Europe Primary Angle Closure Glaucoma Market

Market Size in USD Million

USD

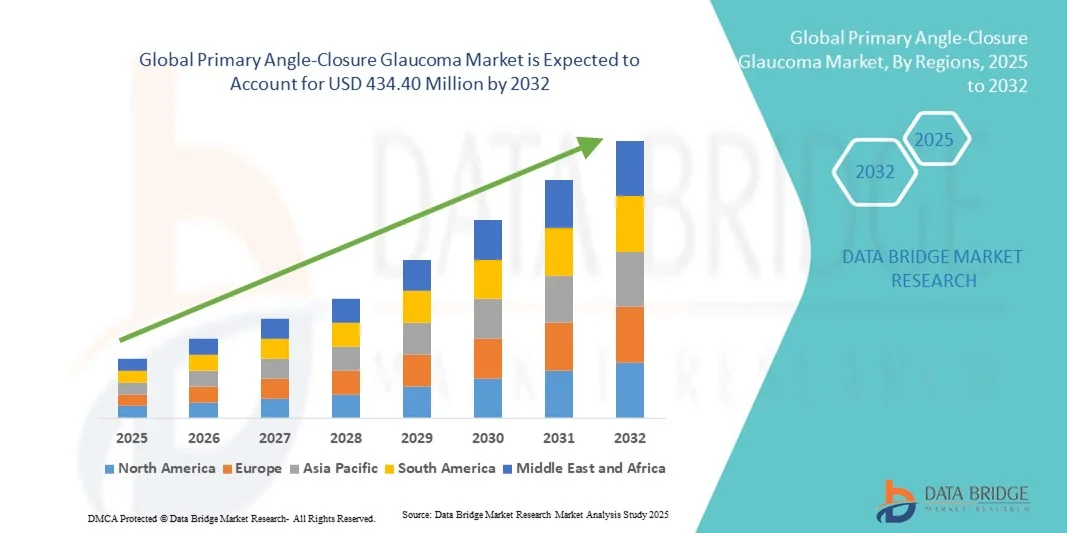

270.05 Million

USD

433.67 Million

2024

2032

USD

270.05 Million

USD

433.67 Million

2024

2032

| 2025 - 2032 | |

| USD 270.05 Million | |

| USD 433.67 Million | |

| % | |

|

Primary Angle-Closure Glaucoma Market Size

- The Europe primary angle-closure glaucoma market size was valued at USD 270.05 Million in 2024 and is expected to reach USD 433.67 Million by 2032, at a CAGR of 6.10% during the forecast period

- The market growth is largely fueled by the increasing prevalence of primary angle-closure glaucoma (PACG), rising geriatric populations, and advancements in diagnostic and imaging technologies that enable early detection and intervention

- Furthermore, growing awareness among patients and healthcare providers, coupled with the development of minimally invasive surgical procedures and innovative pharmacological treatments, is accelerating the adoption of primary angle-closure glaucoma solutions, thereby significantly boosting the market’s growth

Primary Angle-Closure Glaucoma Market Analysis

- Primary Angle-Closure Glaucoma solutions, aimed at preventing vision loss and managing intraocular pressure, are becoming increasingly vital in modern ophthalmology due to the rising prevalence of the condition and the growing geriatric population

- The escalating demand for effective diagnostic and treatment options is primarily fueled by advancements in laser surgery, pharmacological therapies, and increasing awareness among healthcare providers and patients, which are collectively driving the market’s growth

- The U.K. dominated the primary angle-closure glaucoma market with the largest revenue share of 39.8% in 2024, driven by advanced healthcare infrastructure and widespread adoption of innovative therapies

- Germany is expected to be the fastest-growing region during the forecast period, owing to increasing geriatric population, rising awareness of early diagnosis, and growing adoption of advanced laser and surgical interventions for PACG

- The Diagnosis segment held the largest market revenue share of 52.8% in 2024, driven by the high demand for diagnostic procedures such as tonometry, gonioscopy, and optical coherence tomography (OCT)

Report Scope and Primary Angle-Closure Glaucoma Market Segmentation

|

Attributes |

Primary Angle-Closure Glaucoma Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Europe

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Primary Angle-Closure Glaucoma Market Trends

Rising Adoption of Minimally Invasive Glaucoma Surgery (MIGS)

