Europe Silicon Anode Material Battery Market

Market Size in USD Billion

USD

107.02 Billion

USD

2,045.60 Billion

2024

2032

USD

107.02 Billion

USD

2,045.60 Billion

2024

2032

| 2025 - 2032 | |

| USD 107.02 Billion | |

| USD 2,045.60 Billion | |

| % | |

|

Silicon Anode Material Battery Market Size

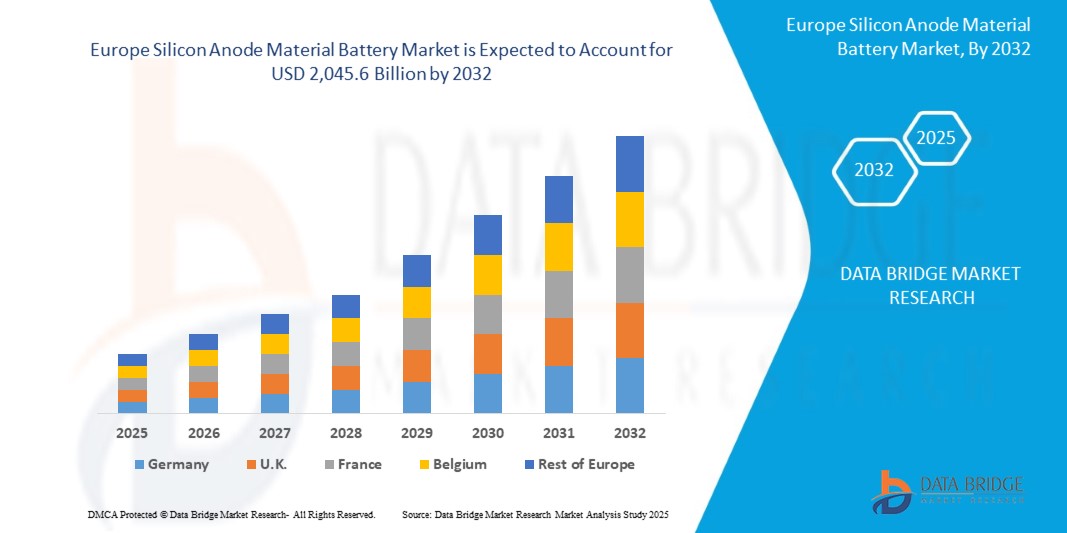

- The Europe Silicon Anode Material Battery market size was valued at USD 107.02 billion in 2024 and is expected to reach USD 2,045.6 billion by 2032, at a CAGR of 44.60% during the forecast period

- This exponential growth is driven by an unprecedented surge in demand for high-energy-density batteries across electric vehicles (EVs), consumer electronics, and renewable energy storage systems. The adoption of silicon anode technology, which offers superior energy density, faster charging capabilities, and enhanced durability compared to traditional graphite-based batteries, is a key catalyst. Europe’s ambitious climate goals, stringent emissions regulations, and substantial investments in battery innovation further propel market expansion.

- Germany dominates the region, commanding 32.41% of the market share in 2024, equivalent to USD 26.71 million. This leadership is attributed to Germany’s robust automotive industry, significant investments in EV infrastructure, and supportive European Union (EU) policies, such as the Fit for 55 package, which aims to reduce carbon emissions by 55.00% by 2032.

Silicon Anode Material Battery Market Analysis

- Silicon anode batteries represent a groundbreaking advancement in lithium-ion battery technology, where silicon either fully replaces or partially supplements conventional graphite anodes. Silicon’s theoretical capacity of 4,200.00 mAh/g, nearly ten times that of graphite’s 372.00 mAh/g, enables batteries with exceptional energy density, rapid charging, and prolonged lifespans. These attributes make silicon anode batteries highly suitable for a diverse array of applications, including electric vehicles, smartphones, smartwatches, laptops, and grid-scale energy storage systems critical for integrating renewable energy sources.

- The market’s growth is fueled by the rapid proliferation of EVs across Europe, with EV sales reaching 2.71 million units in 2023. This surge is driven by stringent EU regulations, such as the ban on internal combustion engine vehicles by 2035.00, and generous incentives, including tax credits and subsidies for EV purchases. Countries like Germany, France, and Norway are at the forefront, with Norway achieving an EV market penetration of 90.12% for new car sales in 2023.

