Europe Prophylaxis Of Organ Rejection Market

Market Size in USD Million

USD

959.37 Million

USD

1,253.57 Million

2025

2033

USD

959.37 Million

USD

1,253.57 Million

2025

2033

| 2026 - 2033 | |

| USD 959.37 Million | |

| USD 1,253.57 Million | |

| % | |

|

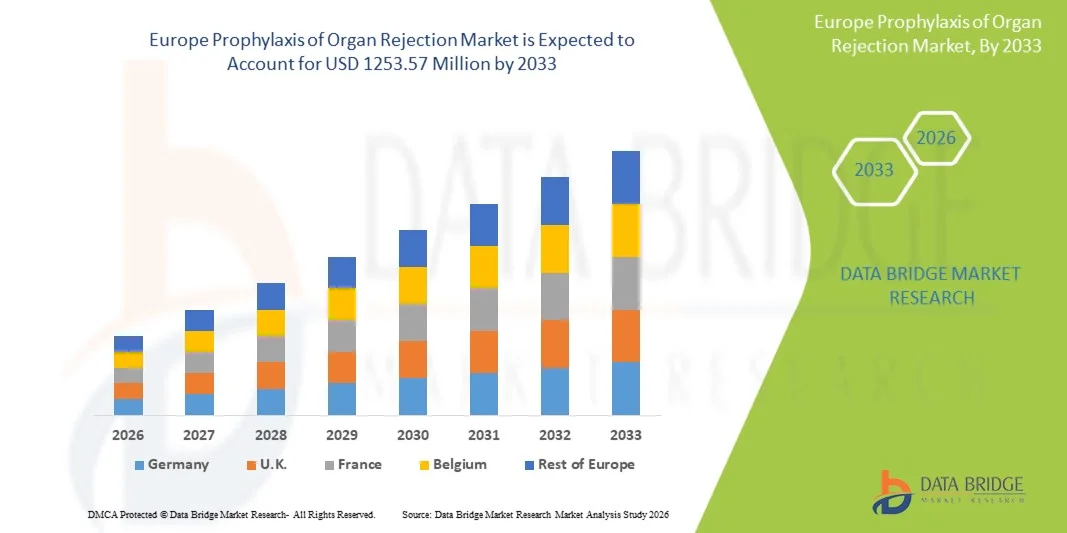

Europe Prophylaxis of Organ Rejection Market Size

- The Europe Prophylaxis of Organ Rejection Market size was valued at USD 959.37 Million in 2025and is expected to reach USD 1253.57 Million by 2033, at a CAGR of3.40% during the forecast period

- The market growth is largely fueled by the increasing number of organ transplant procedures worldwide, rising prevalence of end-stage organ failure, and continuous advancements in immunosuppressive therapies, leading to improved graft survival and long-term transplant outcomes across hospitals and specialty transplant centers

- Furthermore, growing demand for effective post-transplant care, increasing focus on reducing graft rejection risks, and expanding access to personalized immunosuppressive treatment protocols are establishing Prophylaxis of Organ Rejection solutions as an essential component of modern transplant medicine. These converging factors are accelerating the uptake of Prophylaxis of Organ Rejection solutions, thereby significantly boosting the industry's growth

Europe Prophylaxis of Organ Rejection Market Analysis

- Prophylaxis of Organ Rejection therapies, including calcineurin inhibitors, mTOR inhibitors, corticosteroids, antiproliferative agents, and biologic induction therapies, are increasingly vital components of modern transplant medicine due to their role in preventing graft rejection, improving organ survival, and supporting long-term patient outcomes across kidney, liver, heart, and lung transplant procedures

- The escalating demand for Prophylaxis of Organ Rejection therapies is primarily fueled by the rising number of organ transplant procedures, increasing prevalence of chronic kidney and liver diseases, expanding transplant waiting lists, and continuous advancements in personalized immunosuppressive treatment regimens

