Europe Nuclear Medicine Equipment Market

Market Size in USD Billion

USD

4.82 Billion

USD

9.61 Billion

2024

2032

USD

4.82 Billion

USD

9.61 Billion

2024

2032

| 2025 - 2032 | |

| USD 4.82 Billion | |

| USD 9.61 Billion | |

| % | |

|

Nuclear Medicine Equipment Market Size

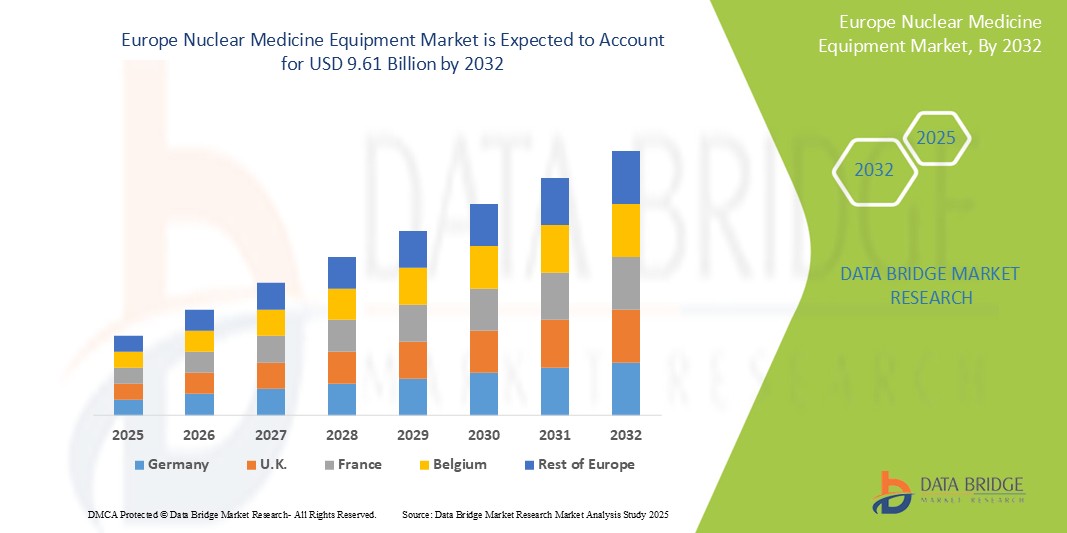

- The Europe Nuclear Medicine Equipment market size was valued at USD 4.82 billion in 2024 and is expected to reach USD 9.61 billion by 2032, at a CAGR of 9.0% during the forecast period

- The market growth is largely fueled by the increasing prevalence of chronic diseases such as cancer and cardiovascular ailments across Europe, coupled with a growing awareness about the importance of early diagnosis and personalized medicine.

- Furthermore, continuous technological advancements in nuclear imaging, including the development of hybrid imaging systems and more effective therapeutic isotopes, are driving market expansion. These converging factors are accelerating the adoption of nuclear medicine equipment, thereby significantly boosting the industry's growth.

Nuclear Medicine Equipment Market Analysis

- Nuclear Medicine Equipment market encompasses a range of specialized medical devices that utilize radioactive substances (radiopharmaceuticals) for both diagnostic imaging and therapeutic purposes. This includes equipment for Single Photon Emission Computed Tomography (SPECT), Positron Emission Tomography (PET), and planar scintigraphy systems. These technologies are crucial for diagnosing and treating a wide array of diseases, including various cancers, cardiovascular disorders, and neurological conditions, by providing unique insights at the cellular and molecular level.

- The escalating demand for nuclear medicine equipment is primarily fueled by the rising number of diagnostic nuclear medicine procedures, the expanding application of radiopharmaceuticals in both diagnosis and targeted therapies, and the increasing focus on precision medicine approaches.

