Europe Refractive Surgery Devices Market

Market Size in USD Million

CAGR :

%

USD

566.98 Million

USD

1,018.74 Million

2025

2033

USD

566.98 Million

USD

1,018.74 Million

2025

2033

| 2026 –2033 | |

| USD 566.98 Million | |

| USD 1,018.74 Million | |

| % | |

|

Europe Refractive Surgery Devices Market Size

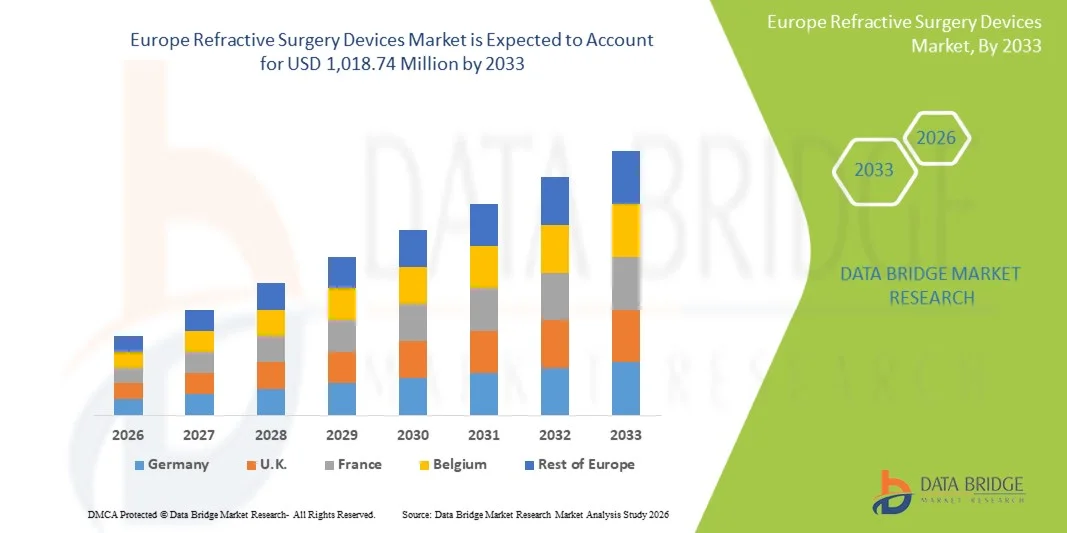

- The Europe refractive surgery devices market size was valued at USD 566.98 million in 2025 and is expected to reach USD 1,018.74 million by 2033, at a CAGR of 7.60% during the forecast period

- The market growth is largely fueled by the increasing prevalence of vision disorders such as myopia, hyperopia, and astigmatism, along with rising awareness and acceptance of advanced vision correction procedures, driving demand for technologically advanced refractive surgery devices across the region

- Furthermore, continuous advancements in laser technologies, growing preference for minimally invasive procedures, and the expanding presence of specialized ophthalmic clinics are establishing refractive surgery devices as a preferred solution for vision correction. These converging factors are accelerating the adoption of refractive surgical procedures, thereby significantly boosting the market growth

Europe Refractive Surgery Devices Market Analysis

- Refractive surgery devices, encompassing technologies such as lasers, phakic intraocular lenses (IOLs), and wavefront aberrometry systems, play a crucial role in correcting vision disorders including myopia, hyperopia, and astigmatism, and are increasingly adopted across ophthalmic clinics and hospitals due to their precision, customization capabilities, and improved surgical outcomes

- The escalating demand for these devices is primarily fueled by the rising burden of vision impairments across Europe, increasing patient awareness regarding advanced surgical options, and a growing preference for minimally invasive and long-term vision correction solutions over conventional eyewear

- Germany dominated the Europe refractive surgery devices market with the largest revenue share of 28.7% in 2025, characterized by advanced healthcare infrastructure, high adoption of cutting-edge laser technologies, and a strong base of skilled ophthalmic surgeons, with the country witnessing increased volumes of LASIK and PRK procedures driven by technological innovation and favorable clinical outcomes

- The United Kingdom is expected to be the fastest growing country in the Europe refractive surgery devices market during the forecast period due to expanding private eye care facilities, rising demand for premium refractive procedures, and increasing investments in ophthalmic technologies

- Laser segment dominated the market with a market share of 46.3% in 2025, driven by its widespread use in procedures such as LASIK and photorefractive keratectomy (PRK), offering high precision, faster recovery times, and strong clinical efficacy, making it the preferred choice among surgeons and patients alike