- Technological breakthroughs in silicon anode materials, such as silicon-carbon composites, silicon-graphene hybrids, and nanostructured silicon, are addressing the critical challenge of silicon’s volumetric expansion, which can reach up to 300.00% during charge-discharge cycles. These innovations enhance cycle life, structural integrity, and overall battery performance, making silicon anodes increasingly viable for commercial applications. For instance, Nexeon Limited, a U.K.-based innovator, has developed silicon-carbon composites that improve battery stability, targeting mass production for EVs by 2026.

- Europe is a global leader in battery research and development (R&D), with a projected CAGR of 48.33% for R&D activities through 2032. Key players, including Nexeon Limited (U.K.), SGL Carbon (Germany), Varta AG (Germany), Elkem ASA (Norway), and Talga Group (Sweden), are driving advancements in silicon anode technology. The region’s commitment to sustainable energy solutions, coupled with the growing demand for high-performance batteries in aerospace, defense, and renewable energy storage, significantly accelerates market growth.

- The automotive sector dominates the market, accounting for 65.68% of silicon anode applications, driven by the need for long-range, fast-charging EV batteries. Consumer electronics, including smartphones and wearables, contribute 15.22% of the market, while energy storage systems for renewable energy integration and other applications, such as aerospace, account for the remaining 9.10%. The >10,000 mAh capacity segment leads, holding a 58.45% share in 2024, due to its critical role in powering EVs and grid storage solutions.

Report Scope and Silicon Anode Material Battery Market Segmentation

|

Attributes |

Silicon Anode Material Battery Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Europe

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Silicon Anode Material Battery Market Trends

“Pioneering Silicon Anode Innovations and EV Battery Advancements”

- Development of Advanced Silicon-Based Materials: The adoption of silicon-carbon composites and nanostructured silicon anodes is a leading trend, significantly reducing volumetric expansion and enhancing battery cycle life. In 2024, 65.78% of new silicon anode products in Europe incorporated these materials, improving stability for EV and consumer electronics applications. These innovations are pivotal for overcoming silicon’s technical challenges and enabling scalable commercialization.

- AI-Driven Battery Design Optimization: Artificial intelligence (AI) is transforming silicon anode development through advanced machine learning models like random forest and deep neural networks. These models optimize anode performance, enhance capacity retention, and minimize degradation. In 2025, European researchers achieved a 12.45% improvement in cycle life using AI-driven simulations, marking a significant leap in battery technology.

- Ultra-Fast Charging Technologies: Ultra-fast charging solutions are reshaping the EV and consumer electronics markets. Silicon-based batteries that charge to 80.00% capacity in under 12.00 minutes are gaining traction, led by companies like Varta AG. These advancements reduce range anxiety, enhance consumer convenience, and accelerate EV adoption, particularly in urban areas.

- Sustainable Manufacturing Practices: Sustainable production is a growing priority, with manufacturers leveraging renewable energy for silicon anode production. Facilities like Elkem ASA’s plant in Norway use 100.00% hydropower, minimizing environmental impact. In 2024, 22.67% of Europe’s silicon anode production was powered by renewables, aligning with the EU’s sustainability goals.

- Aerospace and Defense Applications: Silicon anode batteries are increasingly used in aerospace and defense, powering drones, satellites, and mission-critical systems due to their high energy density and compact form factor. This segment is growing at a CAGR of 50.89% through 2032, highlighting the versatility of silicon anode technology.

- Strategic Industry Collaborations: Partnerships between automakers and battery manufacturers are driving commercialization. BMW’s collaboration with SGL Carbon to integrate silicon-enhanced anodes is a prime example, with 18.34% of European EV battery contracts in 2024 involving silicon anode suppliers, signaling strong market confidence.

Silicon Anode Material Battery Market Dynamics

Driver

“EV Surge, EU Policies, and Technological Breakthroughs”

- Rapid EV Adoption Across Europe: The surge in EV sales, with Germany and France accounting for 1.42 million units in 2023, drives demand for silicon anode batteries offering extended range and faster charging. By 2030, EVs are expected to represent 65.78% of new car sales, creating sustained demand for advanced battery technologies.

- Supportive EU Policies and Incentives: The EU’s Fit for 55 package and 2035.00 ban on internal combustion engine vehicles foster a conducive environment for battery innovation. The EU has allocated EUR 10.22 billion for battery R&D and manufacturing by 2030, with national incentives like Germany’s EUR 7,000.00 EV subsidies accelerating adoption.

