Europe Vaccine Administration Devices Market

Market Size in USD Billion

USD

1.08 Billion

USD

2.00 Billion

2024

2032

USD

1.08 Billion

USD

2.00 Billion

2024

2032

| 2025 - 2032 | |

| USD 1.08 Billion | |

| USD 2.00 Billion | |

| % | |

|

Europe Vaccine Administration Devices Market Size

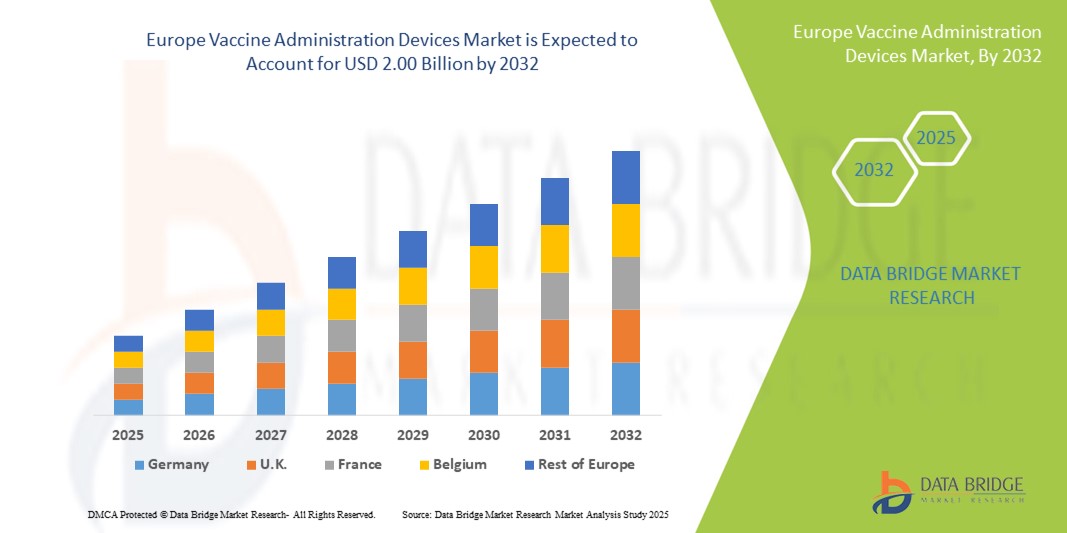

- The Europe vaccine administration devices market size was valued at USD 1.08 billion in 2024 and is expected to reach USD 2.00 billion by 2032, at a CAGR of 8.00% during the forecast period

- The market growth is largely fueled by rising prevalence of chronic diseases, increasing demand for COVID-19 vaccines, and substantial investments in vaccine research and development, driving adoption of efficient vaccine delivery systems across healthcare settings

- Furthermore, technological advancements such as needle-free injectors, microneedles, and auto-injectors are improving the efficiency, safety, and patient comfort of vaccine administration, positioning these devices as preferred solutions in modern immunization programs and accelerating market growth

Europe Vaccine Administration Devices Market Analysis

- Vaccine administration devices, including auto-injectors, jet injectors, microneedles, and inhalation delivery systems, are increasingly vital components of Europe’s immunization programs due to their ability to improve safety, efficiency, and patient compliance across hospitals, clinics, and mass vaccination campaigns

- The escalating demand for vaccine administration devices is primarily fueled by the rising prevalence of infectious diseases, increasing government immunization initiatives, and growing investments in vaccine research and development

- Germany dominated the Europe vaccine administration devices market with the largest revenue share of 29.5% in 2024, supported by robust healthcare infrastructure, strong public health programs, and early adoption of advanced vaccine delivery technologies

- Poland is expected to be the fastest-growing country in the Europe vaccine administration devices market during the forecast period, driven by increasing vaccination coverage, expanding healthcare infrastructure, and rising adoption of auto-injector devices

- Auto-injector segment dominated the Europe vaccine administration devices market with a market share of 43% in 2024, driven by ease of use, patient compliance, and suitability for both routine and mass vaccination programs

Report Scope and Europe Vaccine Administration Devices Market Segmentation

|

Attributes |

Europe Vaccine Administration Devices Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Europe

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Europe Vaccine Administration Devices Market Trends

