Europe Nuclear Imaging Devices Market

Market Size in USD Million

USD

238.12 Million

USD

320.90 Million

2024

2032

USD

238.12 Million

USD

320.90 Million

2024

2032

| 2025 - 2032 | |

| USD 238.12 Million | |

| USD 320.90 Million | |

| % | |

|

Nuclear Imaging Devices Market Size

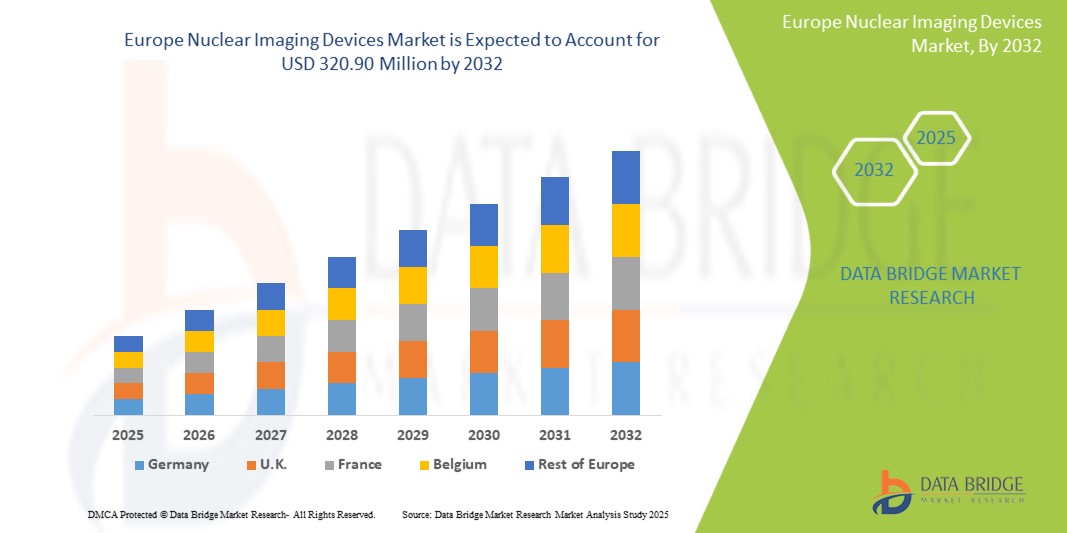

- The Europe Nuclear Imaging Devices Market Treatment market was valued at USD 238.12 million in 2024 and is expected to reach USD 320.90 Million by 2032, at a CAGR of 3.8%, during the forecast period

- The increasing prevalence of chronic kidney disease (CKD) and a strong focus on early diagnosis and intervention are fueling demand for the Nuclear Imaging Devices Market in Europe. Furthermore, growing public and professional awareness regarding kidney health, along with technological advancements in haemodialysis and peritoneal dialysis solutions, is contributing to the market’s expansion..

Nuclear Imaging Devices Market Analysis

- The increasing prevalence of chronic kidney disease (CKD) and a strong focus on early diagnosis and intervention are fueling demand for the Nuclear Imaging Devices Market in Europe. Furthermore, growing public and professional awareness regarding kidney health, along with technological advancements in haemodialysis and peritoneal dialysis solutions, is contributing to the market’s expansion.

- Nuclear Imaging Devices are specialized machines used to detect and monitor abnormalities in organs and tissues, playing a vital role in the diagnosis and management of conditions such as chronic kidney disease (CKD). These devices help visualize functional information that complements anatomical imaging, supporting early detection, disease staging, and treatment planning. Advanced nuclear imaging technologies, including PET and SPECT systems, enhance diagnostic accuracy and patient outcomes.

- Germany, the United Kingdom, and France emerge as leading markets within Europe, supported by robust healthcare infrastructure, growing adoption of advanced imaging modalities, and proactive healthcare policies promoting early diagnosis and preventive care.

- Ongoing investments in nuclear medicine, including hybrid imaging systems, AI-integrated diagnostics, and personalized imaging protocols, alongside a growing elderly population and rising CKD burden, continue to accelerate innovation and growth in the region’s Nuclear Imaging Devices market.