- Technological Advancements in Silicon Anodes: Innovations in nanostructured silicon, silicon-graphene composites, and silicon-carbon hybrids enhance performance and reduce costs. Manufacturing costs have dropped by 18.56% since 2020, making silicon anodes more competitive.

- Growing Demand for Consumer Electronics: With 35.67% of European consumers using smart wearables in 2024, demand for compact, high-capacity batteries is rising. Silicon anodes enable longer battery life in smartphones and wearables, driving growth in this segment.

- Renewable Energy Storage Expansion: The EU’s target of 600.00 GW of renewable energy capacity by 2030 increases the need for efficient storage solutions. Silicon anode batteries, with their high energy density, are ideal for grid applications, growing at a CAGR of 45.23%.

- Significant R&D Investments: Europe’s R&D ecosystem, supported by EUR 1.89 billion in battery funding in 2024, accelerates silicon anode commercialization. Initiatives like the European Battery Alliance attract global players, strengthening the market.

Restraint/Challenge

“Volumetric Expansion, High Costs, and Supply Chain Issues”

- Silicon’s Volumetric Expansion: Silicon’s 300.00% expansion during charging causes electrode degradation, reducing lifespan. Advanced engineering solutions are needed to address this, increasing development costs.

- High Production Costs: Complex manufacturing processes and nanostructuring techniques make silicon anode batteries 25.33% more expensive than graphite-based alternatives, limiting scalability in cost-sensitive markets.

- Supply Chain Disruptions: Europe’s reliance on 68.45% of silicon imports from Asia exposes the market to supply chain disruptions and geopolitical tensions, increasing costs by 12.78% in 2024.

- Limited Commercial Scalability: Only 8.22% of silicon anode batteries were in mass-market applications in 2024, due to technical complexities and high capital requirements, slowing adoption.

- Competition from Alternative Anode Materials: Lithium titanate and other solid-state materials, with 15.67% lower costs, compete with silicon anodes in certain applications, challenging market growth.

- Stringent Regulatory Requirements: EU regulations mandating recycled content and carbon footprint reporting increase compliance costs by 10.45% of production expenses, delaying market entry.

Silicon Anode Material Battery Market Scope

The Europe residential lighting market is segmented on the basis of product type, component, application, technology, end-user, and sales channel.

- By Raw Material

On the basis of raw material, the market is segmented into silicon compounds and silicon isotopes. The silicon compounds segment dominated the market with a commanding revenue share of 68.22% in 2024, driven by its widespread use in silicon-carbon composites for EV batteries.

The silicon isotope segment is expected to witness the fastest CAGR of 51.45% from 2025 to 2032, fueled by its use in high-performance electronics.

- By Battery Application

On the basis of battery application, the market is segmented into pure anode silicon battery and SiliconX battery. The SiliconX battery segment accounted for the largest market revenue share of 62.78% in 2024, valued at USD 51.76 million, driven by its hybrid silicon-graphite design for EVs.

The pure anode silicon battery segment is expected to witness the fastest CAGR of 53.12% from 2025 to 2032, propelled by advancements in 100% silicon anode technology.

- By End User

On the basis of end-user, the market is segmented into automotive, electronics, energy and power, and others. The automotive segment held the largest market revenue share of 65.68% in 2024, driven by the surging demand for EV batteries.

The electronics segment is expected to witness the fastest CAGR of 49.33% from 2025 to 2032, fueled by the growing adoption of smart wearables and smartphones.

- By Capacity

On the basis of capacity, the market is segmented into 0–3,000 mAh, 3,000–10,000 mAh, 10,000–60,000 mAh, and 60,000 mAh and above. The >10,000 mAh segment dominated the market with a commanding revenue share of 58.45% in 2024, driven by its critical role in EVs and grid storage applications.

The 3,000–10,000 mAh segment is expected to witness the fastest CAGR of 50.67% from 2025 to 2032, propelled by its use in consumer electronics.

