Europe Ultrasound Gels Market

Market Size in USD Billion

USD

28.50 Billion

USD

37.52 Billion

2025

2033

USD

28.50 Billion

USD

37.52 Billion

2025

2033

| 2026 - 2033 | |

| USD 28.50 Billion | |

| USD 37.52 Billion | |

| % | |

|

Europe Ultrasound Gels Market Overview

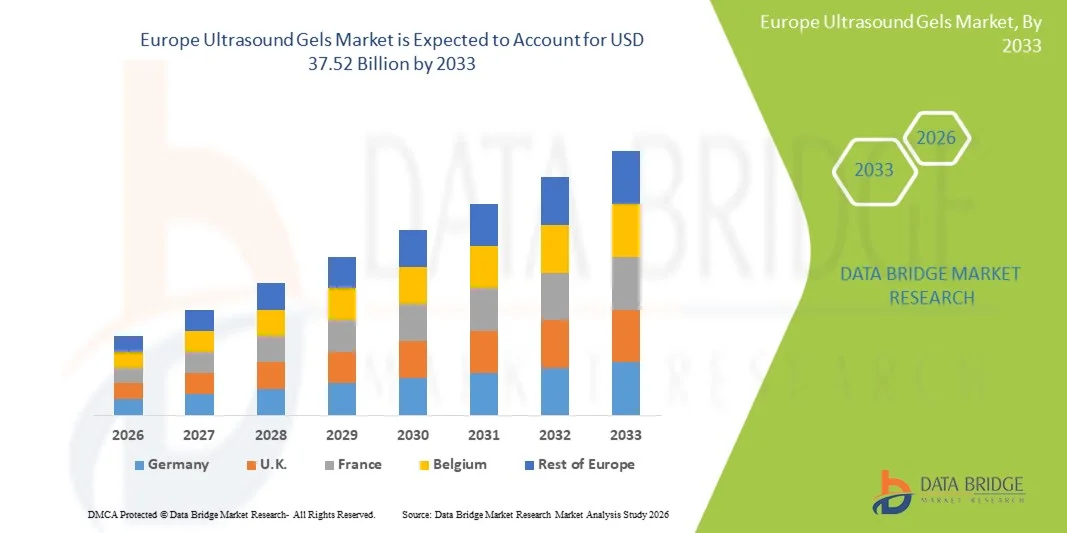

The Europe Ultrasound Gels market was valued at USD 28.50 billion in 2025 and is projected to reach USD 37.52 billion by 2033, growing at a CAGR of 3.50% from 2026 to 2033. The Europe Ultrasound Gels market is experiencing steady growth driven by increasing demand for high-quality diagnostic imaging, rising adoption of ultrasound-based procedures across hospitals and diagnostic centers, and continuous advancements in medical imaging consumables. Growing emphasis on non-invasive, cost-effective, and real-time diagnostic techniques is further accelerating the use of ultrasound gels in clinical applications.

The increasing prevalence of chronic diseases, expanding geriatric population, and rising number of diagnostic imaging procedures across Europe are key factors supporting market expansion. In addition, stringent healthcare quality standards and the growing focus on improving patient comfort and imaging accuracy are encouraging healthcare providers to adopt advanced, hypoallergenic, and high-conductivity ultrasound gels in routine diagnostic workflows.

Key Market Trends & Insights

- The U.K. dominated the Europe Ultrasound Gels market in 2025, driven by advanced NHS imaging networks, high diagnostic ultrasound utilization, and strong presence of well-established hospitals and diagnostic centers.

- The Non-Sterile Ultrasound Gels segment dominated the market with a 64.38% share in 2025, owing to its widespread use in routine diagnostic imaging procedures across hospitals, clinics, and diagnostic centers.

- Germany is expected to be the fastest-growing country in the Europe Ultrasound Gels market during the forecast period, supported by increasing healthcare investments, expansion of diagnostic imaging infrastructure, and rising demand for advanced ultrasound-based procedures.