Growing Adoption of Auto-Injectors and Needle-Free Delivery Systems

- A significant and accelerating trend in the Europe vaccine administration devices market is the rising adoption of auto-injectors, jet injectors, and needle-free systems, which improve patient compliance and ease of vaccine delivery across hospitals, clinics, and homecare settings

- For instance, the BD Uniject auto-disable pre-filled injection system allows healthcare workers to deliver vaccines safely and efficiently without requiring complex preparation, minimizing errors in dose administration

- Innovations in needle-free and microneedle-based devices are enabling pain-free administration, reducing needle-stick injuries, and facilitating rapid mass vaccination programs in Europe

- These devices are increasingly integrated with digital monitoring tools that track vaccine usage and adherence, helping healthcare providers manage immunization campaigns more effectively

- The trend toward more convenient, safe, and patient-friendly vaccine administration devices is reshaping user expectations, prompting manufacturers such as Gx InnoSafe to develop advanced auto-injectors and microneedle systems with enhanced safety and usability

- The demand for devices that combine precision, safety, and ease of use is growing rapidly across hospitals, community health centers, and homecare settings, driven by both routine immunization programs and pandemic preparedness initiatives

Europe Vaccine Administration Devices Market Dynamics

Driver

Rising Need Due to Increasing Vaccination Programs and Public Health Initiatives

- The growing emphasis on immunization programs and preventive healthcare across Europe is a major driver for the increasing adoption of advanced vaccine administration devices

- For instance, Poland’s national vaccination campaigns have accelerated the use of auto-injectors and needle-free devices to ensure safe and efficient vaccine delivery to large populations

- The need to reduce errors in vaccine administration, improve patient comfort, and enhance compliance is pushing healthcare providers toward auto-injectors, jet injectors, and microneedle-based systems

- The rising prevalence of infectious diseases and ongoing pandemic preparedness initiatives further fuels the demand for reliable, user-friendly vaccine administration devices

- Ease of use, consistent dose delivery, and compatibility with multiple vaccine types are key factors propelling adoption across hospitals, clinics, and mass immunization centers, making these devices integral to modern healthcare infrastructure

- Digital integration with healthcare monitoring platforms and patient tracking systems adds value to these devices, supporting their widespread acceptance in Europe’s public health programs

Restraint/Challenge

High Cost and Regulatory Compliance Barriers

- The relatively high cost of advanced vaccine administration devices, including auto-injectors and jet injectors, can be a barrier to adoption, especially in budget-constrained healthcare facilities

- For instance, premium auto-injector systems with integrated monitoring features have a higher price point compared to traditional syringes, limiting their use in smaller clinics or community centers

- Regulatory compliance across multiple European countries poses challenges for manufacturers, requiring rigorous testing, approvals, and adherence to safety standards before market entry

- Delays in obtaining certifications and meeting country-specific requirements can slow down product launches and limit market penetration

- Concerns about device usability, training requirements for healthcare staff, and the need for safe disposal of single-use devices can further restrain adoption

- Overcoming these challenges through cost-effective device design, harmonized regulatory pathways, and staff training initiatives is essential for sustained growth of the Europe vaccine administration devices market

Europe Vaccine Administration Devices Market Scope

The market is segmented on the basis of product, route of administration, type, brand, dosage, vaccine type, modality, usability, end user, and distribution channel.

- By Product

On the basis of product, the Europe vaccine administration devices market is segmented into syringes, auto-injectors, jet injectors, microneedles, inhalation/pulmonary delivery, microinjection system, pen injector devices, biodegradable implants, electroporation-based needle-free injection systems, buccal/sublingual vaccine delivery systems, auto-injector trainer devices, and other devices. The auto-injector segment dominated the market with a revenue share of 43% in 2024, driven by its ease of use, accurate dose delivery, and suitability for both routine and mass vaccination programs. Auto-injectors reduce administration errors and improve patient compliance, making them highly preferred in hospitals and community centers. They are often integrated with digital monitoring systems to track vaccine usage and adherence. The convenience of self-administration in homecare settings further boosts demand. Manufacturers continue to innovate ergonomic designs and combination devices for multiple vaccines. These factors collectively reinforce the segment’s market dominance across Europe.

