMERICA

12.7.2 EUROPE

12.7.3 ASIA-PACIFIC

12.7.4 SOUTH AMERICA

12.7.5 MIDDLE EAST & AFRICA

12.8 EUROPE DISTRIBUTORS / VALUE-ADDED RESELLERS IN NON-METALLIC ENCLOSURE MARKET, BY REGION, 2018-2033 (USD THOUSAND)

12.8.1 NORTH AMERICA

12.8.2 EUROPE

12.8.3 ASIA-PACIFIC

12.8.4 SOUTH AMERICA

12.8.5 MIDDLE EAST & AFRICA

12.9 EUROPE SYSTEM INTEGRATORS & PANEL BUILDERS IN NON-METALLIC ENCLOSURE MARKET, BY REGION, 2018-2033 (USD THOUSAND)

12.9.1 NORTH AMERICA

12.9.2 EUROPE

12.9.3 ASIA-PACIFIC

12.9.4 SOUTH AMERICA

12.9.5 MIDDLE EAST & AFRICA

12.1 EUROPE ONLINE INDUSTRIAL MARKETPLACES IN NON-METALLIC ENCLOSURE MARKET, BY REGION, 2018-2033 (USD THOUSAND)

12.10.1 NORTH AMERICA

12.10.2 EUROPE

12.10.3 ASIA-PACIFIC

12.10.4 SOUTH AMERICA

12.10.5 MIDDLE EAST & AFRICA

12.11 EUROPE RETAIL IN NON-METALLIC ENCLOSURE MARKET, BY REGION, 2018-2033 (USD THOUSAND)

12.11.1 NORTH AMERICA

12.11.2 EUROPE

12.11.3 ASIA-PACIFIC

12.11.4 SOUTH AMERICA

12.11.5 MIDDLE EAST & AFRICA

13 EUROPE NON-METALLIC ENCLOSURE MARKET, BY REGION

13.1 NORTH AMERICA

13.1.1 U.S.

13.1.2 CANADA

14 EUROPE NON-METALLIC ENCLOSURE MARKET: COMPANY LANDSCAPE

14.1 MANUFACTURER COMPANY SHARE ANALYSIS: GLOBAL

15 SWOT ANALYSIS

16 COMPANY PROIFILE

16.1 SCHNEIDER ELECTRIC

16.1.1 COMPANY SNAPSHOT

16.1.2 REVENUE ANALYSIS

16.1.3 COMPANY SHARA ANALYSIS

16.1.4 PRODUCT PORTFOLIO

16.1.5 RECENT DEVELOPMENT

16.2 ABB

16.2.1 COMPANY SNAPSHOT

16.2.2 REVENUE ANALYSIS

16.2.3 COMPANY SHARA ANALYSIS

16.2.4 PRODUCT PORTFOLIO

16.2.5 RECENT DEVELOPMENT

16.3 RITTAL GMBH & CO. KG

16.3.1 COMPANY SNAPSHOT

16.3.2 COMPANY SHARA ANALYSIS

16.3.3 PRODUCT PORTFOLIO

16.3.4 RECENT DEVELOPMENTS

16.4 EATON

16.4.1 COMPANY SNAPSHOT

16.4.2 REVENUE ANALYSIS

16.4.3 COMPANY SHARE ANALYSIS

16.4.4 PRODUCT PORTFOLIO

16.4.5 RECENT DEVELOPMENT

16.5 LEGRAND

16.5.1 COMPANY SNAPSHOT

16.5.2 REVENUE ANALYSIS

16.5.3 COMPANY SHARA ANALYSIS

16.5.4 PRODUCT PORTFOLIO

16.5.5 RECENT DEVELOPMETS

16.6 ALLBRO

16.6.1 COMPANY SNAPSHOT

16.6.2 PRODUCT PORTFOLIO

16.6.3 RECENT DEVELOPMENTS

16.7 ALLIED MOULDED PRODUCTS, INC.

16.7.1 COMPANY SNAPSHOT