Silicon Anode Material Battery Market Regional Analysis

Germany Silicon Anode Material Battery Market Insight

The Germany dominated the Europe silicon anode material battery market with a revenue share of 32.41% in 2024, valued at USD 26.71 million, driven by its robust automotive industry, with 800,000 EV units sold in 2023, and significant R&D investments. Key players like SGL Carbon GmbH and Varta AG are at the forefront of innovation, with Volkswagen Group supporting projects such as Nexo’s silicon anode development. The automotive sector accounted for the largest application share of 80.12% in 2024, with BMW integrating silicon-enhanced anodes into its EV lineup. Germany is expected to maintain its dominance with a projected CAGR of 48.27% from 2025 to 2032, fueled by EU policies like the Fit for 55 package and a €3 billion investment in EV charging infrastructure.

France Silicon Anode Material Battery Market Insight

France’s market was valued at USD 18.3 million in 2024, driven by NEO Battery Materials’ plant, which is set to produce 5,000 tons of silicon anodes annually by 2026. Government incentives, including 49-year tax exemptions, support market growth. The automotive and energy storage sectors accounted for significant shares in 2024, driven by France’s EV sales of 600,000 units in 2023. France is expected to witness a CAGR of 45% from 2025 to 2032, fueled by its focus on sustainable energy and proximity to EU markets.

United Kingdom Silicon Anode Material Battery Market Insight

The United Kingdom’s market was valued at USD 15.1 million in 2024, driven by its growing role in EV supply chains, with companies like Tesla establishing manufacturing facilities. The automotive segment accounted for the largest application share of 70% in 2024, driven by exports to the EU. The UK is anticipated to witness a CAGR of 43% from 2025 to 2032, supported by trade agreements like Brexit and increasing EV production.

Silicon Anode Material Battery Market Share

- The Silicon Anode Material Battery industry is primarily led by well-established companies, including:

- Amprius Technologies (U.S.)

- Sila Nanotechnologies Inc. (U.S.)

- Group14 Technologies Inc. (U.S.)

- NanoGraf Corporation (U.S.)

- Enovix Corporation (U.S.)

- Enevate Corporation (U.S.)

- California Lithium Battery (U.S.)

- Solidion Technology, Inc. (U.S.)

- Ionblox Inc. (U.S.)

- NEO Battery Materials Ltd. (Canada)

- Targray Technology International (Canada)

Latest Developments in Europe Silicon Anode Material Battery Market

- In April 2025, Sila Nanotechnologies commenced commissioning its cutting-edge manufacturing facility in Moses Lake, Washington, strategically designed to produce 10 GWh of high-performance silicon anode material annually by 2026. This facility leverages low-cost, renewable hydropower to ensure sustainable, eco-friendly production, positioning Sila as a leader in scalable, environmentally responsible battery technology and supporting the growing demand for EV and energy storage solutions across North America.

- In December 2024, Sionic Energy unveiled a groundbreaking 100% silicon anode battery, delivering an impressive 40% higher energy density compared to conventional graphite-based batteries. This innovative battery has been integrated into select U.S. electric vehicle models, offering enhanced range and performance, marking a significant milestone in the commercialization of pure silicon anode technology and reinforcing Sionic’s role in advancing EV battery capabilities.

- In March 2025, Samsung SDI showcased its revolutionary 50Amp ultra-high-power cylindrical battery featuring advanced silicon anodes at InterBattery 2025, a premier global battery exhibition. Targeting high-performance EV applications, this battery offers 20% faster charging times, enabling rapid charge cycles that enhance consumer convenience and support the widespread adoption of electric vehicles in competitive markets.

- In July 2023, Panasonic Energy entered into a strategic long-term agreement with Nexeon, a leading silicon anode material supplier, to secure a steady supply of high-quality silicon anodes for its advanced battery manufacturing facility in Kansas. This collaboration, set to enhance EV battery performance starting in 2025, underscores Panasonic’s commitment to integrating next-generation materials to deliver superior energy density and efficiency in electric vehicle applications.

- In 2024, NEO Battery Materials secured an 8-acre site in Windsor, Canada, for the construction of its first dedicated silicon anode manufacturing facility. This ambitious project aims to achieve an annual production capacity of 5,000 tons upon full-phase expansion, positioning NEO as a key player in Canada’s growing battery supply chain and supporting the region’s EV and energy storage markets with domestically produced, high-performance anode materials.

