Europe Warehouse Management System Market

Market Size in USD Billion

USD

1.56 Billion

USD

5.21 Billion

2025

2033

USD

1.56 Billion

USD

5.21 Billion

2025

2033

| 2026 - 2033 | |

| USD 1.56 Billion | |

| USD 5.21 Billion | |

| % | |

|

Europe Warehouse Management System Market Overview

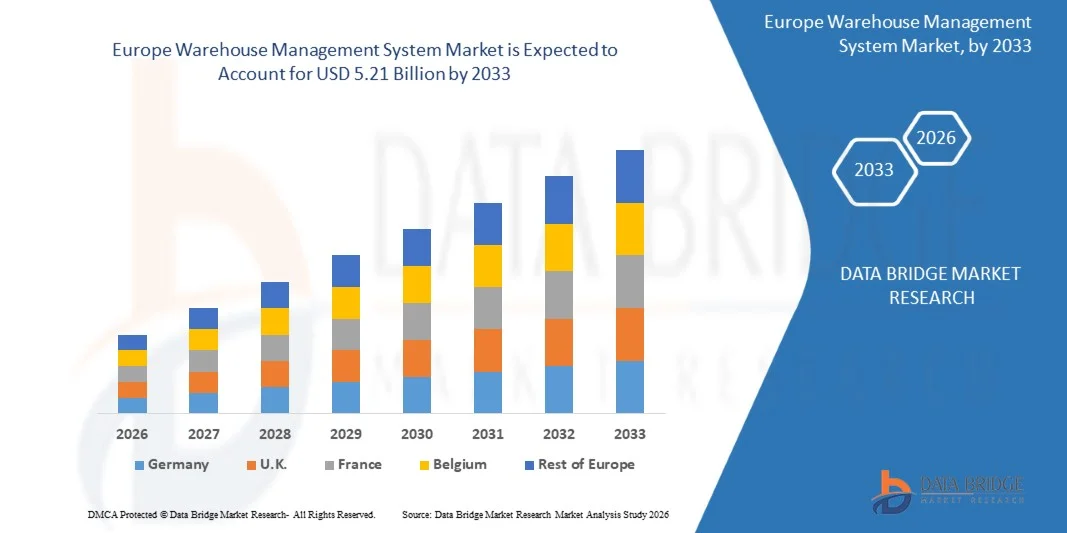

As per Data Bridge Market Research analysis the Europe warehouse management system market was valued at USD 1.56 billion in 2025 and is projected to reach USD 5.21 billion by 2033, growing at a CAGR of 16.30% from 2026 to 2033. The market is experiencing strong growth driven by the rapid expansion of e-commerce, increasing adoption of cloud-based warehouse software, and rising demand for real-time inventory visibility, order accuracy, and automated fulfillment operations.

The growing complexity of omnichannel retail, shorter delivery expectations, and increasing labor costs are compelling retailers, manufacturers, third-party logistics providers, and distributors to deploy advanced warehouse management systems. Cloud-based WMS platforms are enabling organizations to optimize inventory allocation, improve picking and packing efficiency, reduce fulfillment errors, and integrate warehouse operations with robotics, transportation management, and enterprise resource planning systems. The increasing adoption of Software-as-a-Service models among small and medium-sized enterprises is further expanding market accessibility, while demand for intelligent warehouse automation continues to accelerate across transportation, logistics, retail, manufacturing, and healthcare industries.

Key Market Trends & Insights

- Germany dominated the Europe warehouse management system market with the largest revenue share of approximately 28.6% in 2025, supported by its strong manufacturing base, advanced logistics infrastructure, and high concentration of automotive, machinery, chemicals, and industrial goods producers.

- U.K. warehouse management system market is expected to witness the fastest growth rate from 2026 to 2033, recording a CAGR of approximately 14.2%, fueled by the rapid expansion of e-commerce, increasing demand for same-day and next-day delivery services, and the rising need for efficient warehouse operations.

- The software segment held the largest market revenue share of approximately 51.8% in 2025, driven by rising deployment of inventory management, order orchestration, warehouse execution, and real-time tracking platforms across logistics and retail operations. Software solutions are preferred due to their ability to centralize warehouse data, improve inventory accuracy, optimize picking routes, and integrate with enterprise resource planning and transportation management systems.

- The services segment is projected to register the fastest growth at a CAGR of 23.6% from 2026 to 2033, driven by growing demand for implementation, customization, integration, training, and managed support services. Increasing migration from legacy warehouse systems to cloud-based platforms and the need for continuous system upgrades are accelerating segment expansion.

