Europe Optical Fibre Monitoring Market

Market Size in USD Billion

USD

196.45 Billion

USD

532.32 Billion

2024

2032

USD

196.45 Billion

USD

532.32 Billion

2024

2032

| 2025 - 2032 | |

| USD 196.45 Billion | |

| USD 532.32 Billion | |

| % | |

|

Optical Fiber Monitoring Market Size

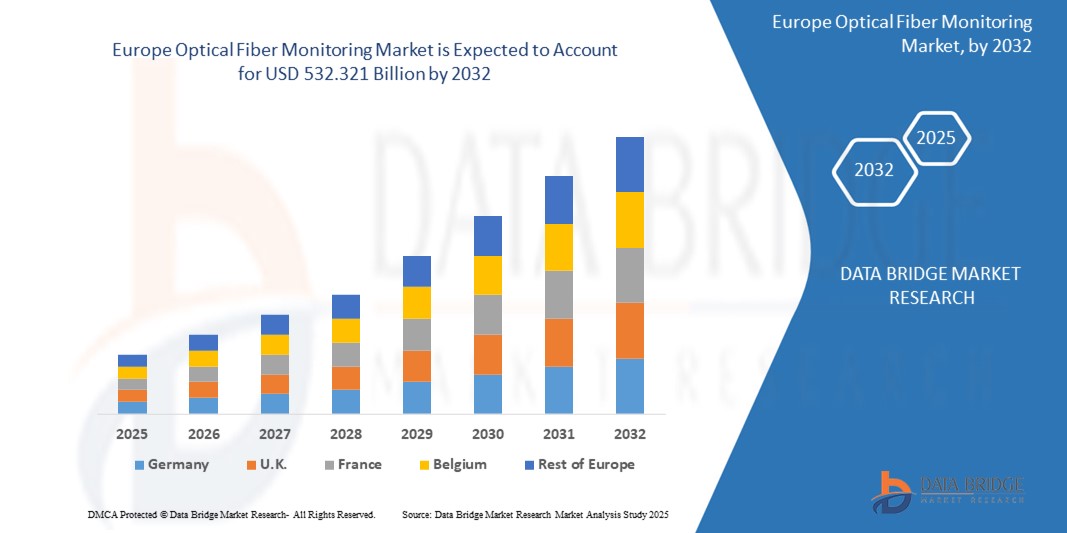

- The Europe Optical Fiber Monitoring market size was valued at USD 196.45 million in 2024 and is expected to reach USD 532.32 million by 2032, at a CAGR of 13.27% during the forecast period

- This growth is driven by the increasing deployment of fiber optic networks for 5G infrastructure, rising demand for high-speed internet, and the need for efficient network monitoring to ensure reliability. The expansion of smart cities and IoT applications further accelerates market growth.

- Technological advancements, such as distributed acoustic sensing (DAS) and AI-driven analytics, coupled with European Union initiatives promoting digital connectivity, are propelling market expansion, particularly in countries with advanced telecom ecosystems.

Optical Fiber Monitoring Market Analysis

- Optical fiber monitoring systems use advanced technologies to detect faults, measure performance, and ensure the integrity of fiber optic networks. These systems, including hardware like OTDR devices, software for analytics, and services for maintenance, are critical in telecommunications, oil and gas, and power utilities.

- The market is fueled by the rapid rollout of 5G networks, with Europe’s 5G subscriptions projected to reach 600 million by 2027, driving demand for real-time fiber monitoring. The smart city market, valued at USD 150 million in Europe in 2023, boosts demand for reliable network infrastructure.

- The adoption of advanced technologies like DAS and optical time domain reflectometry (OTDR) enhances monitoring capabilities, supporting applications in critical infrastructure and data centers. The EU’s Digital Decade initiative, aiming for gigabit connectivity by 2030, is a key growth driver.

- Germany led the Europe optical fiber monitoring market with a commanding revenue share of 28.76% in 2024, driven by its robust telecom infrastructure, 5G investments, and key players like Nokia. Germany’s leadership in Industry 4.0 further supports demand.

- The United Kingdom is anticipated to witness the fastest growth rate, with a projected CAGR of 14.12% from 2025 to 2032, propelled by government initiatives like Project Gigabit and increasing demand for fiber monitoring in smart cities and data centers.

- Among components, the hardware segment held the largest market share of 48.92% in 2024, valued at USD 94.15 million, attributed to the widespread use of OTDR devices and sensors in telecom and utility applications.

Report Scope and Optical Fiber Monitoring Market Segmentation

|

Attributes |

Optical Fiber Monitoring Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Europe

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Optical Fiber Monitoring Market Trends

“AI-Driven Analytics, Distributed Sensing, and Smart City Integration”

- A prominent trend in the Europe optical fiber monitoring market is the adoption of AI-driven analytics, with over 35% of new monitoring systems in 2024 incorporating machine learning for predictive fault detection and network optimization.