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Table of Content

1 INTRODUCTION

1.1 OBJECTIVES OF THE STUDY

1.2 MARKET DEFINITION

1.3 OVERVIEW OF EUROPE SILICON ANODE MATERIAL BATTERY MARKET

1.4 CURRENCY AND PRICING

1.5 LIMITATION

1.6 MARKETS COVERED

2 MARKET SEGMENTATION

2.1 KEY TAKEAWAYS

2.2 ARRIVING AT THE EUROPE SILICON ANODE MATERIAL BATTERY MARKET

2.2.1 VENDOR POSITIONING GRID

2.2.2 TECHNOLOGY LIFE LINE CURVE

2.2.3 MARKET GUIDE

2.2.4 COMPANY POSITIONING GRID

2.2.5 COMAPANY MARKET SHARE ANALYSIS

2.2.6 MULTIVARIATE MODELLING

2.2.7 TOP TO BOTTOM ANALYSIS

2.2.8 STANDARDS OF MEASUREMENT

2.2.9 VENDOR SHARE ANALYSIS

2.2.10 DATA POINTS FROM KEY PRIMARY INTERVIEWS

2.2.11 DATA POINTS FROM KEY SECONDARY DATABASES

2.3 EUROPE SILICON ANODE MATERIAL BATTERY MARKET: RESEARCH SNAPSHOT

2.4 ASSUMPTIONS

3 MARKET OVERVIEW

3.1 DRIVERS

3.2 RESTRAINTS

3.3 OPPORTUNITIES

3.4 CHALLENGES

4 EXECUTIVE SUMMARY

5 PREMIUM INSIGHT

5.1 PORTERS FIVE FORCES

5.2 REGULATORY STANDARDS

5.3 TECHNOLOGICAL TRENDS

5.4 PATENT ANALYSIS

5.5 CASE STUDY

5.6 VALUE CHAIN ANALYSIS

5.7 COMPANY COMPARITIVE ANALYSIS

5.8 PRICING ANALYSIS

6 EUROPE SILICON ANODE MATERIAL BATTERY MARKET, BY COMPONENTS

6.1 OVERVIEW

6.2 SOLID STATE ELECTROLYTES

6.3 SILICON ANODE (WITH IDENTIFICATION B/W SI)

6.4 SEPARATOR

6.5 CURRENT COLLECTORS

6.6 SULFUR ANODE

6.7 OTHERS

7 EUROPE SILICON ANODE MATERIAL BATTERY MARKET, BY MATERIAL

7.1 OVERVIEW

7.2 SIO

7.3 SI-C

7.4 COATING MATERIAL ON ELECTRODE

7.5 OTHERS

8 EUROPE SILICON ANODE MATERIAL BATTERY MARKET, BY CAPACITY

8.1 OVERVIEW

8.2 0 – 3,000 MAH

8.3 3,000 – 10,000 MAH

8.4 10,000 – 60,000 MAH

8.5 60,000 MAH & ABOVE

9 EUROPE SILICON ANODE MATERIAL BATTERY MARKET, BY SIZE

9.1 OVERVIEW

9.2 LESS THAN 4 MICRON

9.3 MORE THAN 4 MICRON

10 EUROPE SILICON ANODE MATERIAL BATTERY MARKET, BY BATTERY TYPE

10.1 OVERVIEW

10.2 CYLINDRICAL

10.3 PRISMATIC

10.4 POUCH

11 EUROPE SILICON ANODE MATERIAL BATTERY MARKET, BY VOLTAGE

11.1 OVERVIEW

11.2 LOW VOLTAGE