- The cloud-based segment held the largest market revenue share of approximately 58.4% in 2025, driven by its scalability, lower upfront infrastructure requirements, remote accessibility, and ability to support multi-warehouse operations. Cloud-based systems are increasingly adopted by retailers, third-party logistics providers, and small and medium-sized enterprises seeking faster deployment and subscription-based pricing models.

- The on-premise segment is projected to register steady growth from 2026 to 2033, supported by demand from large enterprises requiring greater control over data security, customization, and integration with existing enterprise infrastructure. Industries handling sensitive operational data, including healthcare, chemicals, and high-value manufacturing, continue to deploy on-premise systems for internal data governance and compliance requirements.

- The advanced segment held the largest market revenue share of approximately 46.2% in 2025, driven by growing demand for artificial intelligence-enabled analytics, robotics integration, labor optimization, predictive replenishment, and real-time inventory visibility. Advanced WMS platforms are widely used by large e-commerce operators, manufacturers, and logistics providers managing high-volume and complex warehouse networks.

- The intermediate segment is projected to register the fastest growth at a CAGR of 22.9% from 2026 to 2033, driven by increasing adoption among mid-sized businesses seeking configurable inventory, order fulfillment, and warehouse control capabilities. These solutions offer a balance between functionality, deployment cost, and scalability, making them suitable for organizations transitioning from manual or basic warehouse processes.

- The analytics and optimization segment held the largest market revenue share of approximately 31.6% in 2025, driven by increasing demand for predictive inventory planning, warehouse performance monitoring, dynamic slotting, and automated replenishment. Analytics tools help warehouse operators improve throughput, reduce stockouts, and optimize labor utilization across fulfillment operations.

- The labour management system segment is projected to register the fastest growth at a CAGR of 24.1% from 2026 to 2033, driven by rising labor costs, workforce shortages, and the need to improve employee productivity. Labor management platforms enable organizations to track worker performance, allocate tasks efficiently, and reduce picking and packing delays across large warehouse facilities.

- The online segment held the largest market revenue share of approximately 63.7% in 2025, driven by the increasing availability of cloud-based WMS platforms, direct vendor subscriptions, and digital procurement channels. Online distribution enables organizations to evaluate software features, access remote demonstrations, and deploy scalable warehouse solutions with reduced implementation time.

- The offline segment is projected to register steady growth from 2026 to 2033, supported by demand for direct consulting, customized implementation, and enterprise-level system integration services. Large warehouse operators continue to rely on offline channels for detailed requirement assessment, hardware installation, and long-term service support.

- The e-commerce segment held the largest market revenue share of approximately 28.9% in 2025, driven by rising online order volumes, growing consumer expectations for same-day delivery, and increasing need for accurate inventory visibility. E-commerce companies are deploying WMS platforms to automate picking, packing, returns processing, and real-time order tracking across high-volume fulfillment centers.

- The third-party logistics segment is projected to register the fastest growth at a CAGR of 24.8% from 2026 to 2033, driven by expanding outsourcing of warehousing and fulfillment activities by retailers, manufacturers, and consumer goods companies. Third-party logistics providers are increasingly adopting WMS platforms to manage multi-client inventory, improve billing accuracy, optimize warehouse capacity, and provide real-time operational visibility to customers.

Market Size & Forecast

- Market Value (2025): USD 1.56 Billion

- Expected Market Value (2033): USD 5.21 Billion

- Forecast CAGR (2026–2033): 16.30%

- Leading Country in 2025: Germany

- Fastest Growing Country: U.K.

Report Scope and Europe Warehouse Management System Market Segmentation

|

Attributes |

Europe Warehouse Management System Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Europe

|

|

Key Market Players |

• Körber AG (Germany) |

|

Market Opportunities |

• Integration Of Artificial Intelligence And Machine Learning In Warehouse Operations • Rising Adoption Of Cloud-Based Warehouse Management Systems |

|

Value Added Data Infosets |

In addition to the market insights such as market value, growth rate, market segments, geographical coverage, market players, and market scenario, the market report curated by the Data Bridge Market Research team includes in-depth expert analysis, import/export analysis, pricing analysis, production consumption analysis, and pestle analysis. |

Europe Warehouse Management System Market Trends

Trend: Integration Of Artificial Intelligence, Robotics, And Cloud-Based Warehouse Automation

The growing need for faster order fulfillment, accurate inventory control, and cost-efficient logistics operations is increasing adoption of advanced warehouse management systems across retail, e-commerce, manufacturing, healthcare, and third-party logistics industries. Traditional warehouse operations relying on manual inventory recording, paper-based picking, and disconnected software systems often result in stock inaccuracies, delayed dispatches, and higher labor costs, encouraging businesses to implement integrated digital warehouse platforms.