- A significant and accelerating trend in the global Primary Angle-Closure Glaucoma market is the growing adoption of minimally invasive glaucoma surgeries (MIGS) such as trabecular micro-bypass stents, gonioscopy-assisted transluminal trabeculotomy, and ab interno trabeculectomy. These procedures are increasingly preferred due to shorter recovery times, reduced complication rates, and effective intraocular pressure (IOP) control

- For instance, the iStent inject and Kahook Dual Blade procedures are being widely adopted in Asia-Pacific and North American markets, providing safer alternatives to traditional trabeculectomy for patients with early to moderate glaucoma

- Clinical studies demonstrate that MIGS procedures not only improve patient outcomes but also reduce the dependency on multiple ocular hypotensive medications, making long-term disease management more convenient

- Hospitals and specialty eye care centers are increasingly integrating MIGS techniques into their surgical protocols, while training programs for ophthalmologists are expanding to meet growing demand

- This trend toward minimally invasive procedures is transforming patient expectations, driving higher adoption rates, and influencing healthcare infrastructure investments in key markets

- The demand for MIGS is anticipated to continue growing rapidly during the forecast period, especially in regions with high glaucoma prevalence and advanced healthcare systems

Primary Angle-Closure Glaucoma Market Dynamics

Driver

Growing Need Due to Increasing Prevalence and Early Diagnosis

- The increasing prevalence of primary angle-closure glaucoma, coupled with rising awareness about early diagnosis and treatment options, is a significant driver for market growth

- For instance, in April 2024, key ophthalmology centers reported enhanced adoption of advanced diagnostic imaging, such as anterior segment optical coherence tomography (AS-OCT), facilitating early detection of angle-closure glaucoma. Such initiatives by healthcare providers are expected to drive the Primary Angle-Closure Glaucoma industry growth in the forecast period

- As patients become more aware of potential vision loss risks and seek timely interventions, advanced treatment options such as laser peripheral iridotomy (LPI) and minimally invasive glaucoma surgery (MIGS) offer effective disease management, providing a compelling alternative to conventional surgical approaches

- Furthermore, the growing availability of diagnostic devices and screening programs in clinics and hospitals is enabling early identification of at-risk populations, facilitating prompt treatment and reducing complications

- The convenience of outpatient procedures, improved post-operative outcomes, and integration of treatment protocols in standard ophthalmology practice are key factors propelling the adoption of primary angle-closure glaucoma management solutions across both developed and emerging markets. The trend towards preventive eye care and increasing patient education further contributes to market growth

Restraint/Challenge

Concerns Regarding Treatment Accessibility and High Costs

- Concerns surrounding the affordability and accessibility of advanced glaucoma treatments pose a significant challenge to broader market penetration. As procedures such as laser iridotomy, phacoemulsification, and MIGS require specialized equipment and trained ophthalmologists, they remain inaccessible in certain regions, raising anxieties about equitable care delivery

- For instance, limited availability of ophthalmic care infrastructure in rural or underdeveloped regions has made some patients hesitant to seek treatment, impacting timely intervention

- Addressing these accessibility concerns through expanded healthcare infrastructure, insurance coverage, and training programs for eye care professionals is crucial for building patient trust and improving treatment uptake

- In addition, the relatively high cost of some advanced glaucoma treatment procedures compared to standard medications can be a barrier for price-sensitive patients, particularly in developing regions or for those without adequate healthcare coverage

- While prices and procedural efficiency are gradually improving, the perceived premium for advanced glaucoma management can still hinder widespread adoption, especially among low-income population

- Overcoming these challenges through improved healthcare access, government-supported screening programs, and the development of cost-effective treatment alternatives will be vital for sustained market growth

Primary Angle-Closure Glaucoma Market Scope

The market is segmented on the basis of disease type, type, end user, and distribution channel.

- By Disease Type

On the basis of disease type, the Primary Angle-Closure Glaucoma market is segmented into Acute Angle-Closure Glaucoma and Chronic Angle-Closure Glaucoma. The Acute Angle-Closure Glaucoma segment dominated the largest market revenue share of 46.5% in 2024, driven by its sudden onset, higher risk of vision loss, and urgent need for medical intervention. Hospitals and specialty clinics prioritize rapid diagnosis and treatment to prevent permanent vision damage, which results in higher treatment volumes. This segment benefits from established clinical protocols, widespread awareness among ophthalmologists, and patient education programs promoting early detection. Increasing availability of advanced diagnostic tools and timely surgical interventions further reinforces market dominance. Government-supported eye screening programs and growing healthcare expenditure enhance accessibility and drive steady adoption. Emergency management cases contribute significantly to hospital revenues, strengthening the financial base of this segment.