- Germany dominates the Nuclear Medicine Equipment market in Europe with the largest revenue share of 28.5% in 2025, supported by its advanced healthcare infrastructure, strong investment in diagnostic imaging, and the presence of leading radiopharmaceutical and imaging equipment manufacturers. The country’s focus on early cancer detection, cardiac diagnostics, and neurological imaging has driven significant adoption of SPECT and PET systems across hospitals and academic centers.

- Germany is also expected to be the fastest-growing country in the Europe Nuclear Medicine Equipment market during the forecast period, driven by the rapid integration of hybrid imaging technologies (PET/CT, SPECT/CT), government-supported cancer screening programs, and increased funding for molecular imaging research. Moreover, the country’s expanding geriatric population and growing demand for precision diagnostics further contribute to market acceleration.

- SPECT (Single Photon Emission Computed Tomography) systems are expected to dominate the Europe Nuclear Medicine Equipment market with a market share of 41.3% in 2025, owing to their widespread availability, cost-effectiveness compared to PET, and broad application in cardiac, bone, and thyroid imaging. Continuous enhancements in detector technology and integration with CT for hybrid imaging support their ongoing clinical utility in hospitals and imaging centers throughout the region.

Report Scope and Nuclear Medicine Equipment Market Segmentation

|

Attributes |

Nuclear Medicine Equipment Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Europe

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Nuclear Medicine Equipment Market Trends

“Development of hybrid PET/CT and SPECT/CT systems”

- Technological Advancements in Imaging and Theranostics: A significant and accelerating trend in the Europe nuclear medicine equipment market is the continuous technological advancement in imaging modalities and the growing emphasis on theranostics (therapy + diagnostics). This evolution is significantly enhancing diagnostic precision, treatment efficacy, and personalized patient care.

- For instance, innovations include improved PET and SPECT imaging systems, such as hybrid PET/CT and SPECT/CT, which combine functional and anatomical information for more comprehensive diagnoses. New generation total-body PET scanners are being introduced, offering novel methods for studying diseases that affect the entire body with exceptional time and spatial resolution.

- The development and increased use of novel radionuclides are expanding the range of diagnostic and therapeutic applications. Theranostics, which uses diagnostic imaging to identify target receptors on cancer cells followed by targeted radiation treatment, is gaining significant traction in oncology.

- The integration of artificial intelligence (AI) into molecular imaging workflows is enhancing clinical workflows, from image acquisition and analysis to reporting and biomedical research. AI-driven reconstruction algorithms are demonstrating the ability to cut scan times while preserving diagnostic image quality.

- This trend towards more integrated, precise, and personalized nuclear medicine solutions is fundamentally reshaping diagnostic and therapeutic approaches in Europe. Consequently, companies are investing heavily in R&D to develop next-generation equipment and radiopharmaceuticals that support these advancements.

Nuclear Medicine Equipment Market Dynamics

Driver

“Increasing incidence of cancer”

- Rising Prevalence of Cancer and Cardiovascular Diseases: The increasing incidence of chronic diseases, particularly cancer and cardiovascular diseases (CVDs), across Europe is a major driver for the growth of the nuclear medicine equipment market

- For instance, cancer remains a leading cause of mortality globally, and cardiovascular diseases affect millions across Europe, necessitating a high volume of diagnostic and therapeutic interventions. Nuclear medicine plays a crucial role in the early detection, staging, and monitoring of these diseases, as well as in guiding targeted therapies

- The increasing geriatric population in Europe is more susceptible to these age-related conditions, further accelerating the demand for nuclear medicine procedures.

- Furthermore, government funding and initiatives, such as the European Union's Beating Cancer Plan, are providing substantial financial support for the development and adoption of nuclear medicine technologies.

- The non-invasive nature of nuclear medicine procedures and their ability to provide information at the cellular and molecular level offer a significant advantage over other imaging procedures, driving product demand

Restraint/Challenge

“High cost of equipment and radiopharmaceuticals”

- High Costs and Regulatory Hurdles: The substantial costs associated with nuclear medicine imaging equipment and radiopharmaceuticals, coupled with stringent regulatory guidelines for the approval and use of radioactive materials, present significant challenges to widespread market adoption.