In modern e-commerce fulfillment centers, organizations are deploying warehouse management systems with artificial intelligence, machine learning, barcode scanning, RFID, automated guided vehicles, and robotic picking technologies to improve inventory accuracy and optimize order processing. For instance, Amazon has deployed more than 750,000 robots across its global fulfillment network, supporting faster picking, sorting, and material movement operations while reducing dependence on manual workflows. Similarly, Walmart has expanded automated fulfillment and inventory management capabilities across its distribution network to support high-volume omnichannel order fulfilment.

The rapid expansion of online retail and same-day delivery expectations is also increasing demand for cloud-based warehouse management systems capable of providing real-time inventory visibility across multiple locations. Global e-commerce sales exceeded USD 6 trillion in 2024, creating substantial pressure on retailers and logistics providers to improve warehouse throughput and delivery accuracy. In addition, the adoption of cloud WMS platforms is enabling small and medium-sized enterprises to access scalable inventory management, labor planning, and analytics tools without large upfront infrastructure investments.

Global Warehouse Management System Market Dynamics

Key Market Driver: Rising Demand For E-Commerce Fulfillment And Real-Time Inventory Visibility

The expansion of e-commerce, omnichannel retailing, and direct-to-consumer business models is creating strong demand for warehouse management systems that can coordinate inventory, picking, packing, shipping, and returns operations in real time. Retailers and logistics providers are under growing pressure to maintain accurate stock availability across warehouses, stores, and online platforms while meeting shorter delivery timelines and reducing fulfillment costs.

Organizations across retail, consumer goods, automotive, pharmaceuticals, and industrial manufacturing are increasingly implementing WMS platforms to improve inventory traceability and warehouse productivity. For instance, global retail e-commerce sales reached approximately USD 6 trillion in 2024, highlighting the scale of fulfillment activity requiring efficient warehouse operations. WMS platforms help businesses reduce manual errors by integrating barcode, RFID, voice picking, and mobile scanning technologies into daily warehouse workflows.

Similarly, third-party logistics providers are deploying cloud-based WMS solutions to manage multi-client warehouses, optimize labor allocation, and support real-time customer reporting. The global logistics industry continues to face labor shortages and rising operational expenses, increasing the value of systems that can improve pick-path planning, automate replenishment, and provide predictive inventory insights. Large-scale distribution centers using integrated WMS and automation technologies have reported inventory accuracy levels exceeding 99% in controlled warehouse environments.

Key Restraint/Challenge: High Implementation Costs And Complex System Integration

Warehouse management system implementation can require substantial investment in software configuration, data migration, employee training, warehouse process redesign, and integration with enterprise resource planning, transportation management, and automation systems. These requirements can create adoption barriers for small and medium-sized enterprises with limited technology budgets and legacy warehouse infrastructure.

In addition, organizations operating across multiple warehouse locations may face difficulties in standardizing product data, inventory processes, and fulfillment rules before deploying a centralized WMS platform. Integration with automated storage and retrieval systems, conveyor networks, robotics, RFID infrastructure, and handheld devices can further increase project complexity and deployment timelines. Industry implementation studies indicate that enterprise WMS deployments can take between six and eighteen months depending on warehouse size, system customization requirements, and integration scope.

Cybersecurity concerns and dependence on uninterrupted network connectivity also remain important challenges for cloud-based warehouse management systems. Warehouses processing pharmaceutical products, food items, and high-value consumer goods require strong access controls, data protection, and traceability capabilities to maintain regulatory compliance and prevent operational disruption. Limited availability of skilled warehouse technology professionals can further delay system adoption and reduce the effectiveness of advanced WMS deployments.

Key Market Opportunity: Expansion Of Autonomous Warehousing And Intelligent Supply Chain Networks

The growing adoption of autonomous mobile robots, automated guided vehicles, robotic picking systems, and artificial intelligence-based analytics is creating significant opportunities for warehouse management system providers. These technologies require advanced software platforms capable of coordinating inventory movement, task allocation, labor utilization, and equipment performance across increasingly automated warehouse environments.

