Europe Ultrasound Devices Market

Market Size in USD Billion

USD

3.47 Billion

USD

5.65 Billion

2024

2032

USD

3.47 Billion

USD

5.65 Billion

2024

2032

| 2025 - 2032 | |

| USD 3.47 Billion | |

| USD 5.65 Billion | |

| % | |

|

Ultrasound Devices Market Size

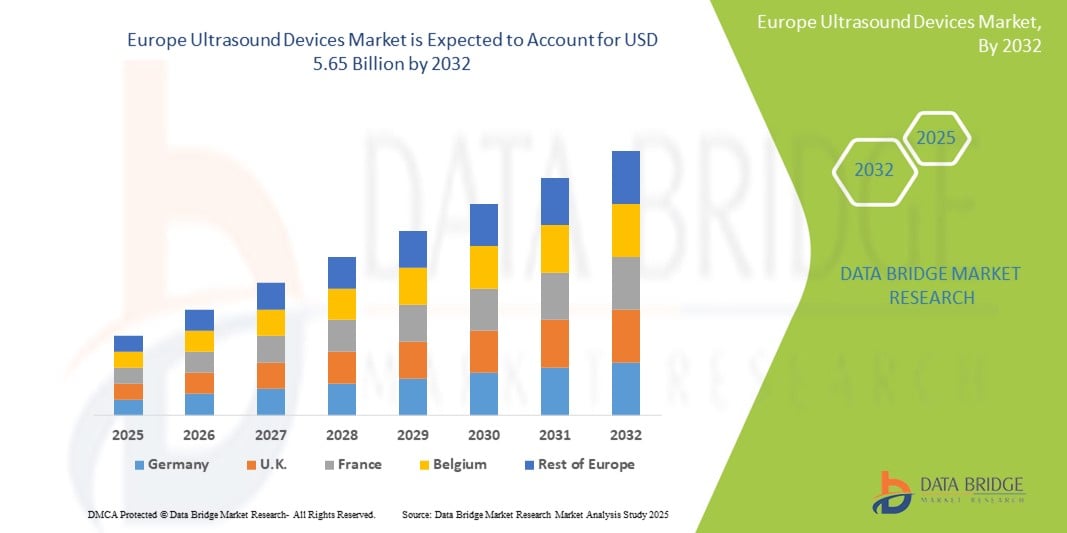

- The Europe Ultrasound Devices market size was valued at USD 3.47 billion in 2024 and is projected to reach USD 5.65 billion by 2032, exhibiting a CAGR of 6.5% during the forecast period of 2025-2032.

- Furthermore, the increasing prevalence of chronic diseases requiring early diagnosis and monitoring, coupled with a growing preference for non-invasive diagnostic procedures, is establishing ultrasound devices as crucial tools in patient care and management.

- These converging factors are accelerating the adoption of ultrasound devices, thereby significantly boosting the industry's growth in the region.

Ultrasound Devices Market Analysis

- Ultrasound devices, offering real-time imaging, non-invasiveness, and portability, are increasingly vital components of modern diagnostic and therapeutic care in various settings due to their ability to facilitate early disease detection, guide procedures, and monitor treatment efficacy.

- The escalating demand for ultrasound devices is primarily fueled by the demographic shift towards an older population, the rising incidence of various medical conditions, and the continuous innovation in device technology offering better clinical outcomes and wider applications.

- U.K. dominates the Ultrasound Devices market with the largest revenue share of 45.25% in 2024, due to well-established healthcare infrastructure, high healthcare expenditure, and the presence of leading medical device manufacturers.

- The Diagnostic Ultrasound Devices segment is expected to dominate the Ultrasound Devices market with a market share of 58.8% in 2025, due to their widespread use in various medical specialties for routine diagnostics and the continuous development of advanced imaging capabilities.