- K. dominated the Europe Prophylaxis of Organ Rejection Market in Europe with the largest revenue share of approximately 32.9% in 2025, characterized by advanced transplant care infrastructure, high healthcare expenditure, increasing transplant procedure volumes, and strong adoption of advanced immunosuppressive therapies across major hospitals and specialty centers

- Germany is expected to be the fastest-growing market in the prophylaxis of organ rejection sector during the forecast period, projected to register a CAGR of approximately 8.7%, due to improving transplant healthcare infrastructure, increasing awareness regarding organ donation, rising number of kidney and liver transplant procedures, expanding access to specialty care, and growing demand for advanced and personalized immunosuppressive treatment approaches

- The adults segment dominated the largest market revenue share of 81.6% in 2025, driven by the higher number of adult transplant procedures globally

Report Scope and Europe Prophylaxis of Organ Rejection Market Segmentation

|

Attributes |

Prophylaxis of Organ Rejection Key Market Insights |

|

Segments Covered |

· By Cause: Epidemiologic Exposure, Antibacterial Prophylaxis, Prophylaxis Against Other Pathogens, and Others · By Treatment: Outpatient Immunosuppressant, Inpatient Immunosuppressant, and Others · By Route of Administration: Oral and Intravenous · By Organ: Kidney, Liver, Heart, Lung, and Others · By Patient Type: Paediatric and Adults · By End User: Hospitals, Clinic, Home Healthcare, and Others · By Distribution Channel: Direct Tender, Pharmacy Stores, and Others |

|

Countries Covered |

Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Europe |

|

Key Market Players |

· Astellas Pharma Inc. (Japan) · Novartis AG (Switzerland) · F. Hoffmann-La Roche Ltd. (Switzerland) · Pfizer Inc. (U.S.) · Sanofi S.A. (France) · Bristol-Myers Squibb Company (U.S.) · AbbVie Inc. (U.S.) · Teva Pharmaceutical Industries Ltd. (Israel) · Dr. Reddy’s Laboratories Ltd. (India) · Sun Pharmaceutical Industries Ltd. (India) · Viatris Inc. (U.S.) · Johnson & Johnson (U.S.) · Merck & Co., Inc. (U.S.) · GlaxoSmithKline plc (U.K.) · Biocon Biologics Ltd. (India) · Sandoz International GmbH (Switzerland) · Chugai Pharmaceutical Co., Ltd. (Japan) · Takeda Pharmaceutical Company Limited (Japan) · Lupin Limited (India) · Cipla Limited (India) |

|

Market Opportunities |

· Growing demand for personalized immunosuppressive therapies · Rising Demand in Emerging Markets |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Europe Prophylaxis of Organ Rejection Market Trends

“Rising Organ Transplant Procedures and Advancements in Immunosuppressive Therapies”

- A significant and accelerating trend in the Europe Prophylaxis of Organ Rejection Market is the steady rise in organ transplant procedures, including kidney, liver, heart, and lung transplants, which is increasing the demand for effective rejection-prevention therapies. Growing healthcare investments and expanding transplant infrastructure across countries such as China, India, Japan, South Korea, and Australia are supporting market growth

- For instance, leading immunosuppressive drugs such as tacrolimus, mycophenolate mofetil, cyclosporine, and everolimus are widely prescribed as part of post-transplant maintenance therapy to reduce the risk of graft rejection and improve long-term survival outcomes. These therapies remain essential in kidney and liver transplant programs across major Europe healthcare centers

- Continuous advancements in immunosuppressive treatment regimens are improving efficacy while reducing adverse effects such as nephrotoxicity, infection risk, and metabolic complications. The adoption of combination therapy approaches and individualized dosing strategies is helping physicians optimize patient outcomes after transplantation

- Increasing awareness regarding organ donation, improving surgical expertise, and supportive government initiatives to strengthen transplant networks are further expanding the eligible patient pool requiring prophylaxis of organ rejection therapies. Several countries in the region are modernizing transplant regulations and donor registries to address organ shortages

- The trend toward precision medicine is also reshaping the market, with healthcare providers increasingly using therapeutic drug monitoring and biomarker-based assessment to personalize immunosuppressive therapy. This approach improves graft preservation while minimizing unnecessary exposure to high-dose medications