- The market includes Abdominal Ultrasound, Obstetric Ultrasound, Hysterosonography, Pelvic Ultrasound, Musculoskeletal Ultrasound, Breast Ultrasound, Prostate Ultrasound, Carotid Ultrasound, Venous Ultrasound (Extremities), Scrotal Ultrasound, Thyroid Ultrasound, and Others, with Abdominal Ultrasound and Obstetric Ultrasound among the leading contributors.

- The market is segmented into Hospitals, Clinics, Diagnostic Centers, Ambulatory Surgical Centers, and Others, with Hospitals accounting for the dominant share due to high patient inflow and extensive diagnostic imaging usage.

- The market is segmented into Retail Sales, Online Sales, and Direct Tender, with Direct Tender leading the market due to bulk procurement by hospitals and public healthcare systems.

Market Size & Forecast

- Europe Market Value (2025): USD 28.50 Billion

- Expected Market Value (2033): USD 37.52 Billion

- Forecast CAGR (2026–2033): 3.50%

- Leading Region in 2025: U.K.

- Fastest Growing Region: Germany

Report Scope and Europe Ultrasound Gels Market Segmentation

|

Attributes |

Ultrasound Gels Key Market Insights |

|

Segments Covered |

· By Type: Sterile Ultrasound Gels and Non-Sterile Ultrasound Gels · By Application: Abdominal Ultrasound, Obstetric Ultrasound, Hysterosonography, Pelvic Ultrasound, Musculoskeletal Ultrasound, Breast Ultrasound, Prostate Ultrasound, Carotid Ultrasound, Venous Ultrasound (Extremities), Scrotal Ultrasound, Thyroid Ultrasound, and Others · By End User: Hospitals, Clinics, Diagnostic Centers, Ambulatory Surgical Centers, and Others · By Distribution Channel: Retail Sales, Online Sales, and Direct Tender |

|

Countries Covered |

Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe · |

|

Key Market Players |

· Parker Laboratories Inc. (U.S.) · DCC Healthcare / DCC Vital (Ireland) · Eco-Med Pharmaceutical Inc. (U.K.) · Sonogel Vertriebs GmbH (Germany) · 3M Company (U.S.) · GE HealthCare (U.S.) · Cardinal Health Inc. (U.S.) · B. Braun Melsungen AG (Germany) · Paul Hartmann AG (Germany) · Teleflex Incorporated (U.S.) · Medline Industries, LP (U.S.) · Aspen Surgical Products Inc. (U.S.) · Nissha Medical Technologies (U.S./Europe operations) · Laboratoires Guerbet (France) · Biosynex S.A. (France) · Laboratoire CCD (France) · Ultragel Ltd. (Europe) · MCM Medical (Europe) · GE Medical Systems (Europe division of GE HealthCare) · Dr. Schumacher GmbH (Germany) · Bode Chemie GmbH (Germany) · MediGroup (Europe) · Halyard Health (now part of Owens & Minor, U.S.) · Owens & Minor Inc. (U.S.) · Fresenius Kabi AG (Germany) · Smith & Nephew plc (U.K.) · ConvaTec Group plc (U.K.) · Coloplast A/S (Denmark) · Ambu A/S (Denmark) |

|

Market Opportunities |

· Rising Demand for Diagnostic Imaging Procedures · Expansion of Point-of-Care and Portable Ultrasound Devices · Shift Toward Eco-Friendly and Hypoallergenic Gel Formulations |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, geographically represented company-wise production and capacity, network layouts of distributors and partners, detailed and updated price trend analysis and deficit analysis of supply chain and demand. |

Europe Ultrasound Gels Market Trends

Trend: Rising Demand for Infection Control and Sterile Ultrasound Procedures

The increasing emphasis on infection prevention and patient safety is driving demand for sterile ultrasound gels across healthcare facilities. Sterile gels are being widely adopted for invasive and interventional procedures such as biopsies, vascular access, catheter placements, and surgical ultrasound applications to minimize the risk of cross-contamination. Healthcare organizations and regulatory bodies continue to strengthen infection-control protocols, encouraging the use of single-use sterile gel packets. In addition, growing procedure volumes in emergency departments, operating rooms, and ambulatory surgical centers are supporting the demand for high-quality ultrasound gel products. The trend is further reinforced by rising awareness of healthcare-associated infections (HAIs) and the need for improved diagnostic hygiene standards.