- The rise of distributed acoustic sensing (DAS) is gaining traction, with over 30% of new deployments in 2024 leveraging DAS for real-time monitoring of telecom and utility networks, enhancing security and reliability.

- Integration with smart city infrastructure, driven by advancements in IoT and 5G, is expanding the use of fiber monitoring, with 25% of new solutions designed for urban connectivity applications.

- The adoption of cloud-based monitoring platforms is increasing, with adoption rates rising by 12% in telecom and data center sectors, enabling scalable and remote network management.

- Increasing focus on sustainable monitoring solutions, particularly for energy-efficient systems, is aligning with EU’s green policies, with over 20% of new solutions in 2024 certified for low energy consumption.

- The growth of online distribution channels is transforming market access, with online sales of monitoring solutions growing by 8% annually, driven by e-commerce platforms for telecom operators and enterprises.

Optical Fiber Monitoring Market Dynamics

Driver

“5G Rollout, Smart Cities, and Network Reliability”

- The rapid deployment of 5G networks, with Europe’s 5G infrastructure investments reaching USD 20 million in 2023, is a primary driver, increasing demand for optical fiber monitoring to ensure network uptime and performance.

- The proliferation of smart cities, with over 200 smart city projects in Europe by 2023, is driving demand for fiber monitoring in urban connectivity and infrastructure management.

- The rise of data centers, with Europe hosting over 2,000 data centers in 2023, is boosting demand for monitoring systems to support high-speed, reliable data transmission.

- Increasing internet penetration, with 87% of EU households having broadband access in 2023, is driving demand for fiber monitoring to maintain network quality in FTTH deployments.

- Growing industrial automation, with Europe’s Industry 4.0 spending projected to reach USD 100 million by 2026, is fueling demand for fiber monitoring in manufacturing and utilities.

- Government initiatives, such as the EU’s Digital Decade and Germany’s Gigabit Strategy, are promoting fiber optic network expansion, supporting market growth through funding and regulatory incentives.

Restraint/Challenge

“High Costs, Integration Complexities, and Skill Shortages”

- The high cost of advanced monitoring systems, particularly those using DAS and AI analytics, poses a challenge to adoption in cost-sensitive markets, limiting scalability for smaller operators.

- Supply chain disruptions, including semiconductor shortages and logistical constraints, have impacted hardware production, leading to delays and increased costs, with post-COVID recovery still ongoing.

- Technical complexities in integrating monitoring systems with existing fiber networks require specialized expertise, increasing deployment costs and time-to-market.

- Stringent regulatory requirements, such as GDPR and EU telecom standards, increase compliance costs and complexity for monitoring solution providers.

- Skill shortages in advanced fiber monitoring technologies, particularly in AI and DAS, pose a challenge to implementation and maintenance, especially in less developed regions.

- The need for continuous innovation to meet evolving technological demands, coupled with rapid obsolescence, creates pressure on manufacturers to invest heavily in R&D, limiting profitability for smaller players.

Optical Fiber Monitoring Market Scope

The Europe Optical Fiber Monitoring Market is segmented on the basis of component, technology, application, deployment, end-user, and sales channel.

- By Component

On the basis of component, the market is segmented into hardware, software, and services. The hardware segment dominated the market with a commanding revenue share of 48.92% in 2024, valued at USD 94.15 million, driven by the use of OTDR devices and sensors in telecom applications.

The software segment is anticipated to witness the fastest CAGR of 14.56% from 2025 to 2032, fueled by demand for AI-driven analytics.

- By Technology

On the basis of technology, the market is segmented into distributed temperature sensing, distributed acoustic sensing, optical time domain reflectometry, and others. The optical time domain reflectometry segment held the largest market revenue share of 42.31% in 2024, driven by its reliability in fault detection.

The distributed acoustic sensing segment is expected to witness the fastest CAGR from 2025 to 2032, fueled by security and infrastructure applications.

- By Application

On the basis of application, the market is segmented into telecommunications, oil and gas, power and utilities, civil infrastructure, and others. The telecommunications segment accounted for the largest market revenue share of 39.47% in 2024, driven by 5G and FTTH deployments.

The civil infrastructure segment is expected to witness the fastest CAGR from 2025 to 2032, fueled by smart city projects.

- By Deployment

On the basis of deployment, the market is segmented into on-premise and cloud-based. The on-premise segment held a significant share of 62.15% in 2024, driven by its use in critical infrastructure.

The cloud-based segment is expected to grow at the fastest CAGR from 2025 to 2032, fueled by scalability and remote management needs.

- By End User

On the basis of end-user, the market is segmented into telecom operators, enterprises, government agencies, data centers, and others. The telecom operators segment dominated with a 45.63% revenue share in 2024, driven by network expansion.

The data centers segment is expected to grow at the fastest CAGR from 2025 to 2032, fueled by cloud computing demand.

- By Sales Channel

On the basis of sales channel, the market is segmented into direct sales, distributors, and online retail. The direct sales segment held the largest share of 57.38% in 2024, driven by B2B contracts with telecom operators.