- Demand for safer, more effective, and long-term transplant management therapies is rising rapidly across the Europe region as survival rates improve and more patients require lifelong immunosuppressive care

Europe Prophylaxis of Organ Rejection Market Dynamics

Driver

“Growing Need Due to Increasing Transplant Volume and Better Access to Specialized Care”

- The increasing number of organ transplant surgeries across Asia-Pacific, combined with broader access to tertiary care hospitals and transplant specialists, is a major driver for the Europe Prophylaxis of Organ Rejection Market

- For instance, countries such as India and China have reported continued expansion in kidney and liver transplant programs, while Japan and South Korea are investing in advanced transplant centers and postoperative care systems. These developments are expected to drive demand for rejection-prevention therapies during the forecast period

- As survival rates after transplantation continue to improve, patients require long-term immunosuppressive therapy, creating sustained demand for branded and generic prophylactic drugs. Regular follow-up care and monitoring further support recurring market revenues

- In addition, increasing incidence of chronic kidney disease, liver failure, cardiovascular disorders, and diabetes-related complications is expanding the number of patients eligible for transplantation, thereby increasing the future need for organ rejection prophylaxis

- Favorable reimbursement policies in developed Europe economies and improving healthcare coverage in emerging markets are also contributing to wider treatment adoption

Restraint/Challenge

“High Treatment Costs, Side Effects, and Risk of Infection”

- The high cost of long-term immunosuppressive therapy remains a significant challenge, particularly in low- and middle-income Europe countries where out-of-pocket healthcare spending is still substantial. Lifelong treatment can create affordability concerns for many transplant recipients

- For instance, premium immunosuppressive agents such as tacrolimus extended-release formulations or mTOR inhibitors may be costly for uninsured patients, limiting access in price-sensitive markets. In some countries, access disparities between urban and rural healthcare systems also affect treatment continuity

- Another major challenge is the risk of side effects associated with chronic immunosuppression, including opportunistic infections, hypertension, diabetes, nephrotoxicity, and increased malignancy risk. These complications require close monitoring and may lead to therapy modifications

- Medication non-adherence is also a concern, as missed doses can trigger acute graft rejection and hospitalization. Complex dosing schedules and long treatment duration can negatively affect patient compliance

- Overcoming these barriers through affordable generic drug availability, better reimbursement systems, improved patient education, and development of safer next-generation immunosuppressants will be vital for sustained market growth in the Europe region

Europe Prophylaxis of Organ Rejection Market Scope

The market is segmented on the basis of cause, treatment, route of administration, organ, patient type, end user, and distribution channel.

- By Cause

On the basis of cause, the Europe Prophylaxis of Organ Rejection Market is segmented into epidemiologic exposure, antibacterial prophylaxis, prophylaxis against other pathogens, and others. The antibacterial prophylaxis segment dominated the largest market revenue share of 38.7% in 2025, driven by the critical need to prevent bacterial infections in immunosuppressed transplant recipients. Organ transplant patients remain highly vulnerable to opportunistic infections during the post-operative period. Hospitals widely adopt antibacterial prophylaxis protocols to reduce complications and graft loss risks. Increasing kidney and liver transplant volumes globally support segment demand. Broad-spectrum antibiotics are commonly prescribed during early recovery stages. Clinical guidelines recommending preventive infection management strengthen utilization. Rising antimicrobial stewardship programs are improving treatment selection efficiency. Growth in transplant centers across emerging economies further boosts prescriptions. Continuous monitoring of infection risk in high-acuity patients supports recurring demand. Healthcare providers prioritize prophylaxis to reduce readmission rates and treatment costs. Improved survival rates after transplantation continue to expand eligible patient pools. Strong physician preference for evidence-based preventive regimens sustains market dominance.

