Europe Surgical Glue Market

Market Size in USD Billion

USD

1.88 Billion

USD

3.50 Billion

2025

2033

USD

1.88 Billion

USD

3.50 Billion

2025

2033

| 2026 - 2033 | |

| USD 1.88 Billion | |

| USD 3.50 Billion | |

| % | |

|

Europe Surgical Glue Market Size

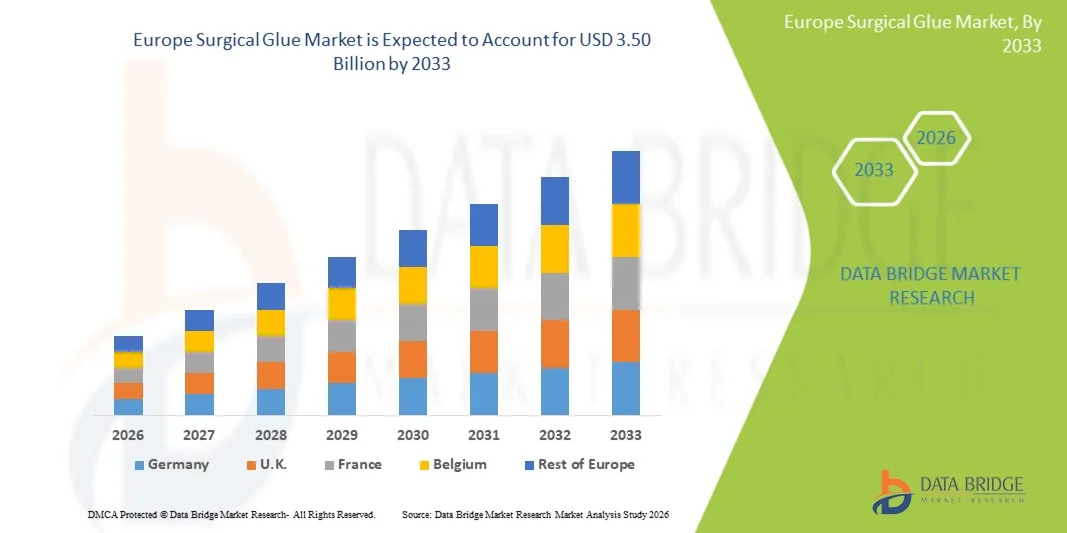

- The Europe Surgical Glue Market size was valued at USD 1.88 billion in 2025 and is expected to reach USD 3.50billion by 2033, at a CAGR of 8.10% during the forecast period

- The market growth is largely fueled by the increasing adoption of minimally invasive surgeries, rising demand for faster wound closure solutions, and growing preference for alternatives to traditional sutures and staples in hospitals and surgical centers, leading to improved patient outcomes, reduced procedure time, and lower risk of infection

- Furthermore, rising technological advancements in bioadhesive formulations, expanding applications across cardiovascular, orthopedic, and general surgeries, and increasing awareness among healthcare providers about the benefits of surgical adhesives are establishing Surgical Glue solutions as essential tools in modern surgical procedures. These converging factors are accelerating the uptake of these products, thereby significantly boosting the industry’s growth

Europe Surgical Glue Market Analysis

- Surgical glue, offering advanced adhesive solutions for wound closure and tissue repair, is increasingly vital in modern surgical procedures across hospitals, ambulatory centers, and specialty clinics due to its efficiency, reduced procedure time, and improved patient outcomes

- The escalating demand for surgical glue is primarily fueled by the widespread adoption of minimally invasive surgeries, growing prevalence of chronic wounds and surgical interventions, and a rising preference for faster, safer, and less invasive wound closure solutions

- The U.K. dominated the Europe Surgical Glue Market with the largest revenue share of approximately 38.9% in 2025, supported by advanced healthcare infrastructure, high healthcare expenditure, and the strong presence of leading surgical product manufacturers. The country accounts for a significant share due to the increasing number of surgical procedures and growing adoption of advanced wound closure technologies across hospitals and outpatient surgical centers

- Germany is expected to be the fastest-growing region in the Europe Surgical Glue Market during the forecast period, registering a CAGR of approximately 7.8%, driven by improving healthcare infrastructure, rising adoption of minimally invasive surgeries, increasing investments in healthcare innovation, and growing awareness regarding advanced surgical adhesives across hospitals, ambulatory surgical centers, and specialty clinics

- The hemostasis segment dominated the largest market revenue share of around 49.2% in 2025, driven by the critical need to control bleeding during surgeries and trauma management

Report Scope and Europe Surgical Glue Market Segmentation

|

Attributes |

Surgical Glue Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Europe

|

|

Key Market Players |

• Baxter International (U.S.) |

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Europe Surgical Glue Market Trends

“Growing Need for Minimally Invasive Procedures and Advanced Wound Closure Solutions”