The microneedle segment is anticipated to witness the fastest growth from 2025 to 2032, fueled by increasing demand for pain-free vaccine delivery and minimally invasive methods. Microneedle patches reduce needle-stick injuries and biohazard waste, making them highly attractive for mass immunization campaigns. They are gaining adoption in research and clinical trials for vaccines such as influenza and pneumococcal conjugate vaccines. Enhanced patient compliance, particularly among children and needle-averse populations, is driving market uptake. Ongoing R&D and the launch of innovative microneedle devices across Europe are expected to accelerate growth further. The compact form factor and potential for self-administration also support their rising popularity.

- By Route of Administration

On the basis of route of administration, the Europe vaccine administration devices market is segmented into intramuscular, subcutaneous, and intradermal. The intramuscular segment dominated the market in 2024, accounting for the majority of revenue due to its compatibility with most marketed vaccines and established protocols in hospitals and vaccination centers. Intramuscular devices allow precise and rapid delivery of vaccines, ensuring optimal immune response. The segment benefits from extensive use in mass immunization programs and public health campaigns. In addition, the availability of auto-injectors and pre-filled syringes designed for intramuscular delivery strengthens market dominance. Healthcare providers prefer intramuscular administration due to familiarity, training, and regulatory acceptance. This segment remains the backbone of routine immunization in Europe.

The intradermal segment is expected to be the fastest growing from 2025 to 2032, driven by its ability to use lower vaccine doses while eliciting sufficient immunogenic response. Intradermal devices, including microneedles and microinjection systems, are increasingly adopted for influenza, BCG, and emerging vaccine candidates. The growth is further supported by research initiatives and pilot immunization programs across Europe. Intradermal delivery is particularly attractive for pandemic preparedness and cost-effective vaccine administration. Its minimal invasiveness improves patient comfort and compliance. The segment’s expansion is expected to continue with innovations in device technology.

- By Type

On the basis of type, the Europe vaccine administration devices market is segmented into marketed vaccines and clinical-stage vaccines (electroporation). The marketed vaccines segment dominated the market in 2024, holding the largest revenue share due to widespread adoption in routine immunization programs and established regulatory approvals. Hospitals, clinics, and public health authorities rely heavily on marketed vaccines delivered via auto-injectors and pre-filled syringes for reliable administration. The segment benefits from consistent demand for seasonal vaccines, such as influenza, and combination vaccines such as DTP-HEPB-HIB. Devices optimized for marketed vaccines enhance efficiency and reduce errors. Strong supply chains and government procurement programs further reinforce dominance. Marketed vaccines remain the primary driver for device sales across Europe.

The clinical-stage vaccines segment is expected to witness the fastest growth from 2025 to 2032, driven by increasing clinical trials and R&D initiatives for novel vaccines, including electroporation-based delivery. Expanding research activities across Europe for COVID-19, influenza, and emerging infectious diseases are boosting demand for specialized administration devices. Clinical-stage vaccines often require precise dosage delivery, making auto-injectors and needle-free systems critical. Collaboration between biotech firms and device manufacturers is accelerating adoption. Rising investments in vaccine innovation are driving market expansion. Early adoption of advanced delivery technologies positions this segment for rapid growth.

- By Brand

On the basis of brand, the Europe vaccine administration devices market is segmented into BD Accuspray Nasal Spray System, BD Hypak for Vaccines Glass Pre-Fillable Syringe System, BD Uniject Auto-Disable Pre-Fillable Injection System, Gx InnoSafe, Gx RTF ClearJect, Plajex, and others. The BD Uniject Auto-Disable Pre-Fillable Injection System dominated the market in 2024 due to its high safety standards, ease of use, and wide adoption in public vaccination programs. Its pre-filled, auto-disable mechanism prevents reuse and enhances immunization safety. Hospitals and community centers prefer it for consistent and reliable delivery. Regulatory approvals and strong brand reputation reinforce dominance. Integration with digital tracking systems improves adherence and efficiency. The device’s widespread use in mass immunization campaigns solidifies its leading position.

The Gx InnoSafe brand is anticipated to witness the fastest growth, driven by innovations such as ergonomic design, needle-free options, and compatibility with multiple vaccines. Adoption is increasing in emerging European markets and clinical trial settings. Its ease of use and patient-friendly design make it attractive for both healthcare providers and homecare settings. Strategic partnerships with public health agencies accelerate penetration. Ongoing product launches and promotional initiatives support rapid revenue growth. Gx InnoSafe’s flexibility and technological advancements position it for strong market expansion.