Report Scope and Nuclear Imaging Devices Market Segmentation

|

Attributes |

Nuclear Imaging Devices Market Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Europe

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Nuclear Imaging Devices Market Trends

“Integration of Artificial Intelligence in Nuclear Imaging”

- A key trend shaping the Europe Nuclear Imaging Devices Market is the growing integration of artificial intelligence (AI) in nuclear imaging technologies, aimed at improving diagnostic precision, workflow efficiency, and clinical outcomes.

- AI-powered tools are increasingly being used to automate image reconstruction, enhance image quality, and assist radiologists in detecting early signs of disease, particularly in complex conditions such as chronic kidney disease (CKD).

- For instance, AI algorithms can rapidly analyze imaging data to identify subtle abnormalities, reducing diagnostic errors and supporting faster, more informed clinical decisions.

- The use of machine learning and predictive analytics is also enabling personalized patient care, allowing clinicians to tailor imaging protocols based on individual risk profiles and disease progression.

- This trend is helping to streamline nuclear imaging operations, reduce radiologist workload, and improve patient throughput—factors that are boosting the adoption of advanced imaging systems across healthcare facilities in Europe.

- As regulatory bodies increasingly recognize the value of AI in medical imaging, continued investment and collaboration between tech companies and healthcare providers are expected to drive further innovation and market growth.

Nuclear Imaging Devices Market Dynamics

Driver

“Growing Emphasis on Early Disease Detection and Preventive Healthcare”

- The shift in European healthcare systems from reactive to preventive care is driving the adoption of advanced diagnostic tools such as nuclear imaging devices. Governments and healthcare providers are investing in technologies that enable early disease detection to reduce long-term treatment costs and improve patient outcomes.

- Nuclear imaging plays a key role in detecting renal and cardiovascular complications in their early stages, particularly among high-risk groups such as the elderly and patients with chronic conditions.

For instance,

- The European Commission’s “Europe’s Beating Cancer Plan” and national CKD screening initiatives are expanding access to diagnostic imaging services as part of comprehensive early intervention strategies.

- In 2024, the UK’s NHS announced increased funding for community-based imaging centers to improve access to early diagnostic services, including nuclear imaging.

- As the burden of chronic disease grows across the continent, there is rising demand for non-invasive, high-accuracy diagnostic tools. This trend is significantly boosting the Nuclear Imaging Devices Market in Europe.

Opportunity

“Expansion of Hybrid Imaging Technologies and Multi-Modality Platforms”

- Hybrid imaging systems, such as PET/CT and SPECT/CT, are gaining popularity in Europe due to their ability to provide both anatomical and functional information in a single scan, improving diagnostic accuracy and patient workflow.

- The growing integration of nuclear imaging with other imaging modalities like MRI and ultrasound offers more precise and holistic assessments, particularly in complex cases involving CKD, cancer, or cardiovascular disease.

For instance,

- Hospitals across Germany and the Netherlands have rapidly adopted PET/MRI systems for their ability to offer superior soft-tissue contrast alongside metabolic imaging—critical for comprehensive CKD assessment.

- In 2024, several EU-funded research programs supported the development of modular imaging platforms that combine nuclear imaging with AI-assisted image analysis.

- These innovations are not only enhancing clinical outcomes but also creating opportunities for vendors offering integrated diagnostic ecosystems that support precision medicine and streamlined workflows.

Restraint/Challenge

“Workforce Shortages and Limited Radiology Training”

- Despite growing demand, a persistent shortage of skilled radiologists and nuclear medicine specialists in Europe is limiting the full-scale adoption of advanced imaging technologies. Many healthcare facilities, especially in rural or underserved areas, lack personnel trained to operate and interpret nuclear imaging systems.

- The complexity of modern hybrid imaging platforms and AI-based diagnostic tools requires continuous professional development, which many institutions struggle to fund or prioritize.

For instance,

- A 2023 report from the European Society of Radiology (ESR) highlighted that over 30% of imaging departments in Eastern and Southern Europe face radiologist shortages, leading to longer diagnostic delays.

- EU-wide surveys show a growing need for harmonized nuclear medicine training programs and cross-border accreditation to meet future imaging demands.

- Without adequate workforce support and standardized training pathways, healthcare systems may face challenges in maintaining diagnostic efficiency and expanding nuclear imaging services—ultimately restraining market growth.