The prophylaxis against other pathogens segment is projected to grow at the fastest CAGR of 9.8% from 2026 to 2033, owing to increasing focus on viral, fungal, and parasitic infection prevention after transplantation. Rising incidence of cytomegalovirus and fungal infections is driving adoption of advanced prophylactic therapies. Transplant specialists are increasingly using targeted regimens based on patient risk profiles. Improved diagnostic screening enables earlier identification of infection threats. Growing use of combination immunosuppressive therapy increases need for broader pathogen coverage. Advancements in antifungal and antiviral drugs support market expansion. Lung and heart transplant recipients especially contribute to rising demand. Hospitals are strengthening long-term infection monitoring programs. Favorable reimbursement for post-transplant care in developed markets accelerates uptake. Research into next-generation prophylactic therapies enhances treatment pipelines. Increasing awareness regarding graft preservation outcomes supports demand. Expansion of transplant procedures worldwide further fuels growth.

- By Treatment

On the basis of treatment, the Europe Prophylaxis of Organ Rejection Market is segmented into outpatient immunosuppressant, inpatient immunosuppressant, and others. The outpatient immunosuppressant segment accounted for the largest market revenue share of 56.1% in 2025, driven by lifelong maintenance therapy requirements after transplantation. Most transplant recipients require long-term oral immunosuppressive medication after hospital discharge. Regular prescription refills generate stable recurring demand across major markets. Increasing patient survival rates expand the chronic treatment population. Outpatient care lowers hospitalization costs and improves convenience. Advancements in once-daily formulations improve adherence levels. Telemedicine and remote monitoring programs further support outpatient management. Hospitals increasingly transition stable patients to home-based treatment pathways. Rising kidney transplant numbers significantly contribute to this segment. Insurance coverage for maintenance drugs in developed economies strengthens uptake. Physicians prefer continuous outpatient therapy to minimize rejection episodes. Strong pharmacy network availability supports product accessibility.

The inpatient immunosuppressant segment is projected to grow at the fastest CAGR of 8.9% from 2026 to 2033, owing to rising transplant surgeries and intensive induction therapy demand. Newly transplanted patients require close monitoring and intravenous immunosuppressive administration during hospitalization. Increasing complex transplant cases such as heart and lung procedures support growth. Hospitals are adopting advanced biologics for immediate rejection prevention. Higher acuity patients with complications often need inpatient dose adjustments. Growth in specialized transplant centers is expanding treatment capacity. Rising elderly transplant recipients require supervised inpatient care. Improved hospital protocols enhance medication outcomes and safety. Emerging markets are increasing investment in tertiary transplant hospitals. Clinical innovations in induction therapies strengthen adoption. Greater awareness of early graft protection benefits supports utilization. Expansion of organ donation programs further boosts demand.

- By Route Of Administration

On the basis of route of administration, the Europe Prophylaxis of Organ Rejection Market is segmented into oral and intravenous. The oral segment held the largest market revenue share of 63.4% in 2025, driven by widespread use of tablets and capsules for long-term maintenance therapy. Oral drugs provide convenient self-administration and strong patient compliance. Most chronic immunosuppressive regimens rely on oral formulations after discharge. Reduced hospital dependency supports preference for oral treatments. Pharmaceutical companies continue launching improved extended-release products. Large patient populations with kidney transplants support consistent demand. Retail and specialty pharmacy availability strengthens accessibility. Physicians favor oral regimens for stable recipients with predictable monitoring needs. Lower administration costs compared with hospital infusions aid adoption. Increasing homecare trends further reinforce segment leadership. Strong reimbursement coverage in developed countries supports usage. Continued innovation in combination oral therapies sustains dominance.

The intravenous segment is projected to grow at the fastest CAGR of 8.5% from 2026 to 2033, owing to increasing use during induction therapy and acute rejection prevention. Intravenous drugs provide rapid therapeutic action in critical care settings. Hospitals prefer IV administration immediately after transplantation procedures. Biologic immunosuppressants delivered intravenously are gaining traction. Rising heart and liver transplant complexity supports demand. Patients unable to tolerate oral medication also require IV therapy. Expansion of infusion centers improves treatment access. New monoclonal antibody therapies are supporting segment growth. Improved inpatient monitoring reduces adverse event risks. Emerging markets are increasing transplant infrastructure investments. Physicians value dose precision and rapid control with IV regimens. Higher use in severe complications continues to accelerate adoption.