- By Dosage

On the basis of dosage, the Europe vaccine administration devices market is segmented into fixed and variable. The fixed dosage segment dominated the market in 2024, holding the largest revenue share due to standardized vaccine delivery protocols and regulatory acceptance. Fixed dosage devices minimize administration errors and simplify training requirements for healthcare staff. They are widely used in hospitals, clinics, and mass immunization programs for both routine and seasonal vaccines. Auto-injectors and pre-filled syringes commonly feature fixed dosages for efficiency and safety. Regulatory compliance and ease of inventory management further support market dominance. Fixed dosage ensures consistency in immunogenic response across patient populations.

The variable dosage segment is expected to witness the fastest growth from 2025 to 2032, driven by demand for personalized vaccination strategies and emerging clinical applications. Variable dosage devices allow precise adjustment based on age, weight, or clinical condition, increasing flexibility in vaccine administration. Adoption is rising in research centers and specialized healthcare facilities. Variable dosage devices also support combination vaccines and multi-dose regimens, enhancing versatility. Increasing awareness of patient-specific dosing requirements is fueling growth. Manufacturers are innovating to improve ease of use and accuracy, further accelerating market adoption.

- By Vaccine Type

On the basis of vaccine type, the Europe vaccine administration devices market is segmented into bivalent oral polio vaccine, BCG vaccine, tetanus-diphtheria vaccine, DTP-HEPB-HIB vaccine, influenza vaccine, pneumococcal conjugate vaccine, measles vaccine, and others. The influenza vaccine segment dominated the market in 2024 due to high seasonal demand and widespread immunization campaigns. Hospitals and community centers rely on auto-injectors and pre-filled syringes to deliver influenza vaccines efficiently. Public health authorities prioritize influenza vaccination programs for both children and adults. Consistent demand ensures continuous utilization of administration devices. Integration with digital monitoring systems enhances tracking and reporting. Influenza vaccines remain a major revenue driver for the device market.

The pneumococcal conjugate vaccine segment is expected to witness the fastest growth from 2025 to 2032, driven by increasing awareness of respiratory infections and preventive healthcare. Adoption is rising in both routine immunization and special vaccination programs for at-risk populations. Advanced administration devices such as auto-injectors and microneedle patches enhance compliance and reduce errors. Growing pediatric vaccination programs across Europe support growth. Manufacturers are expanding device compatibility for multi-dose and combination vaccines. Technological innovations in delivery systems are accelerating adoption for this vaccine type.

- By Modality

On the basis of modality, the Europe vaccine administration devices market is segmented into automatic vaccine administration devices and manual vaccine administration devices. The automatic vaccine administration devices segment dominated the market in 2024, driven by the convenience, accuracy, and reduced risk of administration errors. These devices, including auto-injectors and needle-free systems, allow precise and consistent delivery, making them highly preferred in hospitals, clinics, and mass vaccination programs. Automation reduces the burden on healthcare staff and enhances operational efficiency. Integration with digital tracking and monitoring systems further supports widespread adoption. Automatic devices also improve patient compliance and safety, reinforcing their market leadership. Regulatory acceptance and proven efficacy across multiple vaccine types solidify dominance.

The manual vaccine administration devices segment is expected to witness the fastest growth from 2025 to 2032, driven by cost-effectiveness and adoption in smaller clinics and community health centers. Manual devices, such as traditional syringes and pen injector systems, are widely used in emerging European markets. Healthcare professionals value manual devices for flexibility in administering different vaccine types. Increasing training programs and awareness campaigns enhance their adoption. The segment benefits from compatibility with both marketed and clinical-stage vaccines. Innovations in ergonomic and safety-enhanced manual devices further accelerate growth opportunities.

- By Usability

On the basis of usability, the Europe vaccine administration devices market is segmented into disposable and reusable devices. The disposable segment dominated the market in 2024, holding the largest revenue share due to its superior safety, ease of use, and prevention of cross-contamination. Disposable auto-injectors and pre-filled syringes are widely used in hospitals, community centers, and mass vaccination campaigns. Single-use devices simplify logistics and inventory management. Regulatory guidelines favor disposable systems for routine immunization programs. Widespread adoption of disposable devices ensures compliance with hygiene standards. The convenience of disposables supports patient and provider preference, reinforcing dominance.