- The global demand for surgical glue is being driven by the increasing adoption of minimally invasive procedures that reduce patient recovery times, lower the risk of infection, and improve cosmetic outcomes compared to traditional sutures and staples

- For instance, in 2024, Ethicon (Johnson & Johnson) launched a new cyanoacrylate-based surgical adhesive for laparoscopic gastrointestinal surgeries, which significantly reduced post-operative complications and improved closure efficiency

- The rising prevalence of chronic diseases such as diabetes, cardiovascular disorders, and obesity is contributing to higher incidences of surgical interventions, which boosts the need for effective tissue adhesives

- Advancements in surgical glue formulations, including faster polymerization, superior biocompatibility, and stronger tissue adhesion, are enhancing surgeon confidence and patient outcomes, increasing global adoption

- The convenience of surgical glue, such as reduced operation time, decreased need for follow-up procedures, and improved patient comfort, is further propelling its use across hospitals, outpatient surgical centers, and ambulatory care facilities

- Increasing awareness among clinicians about the benefits of surgical adhesives in reducing post-operative complications, hematoma formation, and wound dehiscence is also accelerating market growth globally

Europe Surgical Glue Market Dynamics

Driver

“Technological Innovations and Expanding Applications Across Surgical Specialties”

- The Europe Surgical Glue Market is witnessing significant technological innovation, with new delivery systems, pre-filled applicators, and advanced formulations improving ease of use, precision, and safety

- For instance, in 2025, B. Braun introduced a fibrin-based hemostatic adhesive for orthopedic procedures, which minimized intraoperative bleeding and reduced post-operative hematoma formation

- Surgical glues are increasingly being integrated with bioactive materials and absorbable scaffolds to promote tissue regeneration and accelerate wound healing

- Growth in minimally invasive and robotic-assisted surgeries is expanding the use of surgical adhesives, as these procedures require precise, sterile closure in complex anatomical areas

- New applications are emerging in ophthalmology, cardiovascular surgery, urology, and cosmetic procedures, highlighting the versatility of surgical glues beyond traditional general surgery

- Expansion into emerging markets is contributing to global growth, driven by increasing surgical volumes, rising healthcare investments, and government initiatives supporting modern wound management solutions

Restraint/Challenge

“High Costs, Regulatory Hurdles, and Limited Awareness in Emerging Markets”

- The relatively high price of advanced surgical glues compared to conventional sutures or staples remains a significant barrier to adoption, especially in cost-sensitive regions

- For instance, adoption in Southeast Asian hospitals has been slower due to price constraints and limited familiarity with fibrin-based and cyanoacrylate adhesives

- Stringent regulatory requirements across regions, such as the FDA in the U.S., EMA in Europe, and PMDA in Japan, can delay product approvals and increase research and development costs

- Limited training and awareness among healthcare professionals about optimal application techniques and benefits of surgical adhesives can hinder market penetration, particularly in developing countries

- Storage and handling challenges, including sensitivity to moisture, short shelf life, and the need for specialized applicators, create additional barriers for hospitals and surgical centers

- Potential allergic reactions or rare tissue incompatibility issues may raise concerns among clinicians, necessitating additional safety studies and product information dissemination

- Competition from alternative wound closure methods, including advanced sutures, staples, and novel wound dressings, may restrict rapid adoption in some regions until further clinical evidence supports broader use

Europe Surgical Glue Market Scope

The Europe Surgical Glue Market is segmented on the basis of product, indication, application, and end user.

• By Product

On the basis of product, the market is segmented into natural, synthetic, and semi-synthetic surgical glues. The synthetic segment dominated the largest market revenue share of approximately 45.6% in 2025, driven by its superior adhesion, consistency, and broad clinical applications. Synthetic surgical glues, such as cyanoacrylates and polymer-based adhesives, are widely used for rapid tissue closure, hemostasis, and wound sealing. Hospitals and specialty clinics prefer synthetic glues due to predictable performance, longer shelf-life, and reduced infection risk. The segment benefits from increasing surgical procedures, rising incidence of trauma, and growing demand for minimally invasive techniques. Technological advancements in polymer chemistry have improved bonding strength, elasticity, and biocompatibility, which further supports adoption. Synthetic glues are used across multiple surgical specialties, including cardiac, orthopedic, and plastic surgeries, ensuring recurring usage. Regulatory approvals and clinical guidelines endorsing synthetic glues for tissue sealing reinforce market dominance. Rising awareness among surgeons about improved patient outcomes with synthetic adhesives drives further adoption. Europe and Europe remain key markets due to established healthcare infrastructure and early technology adoption. The segment also benefits from integration in advanced surgical kits and training programs in hospitals.