16.7.2 PRODUCT PORTFOLIO

16.7.3 RECENT DEVELOPMENTS

16.8 ARLINGTON INDUSTRIES, INC.

16.8.1 COMPANY SNAPSHOT

16.8.2 PRODUCT PORTFOLIO

16.8.3 RECENT DEVELOPMENT

16.9 B&R ENCLOSURES PTY LTD

16.9.1 COMPANY SNAPSHOT

16.9.2 PRODUCT PORTFOLIO

16.9.3 RECENT DEVELOPMENTS

16.1 BCH ELECTRIC LIMITED

16.10.1 COMPANY SNAPSHOT

16.10.2 PRODUCT PORTFOLIO

16.10.3 RECENT DEVELOPMENTS

16.11 BOPLA GEHÄUSE SYSTEME GMBH

16.11.1 COMPANY SNAPSHOT

16.11.2 PRODUCT PORTFOLIO

16.11.3 RECENT DEVELOPMENT

16.12 BUD INDUSTRIES

16.12.1 COMPANY SNAPSHOT

16.12.2 PRODUCT PORTFOLIO

16.12.3 RECENT DEVELOPMENTS

16.13 CHINT EUROPE INTERNATIONAL PTE LTD

16.13.1 COMPANY SNAPSHOT

16.13.2 PRODUCT PORTFOLIO

16.13.3 RECENT DEVELOPMENTS

16.14 DELIXI ELECTRIC

16.14.1 COMPANY SNAPSHOT

16.14.2 PRODUCT PORTFOLIO

16.14.3 RECENT DEVELOPMENTS

16.15 ENGINEERED PRODUCTS COMPANY (EPCO)

16.15.1 COMPANY SNAPSHOT

16.15.2 PRODUCT PORTFOLIO

16.15.3 RECENT DEVELOPMENT

16.16 FCG FLAMEPROOF CONTROL GEARS (INDIA) PVT LTD

16.16.1 COMPANY SNAPSHOT

16.16.2 PRODUCT PORTFOLIO

16.16.3 RECENT DEVELOPMENT

16.17 GUSTAV HENSEL GMBH & CO. KG

16.17.1 COMPANY SNAPSHOT

16.17.2 PRODUCT PORTFOLIO

16.17.3 RECENT DEVELOPMENT

16.18 HAMMOND MANUFACTURING LTD.

16.18.1 COMPANY SNAPSHOT

16.18.2 PRODUCT PORTFOLIO

16.18.3 RECENT DEVELOPMENT

16.19 HYLEC-APL LTD

16.19.1 COMPANY SNAPSHOT

16.19.2 PRODUCT PORTFOLIO

16.19.3 RECENT DEVELOPMENTS

16.2 LEOTECH

16.20.1 COMPANY SNAPSHOT

16.20.2 PRODUCT PORTFOLIO

16.20.3 RECENT DEVELOPMENT

16.21 OKW ENCLOSURE SYSTEMS

16.21.1 COMPANY SNAPSHOT

16.21.2 PRODUCT PORTFOLIO

16.21.3 RECENT DEVELOPMENTS

16.22 PHOENIX CONTACT

16.22.1 COMPANY SNAPSHOT

16.22.2 PRODUCT PORTFOLIO

16.22.3 RECENT DEVELOPMENT

16.23 POLYCASE

16.23.1 COMPANY SNAPSHOT

16.23.2 PRODUCT PORTFOLIO

16.23.3 RECENT DEVELOPMENTS

16.24 SAGINAW CONTROL AND ENGINEERING

16.24.1 COMPANY SNAPSHOT

16.24.2 PRODUCT PORTFOLIO

16.24.3 RECENT DEVELOPMENT

16.25 SAIPWELL ELECTRIC CO., LTD.

16.25.1 COMPANY SNAPSHOT

16.25.2 PRODUCT PORTFOLIO

16.25.3 RECENT DEVELOPMETS

16.26 STAHLIN

16.26.1 COMPANY SNAPSHOT

16.26.2 PRODUCT PORTFOLIO