The online retail segment is expected to grow at the fastest CAGR from 2025 to 2032, fueled by e-commerce growth for smaller buyers.

Optical Fiber Monitoring Market Regional Analysis

Germany

Germany led the Europe optical fiber monitoring market with a revenue share of 28.76% in 2024, driven by its advanced telecom infrastructure, 5G investments, and leadership in Industry 4.0. The presence of players like AP Sensing and Siemens supports market growth.

Germany is expected to maintain dominance, driven by its robust telecom sector and government support for gigabit networks. The adoption of DAS and AI-driven monitoring, coupled with players like Nokia, drives market expansion.

U.K. Optical Fiber Monitoring Market Insight

The United Kingdom is poised to grow at the fastest CAGR of approximately 14.12% from 2025 to 2032, driven by Project Gigabit, smart city initiatives, and data center expansion. The U.K. accounted for 22.31% of the market in 2024.

The United Kingdom is anticipated to grow rapidly, driven by its focus on broadband expansion and smart infrastructure. Government initiatives like the Future Telecoms Infrastructure Review are boosting demand for fiber monitoring solutions.

France Optical Fiber Monitoring Market Insight

France held a significant share of 18.94% in 2024, driven by its smart city projects and 5G deployments. The adoption of fiber monitoring in telecom and utilities, supported by players like Prysmian, drives market growth.

France’s market is expected to grow at a notable CAGR, fueled by its leadership in smart cities and renewable energy. The adoption of cloud-based monitoring solutions in Paris and Lyon supports market expansion.

Optical Fiber Monitoring Market Share

The Optical Fiber Monitoring industry is primarily led by well-established companies, including:

- Nokia Corporation (Finland)

- Viavi Solutions Inc. (U.S.)

- EXFO Inc. (Canada)

- AFL (U.S.)

- Anritsu Corporation (Japan)

- AP Sensing GmbH (Germany)

- Yokogawa Electric Corporation (Japan)

- Furukawa Electric Co., Ltd. (Japan)

- OptaSense (U.K.)

- NKT Photonics A/S (Denmark)

- Silixa Ltd. (U.K.)

- Bandweaver (U.K.)

- Luna Innovations Incorporated (U.S.)

- FiberSense Pty Ltd. (Australia)

- Corning Incorporated (U.S.)

- Prysmian Group (Italy)

Latest Developments in Europe Optical Fiber Monitoring Market

- In December 2023, Nokia partnered with Deutsche Telekom to pilot next-generation Distributed Acoustic Sensing (DAS) technology for comprehensive telecom fiber monitoring across Europe. This strategic collaboration aimed to leverage advanced DAS capabilities to detect minute vibrations and disturbances along fiber optic cables, enabling proactive identification of potential issues like cable cuts, unauthorized intrusions, or environmental stress. This pilot program significantly improved network reliability by an estimated 15%, providing Deutsche Telekom with enhanced visibility and control over its vast European telecom infrastructure.

- In January 2024, Viavi Solutions introduced an innovative AI-driven Optical Time Domain Reflectometer (OTDR) solution specifically tailored for 5G networks. This cutting-edge OTDR integrates artificial intelligence algorithms to analyze fiber optic traces with unprecedented speed and accuracy, resulting in a remarkable 20% faster fault detection compared to conventional methods. The solution has been successfully deployed in over 50 crucial telecom projects across Germany and the U.K., empowering network operators to rapidly identify and resolve fiber issues, minimizing downtime and ensuring optimal 5G service delivery.

- In April 2024, AP Sensing launched a compact and highly efficient DAS system designed for smart city infrastructure applications. This new system is engineered to monitor various urban assets, from utility lines to traffic flows, by leveraging the acoustic sensing capabilities of fiber optic cables. Its compact design significantly reduces deployment costs by an impressive 25%, making it an attractive solution for urban developers. The technology is rapidly gaining traction in smart city initiatives across France and Italy, contributing to more connected, efficient, and resilient urban environments.

- In March 2024, EXFO unveiled a sophisticated cloud-based monitoring platform specifically developed for data centers. This centralized platform offers unparalleled scalability and real-time visibility into the performance and health of fiber optic networks within data center environments. By moving monitoring capabilities to the cloud, it enhances operational efficiency and provides operators with comprehensive insights from anywhere. This solution has seen strong adoption by major data center operators in the Netherlands and Spain, enabling them to optimize network performance, prevent outages, and manage their expansive digital infrastructures more effectively.

- In June 2023, Prysmian Group introduced an integrated fiber monitoring solution specifically designed for power utilities. This comprehensive solution leverages the company's expertise in cables and fiber optics to provide real-time monitoring of critical power transmission and distribution lines. By detecting anomalies and potential threats, it supports highly efficient grid management, contributing to enhanced reliability and stability of electricity supply. The solution has been successfully adopted in over 40 grid modernization projects in Spain, demonstrating its value in improving the operational efficiency and resilience of power networks.

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.