The natural segment is expected to witness the fastest CAGR of 9.3% from 2026 to 2033, fueled by increasing demand for bio-based, biodegradable adhesives that minimize tissue irritation. Natural glues, including fibrin-based products, offer excellent biocompatibility and are widely used for hemostasis and wound closure. Growing adoption in cardiac, neurosurgical, and cosmetic procedures supports growth. The segment is further driven by rising patient preference for natural and safer alternatives, as well as expanding hospital procurement of advanced bioadhesives. Technological enhancements in fibrin glue production and sterilization have improved safety and shelf stability. Emerging markets are seeing higher adoption due to increasing surgical volumes and healthcare infrastructure development. Clinical studies validating the efficacy of natural glues encourage wider usage. Additionally, training programs in hospitals and surgical centers promote adoption among surgeons. The combination of bio-safety, patient outcomes, and regulatory support is expected to drive robust growth.

• By Indication

On the basis of indication, the market is segmented into hemostasis and tissue sealing. The hemostasis segment dominated the largest market revenue share of around 49.2% in 2025, driven by the critical need to control bleeding during surgeries and trauma management. Surgical glues for hemostasis are widely used in cardiac, liver, spleen, and orthopedic surgeries to reduce intraoperative blood loss and improve patient recovery. Hospitals, specialty clinics, and ambulatory surgical centers increasingly rely on hemostatic glues for their rapid action, ease of application, and compatibility with minimally invasive procedures. Advancements in polymer chemistry and fibrin formulations have enhanced clotting efficiency and reduced postoperative complications. Regulatory approvals and clinical guideline recommendations for hemostasis in high-risk surgeries further support adoption. Recurrent use in multiple surgeries ensures stable revenue streams. Growth is also driven by increasing awareness among surgeons and rising volumes of elective and emergency surgical procedures.

The tissue sealing segment is expected to witness the fastest CAGR of 8.9% from 2026 to 2033, fueled by the growing adoption of surgical glues for wound closure, internal tissue bonding, and anastomosis in minimally invasive procedures. Tissue sealing glues are increasingly used in plastic surgery, general surgeries, and gastrointestinal interventions, providing suture-less closure options. Technological improvements in adhesive formulations and delivery systems, coupled with enhanced tissue compatibility, drive rapid adoption. Rising surgical volumes, patient preference for reduced scarring, and faster recovery times further contribute to growth. Hospitals and outpatient surgical centers are increasingly integrating tissue-sealing glues into standard procedural kits.

• By Application

On the basis of application, the market is segmented into cardiac surgery, neurosurgery, general surgeries, orthopedic surgery, plastic surgery, wound management, pulmonary surgery, burn bleeding, liver and spleen lacerations, and others. The general surgeries segment dominated the market with a revenue share of approximately 35.8% in 2025, driven by the high number of procedures requiring tissue closure and hemostasis. Hospitals and surgical centers frequently use surgical glues for gastrointestinal, appendectomy, hernia repair, and other routine procedures. The segment benefits from the broad applicability of adhesives across multiple surgical specialties, technological advancements in adhesive performance, and growing preference for minimally invasive techniques. Clinical guidelines endorsing the use of glues in general surgeries, combined with ease of application and reduced operating times, support market dominance. Increasing patient volumes, rising awareness among surgeons, and expanding hospital infrastructure reinforce growth.

The cardiac surgery segment is expected to witness the fastest CAGR of 9.5% from 2026 to 2033, driven by the critical role of surgical adhesives in hemostasis, vascular repair, and tissue reinforcement during high-risk cardiac interventions. Surgical glues reduce bleeding complications, enhance suture line integrity, and minimize patient recovery time. Hospitals and specialized cardiac centers are increasingly adopting advanced synthetic and bio-based adhesives. Technological improvements in adhesive viscosity, bonding strength, and biocompatibility accelerate adoption. Increasing prevalence of cardiovascular diseases, rising surgical volumes, and regulatory support for advanced adhesives further drive growth.

• By End User

On the basis of end user, the market is segmented into hospitals/clinics, specialty clinics, and ambulatory surgical centers (ASCs). The hospitals/clinics segment dominated the largest revenue share of approximately 51.4% in 2025, due to the high number of surgical procedures performed and the availability of trained personnel for adhesive application. Hospitals frequently perform complex surgeries, including cardiac, orthopedic, and neurosurgical procedures, requiring reliable hemostasis and tissue sealing solutions. The segment benefits from recurring demand, technological integration, and broad product adoption. Regulatory approvals and clinical guidelines also reinforce hospital reliance on surgical glues.

The ambulatory surgical centers segment is expected to witness the fastest CAGR of 8.7% from 2026 to 2033, fueled by the rising number of outpatient surgeries and minimally invasive procedures. ASCs prefer surgical glues for quick, effective, and suture-less closure, reducing procedure time and patient recovery. Growing adoption in cosmetic, orthopedic, and wound management procedures further supports segment growth. Technological innovations in portable and easy-to-use adhesive systems accelerate uptake.