16.26.3 RECENT DEVELOPMENTS

16.27 TAKACHI ELECTRONICS ENCLOSURE CO., LTD.

16.27.1 COMPANY SNAPSHOT

16.27.2 PRODUCT PORTFOLIO

16.27.3 RECENT DEVELOPMENT

16.28 TE CONNECTIVITY

16.28.1 COMPANY SNAPSHOT

16.28.2 REVENUE ANALYSIS

16.28.3 PRODUCT PORTFOLIO

16.28.4 RECENT DEVELOPMENT

16.29 UNIBOX ENCLOSURES

16.29.1 COMPANY SNAPSHOT

16.29.2 PRODUCT PORTFOLIO

16.29.3 RECENT DEVELOPMENT

16.3 VSM PLAST

16.30.1 COMPANY SNAPSHOT

16.30.2 PRODUCT PORTFOLIO

16.30.3 RECENT DEVELOPMENTS

17 QUESTIONNAIRE

18 RELATED REPORTS

List of Table

TABLE 1 PENETRATION AND GROWTH PROSPECT BY PRODUCT TYPE

TABLE 2 PENETRATION AND GROWTH PROSPECT BY APPLICATION

TABLE 3 NEW BUSINESS REVENUE OPPORTUNITIES

TABLE 4 EMERGING BUSINESS REVENUE OPPORTUNITIES

TABLE 5 COMPANY COMPARATIVE ANALYSIS

TABLE 6 VENDOR SELECTION CRITERIA

TABLE 7 WEIGHTAGE ALLOCATION TABLE

TABLE 8 INNOVATION STRATEGIES AND METHODOLOGIES

TABLE 9 RISK ASSESSMENT AND MITIGATION

TABLE 10 CONSUMER PREFERENCE MATRIX

TABLE 11 EUROPE NON-METALLIC ENCLOSURE MARKET, BY PRODUCT TYPE, 2018-2033 (USD THOUSAND)

TABLE 12 EUROPE POLYMER & PLASTIC ENCLOSURES IN NON-METALLIC ENCLOSURE MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 13 EUROPE POLYMER & PLASTIC ENCLOSURES IN NON-METALLIC ENCLOSURE MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 14 EUROPE COMPOSITE ENCLOSURES IN NON-METALLIC ENCLOSURE MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 15 EUROPE COMPOSITE ENCLOSURES IN NON-METALLIC ENCLOSURE MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 16 EUROPE THERMOPLASTIC ELASTOMER ENCLOSURES IN NON-METALLIC ENCLOSURE MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 17 EUROPE THERMOPLASTIC ELASTOMER ENCLOSURES IN NON-METALLIC ENCLOSURE MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 18 EUROPE OTHER SPECIALTY POLYMERS IN NON-METALLIC ENCLOSURE MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 19 EUROPE OTHER SPECIALTY POLYMERS IN NON-METALLIC ENCLOSURE MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 20 EUROPE NON-METALLIC ENCLOSURE MARKET, BY APPLICATION, 2018-2033 (USD THOUSAND)