The reusable segment is expected to witness the fastest growth from 2025 to 2032, driven by the growing demand for cost-effective devices in research institutes, academic centers, and specialized healthcare facilities. Reusable devices, including multi-dose pen injectors and microinjection systems, allow flexible dosing and reduce long-term operational costs. Expansion of training programs and laboratory applications enhances adoption. Reusable devices are gaining traction for clinical-stage vaccine administration. Innovations in sterilization and safety mechanisms increase usability and reliability. Rising awareness of sustainability and resource efficiency supports this segment’s growth.

- By End User

On the basis of end user, the Europe vaccine administration devices market is segmented into hospitals, community centers, homecare settings, research and academic institutes, ambulatory surgical centers, and others. The hospitals segment dominated the market in 2024, accounting for the largest revenue share due to the concentration of routine immunization programs, skilled staff, and high patient volumes. Hospitals extensively use auto-injectors, pre-filled syringes, and needle-free devices for a wide range of vaccines. Institutional preference for standardized, safe, and efficient devices further supports dominance. Integration with hospital information systems enables better tracking and inventory management. Regulatory compliance in hospital settings reinforces device adoption. Hospitals remain the backbone for vaccine administration across Europe.

The homecare setting segment is expected to witness the fastest growth from 2025 to 2032, driven by increasing demand for self-administration, patient convenience, and aging populations requiring at-home immunization. Auto-injectors and easy-to-use devices support home-based vaccination programs. Telehealth initiatives and digital monitoring tools enhance adoption in homecare settings. Rising awareness among patients about vaccine accessibility fuels growth. Innovative device designs, including ergonomic and compact options, facilitate self-administration. Homecare adoption is further supported by healthcare policies promoting outpatient care and decentralized vaccination programs.

- By Distribution Channel

On the basis of distribution channel, the Europe vaccine administration devices market is segmented into direct tender and retail sales. The direct tender segment dominated the market in 2024, capturing the largest revenue share due to widespread government procurement and institutional purchasing for hospitals, community centers, and public health programs. Bulk tenders ensure consistent supply, regulatory compliance, and cost efficiency. Direct tender channels are preferred for large-scale immunization campaigns and seasonal vaccine distribution. Strong partnerships between device manufacturers and public health authorities reinforce dominance. The segment ensures reliable logistics and inventory management for critical vaccine programs. High adoption in routine and pandemic preparedness initiatives supports sustained market leadership.

The retail sales segment is expected to witness the fastest growth from 2025 to 2032, fueled by rising demand for at-home vaccination devices, patient self-administration, and over-the-counter availability of certain vaccines. Retail channels offer convenience, accessibility, and flexibility for end users. Expansion of homecare services and online pharmacies further supports growth. Innovative, easy-to-use devices such as auto-injectors and microneedle patches enhance adoption through retail. Digital platforms and e-commerce integration are increasing penetration. Growing awareness of vaccination and preventive healthcare among consumers accelerates retail channel expansion.

Europe Vaccine Administration Devices Market Regional Analysis

- Germany dominated the Europe vaccine administration devices market with the largest revenue share of 29.5% in 2024, supported by robust healthcare infrastructure, strong public health programs, and early adoption of advanced vaccine delivery technologies

- Healthcare providers in the region prioritize devices that improve safety, accuracy, and patient compliance, such as auto-injectors, pre-filled syringes, and needle-free systems, which are widely used in hospitals, community centers, and homecare settings

- This widespread adoption is further supported by strong public health initiatives, government funding for vaccination programs, and high awareness of preventive healthcare, establishing advanced vaccine administration devices as a preferred solution for both routine and mass immunization campaigns

The Germany Vaccine Administration Devices Market Insight

The Germany vaccine administration devices market dominated the Europe market with the largest revenue share of 29.5% in 2024, driven by robust healthcare infrastructure, well-established vaccination programs, and high adoption of advanced delivery technologies. Hospitals, research institutes, and community centers widely use auto-injectors, pre-filled syringes, and needle-free systems for both routine and mass immunization. The country emphasizes patient safety, efficiency, and regulatory compliance, encouraging the use of technologically advanced devices. Integration with digital monitoring and tracking systems enhances workflow and vaccine coverage. Growing awareness of preventive healthcare and adoption of homecare vaccination programs further drive market expansion. Germany’s focus on innovation, quality standards, and government-backed immunization campaigns positions it as the key market leader in Europe.