Europe Ultrasound Gels Market Dynamics

Key Market Driver: Growing Utilization of Diagnostic Ultrasound Across Healthcare Settings

The increasing use of ultrasound imaging as a safe, non-invasive, and cost-effective diagnostic tool is a primary driver of the Europe Ultrasound Gels market. Ultrasound procedures are extensively used across abdominal, obstetric, musculoskeletal, breast, thyroid, vascular, and cardiac imaging applications. According to healthcare industry estimates, diagnostic ultrasound examinations continue to account for millions of procedures annually across Europe, supported by aging populations, increasing chronic disease prevalence, and growing demand for point-of-care imaging. The expansion of diagnostic centers, hospital imaging departments, and outpatient care facilities has further accelerated ultrasound procedure volumes, directly increasing the consumption of ultrasound gels required for image transmission and diagnostic accuracy.

Key Restraint/Challenge: Risk of Product Contamination and Availability of Alternative Coupling Technologies

One of the major challenges facing the Europe Ultrasound Gels market is the risk of microbial contamination associated with improperly handled multi-use gel containers. Several healthcare facilities have implemented stricter infection-control measures following reported contamination incidents linked to ultrasound gel products used in invasive procedures. These concerns have increased compliance requirements for manufacturers and healthcare providers, leading to additional costs associated with sterile packaging, quality control, and product monitoring. Furthermore, ongoing research into alternative acoustic coupling materials and advanced dry-coupling ultrasound technologies may limit growth opportunities for conventional gel products in certain specialized applications over the long term.

A notable example is the continued recommendation by healthcare authorities and infection-control organizations for the use of sterile ultrasound gel during invasive procedures and for patients with compromised immune systems, highlighting the operational and regulatory challenges associated with product safety and contamination prevention.

Key Market Opportunity: Expansion of Point-of-Care Ultrasound (POCUS) and Portable Imaging Systems

The rapid adoption of point-of-care ultrasound (POCUS) presents a significant growth opportunity for the Europe Ultrasound Gels market. Portable and handheld ultrasound devices are increasingly being deployed in emergency medicine, intensive care units, primary care clinics, ambulatory settings, and home healthcare environments. The growing availability of compact ultrasound systems from leading medical imaging manufacturers has expanded access to real-time diagnostics beyond traditional radiology departments. As healthcare providers continue to invest in decentralized and bedside diagnostic solutions, demand for convenient, sterile, and single-use ultrasound gel products is expected to increase. In addition, advancements in gel formulations offering improved acoustic transmission, skin compatibility, and ease of cleaning are creating new opportunities for manufacturers across hospitals, clinics, and diagnostic centers throughout Europe.

Europe Ultrasound Gels Market Scope

The Ultrasound Gels market is segmented on the basis of type, application, end user, and distribution channel.

- By Type

On the basis of type, the Europe Ultrasound Gels market is segmented into sterile ultrasound gels and non-sterile ultrasound gels. The Non-Sterile Ultrasound Gels segment dominated the market with a 64.38% share in 2025, owing to its widespread use in routine diagnostic imaging procedures across hospitals, clinics, and diagnostic centers. These gels are preferred due to their cost-effectiveness, easy availability, and compatibility with a broad range of ultrasound examinations. The segment benefits from the increasing number of abdominal, musculoskeletal, vascular, and thyroid ultrasound procedures performed annually across Europe. Non-sterile gels offer efficient acoustic coupling and are suitable for high-volume imaging environments where invasive procedures are not required. Growing healthcare expenditure, expanding diagnostic infrastructure, and rising demand for early disease detection are further supporting adoption. In addition, the availability of various viscosity grades and packaging formats enhances operational convenience for healthcare professionals. The segment continues to benefit from the increasing use of portable and point-of-care ultrasound systems across healthcare settings, reinforcing its leading market position.