- By Organ

On the basis of organ, the Europe Prophylaxis of Organ Rejection Market is segmented into kidney, liver, heart, lung, and others. The kidney segment accounted for the largest market revenue share of 47.8% in 2025, driven by kidney transplantation being the most commonly performed organ transplant worldwide. Large end-stage renal disease populations create sustained transplant demand. Kidney recipients require lifelong immunosuppressive prophylaxis, supporting recurring revenues. Improved donor matching technologies are increasing procedure success rates. Government support for renal replacement programs boosts transplant volumes. Expanding dialysis-to-transplant conversion trends support growth. Availability of established treatment protocols strengthens adoption. High survival rates increase long-term maintenance therapy usage. Specialty nephrology centers continue to expand globally. Pharmaceutical companies prioritize kidney transplant indications in trials. Rising living donor procedures also support segment expansion. Strong clinical awareness maintains market dominance.

The lung segment is projected to grow at the fastest CAGR of 10.2% from 2026 to 2033, owing to high rejection risk and intensive prophylaxis requirements. Lung transplant recipients require aggressive immunosuppressive monitoring compared with other organs. Increasing prevalence of advanced pulmonary diseases supports procedure growth. Better surgical techniques are improving transplant success rates. Hospitals are expanding thoracic transplant programs globally. Frequent post-operative infections create additional prophylactic demand. Advanced biologics and tailored regimens support better outcomes. Rising awareness of transplant options for end-stage lung disease boosts adoption. Developed countries are witnessing higher donor utilization rates. Continuous follow-up protocols sustain long-term therapy needs. Research into chronic rejection management supports market expansion. Strong specialist involvement accelerates growth trajectory.

- By Patient Type

On the basis of patient type, the Europe Prophylaxis of Organ Rejection Market is segmented into paediatric and adults. The adults segment dominated the largest market revenue share of 81.6% in 2025, driven by the higher number of adult transplant procedures globally. Chronic diseases such as diabetes, hypertension, and hepatitis increase organ failure risk in adults. Kidney and liver transplants are especially common among middle-aged populations. Adults also represent the largest long-term immunosuppressive user base. Higher healthcare access supports diagnosis and transplantation rates. Insurance coverage in major economies improves treatment continuity. Expansion of adult transplant waiting lists sustains demand. Hospitals maintain dedicated adult transplant programs worldwide. Pharmaceutical dosing protocols are well established for adult patients. Growing elderly transplant candidates also add to volumes. Strong follow-up compliance in monitored settings supports therapy use. These factors reinforce adult segment leadership.

The paediatric segment is projected to grow at the fastest CAGR of 9.4% from 2026 to 2033, owing to improving survival rates and specialized pediatric transplant programs. Advances in surgical care are increasing successful pediatric liver and heart transplants. Greater awareness of congenital organ disorders supports early intervention. Specialized children’s hospitals are expanding transplant capacity. Tailored immunosuppressive dosing protocols improve safety outcomes. Rising investment in rare disease management benefits this segment. Family support systems enhance treatment adherence after surgery. Better donor matching technologies are reducing complications. Government assistance for pediatric critical care supports access. New formulations designed for children are entering the market. Long-term monitoring programs improve graft survival. These factors are accelerating pediatric market growth.

- By End User

On the basis of end user, the Europe Prophylaxis of Organ Rejection Market is segmented into hospitals, clinic, home healthcare, and others. The hospitals segment accounted for the largest revenue share of 58.9% in 2025, driven by concentration of transplant surgeries and post-operative monitoring. Hospitals remain the primary setting for organ transplantation procedures globally. Intensive care support and specialist teams enable safe treatment delivery. Inpatient induction therapy is mainly administered in hospitals. Large procurement contracts strengthen pharmaceutical demand. Advanced diagnostic labs support rejection surveillance. Rising transplant center accreditations boost patient volumes. Public and private hospital expansion supports access. Multidisciplinary care improves outcomes and retention. Emergency complication management further increases hospital dependence. Strong reimbursement structures favor hospital treatment settings. These factors sustain segment dominance.