Report Scope and Europe Refractive Surgery Devices Market Segmentation

|

Attributes |

Europe Refractive Surgery Devices Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Europe

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Europe Refractive Surgery Devices Market Trends

“Rising Adoption of Advanced Laser-Based and Customized Vision Correction Technologies”

- A significant and accelerating trend in the Europe refractive surgery devices market is the growing adoption of advanced laser-based technologies such as femtosecond lasers and wavefront-guided systems, enabling highly precise and customized vision correction procedures

- For instance, LASIK procedures using femtosecond laser platforms and wavefront-guided customization are increasingly performed across leading ophthalmic clinics in Germany and the U.K., improving surgical accuracy and patient outcomes

- Integration of advanced diagnostic tools such as aberrometers and corneal topography systems allows surgeons to create individualized treatment plans, enhancing the precision of refractive procedures and reducing postoperative complications. Furthermore, the use of minimally invasive techniques such as SMILE is gaining traction due to faster recovery and reduced flap-related risks

- The seamless integration of diagnostic and surgical devices within ophthalmic platforms facilitates a streamlined workflow in clinics and hospitals, enabling comprehensive preoperative assessment and precise surgical execution in a single ecosystem

- This trend towards more precise, minimally invasive, and technology-driven refractive procedures is reshaping patient expectations for vision correction. Consequently, companies are increasingly focusing on developing next-generation laser platforms and integrated surgical solutions with enhanced safety and efficiency

- The demand for advanced refractive surgery devices with higher accuracy, faster recovery times, and improved patient comfort is growing rapidly across Europe, as both patients and surgeons prioritize predictable outcomes and long-term visual quality

- Growing investments by ophthalmic device manufacturers in R&D for next-generation excimer and femtosecond laser platforms are accelerating innovation and expanding the availability of advanced refractive solutions across the region

Europe Refractive Surgery Devices Market Dynamics

Driver

“Growing Need Due to Rising Prevalence of Vision Disorders and Increasing Demand for Vision Correction Procedures”

- The increasing prevalence of refractive vision disorders among the European population, coupled with a growing preference for surgical vision correction, is a significant driver for the heightened demand for refractive surgery devices

- For instance, in 2025, expanding adoption of LASIK and PRK procedures across private ophthalmology centers in countries such as France and Germany reflects rising patient willingness to opt for permanent vision correction solutions

- As individuals become more aware of advanced treatment options and seek alternatives to glasses and contact lenses, refractive surgery devices offer effective solutions with long-term benefits such as improved visual acuity and reduced dependency on corrective eyewear

- Furthermore, the increasing availability of skilled ophthalmic surgeons and the expansion of specialized eye care clinics are making refractive procedures more accessible across urban and semi-urban regions in Europe. The growing trend of elective procedures and medical tourism within the region further contributes to market growth

- The convenience of quick procedures, minimal downtime, and high success rates associated with modern refractive surgeries are key factors propelling the adoption of these devices in both public and private healthcare settings. The rising penetration of advanced surgical technologies further supports market expansion

- Rising aging population across Europe is also contributing to higher incidences of presbyopia and other vision-related disorders, thereby increasing the addressable patient pool for refractive procedures

- Increasing awareness campaigns and promotional activities by ophthalmology clinics and device manufacturers are further encouraging patients to opt for corrective surgeries, boosting overall procedure volumes

Restraint/Challenge

“High Procedure Costs and Stringent Regulatory Approval Requirements”

- Concerns surrounding the high cost of refractive surgery procedures and associated devices, along with stringent regulatory requirements in Europe, pose a significant challenge to broader market penetration. As these procedures are often not fully covered by public insurance, affordability becomes a barrier for many patients

- For instance, high treatment costs for procedures using advanced laser systems such as femtosecond lasers and customized wavefront-guided treatments can limit adoption among price-sensitive patients despite their clinical benefits

- Addressing cost-related barriers through flexible financing options, increased insurance coverage in select markets, and the development of cost-efficient technologies is crucial for expanding patient access. Companies and clinics are increasingly highlighting long-term value and reduced dependency on corrective eyewear to justify procedure costs. In addition, compliance with strict medical device regulations under EU MDR increases time-to-market for new technologies

- While technological advancements continue to improve safety and efficacy, the complexity of regulatory approvals and the need for extensive clinical validation can delay the introduction of innovative refractive devices

- Overcoming these challenges through cost optimization, streamlined regulatory processes, and increased patient awareness regarding the long-term benefits of refractive surgery will be vital for sustained market growth

- Limited reimbursement policies for elective vision correction procedures across several European countries further restrict patient adoption, particularly in public healthcare systems

- In addition, variability in surgeon expertise and the need for specialized training to operate advanced laser systems can act as an operational constraint for widespread adoption of newer technologies

Europe Refractive Surgery Devices Market Scope

The market is segmented on the basis of product type, surgery type, application, end user, and distribution channel.