U.K. Vaccine Administration Devices Market Insight

The U.K. vaccine administration devices market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by rising vaccination campaigns and increasing demand for patient-friendly delivery systems. The adoption of auto-injectors, pre-filled syringes, and microneedle patches is accelerating due to their ease of use and accuracy. Public health authorities emphasize safe and efficient vaccine administration, supporting widespread market penetration. Integration with digital health platforms for tracking and compliance adds value to healthcare providers. Increasing urbanization, awareness of preventive healthcare, and demand for at-home vaccination options are stimulating growth. The U.K.’s strong healthcare infrastructure and regulatory support further bolster market expansion.

France Vaccine Administration Devices Market Insight

The France vaccine administration devices market is expected to grow at a substantial CAGR, fueled by government-led immunization programs and high public health awareness. Hospitals, clinics, and community health centers extensively use advanced delivery devices such as auto-injectors and needle-free systems. Digital monitoring tools and patient tracking enhance adoption and ensure accurate vaccination coverage. France prioritizes safety, patient comfort, and compliance, which supports widespread device usage. Increasing investments in clinical-stage vaccines and research programs are further driving demand. Both residential and institutional vaccination initiatives contribute to steady market growth.

Poland Vaccine Administration Devices Market Insight

The Poland vaccine administration devices market is expected to witness the fastest CAGR during the forecast period, driven by expanding healthcare infrastructure, increasing vaccination coverage, and rising adoption of auto-injector and needle-free devices. Public health initiatives and government support for mass immunization campaigns are accelerating device adoption. Hospitals, clinics, and homecare programs are increasingly integrating advanced delivery systems for patient safety and compliance. Growing awareness of preventive healthcare and emerging clinical trials further contribute to market growth. Affordable and easy-to-use devices are boosting adoption in both urban and semi-urban regions. Expansion in training programs and digital tracking initiatives reinforces market penetration.

Europe Vaccine Administration Devices Market Share

The Europe vaccine administration devices industry is primarily led by well-established companies, including:

- BD (U.S.)

- Ypsomed (Switzerland)

- CROSSJECT (France)

- SHL Medical (Switzerland)

- Stevanato Group (Italy)

- Idevax (Belgium)

- Gerresheimer AG (Germany)

- ConvaTec Group PLC (U.K.)

- B. Braun SE (Germany)

- Terumo Europe NV (Belgium)

- Owen Mumford (U.K.)

- Vetter Pharma (Germany)

- West Pharmaceutical Services, Inc. (U.S.)

- SCHOTT Pharma (Germany)

- Nipro Europe Group Companies (Belgium)

- AptarGroup, Inc. (U.S.)

- Elcam Medical (Israel)

- ApiJect Systems, Corp (U.S.)

- Kindeva (U.S.)

- Phillips-Medisize (U.S.)

What are the Recent Developments in Europe Vaccine Administration Devices Market?

- In July 2025, The European Commission approved a novel pre-filled autoinjector for subcutaneous, once-monthly octreotide depot therapy (Oczyesa pen) for acromegaly patients. This device supports self-administration of a long-acting therapeutic via a pre-filled pen format

- In June 2025, the European Commission approved the needle-free nasal spray EURneffy for emergency treatment of severe allergic reactions (anaphylaxis) in Germany — the EU’s first nasal epinephrine product, representing a major needle-free alternative to traditional auto-injector devices

- In May 2025, Sandoz launched its Pyzchiva autoinjector in Europe the first European commercial autoinjector format of a ustekinumab biosimilar, offering patients a more comfortable self-administration experience with accurate automatic dosing and compact design

- In January 2025, Kindeva Drug Delivery entered an exclusive partnership with Emervax to co-develop a microneedle patch vaccine delivery platform combining Kindeva’s solid-coated microneedle array patch technology with Emervax’s thermostable circular RNA vaccine platform (emxRNATM). The collaboration aims at vaccine administration that is minimally invasive and easier to transport, potentially reducing cold chain requirements

- In January 2023, AstraZeneca received EU approval for a Tezspire pre-filled pen device, enabling patients to self-administer severe asthma therapy at home or in clinic with simple, guided auto-injector style use

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.