- For instance, advanced PET and SPECT systems require significant capital investment, which can be a deterrent for smaller healthcare facilities or those with budget constraints. The short half-life of many radiopharmaceuticals also necessitates just-in-time delivery and complex logistics, adding to operational costs.

- Strict regulatory frameworks for the approval and use of radioactive materials and radiopharmaceuticals can pose challenges to market expansion, leading to lengthy approval processes and high compliance costs.

- Additionally, a shortage of skilled nuclear medicine technologists and physicians, along with a lack of comprehensive reimbursement for all nuclear medicine procedures, can hinder market growth. Concerns regarding the scarcity of evidence to prove that some nuclear medicine procedures will significantly improve patient outcomes also exist

Nuclear Medicine Equipment Market Scope

The market is segmented on the basis product, application and end user.

- By Product

On the basis of Product, the Nuclear Medicine Equipment Market is segmented into SPECT, Hybrid PET, and Planar Scintigraphy. The SPECT (Single Photon Emission Computed Tomography) segment is expected to dominate the market with the largest revenue share of 41.3% in 2025, due to its widespread use in diagnosing cardiovascular, skeletal, and thyroid conditions. SPECT systems are cost-effective, widely available across European hospitals, and increasingly integrated with CT to enhance imaging precision. Their established clinical value and reimbursement support in several European countries further drive their market leadership.

The Hybrid PET (Positron Emission Tomography) segment is anticipated to witness the fastest growth rate of 4.8% from 2025 to 2032, fueled by its high sensitivity in oncology and neurology imaging. Hybrid PET/CT and emerging PET/MRI systems provide functional and anatomical data in a single scan, improving diagnostic accuracy and patient management. Increasing investment in precision medicine, particularly in Germany, France, and the UK, is boosting demand for PET technologies across tertiary care institutions.

- By Application

On the basis of application, the Nuclear Medicine Equipment market is segmented into Oncology, Cardiology, Neurology, and General Imaging. The Oncology held the largest market revenue share in 2025 owing to the rising incidence of cancer across Europe and the critical role of nuclear medicine imaging in tumor detection, staging, and therapy monitoring. Hybrid PET/CT systems are especially prevalent in oncology centers for evaluating metabolic activity and treatment response.

The Neurology is expected to witness the fastest CAGR from 2025 to 2032, driven by the increasing prevalence of neurodegenerative disorders such as Alzheimer’s and Parkinson’s disease. Nuclear medicine imaging techniques like SPECT and PET are valuable in assessing cerebral blood flow and amyloid plaque buildup, supporting early diagnosis and disease progression tracking.

- By End users

On the basis of end users, the Nuclear Medicine Equipment market is segmented into Hospitals, Imaging Centers, and Others. The Hospitals segment accounted for the largest market revenue share in 2024, due to the high patient footfall, availability of multidisciplinary diagnostic infrastructure, and growing deployment of nuclear imaging modalities for in-house diagnostics. Public hospitals in countries like Germany, France, and Italy benefit from strong government healthcare funding, enabling regular upgrades to nuclear medicine systems.

The Imaging Centers segment is expected to witness the fastest CAGR from 2025 to 2032, as standalone diagnostic facilities increasingly invest in hybrid imaging systems to cater to outpatient demand. These centers offer flexible scheduling, reduced patient wait times, and high-quality imaging—making them attractive alternatives to hospital-based imaging departments. This trend is particularly strong in the UK, Spain, and Scandinavian countries where private diagnostics networks are expanding.