- By Product Type

On the basis of product type, the Europe refractive surgery devices market is segmented into laser, phakic intraocular lens (IOL), aberrometer/wavefront aberrometry, surgical instruments & accessories, refractive surgery kits, pupillary diameter meters, epikeratomes, microkeratomes, thermokeratoplasty, limbal relaxing incision kits, and others. The laser segment dominated the market with the largest market revenue share of 46.3% in 2025, driven by its extensive use in procedures such as LASIK and PRK, offering high precision, predictable outcomes, and faster recovery times. Laser systems are widely adopted across hospitals and specialty clinics due to their clinical reliability and compatibility with advanced surgical workflows. In addition, continuous technological advancements in femtosecond and excimer lasers, along with increasing surgeon preference for bladeless procedures, further reinforce their dominance. The segment also benefits from strong investments by manufacturers in upgrading laser platforms with improved safety features and automation. Growing patient demand for minimally invasive procedures continues to sustain the high adoption of laser-based devices across Europe.

The phakic intraocular lens (IOL) segment is expected to witness the fastest growth rate from 2026 to 2033, driven by increasing demand for alternatives to laser-based procedures, particularly among patients with high refractive errors or thin corneas. Phakic IOLs offer reversible and effective vision correction without altering corneal structure, making them suitable for a broader patient pool. Rising awareness of implantable lens options and advancements in lens design with improved biocompatibility are contributing to their adoption. In addition, increasing surgical success rates and expanding indications for phakic IOLs are encouraging ophthalmologists to recommend them as a viable option. The segment is also gaining traction in cases where laser procedures are not clinically recommended, further expanding its growth potential.

- By Surgery Type

On the basis of surgery type, the market is segmented into LASIK (Laser In-Situ Keratomileusis), Photorefractive Keratectomy (PRK), phakic intraocular lenses (IOL), astigmatic keratotomy (AK), automated lamellar keratoplasty (ALK), intracorneal ring (INTACS), laser thermal keratoplasty (LTK), conductive keratoplasty (CK), radial keratotomy (RK), and others. The LASIK segment dominated the market with the largest market revenue share of 48.5% in 2025, driven by its high success rate, quick recovery time, and widespread acceptance among patients and surgeons. LASIK remains the most commonly performed refractive procedure in Europe due to its minimally invasive nature and proven clinical outcomes. Its ability to correct a wide range of refractive errors with minimal discomfort has contributed significantly to its dominance. Furthermore, continuous improvements in laser precision and flap creation techniques have enhanced procedural safety and predictability. Strong patient preference for LASIK over other procedures further supports its leading position in the market.

The phakic intraocular lenses (IOL) surgery segment is expected to witness the fastest growth rate from 2026 to 2033, owing to its increasing use in patients who are not ideal candidates for laser-based surgeries. Phakic IOL procedures preserve the natural corneal structure while providing high-quality vision correction, making them particularly suitable for younger patients with severe refractive errors. Advancements in lens materials and surgical techniques have improved patient outcomes and reduced complication rates. Growing clinical acceptance among ophthalmologists and rising awareness about lens-based correction options are further accelerating adoption. The segment is also benefiting from increasing demand for reversible vision correction procedures, enhancing its growth trajectory across Europe.

- By Application

On the basis of application, the market is segmented into nearsightedness (myopia), farsightedness (hyperopia), astigmatism, and presbyopia. The myopia segment dominated the market with the largest market revenue share of 52.1% in 2025, driven by the high prevalence of myopia across Europe, particularly among younger populations due to increased screen time and digital device usage. Myopia correction procedures are among the most frequently performed refractive surgeries, supported by strong patient demand for permanent vision correction solutions. The availability of advanced laser technologies and proven surgical outcomes further contributes to the dominance of this segment. In addition, rising awareness regarding early treatment of myopia and its long-term complications is encouraging more patients to undergo corrective procedures. The segment continues to benefit from a large addressable patient pool and consistent procedural volumes across the region.