The Sterile Ultrasound Gels segment is projected to register the fastest CAGR of 6.8% from 2026 to 2033, driven by increasing demand for infection control and patient safety during invasive and interventional ultrasound procedures. Rising utilization in catheter placements, biopsies, surgical imaging, and obstetric applications is accelerating segment growth. Healthcare facilities are increasingly adopting sterile products to comply with stringent hygiene regulations and reduce the risk of healthcare-associated infections. Growing awareness regarding contamination risks associated with reusable products is further supporting demand. In addition, advancements in single-use packaging formats and preservative-free formulations are improving product acceptance. Expanding surgical volumes, increasing hospitalization rates, and rising adoption of minimally invasive procedures are contributing significantly to market expansion. The growing focus on premium-quality medical consumables and regulatory compliance is expected to further drive the uptake of sterile ultrasound gels across Europe.

- By Application

On the basis of application, the Europe Ultrasound Gels market is segmented into abdominal ultrasound, obstetric ultrasound, hysterosonography, pelvic ultrasound, musculoskeletal ultrasound, breast ultrasound, prostate ultrasound, carotid ultrasound, venous ultrasound (extremities), scrotal ultrasound, thyroid ultrasound, and others. The Abdominal Ultrasound segment dominated the market with a 28.91% share in 2025, driven by its extensive use in the diagnosis of liver disorders, kidney diseases, gallbladder conditions, gastrointestinal abnormalities, and other internal organ assessments. The increasing prevalence of chronic diseases and growing emphasis on preventive healthcare have significantly increased the number of abdominal imaging procedures performed across Europe. Abdominal ultrasound remains one of the most commonly prescribed diagnostic tests due to its non-invasive nature, affordability, and real-time imaging capabilities. Rising healthcare accessibility and advancements in imaging technologies are further enhancing procedural volumes. The segment also benefits from routine screening programs and increasing adoption in emergency care settings. Continuous demand from hospitals and diagnostic centers reinforces its dominant position in the market.

The Obstetric Ultrasound segment is expected to witness the fastest CAGR of 7.1% from 2026 to 2033, driven by growing awareness regarding prenatal care and fetal health monitoring. Increasing birth rates in several European countries and expanding maternal healthcare programs are contributing to higher demand for obstetric imaging procedures. Technological advancements in 3D and 4D ultrasound systems are enhancing diagnostic accuracy and improving patient experiences. Rising government initiatives focused on maternal and child health are encouraging regular prenatal screenings. In addition, increasing healthcare spending and improved access to specialized obstetric care are supporting market growth. The segment is also benefiting from rising demand for early detection of fetal abnormalities and pregnancy-related complications. Growing adoption of advanced ultrasound equipment in both public and private healthcare facilities is expected to sustain strong growth throughout the forecast period.

- By End User

On the basis of end user, the Europe Ultrasound Gels market is segmented into hospitals, clinics, diagnostic centers, ambulatory surgical centers, and others. The Hospitals segment dominated the market with a 46.72% share in 2025 due to the large volume of diagnostic and therapeutic ultrasound procedures performed within hospital settings. Hospitals possess advanced imaging infrastructure and skilled healthcare professionals, enabling extensive utilization of ultrasound technologies across radiology, cardiology, obstetrics, emergency medicine, and surgical departments. The increasing number of patient admissions and rising prevalence of chronic diseases continue to drive demand for ultrasound examinations. Hospitals also serve as primary centers for complex and specialized diagnostic procedures requiring high-quality imaging consumables. Strong procurement capabilities and long-term supply contracts further support market dominance. In addition, growing investments in healthcare infrastructure and technological modernization across Europe are reinforcing the segment's leadership position.

The Diagnostic Centers segment is anticipated to witness the fastest CAGR of 6.9% from 2026 to 2033, driven by the increasing preference for specialized outpatient imaging services. Diagnostic centers offer cost-effective, efficient, and rapid imaging solutions, attracting a growing patient population. The expansion of independent diagnostic chains and imaging networks across urban and semi-urban regions is significantly contributing to growth. Increasing adoption of advanced ultrasound technologies and rising demand for preventive health screenings are further supporting market expansion. Diagnostic centers are also benefiting from shorter waiting times and improved accessibility compared to large hospitals. Growing healthcare awareness and the rising burden of chronic diseases are increasing the number of imaging referrals. Furthermore, strategic investments in modern diagnostic equipment and digital healthcare solutions are expected to accelerate segment growth during the forecast period.