11.3 MEDIUM VOLTAGE

11.4 HIGH VOLTAGE

12 EUROPE SILICON ANODE MATERIAL BATTERY MARKET, BY DISTRIBUTION CHANNEL

12.1 OVERVIEW

12.2 DIRECT

12.3 IN-DIRECT

13 EUROPE SILICON ANODE MATERIAL BATTERY MARKET, BY END USER

13.1 OVERVIEW

13.2 AUTOMOTIVE

13.2.1 AUTOMOTIVE, BY TYPE

13.2.1.1. BATTERY ELECTRIC VEHICLES (BEVS)

13.2.1.2. PLUG-IN HYBRID ELECTRIC VEHICLES (PHEVS)

13.2.1.3. HYBRID ELECTRIC VEHICLES (HEVS)

13.2.1.4. ELECTRIC BICYLCES

13.2.2 MATERIAL, BY TYPE

13.2.2.1. SOLID STATE ELECTROLYTES

13.2.2.2. SILICON ANODE (WITH IDENTIFICATION B/W SI)

13.2.2.3. SIO

13.2.2.4. SI-C

13.2.2.5. COATING MATERIAL ON ELECTRODE

13.2.2.6. SEPARATOR

13.2.2.7. CURRENT COLLECTORS

13.2.2.8. SULFUR ANODE

13.2.2.9. OTHERS

13.3 CONSUMER ELECTRONICS

13.3.1 CONSUMER ELECTRONICS, BY TYPE

13.3.1.1. 3G/4G CELLPHONES

13.3.1.2. LAPTOPS

13.3.1.3. TABLETS

13.3.1.4. MP4

13.3.1.5. DIGITAL CAMERAS

13.3.1.6. OTHER ELECTRONIC DEVICES

13.3.2 MATERIAL, BY TYPE

13.3.2.1. SOLID STATE ELECTROLYTES

13.3.2.2. SILICON ANODE (WITH IDENTIFICATION B/W SI)

13.3.2.3. SIO

13.3.2.4. SI-C

13.3.2.5. COATING MATERIAL ON ELECTRODE

13.3.2.6. SEPARATOR

13.3.2.7. CURRENT COLLECTORS

13.3.2.8. SULFUR ANODE

13.3.2.9. OTHERS

13.4 INDUSTRIAL

13.4.1 MATERIAL, BY TYPE

13.4.1.1. SOLID STATE ELECTROLYTES

13.4.1.2. SILICON ANODE (WITH IDENTIFICATION B/W SI)

13.4.1.3. SIO

13.4.1.4. SI-C

13.4.1.5. COATING MATERIAL ON ELECTRODE

13.4.1.6. SEPARATOR

13.4.1.7. CURRENT COLLECTORS

13.4.1.8. SULFUR ANODE

13.4.1.9. OTHERS

13.5 GRID & RENEWABLE ENERGY

13.5.1 MATERIAL, BY TYPE

13.5.1.1. SOLID STATE ELECTROLYTES

13.5.1.2. SILICON ANODE (WITH IDENTIFICATION B/W SI)

13.5.1.3. SIO

13.5.1.4. SI-C

13.5.1.5. COATING MATERIAL ON ELECTRODE

13.5.1.6. SEPARATOR

13.5.1.7. CURRENT COLLECTORS

13.5.1.8. SULFUR ANODE

13.5.1.9. OTHERS

14 EUROPE SILICON ANODE MATERIAL BATTERY MARKET, BY GEOGRAPHY

EUROPE SILICON ANODE MATERIAL BATTERY MARKET, (ALL SEGMENTATION PROVIDED ABOVE IS REPRESENTED IN THIS CHAPTER BY COUNTRY)