The Chronic Angle-Closure Glaucoma segment is expected to witness the fastest CAGR of 23.1% from 2025 to 2032, fueled by the increasing prevalence of chronic cases due to aging populations, urban lifestyles, and comorbidities such as diabetes. Advancements in minimally invasive surgical options, laser therapies, and pharmacological management attract both patients and clinicians. Expansion of outpatient care facilities and ambulatory surgical centers facilitates long-term disease management. Rising awareness of preventive eye care and early interventions enhances the adoption of routine diagnostic and follow-up procedures. Increasing healthcare access in emerging regions, coupled with patient preference for specialized care centers, supports rapid market expansion.

- By Type

On the basis of type, the market is segmented into Diagnosis and Treatment. The Diagnosis segment held the largest market revenue share of 52.8% in 2024, driven by the high demand for diagnostic procedures such as tonometry, gonioscopy, and optical coherence tomography (OCT). Early detection is crucial for preserving vision, which ensures frequent patient visits and repeat testing. Hospitals and specialty clinics leverage advanced diagnostic equipment to improve accuracy and efficiency. Awareness campaigns and regular eye screening initiatives enhance market penetration. Institutional support for preventive care, combined with the rising number of ophthalmologists, drives sustained adoption. Availability of portable and non-invasive devices for community screenings contributes to higher revenue. Technological integration in electronic health records ensures accurate tracking and follow-up.

The Treatment segment is expected to witness the fastest CAGR of 21.4% from 2025 to 2032, fueled by rising adoption of surgical interventions, laser therapies, and pharmacological treatments. Growing patient preference for minimally invasive procedures, coupled with outpatient care expansion, drives market growth. Continuous innovation in surgical devices and glaucoma medications attracts hospitals and specialty clinics. Increased healthcare funding and insurance coverage further enhance access to treatments. Emerging markets are witnessing greater adoption due to improving infrastructure and awareness campaigns. The segment benefits from increased availability of skilled ophthalmic surgeons and advanced equipment in tertiary care centers. Patient demand for quality care and faster recovery options strengthens growth potential.

- By End User

On the basis of end user, the market is segmented into Hospitals, Specialty Clinics, Ambulatory Surgical Centers, and Others. The Hospitals segment accounted for the largest market revenue share of 49.2% in 2024, owing to advanced infrastructure, availability of trained ophthalmologists, and capability to handle both acute and chronic cases. Hospitals provide comprehensive diagnostic and treatment services, high patient throughput, and integration of latest technologies, which drives market dominance. Large-scale procurement and institutional funding support consistent supply of devices and treatments. Hospitals also benefit from government programs and insurance reimbursements. Continuous staff training, research activities, and patient monitoring enhance service quality and patient outcomes. Emergency care for acute glaucoma cases further strengthens revenue.

The Specialty Clinics segment is expected to witness the fastest CAGR of 22.7% from 2025 to 2032, driven by patient preference for personalized and outpatient care, increasing number of dedicated ophthalmology centers, and focus on minimally invasive procedures. Growing awareness of early diagnosis and preventive eye care boosts clinic visits. Specialty clinics offer targeted treatment packages, flexible scheduling, and enhanced patient interaction. Expansion in urban and semi-urban areas ensures better reach. Rising disposable income and insurance penetration support adoption. Technological advancements and telemedicine integration further accelerate growth.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into Direct Tender, Retail Sales, and Others. The Direct Tender segment dominated with 44% revenue share in 2024, benefiting from institutional procurement by hospitals and surgical centers, ensuring consistent supply of diagnostic and treatment devices. Centralized tendering ensures cost efficiency, quality compliance, and bulk availability. Direct procurement allows for integration with hospital treatment protocols and long-term maintenance agreements. Government and private institutions prefer direct tendering for predictable supply and contract reliability.

The Retail Sales segment is expected to witness the fastest CAGR of 20.8% from 2025 to 2032, driven by growing patient awareness, rising online and offline availability of ophthalmic devices, and adoption of home-monitoring tools. Convenience, accessibility, and increased disposable income facilitate market expansion. Retail channels support faster distribution, promotional campaigns, and patient education initiatives. In addition, partnerships between device manufacturers and retail chains are enhancing product visibility and reach. The segment also benefits from the rise of e-commerce platforms, enabling patients in remote areas to access advanced ophthalmic solutions efficiently.