TABLE 21 EUROPE ELECTRICAL & ELECTRONICS IN NON-METALLIC ENCLOSURE MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 22 EUROPE ELECTRICAL & ELECTRONICS IN NON-METALLIC ENCLOSURE MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 23 EUROPE INDUSTRIAL AUTOMATION IN NON-METALLIC ENCLOSURE MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 24 EUROPE INDUSTRIAL AUTOMATION IN NON-METALLIC ENCLOSURE MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 25 EUROPE ENERGY & UTILITIES IN NON-METALLIC ENCLOSURE MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 26 EUROPE ENERGY & UTILITIES IN NON-METALLIC ENCLOSURE MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 27 EUROPE TELECOMMUNICATIONS IN NON-METALLIC ENCLOSURE MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 28 EUROPE TELECOMMUNICATIONS IN NON-METALLIC ENCLOSURE MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 29 EUROPE TRANSPORTATION IN NON-METALLIC ENCLOSURE MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 30 EUROPE TRANSPORTATION IN NON-METALLIC ENCLOSURE MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 31 EUROPE CONSUMER ELECTRONICS IN NON-METALLIC ENCLOSURE MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 32 EUROPE CONSUMER ELECTRONICS IN NON-METALLIC ENCLOSURE MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 33 EUROPE MEDICAL & HEALTHCARE IN NON-METALLIC ENCLOSURE MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 34 EUROPE MEDICAL & HEALTHCARE IN NON-METALLIC ENCLOSURE MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 35 EUROPE DEFENSE & AEROSPACE IN NON-METALLIC ENCLOSURE MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 36 EUROPE DEFENSE & AEROSPACE IN NON-METALLIC ENCLOSURE MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 37 EUROPE NON-METALLIC ENCLOSURE MARKET, BY FORM FACTOR, 2018-2033 (USD THOUSAND)

TABLE 38 EUROPE BOX ENCLOSURES IN NON-METALLIC ENCLOSURE MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 39 EUROPE BOX ENCLOSURES IN NON-METALLIC ENCLOSURE MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 40 EUROPE CABINET & RACK-MOUNT IN NON-METALLIC ENCLOSURE MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 41 EUROPE CABINET & RACK-MOUNT IN NON-METALLIC ENCLOSURE MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 42 EUROPE DIN-RAIL ENCLOSURES IN NON-METALLIC ENCLOSURE MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 43 EUROPE CUSTOM & MODULAR ENCLOSURES IN NON-METALLIC ENCLOSURE MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 44 EUROPE HINGED COVER ENCLOSURES IN NON-METALLIC ENCLOSURE MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 45 EUROPE SEALED / GASKETED ENCLOSURES IN NON-METALLIC ENCLOSURE MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 46 EUROPE NON-METALLIC ENCLOSURE MARKET, BY MATERIAL TYPE, 2018-2033 (USD THOUSAND)

TABLE 47 EUROPE THERMOPLASTICS IN NON-METALLIC ENCLOSURE MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 48 EUROPE THERMOPLASTICS IN NON-METALLIC ENCLOSURE MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 49 EUROPE THERMOSET IN NON-METALLIC ENCLOSURE MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 50 EUROPE THERMOSET IN NON-METALLIC ENCLOSURE MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 51 EUROPE ELASTOMERS IN NON-METALLIC ENCLOSURE MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 52 EUROPE ELASTOMERS IN NON-METALLIC ENCLOSURE MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 53 EUROPE OTHERS IN NON-METALLIC ENCLOSURE MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 54 EUROPE NON-METALLIC ENCLOSURE MARKET, BY DISTRIBUTION CHANNEL, 2018-2033 (USD THOUSAND)

TABLE 55 EUROPE OEM DIRECT SALES IN NON-METALLIC ENCLOSURE MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 56 EUROPE DISTRIBUTORS / VALUE-ADDED RESELLERS IN NON-METALLIC ENCLOSURE MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 57 EUROPE SYSTEM INTEGRATORS & PANEL BUILDERS IN NON-METALLIC ENCLOSURE MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 58 EUROPE ONLINE INDUSTRIAL MARKETPLACES IN NON-METALLIC ENCLOSURE MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 59 EUROPE RETAIL IN NON-METALLIC ENCLOSURE MARKET, BY REGION, 2018-2033 (USD THOUSAND)

TABLE 60 REGION

TABLE 61 NORTH AMERICA NON-METALLIC ENCLOSURE MARKET, BY COUNTRY, 2018-2033 (USD THOUSAND)