Report Scope and Ultrasound Devices Market Segmentation

|

Attributes |

Ultrasound Devices Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Europe

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Ultrasound Devices Market Trends

“Growing Adoption of Point-of-Care Ultrasound (POCUS)”

- A significant trend in the Europe ultrasound devices market is the increasing preference for point-of-care ultrasound (POCUS). These devices offer benefits such as immediate diagnostic capabilities, reduced patient transfer times, and improved clinical decision-making at the patient’s bedside, leading to increased adoption by various healthcare professionals.

- For instance, advancements in portable and handheld ultrasound devices are expanding the range of conditions that can be diagnosed and monitored in diverse clinical settings, including emergency rooms, intensive care units, and primary care clinics.

- Furthermore, the integration of AI-powered imaging and analysis in ultrasound systems is gaining traction. These systems offer enhanced image quality, automated measurements, and improved diagnostic accuracy, potentially leading to improved patient outcomes and greater efficiency.

- The seamless integration of advanced imaging technologies with electronic health records (EHRs) and telemedicine platforms is also enhancing the accessibility and utility of ultrasound examinations.

Ultrasound Devices Market Dynamics

Driver

“Technological Advancements and Increasing Applications”

- The continuous technological advancements in ultrasound devices, coupled with their expanding range of clinical applications, are significant drivers for the heightened demand in the Europe market.

- For instance, innovations such as 3D/4D imaging, elastography, and contrast-enhanced ultrasound provide more detailed and accurate diagnostic information, leading to improved patient management. Similarly, the growing use of ultrasound in interventional procedures, such as guided biopsies and therapeutic ablations, further expands its utility.

- As the capabilities of ultrasound technology continue to evolve, and its applications become more diverse, the demand for a wide range of ultrasound devices is expected to increase substantially.

- Furthermore, the growing awareness among patients and healthcare professionals regarding the non-invasive nature and versatility of ultrasound examinations is contributing to increased adoption rates.

Restraint/Challenge

“High Cost of Advanced Ultrasound Systems and Skilled Workforce Requirements”

- The relatively high cost of some advanced ultrasound devices, particularly those with cutting-edge technologies like 3D/4D capabilities and integrated AI, can pose a significant challenge to broader market access.

- For instance, the acquisition cost of high-end cart-based ultrasound systems can be substantial, potentially limiting their adoption, especially in smaller healthcare facilities or those with stringent budget constraints. Additionally, the need for highly skilled and trained professionals to operate and interpret complex ultrasound examinations can create a bottleneck in wider adoption, particularly in regions facing a shortage of specialized sonographers and radiologists.

- Addressing these cost and workforce challenges through value-based purchasing models, training programs, and the development of more user-friendly interfaces will be crucial for ensuring wider patient access to advanced ultrasound devices.

- While efforts are underway to improve affordability and address workforce needs, these issues remain significant considerations for market growth.

Ultrasound Devices Market Scope

The market is segmented on the basis of type, portability, application, and end-user.

By Type

On the basis of type, the ultrasound devices market can be segmented into diagnostic ultrasound devices (2D ultrasound, 3D/4D ultrasound, Doppler ultrasound, others) and therapeutic ultrasound devices (High-Intensity Focused Ultrasound (HIFU), Extracorporeal Shockwave Lithotripsy (ESWL), others). The diagnostic ultrasound devices segment dominates the largest market revenue share of 58.8% in 2025 due to their widespread and increasing use in a broad range of diagnostic applications across various medical specialties.

The therapeutic ultrasound devices segment is anticipated to witness the fastest growth rate of 13.7% from 2025 to 2032 due to its non-invasive nature, real-time imaging capabilities, and expanding applications across diverse medical fields. Technological advancements, including AI integration and portable point-of-care systems, are enhancing diagnostic accuracy and accessibility.

By Portability

On the basis of portability, the market is segmented into cart/trolley-based ultrasound devices and compact/handheld ultrasound devices. The cart/trolley-based ultrasound devices segment dominates the largest market revenue share in 2025 due to their increasing adoption in point-of-care settings, emergency medicine, and remote diagnostics, offering enhanced convenience and accessibility.