- By Distribution Channel

On the basis of distribution channel, the Europe Ultrasound Gels market is segmented into retail sales, online sales, and direct tender. The Direct Tender segment dominated the market with a 52.14% share in 2025, owing to extensive procurement by hospitals, government healthcare institutions, and large diagnostic laboratory networks. Direct tender contracts enable healthcare providers to secure bulk purchases at competitive prices while ensuring consistent product availability. This channel remains highly preferred for institutional procurement due to streamlined purchasing processes and long-term supplier relationships. Increasing public healthcare spending and centralized procurement systems across several European countries further support segment growth. Direct tenders also help maintain quality standards and regulatory compliance for medical consumables. The growing number of healthcare facilities and imaging centers requiring large-volume supplies continues to reinforce the segment's leading market position. In addition, strong relationships between manufacturers and healthcare organizations contribute to sustained demand through this channel.

The Online Sales segment is projected to register the fastest CAGR of 7.3% from 2026 to 2033, driven by the rapid digitalization of healthcare procurement processes and increasing adoption of e-commerce platforms for medical supplies. Healthcare providers are increasingly utilizing online channels due to convenience, wider product availability, competitive pricing, and faster delivery services. Small clinics, diagnostic centers, and independent healthcare professionals are particularly benefiting from streamlined online purchasing options. Growing internet penetration and improvements in digital healthcare infrastructure are further supporting adoption. Online platforms also provide easy access to product information, reviews, and comparison tools, facilitating informed purchasing decisions. Expanding B2B healthcare marketplaces and direct manufacturer-to-customer sales models are creating new growth opportunities. The increasing acceptance of digital procurement solutions is expected to drive strong expansion of the online sales segment throughout the forecast period.

Europe Ultrasound Gels Market Regional Analysis

The Europe Ultrasound Gels market remains a significant contributor to the global market, driven by the region’s well-established healthcare infrastructure, increasing diagnostic imaging volumes, and growing adoption of ultrasound-based procedures across hospitals, clinics, and diagnostic centers. Rising prevalence of chronic diseases, expanding elderly population, and increasing preference for non-invasive diagnostic techniques continue to support market growth. Furthermore, ongoing investments in healthcare modernization, infection-control standards, and advanced imaging technologies are driving consistent demand for both sterile and non-sterile ultrasound gels across Europe.

U.K. Ultrasound Gels Market Insight

The U.K. dominated the Europe Ultrasound Gels market in 2025, driven by advanced NHS imaging networks, high diagnostic ultrasound utilization, and a strong presence of well-established hospitals and diagnostic centers. The increasing number of ultrasound examinations performed for abdominal, obstetric, vascular, and musculoskeletal diagnostics continues to support demand for ultrasound gels across healthcare settings. Additionally, government investments in diagnostic capacity expansion, growing adoption of point-of-care ultrasound (POCUS), and increasing focus on early disease detection are further contributing to market growth in the country.

Germany Ultrasound Gels Market Insight

Germany is expected to be the fastest-growing country in the Europe Ultrasound Gels market during the forecast period, supported by increasing healthcare investments, expansion of diagnostic imaging infrastructure, and rising demand for advanced ultrasound-based procedures. The country’s growing emphasis on preventive healthcare, expanding network of hospitals and diagnostic centers, and increasing adoption of portable and high-resolution ultrasound systems are accelerating ultrasound gel consumption. Furthermore, advancements in medical imaging technologies, rising outpatient diagnostic procedures, and continuous healthcare modernization initiatives are expected to strengthen market growth in Germany over the coming years.

Europe Ultrasound Gels Market Share

The Ultrasound Gels industry is primarily led by well-established companies, including:

- Parker Laboratories Inc. (U.S.)

- DCC Healthcare / DCC Vital (Ireland)

- Eco-Med Pharmaceutical Inc. (U.K.)

- Sonogel Vertriebs GmbH (Germany)

- 3M Company (U.S.)

- GE HealthCare (U.S.)

- Cardinal Health Inc. (U.S.)

- B. Braun Melsungen AG (Germany)

- Paul Hartmann AG (Germany)

- Teleflex Incorporated (U.S.)

- Medline Industries, LP (U.S.)