Europe Surgical Glue Market Regional Analysis

- Europe dominated the Europe Surgical Glue Market with the largest revenue share in 2025, driven by the region’s advanced healthcare infrastructure, widespread adoption of minimally invasive surgical procedures, and the strong presence of major surgical adhesive manufacturers. High surgical volumes across cardiovascular, orthopedic, and general surgeries, along with a growing preference for rapid and effective wound closure solutions, have significantly supported market growth across the region

- Europe also benefits from continuous product innovations, increasing awareness among surgeons regarding advanced wound closure technologies, and ongoing clinical research validating the safety and effectiveness of surgical adhesives, which collectively contribute to the growing demand for surgical glue across hospitals and surgical centers

- Furthermore, collaborations between medical device manufacturers and healthcare institutions for training programs, product demonstrations, and clinical workshops have strengthened surgeon confidence in surgical adhesive technologies, thereby encouraging broader adoption across multiple surgical specialties

U.K. Europe Surgical Glue Market Insight

The U.K. Europe Surgical Glue Market dominated the Europe Surgical Glue Market with the largest revenue share of approximately 38.9% in 2025, supported by advanced healthcare infrastructure, high healthcare expenditure, and the strong presence of leading surgical product manufacturers. The country accounts for a significant share due to the increasing number of surgical procedures and the growing adoption of advanced wound closure technologies across hospitals and outpatient surgical centers. In addition, the expanding use of minimally invasive surgical techniques and increasing focus on improving patient recovery outcomes are further contributing to the growth of the Europe Surgical Glue Market in the U.K.

Germany Europe Surgical Glue Market Insight

The Germany Europe Surgical Glue Market is expected to be the fastest-growing market during the forecast period, registering a CAGR of approximately 7.8%, driven by improving healthcare infrastructure, rising adoption of minimally invasive surgeries, and increasing investments in healthcare innovation. Growing awareness regarding advanced surgical adhesives and their benefits in reducing surgical complications and improving healing outcomes is encouraging their adoption across hospitals, ambulatory surgical centers, and specialty clinics in the country. Additionally, the increasing number of surgical procedures and the presence of advanced healthcare facilities are further supporting the expansion of the Europe Surgical Glue Market in Germany.

Europe Surgical Glue Market Share

The Surgical Glue industry is primarily led by well-established companies, including:

• Baxter International (U.S.)

• Terumo Corporation (Japan)

• Johnson & Johnson (U.S.)

• Medtronic (Ireland)

• H.B. Fuller (U.S.)

• PolyNovo (Australia)

• Arthrex (U.S.)

• GEM Biomedical (France)

• Bioglue (U.S.)

• SyntheMed (U.S.)

• Cohera Medical (U.S.)

• LeMaitre Vascular (U.S.)

• Advanced Medical Solutions (U.K.)

• Hemostasis LLC (U.S.)

• Medline Industries (U.S.)

• Indermil Biotech (Germany)

Latest Developments in Europe Surgical Glue Market

- In July 2021, Baxter International Inc. acquired the PerClot polysaccharide hemostatic system, strengthening its advanced surgical portfolio by adding a highly effective bleeding control product that complements surgical glue and adhesive technologies used during procedures requiring rapid hemostasis

- In February 2023, Advanced Medical Solutions Group plc announced the acquisition of Connexicon Medical Limited, a Dublin‑based tissue adhesive technology specialist, boosting its capabilities in surgical glue solutions, especially cyanoacrylate‑based adhesives used for skin and soft tissue closure

- In August 2023, Johnson & Johnson launched a new generation of absorbable medical glue designed to enhance tissue adhesion and reduce complications during surgery, leveraging advanced polymer technology to improve surgical outcomes across multiple specialties including minimally invasive procedure

- In July 2023, B. Braun Melsungen AG entered into a strategic partnership to co‑develop new absorbable adhesive technology targeting orthopedic surgical applications, combining its surgical product expertise with advanced bioadhesive innovation

- In March 2024, TELA Bio, Inc. launched LIQUIFIX FIX8, the first adhesive‑based product for hernia mesh fixation that eliminates the need for mechanical fasteners, reducing patient discomfort and expanding surgical glue applications into soft tissue reinforcement

- In August 2024, Resivant Medical secured U.S. FDA 510(k) clearance for Cutiva Topical Skin Adhesive and Cutiva PLUS Skin Closure System, representing a major regulatory milestone that brings new advanced sutureless wound closure solutions to clinical practice

- In April 2025, Baxter International launched the Hemopatch Sealing Hemostat with room‑temperature storage, a surgical adhesive designed to improve bleeding control and leak prevention in operative settings with enhanced accessibility

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.