TABLE 62 NORTH AMERICA

TABLE 63 NORTH AMERICA NON-METALLIC ENCLOSURE MARKET, BY PRODUCT TYPE, 2018-2033 (USD THOUSAND)

TABLE 64 NORTH AMERICA POLYMER & PLASTIC ENCLOSURES IN NON-METALLIC ENCLOSURE MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 65 NORTH AMERICACOMPOSITE ENCLOSURES IN NON-METALLIC ENCLOSURE MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 66 NORTH AMERICA THERMOPLASTIC ELASTOMER ENCLOSURES IN NON-METALLIC ENCLOSURE MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 67 NORTH AMERICA OTHER SPECIALTY POLYMERS IN NON-METALLIC ENCLOSURE MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 68 NORTH AMERICA NON-METALLIC ENCLOSURE MARKET, BY APPLICATIONS, 2018-2033 (USD THOUSAND)

TABLE 69 NORTH AMERICA ELECTRICAL & ELECTRONICS IN NON-METALLIC ENCLOSURE MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 70 NORTH AMERICA INDUSTRIAL AUTOMATION IN NON-METALLIC ENCLOSURE MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 71 NORTH AMERICA ENERGY & UTILITIES IN NON-METALLIC ENCLOSURE MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 72 NORTH AMERICA TELECOMMUNICATIONS IN NON-METALLIC ENCLOSURE MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 73 NORTH AMERICA TRANSPORTATION IN NON-METALLIC ENCLOSURE MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 74 NORTH AMERICA CONSUMER ELECTRONICS IN NON-METALLIC ENCLOSURE MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 75 NORTH AMERICA MEDICAL & HEALTHCARE IN NON-METALLIC ENCLOSURE MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 76 NORTH AMERICA DEFENSE & AEROSPACE IN NON-METALLIC ENCLOSURE MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 77 NORTH AMERICA NON-METALLIC ENCLOSURE MARKET, BY FORM FACTOR, 2018-2033 (USD THOUSAND)

TABLE 78 NORTH AMERICA BOX ENCLOSURES IN NON-METALLIC ENCLOSURE MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 79 NORTH AMERICA CABINET & RACK-MOUNT IN NON-METALLIC ENCLOSURE MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 80 NORTH AMERICA NON-METALLIC ENCLOSURE MARKET, BY MATERIAL TYPE, 2018-2033 (USD THOUSAND)

TABLE 81 NORTH AMERICATHERMOPLASTICS IN NON-METALLIC ENCLOSURE MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 82 NORTH AMERICATHERMOSET IN NON-METALLIC ENCLOSURE MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 83 NORTH AMERICAELASTOMERS IN NON-METALLIC ENCLOSURE MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 84 NORTH AMERICA NON-METALLIC ENCLOSURE MARKET, BY DISTRIBUTION CHANNEL, 2018-2033 (USD THOUSAND)

TABLE 85 U.S. NON-METALLIC ENCLOSURE MARKET, BY PRODUCT TYPE, 2018-2033 (USD THOUSAND)

TABLE 86 U.S. POLYMER & PLASTIC ENCLOSURES IN NON-METALLIC ENCLOSURE MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 87 U.S.COMPOSITE ENCLOSURES IN NON-METALLIC ENCLOSURE MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 88 U.S. THERMOPLASTIC ELASTOMER ENCLOSURES IN NON-METALLIC ENCLOSURE MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 89 U.S. OTHER SPECIALTY POLYMERS IN NON-METALLIC ENCLOSURE MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 90 U.S. NON-METALLIC ENCLOSURE MARKET, BY APPLICATIONS, 2018-2033 (USD THOUSAND)