The compact/handheld ultrasound devices segment is expected to witness the fastest CAGR from 2025 to 2032 due to their portability, ease of use, and affordability. These devices enable point-of-care diagnostics, making ultrasound imaging more accessible in remote or underserved areas.

By Application

On the basis of application, the market is segmented into radiology/general imaging, cardiology, obstetrics/gynecology, point of care (POC), urology, vascular, and others. The radiology/general imaging segment dominates the largest market revenue share in 2025 due to the growing emphasis on immediate diagnosis and intervention across diverse clinical environments, from emergency rooms to remote clinics.

The cardiology segment is expected to witness the fastest CAGR from 2025 to 2032 due to the increasing prevalence of cardiovascular diseases and the demand for non-invasive diagnostic tools. Ultrasound imaging, especially echocardiography, is widely used in assessing heart conditions, including valve disorders, heart failure, and coronary artery disease.

By End-user

On the basis of end-user, the market is segmented into hospitals, diagnostic centers, ambulatory surgical centers, specialty clinics, and others. The hospitals segment dominates the largest market revenue share in 2025 due to the high volume of patient admissions, comprehensive range of diagnostic services, and significant investment in advanced medical equipment.

The diagnostic centers segment is expected to witness the fastest CAGR from 2025 to 2032 due to their ability to offer specialized, accessible, and cost-effective imaging services outside hospital settings. These centers provide shorter wait times, faster reporting, and a wide range of advanced imaging modalities, driving higher patient volumes.

Ultrasound Devices Market Regional Analysis

- The U.K. dominates the Ultrasound Devices market with the largest revenue share of 45.25% in 2024, driven by a large and aging population, high prevalence of chronic diseases, and well-established healthcare infrastructure with favorable reimbursement policies.

- This strong market position is further supported by the presence of major medical device companies and continuous advancements in device technology.

Germany Ultrasound Devices Market Insight

The Germany Ultrasound Devices market captured a significant revenue share within Europe in 2025, driven by an aging population and increasing awareness of the benefits of non-invasive diagnostic imaging. Government initiatives to improve healthcare access and the rising demand for early disease detection are contributing to market expansion.

France Ultrasound Devices Market Insight

The France Ultrasound Devices market captured a notable revenue share within Europe in 2025, due to increasing healthcare expenditure and a growing awareness of advanced diagnostic solutions. The rising incidence of chronic diseases and the need for improved healthcare infrastructure are driving demand for ultrasound devices.

Ultrasound Devices Market Share

The Ultrasound Devices industry is primarily led by well-established companies, including:

- GE Healthcare (U.K.)

- Philips Healthcare (Netherlands)

- Siemens Healthineers (Germany)

- Canon Medical Systems Corporation (Japan)

- Samsung Medison (South Korea)

- Fujifilm Holdings Corporation (Japan)

- Mindray Medical International Limited (China)

- Hitachi, Ltd. (Japan)

- Esaote S.p.A. (Italy)

- Konica Minolta, Inc. (Japan)

- Hologic, Inc. (U.K.)

- Stryker (U.K.)

- Sonosite, Inc. (U.K.)

- Alpinion Medical Systems Co., Ltd. (South Korea)

- BK Medical (U.K.)

Latest Developments in Europe Ultrasound Devices Market

-

In April 2025, a leading medical technology company in Europe announced the launch of a new AI-powered ultrasound system designed to enhance cardiac imaging. This system integrates advanced algorithms for automated ejection fraction measurements and strain analysis, aiming to improve diagnostic accuracy and efficiency for cardiologists.

- In February 2025, a prominent manufacturer received FDA clearance for a new compact, wireless handheld ultrasound device with enhanced image quality for musculoskeletal applications. This development is expected to significantly boost point-of-care diagnostics for sports injuries and orthopedic conditions.

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.