Primary Angle-Closure Glaucoma Market Regional Analysis

- The Europe primary angle-closure glaucoma market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by increasing awareness of early diagnosis, growing adoption of advanced therapies, and the rising prevalence of ocular disorders across the region

- The healthcare infrastructure in Europe, particularly in countries such as the U.K. and Germany, is well-developed, supporting patient access to diagnostic tools and innovative treatments. Rising geriatric population and increasing focus on preventive eye care further contribute to market growth

- In addition, government initiatives and insurance coverage for ophthalmic care facilitate wider adoption of advanced interventions, including laser and surgical procedures. The demand for comprehensive eye care solutions, coupled with technological advancements in diagnostics and therapeutics, is significantly boosting the market

U.K. Primary Angle-Closure Glaucoma Market Insight

The U.K. primary angle-closure glaucoma market dominated Europe with the largest revenue share of 39.8% in 2024, driven by advanced healthcare infrastructure, high patient awareness, and widespread adoption of innovative therapies. The prevalence of PACG and growing preference for early diagnosis and specialized treatment approaches encourage both hospitals and specialty clinics to expand their offerings. Increased government support, access to advanced diagnostic tools, and a well-established network of ophthalmologists and surgical centers further strengthen the market. High adoption of laser and minimally invasive surgical interventions, combined with a strong focus on patient education, reinforces the U.K.’s leading position in the region.

Germany Primary Angle-Closure Glaucoma Market Insight

The Germany primary angle-closure glaucoma market is expected to be the fastest-growing region during the forecast period, fueled by an increasing geriatric population, rising awareness of early diagnosis, and growing adoption of advanced laser and surgical interventions for PACG. The country’s emphasis on technological innovation in healthcare and expanding availability of ophthalmic services enhance treatment accessibility. Patient preference for minimally invasive procedures, coupled with strong clinical expertise and advanced hospital infrastructure, supports market expansion. Moreover, rising healthcare expenditure and proactive government initiatives to improve eye care coverage are contributing to the rapid growth of the German PACG market.

Primary Angle-Closure Glaucoma Market Share

The Primary Angle-Closure Glaucoma industry is primarily led by well-established companies, including:

- Novartis AG (Switzerland)

- Alcon Inc. (Switzerland)

- Théa Pharmaceuticals (France)

- Bausch + Lomb (U.K.)

- Hoya Corporation (Japan)

- Glaukos Corporation (U.K.)

- Carl Zeiss Meditec AG (Germany)

- Ophthalmic Innovations Europe (Netherlands)

- IOLTech SAS (France)

- EpiTech Pharma (Germany)

- Topcon Europe Medical BV (Netherlands)

- Meda Pharma GmbH & Co. KG (Germany)

Latest Developments in Europe Primary Angle-Closure Glaucoma Market

- In April 2025, a study published in BMJ Open Ophthalmology evaluated the efficacy and safety of phacogoniotomy—a combined procedure of phacoemulsification, goniosynechialysis, and goniotomy—in treating advanced PACG with cataract over a two-year follow-up period. The findings suggest that phacogoniotomy may serve as a viable alternative to traditional trabeculectomy, offering significant intraocular pressure reduction and visual improvement for patients with advanced PACG

- In March 2025, research from King's College London, funded by the Mary Dell Hibbert Glaucoma Research Fund, introduced a novel approach to treating glaucoma by focusing on protecting retinal cells through anti-inflammatory strategies. This research, led by Dr. Richard Eva, aims to develop therapies that go beyond reducing intraocular pressure, potentially transforming patient care in glaucoma management

- In February 2025, a systematic review and meta-analysis published in Frontiers in Medicine examined recent advancements in glaucoma treatment, focusing on innovative medications and creative strategies. The review discusses emerging therapies that aim to lower intraocular pressure more effectively and with fewer side effects, reflecting the ongoing evolution in glaucoma management

- In January 2025, a study published in BMC Ophthalmology compared the outcomes of phacoemulsification combined with trabecular meshwork-Schlemm canal bypass surgery to traditional methods in treating PACG. The study found that the combined approach offered improved intraocular pressure control and visual outcomes, suggesting its potential as a preferred treatment option for PACG patients

- In December 2024, the Royal College of Ophthalmologists and the College of Optometrists in the UK published updated guidelines on the management and referral of primary angle closure. These guidelines aim to standardize care and improve early detection and treatment of PACG, emphasizing the importance of timely intervention to prevent vision loss

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.