TABLE 91 U.S. ELECTRICAL & ELECTRONICS IN NON-METALLIC ENCLOSURE MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 92 U.S. INDUSTRIAL AUTOMATION IN NON-METALLIC ENCLOSURE MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 93 U.S. ENERGY & UTILITIES IN NON-METALLIC ENCLOSURE MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 94 U.S. TELECOMMUNICATIONS IN NON-METALLIC ENCLOSURE MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 95 U.S. TRANSPORTATION IN NON-METALLIC ENCLOSURE MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 96 U.S. CONSUMER ELECTRONICS IN NON-METALLIC ENCLOSURE MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 97 U.S. MEDICAL & HEALTHCARE IN NON-METALLIC ENCLOSURE MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 98 U.S. DEFENSE & AEROSPACE IN NON-METALLIC ENCLOSURE MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 99 U.S. NON-METALLIC ENCLOSURE MARKET, BY FORM FACTOR, 2018-2033 (USD THOUSAND)

TABLE 100 U.S. BOX ENCLOSURES IN NON-METALLIC ENCLOSURE MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 101 U.S. CABINET & RACK-MOUNT IN NON-METALLIC ENCLOSURE MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 102 U.S. NON-METALLIC ENCLOSURE MARKET, BY MATERIAL TYPE, 2018-2033 (USD THOUSAND)

TABLE 103 U.S.THERMOPLASTICS IN NON-METALLIC ENCLOSURE MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 104 U.S.THERMOSET IN NON-METALLIC ENCLOSURE MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 105 U.S.ELASTOMERS IN NON-METALLIC ENCLOSURE MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 106 U.S. NON-METALLIC ENCLOSURE MARKET, BY DISTRIBUTION CHANNEL, 2018-2033 (USD THOUSAND)

TABLE 107 CANADA NON-METALLIC ENCLOSURE MARKET, BY PRODUCT TYPE, 2018-2033 (USD THOUSAND)

TABLE 108 CANADA POLYMER & PLASTIC ENCLOSURES IN NON-METALLIC ENCLOSURE MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 109 CANADACOMPOSITE ENCLOSURES IN NON-METALLIC ENCLOSURE MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 110 CANADA THERMOPLASTIC ELASTOMER ENCLOSURES IN NON-METALLIC ENCLOSURE MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 111 CANADA OTHER SPECIALTY POLYMERS IN NON-METALLIC ENCLOSURE MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 112 CANADA NON-METALLIC ENCLOSURE MARKET, BY APPLICATIONS, 2018-2033 (USD THOUSAND)

TABLE 113 CANADA ELECTRICAL & ELECTRONICS IN NON-METALLIC ENCLOSURE MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 114 CANADA INDUSTRIAL AUTOMATION IN NON-METALLIC ENCLOSURE MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 115 CANADA ENERGY & UTILITIES IN NON-METALLIC ENCLOSURE MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 116 CANADA TELECOMMUNICATIONS IN NON-METALLIC ENCLOSURE MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 117 CANADA TRANSPORTATION IN NON-METALLIC ENCLOSURE MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 118 CANADA CONSUMER ELECTRONICS IN NON-METALLIC ENCLOSURE MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 119 CANADA MEDICAL & HEALTHCARE IN NON-METALLIC ENCLOSURE MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 120 CANADA DEFENSE & AEROSPACE IN NON-METALLIC ENCLOSURE MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 121 CANADA NON-METALLIC ENCLOSURE MARKET, BY FORM FACTOR, 2018-2033 (USD THOUSAND)

TABLE 122 CANADA BOX ENCLOSURES IN NON-METALLIC ENCLOSURE MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 123 CANADA CABINET & RACK-MOUNT IN NON-METALLIC ENCLOSURE MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 124 CANADA NON-METALLIC ENCLOSURE MARKET, BY MATERIAL TYPE, 2018-2033 (USD THOUSAND)