- Aspen Surgical Products Inc. (U.S.)

- Nissha Medical Technologies (U.S./Europe operations)

- Laboratoires Guerbet (France)

- Biosynex S.A. (France)

- Laboratoire CCD (France)

- Ultragel Ltd. (Europe)

- MCM Medical (Europe)

- GE Medical Systems (Europe division of GE HealthCare)

- Dr. Schumacher GmbH (Germany)

- Bode Chemie GmbH (Germany)

- MediGroup (Europe)

- Halyard Health (now part of Owens & Minor, U.S.)

- Owens & Minor Inc. (U.S.)

- Fresenius Kabi AG (Germany)

- Smith & Nephew plc (U.K.)

- ConvaTec Group plc (U.K.)

- Coloplast A/S (Denmark)

- Ambu A/S (Denmark)

Latest Developments in Europe Ultrasound Gels Market

- In June 2023, Parker Laboratories Inc., a leading manufacturer of ultrasound gels and medical imaging consumables, announced that the U.S. FDA granted De Novo clearance for Tristel ULT, a high-level disinfectant foam designed for ultrasound probes used in body cavities and on skin-surface transducers. The product provides rapid and effective disinfection while improving patient safety and workflow efficiency in ultrasound departments. This development strengthened Parker Laboratories’ ultrasound product portfolio and highlighted the industry's growing focus on infection prevention and probe hygiene

- In September 2023, Parker Laboratories Inc. announced the launch of the UltraDrape® II UGPIV Barrier and Securement Dressing, a next-generation solution designed for ultrasound-guided peripheral intravenous (UGPIV) procedures. The product was developed to improve patient safety, reduce contamination risks, and enhance procedural efficiency in emergency and clinical settings. This launch reflects the increasing emphasis on sterile ultrasound procedures and advanced consumables supporting ultrasound-guided interventions

- In October 2023, Parker Laboratories Inc. commercially launched Tristel ULT™ in the U.S. market following regulatory clearance. The disinfectant foam was introduced as an innovative solution for high-level disinfection of ultrasound probes, offering healthcare facilities a faster and more cost-effective alternative to conventional disinfection systems. The launch underscored the growing demand for infection-control solutions associated with ultrasound imaging procedures

- In April 2024, Parker Laboratories supported the introduction of a new Ultrasound IV Training Program that received the first-ever Seal of Approval from the Infusion Nurses Society (INS). The program was developed to improve clinician competency in ultrasound-guided vascular access procedures and promote best practices in ultrasound utilization. This development highlighted the industry's increasing focus on ultrasound training, procedural accuracy, and patient safety

- In May 2024, Parker Laboratories introduced the Tristel 3T Digital Track & Traceability Platform for ultrasound probe disinfection management. The platform enables healthcare providers to digitally monitor and document ultrasound transducer disinfection processes, helping facilities improve compliance, traceability, and infection-control standards. This development reflects the growing integration of digital technologies into ultrasound workflow management

- In September 2024, Parker Laboratories presented new patient-safety initiatives focused on aseptic techniques and ultrasound probe disinfection during ultrasound-guided procedures. The initiative emphasized the use of sterile barriers, disinfectants, and infection-prevention protocols to improve clinical outcomes and reduce contamination risks. This development demonstrates the industry's increasing investment in advanced ultrasound consumables and safety-focused solutions

- In February 2025, Parker Laboratories highlighted the inclusion of chlorine dioxide-based disinfection technology in updated healthcare sterilant and high-level disinfectant standards. The company's Tristel ULT platform was positioned as an efficient solution for ultrasound transducer disinfection, supporting healthcare providers in meeting evolving regulatory and infection-control requirements. This development reflects the growing importance of advanced hygiene solutions within the ultrasound ecosystem

- In June 2025, Parker Laboratories showcased its comprehensive ultrasound infection-prevention portfolio, including Aquasonic 100 single-use gel packettes, UltraDrape sterile barrier products, and Tristel ULT disinfectant solutions. The company emphasized improving patient safety, procedural efficiency, and infection-control practices across ultrasound imaging environments. This development highlights continued innovation in ultrasound gels, sterile consumables, and supporting ultrasound accessories

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.