Nuclear Imaging Devices Market Scope

The market is segmented on the product type, application, end user.

|

Segmentation |

Sub-Segmentation |

|

By Product type |

|

|

By application |

|

|

By End Users |

|

In 2025, the Single Photon-Emission Computed Tomography (SPECT) Solutions is Projected to Dominate the Market with the Largest Share in the product type Segment

The Single Photon-Emission Computed Tomography (SPECT) segment is expected to dominate the Europe Nuclear Imaging Devices Market in 2025, accounting for the largest market share of approximately 68.7%. This leadership is primarily driven by the widespread clinical adoption of SPECT for cardiac, renal, and neurological imaging. Its cost-effectiveness, broad diagnostic applications, and integration with hybrid imaging technologies further reinforce its market dominance.

In 2025, Oncology are Expected to Account for the Largest Share During the Forecast Period in application segment

In 2025, Oncology are projected to dominate the Europe Nuclear Imaging Devices Market , accounting for the largest market share of approximately 64.9%. This segment's dominance is fueled by the increasing prevalence of cancer, the growing demand for early and precise tumor detection, and advancements in imaging technologies such as PET/CT and SPECT. These innovations enhance the accuracy of cancer staging, monitoring, and treatment planning, driving widespread adoption in oncology care.

Nuclear Imaging Devices Market Regional Analysis

“Germany is the Dominant country in the Europe Nuclear Imaging Devices Market ”

- Germany leads the Europe Nuclear Imaging Devices Market, driven by its robust healthcare infrastructure, high diagnostic volumes, and the early adoption of advanced imaging technologies such as PET/CT and SPECT systems for oncology, neurology, and cardiology.

- Germany holds the largest market share due to a combination of factors, including a high incidence of chronic diseases, a strong emphasis on early diagnosis, and a well-established medical reimbursement system.

- Government policies and funding for research in nuclear medicine, along with significant investments in healthcare innovation, further support the market's growth in the country.

- Additionally, the presence of major medical device manufacturers such as Siemens Healthineers and Philips, coupled with continuous advancements in nuclear imaging, bolsters Germany’s position as the market leader.

“France is Projected to Register the Highest Growth Rate”

- France is projected to witness the highest growth rate in the Europe Nuclear Imaging Devices Market, fueled by increasing awareness of the importance of early disease detection, expanding access to nuclear imaging technologies, and technological innovations in imaging systems.

- The market benefits from extensive national health campaigns, a growing elderly population, and the increasing prevalence of chronic diseases such as cancer, cardiovascular diseases, and neurological disorders.

- Government-driven initiatives, including subsidies for medical imaging equipment and funding for nuclear medicine research, are further accelerating the adoption of advanced imaging devices.

- Innovations in hybrid imaging technologies, integration of AI into diagnostics, and the push toward personalized medicine are expected to drive rapid market expansion in France, especially in oncology and cardiovascular imaging.

Nuclear Imaging Devices Market Share

The market competitive landscape provides details by competitor. Details included are company overview, company financials, revenue generated, market potential, investment in research and development, new market initiatives, Europe presence, production sites and facilities, production capacities, company strengths and weaknesses, product launch, product width and breadth, application dominance. The above data points provided are only related to the companies' focus related to market.

The Major Market Leaders Operating in the Market Are:

- Siemens Healthineers (Germany)

- Philips Healthcare (Netherlands)

- GE Healthcare (United States)

- Canon Medical Systems Corporation (Japan)

- Medtronic (Ireland)

- Baxter International Inc. (United States)

- Fresenius Medical Care (Germany)

- Elekta AB (Sweden)

- Varian Medical Systems (United States)

- Shimadzu Corporation (Japan)

Latest Developments in Europe Nuclear Imaging Devices Market

- in October 2021, PRISMAP, a new medical radionuclide program, was launched to streamline access to medical research in the European Union and the United Kingdom. PRISMAP serves a consortium of 23 institutions from 13 countries, providing access to intense neutron sources, isotope mass separation facilities, and high-power accelerators and cyclotrons to the biomedical and healthcare research institutions putting those radioisotopes into use in medical diagnosis and treatment.

- in April 2021, the Oncidium Foundation, Belgium, a non-profit organization, in partnership with Telix Pharmaceuticals Limited, launched the NOBLE Registry, an international clinical collaboration for the development of 99mTc-iPSMA SPECT imaging for prostate cancer. The NOBLE demonstrates that PSMA single-photon emission computed tomography (PSMA SPECT) diagnostic imaging technology is a cost-effective and viable alternative.

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.