Nuclear Medicine Equipment Market Regional Analysis

- Germany dominates the Europe Nuclear Medicine Equipment market, holding the largest revenue share of 28.5% in 2025, primarily due to its robust healthcare infrastructure, strong public health spending, and early adoption of hybrid imaging technologies such as PET/CT and SPECT/CT. The country is a regional hub for radiopharmaceutical production and advanced molecular imaging research, making it a key player in the European nuclear medicine landscape.

- Germany’s leadership is further reinforced by large-scale investments in oncology and neurology diagnostics, backed by both public and private health institutions. The presence of global and domestic imaging equipment manufacturers, including Siemens Healthineers and Eckert & Ziegler, facilitates access to cutting-edge nuclear medicine systems and supports domestic manufacturing capabilities.

- The country also benefits from an extensive network of university hospitals and academic research institutions engaged in nuclear medicine innovation. These entities actively collaborate with equipment manufacturers to support clinical trials and optimize next-generation imaging solutions.

France Nuclear Medicine Equipment Market Insight

The France Nuclear Medicine Equipment market is projected to grow at a significant CAGR during the forecast period, supported by increasing cancer screening rates, growing awareness of early neurological disorder detection, and national initiatives for healthcare technology modernization. France has made strategic investments in digital health and hybrid imaging infrastructure, including the deployment of advanced PET scanners across regional cancer centers. The country’s radiopharmaceutical production capabilities and regulatory support from ANSM (Agence Nationale de Sécurité du Médicament) help ensure widespread access to diagnostic isotopes and imaging services. Furthermore, France is participating in multiple EU-funded initiatives aimed at enhancing nuclear imaging research and training skilled personnel, which bolsters long-term market development.

U.K. Nuclear Medicine Equipment Market Insight

The U.K. Nuclear Medicine Equipment market is poised for robust growth, driven by the NHS’s focus on diagnostic capacity building, cancer pathway improvements, and investment in PET/CT and SPECT systems across public hospitals. Despite Brexit-related regulatory changes, the UK remains aligned with international imaging standards and continues to import and deploy advanced nuclear medicine technologies. Increasing incidences of cancer, Alzheimer’s, and cardiovascular diseases are placing higher demands on non-invasive, functional imaging. The growing preference for outpatient diagnostic imaging and the expansion of private imaging centers are further supporting market penetration of hybrid nuclear imaging equipment. Organizations like the British Nuclear Medicine Society (BNMS) are playing a key role in establishing clinical protocols and promoting cross-border collaborations with European and global research institutions, fostering innovation and knowledge exchange in the nuclear medicine space.

Nuclear Medicine Equipment Market Share

The Nuclear Medicine Equipment industry is primarily led by well-established companies, including:

- Siemens Healthineers AG (Germany)

- GE Healthcare (U.K.)

- Koninklijke Philips N.V. (Netherlands)

- Bracco Imaging SpA (Italy)

- Cardinal Health Inc. (U.S.)

- Curium Pharma (France)

- Advanced Accelerator Applications (Novartis AG) (France)

- Merck KGaA (Germany)

- Mediso Medical Imaging Systems, Ltd. (Hungary)

- DDD-Diagnostics A/S (Denmark)

- surgicEye GmbH (Germany)

- Canon Medical Systems Corporation (Japan)

- Nordion Inc. (Canada)

Latest Developments in Europe Nuclear Medicine Equipment Market

- In October 2024, United Imaging launched its next-generation PET/CT systems, the uMI Panvivo and the uMI Panorama GS, and showcased the uMI AI Solution at the European Association of Nuclear Medicine (EANM) 2024 Congress, reinforcing its commitment to advancing molecular imaging in Europe.

- In May 2022, Turku PET Centre, Finland, introduced a new total-body Positron Emission Tomography (PET) scanner, a new generation of medical imaging devices, offering novel methods for studying diseases that affect the entire body.

- In June 2021, EU industry bodies Foratom and Nuclear Medicine Europe sought more support for nuclear medicine, emphasizing the need to maintain medical radioisotope supply, promote new research reactor capacity, and reconsider reimbursement systems.

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.