TABLE 125 CANADATHERMOPLASTICS IN NON-METALLIC ENCLOSURE MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 126 CANADATHERMOSET IN NON-METALLIC ENCLOSURE MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 127 CANADAELASTOMERS IN NON-METALLIC ENCLOSURE MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 128 CANADA NON-METALLIC ENCLOSURE MARKET, BY DISTRIBUTION CHANNEL, 2018-2033 (USD THOUSAND)

List of Figure

FIGURE 1 EUROPE NON-METALLIC ENCLOSURE MARKET: SEGMENTATION

FIGURE 2 EUROPE NON-METALLIC ENCLOSURE MARKET: DATA TRIANGULATION

FIGURE 3 EUROPE NON-METALLIC ENCLOSURE MARKET: DROC ANALYSIS

FIGURE 4 EUROPE NON-METALLIC ENCLOSURE MARKET: EUROPE VS REGIONAL MARKET ANALYSIS

FIGURE 5 EUROPE NON-METALLIC ENCLOSURE MARKET: COMPANY RESEARCH ANALYSIS

FIGURE 6 EUROPE NON-METALLIC ENCLOSURE MARKET: INTERVIEW DEMOGRAPHICS

FIGURE 7 EUROPE NON-METALLIC ENCLOSURE MARKET: DBMR MARKET POSITION GRID

FIGURE 8 EUROPE NON-METALLIC ENCLOSURE MARKET: VENDOR SHARE ANALYSIS

FIGURE 9 EUROPE NON-METALLIC ENCLOSURE MARKET: MULTIVARIVATE MODELING

FIGURE 10 EUROPE NON-METALLIC ENCLOSURE MARKET: PRODUCT TYPE TIMELINE CURVE

FIGURE 11 EUROPE NON-METALLIC ENCLOSURE MARKET: APPLICATION COVERAGE GRID

FIGURE 12 EUROPE NON-METALLIC ENCLOSURE MARKET: SEGMENTATION

FIGURE 13 FOUR SEGMENTS COMPRISE THE EUROPE NON-METALLIC ENCLOSURE MARKET, BY PRODUCT TYPE (2025)

FIGURE 14 EUROPE NON-METALLIC ENCLOSURE MARKET: EXECUTIVE SUMMARY

FIGURE 15 STRATEGIC DECISIONS

FIGURE 16 INCREASING DEMAND FOR CORROSION-RESISTANT SOLUTIONS IS EXPECTED TO DRIVE THE EUROPE NON-METALLIC ENCLOSURE MARKET DURING THE FORECAST PERIOD OF 2026 TO 2033

FIGURE 17 PRODUCT TYPE SEGMENT IS EXPECTED TO ACCOUNT FOR THE LARGEST SHARE OF THE EUROPE NON-METALLIC ENCLOSURE MARKET IN 2025 & 2033

FIGURE 18 PORTER’S FIVE FORCES ANALYSIS

FIGURE 19 DROC ANALYSIS

FIGURE 20 INDIA’S TELECOM SECTOR GROSS REVENUE:

FIGURE 21 EUROPE NON-METALLIC ENCLOSURE MARKET, BY PRODUCT TYPE, 2025

FIGURE 22 EUROPE NON-METALLIC ENCLOSURE MARKET, BY APPLICATION, 2025

FIGURE 23 EUROPE NON-METALLIC ENCLOSURE MARKET, BY FORM FACTOR, 2025

FIGURE 24 EUROPE NON-METALLIC ENCLOSURE MARKET, BY MATERIAL TYPE, 2025

FIGURE 25 EUROPE NON-METALLIC ENCLOSURE MARKET, BY DISTRIBUTION CHANNEL, 2025

FIGURE 26 NORTH AMERICA NON-METALLIC ENCLOSURE MARKET: SNAPSHOT

FIGURE 27 EUROPE NON-METALLIC ENCLOSURE MARKET: COMPANY SHARE 2025 (%)

Europe Non Metallic Enclosure Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Europe Non Metallic Enclosure Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Europe Non Metallic Enclosure Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.