The presbyopia segment is expected to witness the fastest growth rate from 2026 to 2033, driven by the increasing aging population in Europe and the growing need for near-vision correction among individuals aged 40 and above. Presbyopia-correcting procedures are gaining traction as patients seek alternatives to reading glasses and multifocal lenses. Advances in surgical techniques and the development of innovative treatment options, including multifocal implants and laser-based presbyopia correction, are supporting segment growth. Rising patient awareness and improved access to ophthalmic care are further contributing to increased adoption. The segment is also benefiting from ongoing research and development focused on enhancing surgical outcomes for presbyopic patients.

- By End User

On the basis of end user, the market is segmented into hospitals, specialty clinics, ambulatory surgical centers, and others. The specialty clinics segment dominated the market with the largest market revenue share of 41.8% in 2025, driven by the high concentration of refractive surgery procedures performed in dedicated ophthalmic clinics equipped with advanced laser technologies. These clinics offer specialized expertise, shorter waiting times, and personalized care, making them a preferred choice for patients undergoing elective vision correction procedures. The presence of experienced ophthalmologists and state-of-the-art surgical infrastructure further strengthens their dominance. In addition, specialty clinics often focus exclusively on refractive procedures, enabling higher procedure volumes and operational efficiency. Increasing investments in private ophthalmology chains across Europe are also supporting segment growth.

The ambulatory surgical centers (ASCs) segment is expected to witness the fastest growth rate from 2026 to 2033, driven by the increasing shift toward outpatient and cost-effective surgical settings. ASCs offer advantages such as lower procedural costs, reduced hospital stays, and improved operational efficiency, making them an attractive option for both patients and providers. The rising demand for minimally invasive refractive procedures that do not require extended hospitalization is further supporting the adoption of ASCs. In addition, advancements in portable and compact surgical devices are enabling the expansion of refractive procedures into outpatient environments. Growing preference for convenient and time-efficient treatment options continues to accelerate the growth of this segment.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into direct tender, third-party distributors, and others. The direct tender segment dominated the market with the largest market revenue share of 57.6% in 2025, driven by bulk procurement of refractive surgery devices by hospitals, government healthcare systems, and large ophthalmic centers. Direct purchasing agreements with manufacturers ensure cost efficiency, product authenticity, and access to the latest technologies. This channel is particularly prominent in public healthcare systems across Europe, where procurement processes are centralized. Manufacturers also prefer direct tenders to establish long-term contracts and maintain strong relationships with key institutional buyers. The segment benefits from transparency in pricing and streamlined supply chain operations.

The third-party distributors segment is expected to witness the fastest growth rate from 2026 to 2033, driven by the expanding reach of manufacturers into smaller markets and private clinics across Europe. Distributors play a crucial role in providing localized support, logistics, and after-sales services, making advanced refractive devices more accessible. Increasing demand from emerging healthcare facilities and independent ophthalmology practices is encouraging reliance on distributor networks. In addition, distributors help manufacturers navigate regional regulatory requirements and market entry barriers. The growing need for efficient supply chain management and market penetration strategies is further supporting the expansion of this segment.

Europe Refractive Surgery Devices Market Regional Analysis

- Germany dominated the Europe refractive surgery devices market with the largest revenue share of 28.7% in 2025, characterized by advanced healthcare infrastructure, high adoption of cutting-edge laser technologies, and a strong base of skilled ophthalmic surgeons, with the country witnessing increased volumes of LASIK and PRK procedures driven by technological innovation and favorable clinical outcomes

- Patients in the region highly value the precision, safety, and effectiveness offered by refractive surgery devices, along with access to highly skilled ophthalmologists and advanced surgical centers performing procedures such as LASIK and PRK

- This widespread adoption is further supported by increasing awareness of vision correction options, the presence of leading ophthalmic device manufacturers, and a growing preference for minimally invasive procedures, establishing refractive surgery as a key solution for vision correction in both public and private healthcare settings

The Germany Refractive Surgery Devices Market Insight

Germany dominated the Europe refractive surgery devices market with the largest revenue share of 28.7% in 2025, fueled by its advanced ophthalmic healthcare infrastructure and widespread adoption of cutting-edge laser technologies. Patients are increasingly prioritizing precision-based vision correction procedures such as LASIK and PRK due to their high success rates and long-term benefits. The growing presence of specialized eye clinics and highly skilled ophthalmologists further supports procedure volumes. In addition, strong investments in medical technology innovation and integration of diagnostic and surgical systems are contributing to market expansion. Germany’s emphasis on quality healthcare and early adoption of advanced surgical solutions continues to strengthen its leading position in the region.