The home healthcare segment is projected to grow at the fastest CAGR of 10.1% from 2026 to 2033, owing to increasing preference for remote recovery and chronic therapy management. Stable transplant patients are increasingly shifting to home-based monitoring models. Home nursing support improves medication adherence and follow-up care. Telehealth platforms enable specialist consultations without travel burden. Rising healthcare costs encourage decentralized care delivery. Elderly patients especially prefer home treatment convenience. Growth in specialty pharmacy delivery supports accessibility. Digital adherence tools improve therapy outcomes. Governments are promoting homecare to reduce hospital congestion. Expanding wearable monitoring solutions support safety. Higher patient satisfaction further drives adoption. These trends accelerate home healthcare expansion.

- By Distribution Channel

On the basis of distribution channel, the Europe Prophylaxis of Organ Rejection Market is segmented into direct tender, pharmacy stores, and others. The direct tender segment accounted for the largest revenue share of 54.6% in 2025, driven by bulk procurement from transplant hospitals and government institutions. Large healthcare systems prefer direct contracts for pricing efficiency. Continuous medicine supply is critical for transplant patients. Manufacturers benefit from predictable high-volume orders. Tender systems improve inventory planning and compliance standards. Public hospitals in emerging economies increasingly use centralized purchasing. High-cost biologics are often sourced through tenders. Strong supplier relationships support recurring contracts. Procurement transparency enhances institutional trust. Rising transplant procedure numbers boost hospital purchasing demand. Multi-year agreements support revenue stability. These factors sustain segment leadership.

The pharmacy stores segment is projected to grow at the fastest CAGR of 9.3% from 2026 to 2033, owing to rising outpatient maintenance therapy demand. Long-term transplant recipients rely on regular prescription refills from pharmacies. Expansion of specialty pharmacy chains improves access to immunosuppressants. Pharmacist counseling supports adherence and side-effect management. Digital refill systems simplify chronic medicine purchases. Growing urbanization increases pharmacy penetration in emerging markets. Retail chains are adding cold-chain and specialty drug capabilities. Insurance-linked pharmacy networks support recurring demand. Home delivery services further enhance convenience. Increasing transplant survival rates enlarge refill populations. Manufacturers are partnering with retail distributors for reach. These factors drive rapid segment growth.

Europe Prophylaxis of Organ Rejection Market Regional Analysis

- The Europe Prophylaxis of Organ Rejection Market is expected to register a strong CAGR during the forecast period of 2026 to 2033, driven by rising healthcare expenditure, improving transplant care infrastructure, and increasing adoption of advanced immunosuppressive therapies across countries such as the U.K., Germany, France, Italy, and Spain

- Growing awareness regarding organ donation, rising kidney and liver transplant volumes, and expansion of specialty hospitals are further supporting market growth across the region

- In addition, improving access to cost-effective generic immunosuppressants, stronger post-transplant monitoring systems, and increasing investments in advanced transplant centers are enhancing treatment accessibility across Europe

U.K. Europe Prophylaxis of Organ Rejection Market Insight

The U.K. Europe Prophylaxis of Organ Rejection Market accounted for the largest revenue share of approximately 32.9% in Europe in 2025, driven by advanced transplant care infrastructure, high healthcare expenditure, and rising transplant procedure volumes across major healthcare centers. Strong adoption of advanced immunosuppressive therapies, coupled with expanding hospital capacity and improving patient access to specialty care, continues to strengthen market growth. Government support for healthcare modernization and rising awareness regarding post-transplant care are further contributing to market expansion. The U.K. remains the leading market in Europe.