14.1 EUROPE

14.1.1 GERMANY

14.1.2 FRANCE

14.1.3 U.K.

14.1.4 ITALY

14.1.5 SPAIN

14.1.6 RUSSIA

14.1.7 TURKEY

14.1.8 BELGIUM

14.1.9 NETHERLANDS

14.1.10 NORWAY

14.1.11 FINLAND

14.1.12 SWITZERLAND

14.1.13 DENMARK

14.1.14 SWEDEN

14.1.15 POLAND

14.1.16 REST OF EUROPE

14.2 KEY PRIMARY INSIGHTS: BY MAJOR COUNTRIES

15 EUROPE SILICON ANODE MATERIAL BATTERY MARKET,COMPANY LANDSCAPE

15.1 COMPANY SHARE ANALYSIS: EUROPE

15.2 MERGERS & ACQUISITIONS

15.3 NEW PRODUCT DEVELOPMENT AND APPROVALS

15.4 EXPANSIONS

15.5 REGULATORY CHANGES

15.6 PARTNERSHIP AND OTHER STRATEGIC DEVELOPMENTS

16 EUROPE SILICON ANODE MATERIAL BATTERY MARKET, SWOT & DBMR ANALYSIS

17 EUROPE SILICON ANODE MATERIAL BATTERY MARKET, COMPANY PROFILE

17.1 LEYDENJAR TECHNOLOGIES

17.1.1 COMPANY SNAPSHOT

17.1.2 REVENUE ANALYSIS

17.1.3 GEOGRAPHIC PRESENCE

17.1.4 PRODUCT PORTFOLIO

17.1.5 RECENT DEVELOPMENT

17.2 NEXEON® LTD.

17.2.1 COMPANY SNAPSHOT

17.2.2 REVENUE ANALYSIS

17.2.3 GEOGRAPHIC PRESENCE

17.2.4 PRODUCT PORTFOLIO

17.2.5 RECENT DEVELOPMENT

17.3 HUAWEI

17.3.1 COMPANY SNAPSHOT

17.3.2 REVENUE ANALYSIS

17.3.3 GEOGRAPHIC PRESENCE

17.3.4 PRODUCT PORTFOLIO

17.3.5 RECENT DEVELOPMENT

17.4 SILA NANOTECHNOLOGIES INC.

17.4.1 COMPANY SNAPSHOT

17.4.2 REVENUE ANALYSIS

17.4.3 GEOGRAPHIC PRESENCE

17.4.4 PRODUCT PORTFOLIO

17.4.5 RECENT DEVELOPMENT

17.5 TARGRAY

17.5.1 COMPANY SNAPSHOT

17.5.2 REVENUE ANALYSIS

17.5.3 GEOGRAPHIC PRESENCE

17.5.4 PRODUCT PORTFOLIO

17.5.5 RECENT DEVELOPMENT

17.6 ENWAIR ENERGY TECHNOLOGIES CORP

17.6.1 COMPANY SNAPSHOT

17.6.2 REVENUE ANALYSIS

17.6.3 GEOGRAPHIC PRESENCE

17.6.4 PRODUCT PORTFOLIO

17.6.5 RECENT DEVELOPMENT

17.7 NANOXPLORE INC.

17.7.1 COMPANY SNAPSHOT

17.7.2 REVENUE ANALYSIS

17.7.3 GEOGRAPHIC PRESENCE

17.7.4 PRODUCT PORTFOLIO

17.7.5 RECENT DEVELOPMENT

17.8 E-MAGY

17.8.1 COMPANY SNAPSHOT

17.8.2 REVENUE ANALYSIS

17.8.3 GEOGRAPHIC PRESENCE

17.8.4 PRODUCT PORTFOLIO

17.8.5 RECENT DEVELOPMENT

17.9 CALIFORNIA LITHIUM BATTERY

17.9.1 COMPANY SNAPSHOT

17.9.2 REVENUE ANALYSIS

17.9.3 GEOGRAPHIC PRESENCE

17.9.4 PRODUCT PORTFOLIO

17.9.5 RECENT DEVELOPMENT

17.1 GROUP14 TECHNOLOGIES

17.10.1 COMPANY SNAPSHOT

17.10.2 REVENUE ANALYSIS

17.10.3 GEOGRAPHIC PRESENCE

17.10.4 PRODUCT PORTFOLIO

17.10.5 RECENT DEVELOPMENT

17.11 ELKEM ASA

17.11.1 COMPANY SNAPSHOT

17.11.2 REVENUE ANALYSIS

17.11.3 GEOGRAPHIC PRESENCE

17.11.4 PRODUCT PORTFOLIO

17.11.5 RECENT DEVELOPMENT

17.12 CENATE AS

17.12.1 COMPANY SNAPSHOT

17.12.2 REVENUE ANALYSIS

17.12.3 GEOGRAPHIC PRESENCE

17.12.4 PRODUCT PORTFOLIO

17.12.5 RECENT DEVELOPMENT

17.13 ALKEGEN

17.13.1 COMPANY SNAPSHOT

17.13.2 REVENUE ANALYSIS

17.13.3 GEOGRAPHIC PRESENCE

17.13.4 PRODUCT PORTFOLIO

17.13.5 RECENT DEVELOPMENT

17.14 UNIFRAX

17.14.1 COMPANY SNAPSHOT

17.14.2 REVENUE ANALYSIS

17.14.3 GEOGRAPHIC PRESENCE

17.14.4 PRODUCT PORTFOLIO

17.14.5 RECENT DEVELOPMENT

NOTE: THE COMPANIES PROFILED IS NOT EXHAUSTIVE LIST AND IS AS PER OUR PREVIOUS CLIENT REQUIREMENT. WE PROFILE MORE THAN 100 COMPANIES IN OUR STUDY AND HENCE THE LIST OF COMPANIES CAN BE MODIFIED OR REPLACED ON REQUEST

18 CONCLUSION

19 QUESTIONNAIRE

20 RELATED REPORTS

21 ABOUT DATA BRIDGE MARKET RESEARCH

Europe Silicon Anode Material Battery Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Europe Silicon Anode Material Battery Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Europe Silicon Anode Material Battery Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.