U.K. Refractive Surgery Devices Market Insight

The U.K. refractive surgery devices market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by increasing patient awareness regarding vision correction procedures and the rising demand for elective surgeries. Consumers in the country are increasingly prioritizing convenience, safety, and long-term reduction in dependence on corrective eyewear. The expansion of private ophthalmology clinics and availability of advanced laser technologies are further supporting market growth. In addition, the U.K.’s strong healthcare infrastructure and growing preference for minimally invasive procedures are encouraging higher adoption of refractive surgery devices.

France Refractive Surgery Devices Market Insight

The France refractive surgery devices market is expected to expand at a considerable CAGR during the forecast period, driven by rising prevalence of vision disorders and increasing acceptance of refractive surgeries among the population. Patients are increasingly opting for procedures such as LASIK and PRK due to improved clinical outcomes and faster recovery times. The presence of well-established healthcare facilities and growing investments in ophthalmic technologies are further contributing to market growth. Moreover, increasing awareness campaigns and accessibility to advanced eye care services are supporting the adoption of refractive surgery devices across the country.

Italy Refractive Surgery Devices Market Insight

The Italy refractive surgery devices market is gaining momentum due to growing demand for advanced vision correction procedures and increasing awareness regarding minimally invasive surgical options. The country is witnessing rising adoption of laser-based technologies in both public and private healthcare settings. Patients are increasingly seeking alternatives to traditional eyewear, contributing to higher procedure volumes. In addition, the expansion of specialty eye clinics and improvements in healthcare infrastructure are supporting market penetration. Italy’s focus on improving patient outcomes and expanding access to modern ophthalmic treatments continues to drive steady market growth.

Europe Refractive Surgery Devices Market Share

The Europe Refractive Surgery Devices industry is primarily led by well-established companies, including:

- Alcon Inc. (Switzerland)

- Bausch & Lomb Corp. (U.S.)

- Carl Zeiss Meditec AG (Germany)

- Topcon Corp. (Japan)

- Nidek Co., Ltd. (Japan)

- Johnson & Johnson Services, Inc. (U.S.)

- EssilorLuxottica (France)

- Lumibird (France)

- Quantel Medical (France)

- Ophtec BV (Netherlands)

- STAAR Surgical Company (U.S.)

- SCHWIND eye-tech-solutions GmbH (Germany)

- Ziemer Ophthalmic Systems AG (Switzerland)

- Hoya Surgical Optics (Japan)

- Glaukos Corporation (U.S.)

- Amplitude Laser (France)

- Reichert, Inc. (U.S.)

- iVIS Technologies (Italy)

- Rayner Intraocular Lenses Limited (U.K.)

- Moria SA (France)

What are the Recent Developments in Europe Refractive Surgery Devices Market?

- In September 2025, leading ophthalmic technology companies including Heidelberg Engineering, STAAR Surgical, and Ziemer Ophthalmic Systems announced plans to showcase their latest refractive and cataract surgery innovations at the 43rd ESCRS Congress in Copenhagen, signaling active technology evolution in the European market

- In May 2025, Europe’s refractive surgery device market was reported to be strengthening due to cutting-edge research and a mature ophthalmic ecosystem, highlighting rapid innovations in laser-based corrective technologies and expanding healthcare infrastructure

- In May 2025, EssilorLuxottica announced an agreement to acquire Optegra eyecare clinics across several European countries, including the UK, Czech Republic, and Netherlands, expanding clinical networks that provide laser eye surgery and other refractive treatments a strategic move with implications for device demand and service delivery

- In August 2024, ZEISS announced expanded refractive surgery and AI-enhanced ophthalmic solutions at ESCRS 2024 in Barcelona, including first CE-market treatments for hyperopia using lenticule extraction technology and advanced AI tools for surgical planning

- In March 2024, ZEISS unveiled enhancements in ophthalmic surgical visualization and workflow with the VISUMAX 800 and SMILE pro software at ASCRS 2024, reflecting ongoing device innovation that supports refractive surgery procedures a development relevant to European surgeons and clinics adopting similar technologies

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.