Germany Europe Prophylaxis of Organ Rejection Market Insight

The Germany Europe Prophylaxis of Organ Rejection Market is expected to be the fastest-growing market during the forecast period, projected to register a CAGR of approximately 8.7%, supported by improving transplant healthcare infrastructure, increasing awareness regarding organ donation, and rising numbers of kidney and liver transplant procedures. Expanding specialty care networks, growing demand for advanced and personalized immunosuppressive treatment approaches, and improving long-term transplant monitoring systems are accelerating market development. Germany is emerging as a key high-growth market within Europe.

Europe Prophylaxis of Organ Rejection Market Share

The Prophylaxis of Organ Rejection industry is primarily led by well-established companies, including:

- Astellas Pharma Inc. (Japan)

- Novartis AG (Switzerland)

- Hoffmann-La Roche Ltd. (Switzerland)

- Pfizer Inc. (U.S.)

- Sanofi S.A. (France)

- Bristol-Myers Squibb Company (U.S.)

- AbbVie Inc. (U.S.)

- Teva Pharmaceutical Industries Ltd. (Israel)

- Reddy’s Laboratories Ltd. (India)

- Sun Pharmaceutical Industries Ltd. (India)

- Viatris Inc. (U.S.)

- Johnson & Johnson (U.S.)

- Merck & Co., Inc. (U.S.)

- GlaxoSmithKline plc (U.K.)

- Biocon Biologics Ltd. (India)

- Sandoz International GmbH (Switzerland)

- Chugai Pharmaceutical Co., Ltd. (Japan)

- Takeda Pharmaceutical Company Limited (Japan)

- Lupin Limited (India)

- Cipla Limited (India)

Latest Developments in Europe Prophylaxis of Organ Rejection Market

- In July 2021, Astellas Pharma announced that the U.S. FDA approved a supplemental New Drug Application for PROGRAF (tacrolimus) for the prevention of organ rejection in adult and pediatric lung transplant recipients. This marked the first FDA-approved immunosuppressant specifically indicated for lung transplant rejection prophylaxis, significantly expanding tacrolimus use in transplantation medicine

- In December 2021, Bristol Myers Squibb received U.S. FDA approval for Orencia (abatacept) in combination with a calcineurin inhibitor and methotrexate for the prevention of acute graft-versus-host disease (aGVHD) in hematopoietic stem cell transplantation. This broadened the company’s transplant immunology portfolio and highlighted increasing demand for rejection-prevention biologics

- In June 2022, the U.S. FDA expanded the indication for mycophenolate mofetil (MMF) to include prophylaxis of organ rejection in pediatric recipients of allogeneic heart or liver transplants aged 3 months and older. This approval strengthened pediatric transplant treatment options and increased use of MMF in younger transplant populations

- In January 2023, global transplant centers reported increasing adoption of belatacept-based calcineurin inhibitor–free regimens in kidney transplantation, driven by the need to reduce long-term nephrotoxicity associated with tacrolimus and cyclosporine. This trend supported growth in next-generation organ rejection prophylaxis therapies

- In September 2023, multiple transplant programs in North America and Europe expanded use of extended-release tacrolimus formulations to improve adherence and reduce intrapatient variability, helping optimize long-term graft survival outcomes in kidney and liver transplant recipients

- In May 2024, emerging regulatory and clinical attention focused on pediatric transplantation immunosuppression, following publication of FDA regulatory perspectives on mycophenolate mofetil approvals for children receiving heart and liver transplants. This emphasized growing demand for age-specific prophylaxis of organ rejection therapies

- In November 2024, pipeline attention increased around tegoprubart (AT-1501) and other next-generation CD40/CD154 pathway immunotherapies under clinical investigation for kidney and liver transplantation. These therapies aim to reduce toxicity associated with conventional calcineurin inhibitors while maintaining rejection prevention efficacy

- In December 2025, new clinical outcome research published in transplant nephrology demonstrated that high tacrolimus intrapatient variability was strongly associated with rejection episodes and inferior graft outcomes after kidney transplantation, reinforcing demand for improved monitoring tools and next-generation maintenance immunosuppressive regimens

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.