Retailers, manufacturers, and logistics providers are investing in intelligent WMS platforms to support predictive replenishment, dynamic slotting, automated cycle counting, and demand-driven inventory positioning. For instance, DHL has identified that warehouse automation and robotics can improve operational efficiency while helping address persistent labor availability challenges across logistics operations. In pharmaceutical and healthcare distribution, WMS platforms are also being used to support batch tracking, expiry-date monitoring, cold-chain management, and compliance reporting.

Furthermore, the increasing deployment of micro-fulfillment centers and urban distribution hubs is expanding demand for compact, high-throughput WMS solutions. These facilities require rapid inventory updates and automated order orchestration to support same-day and next-day delivery models. The integration of digital twins, predictive analytics, and Internet of Things sensors with warehouse management systems is expected to create new opportunities for real-time warehouse optimization across retail, logistics, manufacturing, healthcare, and consumer goods industries.

Europe Warehouse Management System Market Scope

The market is segmented on the basis of component, deployment, type of tier, function, distribution channel, and end-user.

• By Component

On the basis of component, the warehouse management system market is segmented into hardware, software, and services. The software segment held the largest market revenue share of approximately 51.8% in 2025, driven by rising deployment of inventory management, order orchestration, warehouse execution, and real-time tracking platforms across logistics and retail operations. Software solutions are preferred due to their ability to centralize warehouse data, improve inventory accuracy, optimize picking routes, and integrate with enterprise resource planning and transportation management systems.

The services segment is projected to register the fastest growth at a CAGR of 23.6% from 2026 to 2033, driven by growing demand for implementation, customization, integration, training, and managed support services. Increasing migration from legacy warehouse systems to cloud-based platforms and the need for continuous system upgrades are accelerating segment expansion.

• By Deployment

On the basis of deployment, the warehouse management system market is segmented into cloud-based and on-premise. The cloud-based segment held the largest market revenue share of approximately 58.4% in 2025, driven by its scalability, lower upfront infrastructure requirements, remote accessibility, and ability to support multi-warehouse operations. Cloud-based systems are increasingly adopted by retailers, third-party logistics providers, and small and medium-sized enterprises seeking faster deployment and subscription-based pricing models.

The on-premise segment is projected to register steady growth from 2026 to 2033, supported by demand from large enterprises requiring greater control over data security, customization, and integration with existing enterprise infrastructure. Industries handling sensitive operational data, including healthcare, chemicals, and high-value manufacturing, continue to deploy on-premise systems for internal data governance and compliance requirements.

• By Type Of Tier

On the basis of type of tier, the warehouse management system market is segmented into advanced, intermediate, and basic. The advanced segment held the largest market revenue share of approximately 46.2% in 2025, driven by growing demand for artificial intelligence-enabled analytics, robotics integration, labor optimization, predictive replenishment, and real-time inventory visibility. Advanced WMS platforms are widely used by large e-commerce operators, manufacturers, and logistics providers managing high-volume and complex warehouse networks.

The intermediate segment is projected to register the fastest growth at a CAGR of 22.9% from 2026 to 2033, driven by increasing adoption among mid-sized businesses seeking configurable inventory, order fulfillment, and warehouse control capabilities. These solutions offer a balance between functionality, deployment cost, and scalability, making them suitable for organizations transitioning from manual or basic warehouse processes.

• By Function

On the basis of function, the warehouse management system market is segmented into labour management system, analytics and optimization, billing and yard management, systems integration and maintenance, and consulting services. The analytics and optimization segment held the largest market revenue share of approximately 31.6% in 2025, driven by increasing demand for predictive inventory planning, warehouse performance monitoring, dynamic slotting, and automated replenishment. Analytics tools help warehouse operators improve throughput, reduce stockouts, and optimize labor utilization across fulfillment operations.

The labour management system segment is projected to register the fastest growth at a CAGR of 24.1% from 2026 to 2033, driven by rising labor costs, workforce shortages, and the need to improve employee productivity. Labor management platforms enable organizations to track worker performance, allocate tasks efficiently, and reduce picking and packing delays across large warehouse facilities.

• By Distribution Channel

On the basis of distribution channel, the warehouse management system market is segmented into online and offline. The online segment held the largest market revenue share of approximately 63.7% in 2025, driven by the increasing availability of cloud-based WMS platforms, direct vendor subscriptions, and digital procurement channels. Online distribution enables organizations to evaluate software features, access remote demonstrations, and deploy scalable warehouse solutions with reduced implementation time.

The offline segment is projected to register steady growth from 2026 to 2033, supported by demand for direct consulting, customized implementation, and enterprise-level system integration services. Large warehouse operators continue to rely on offline channels for detailed requirement assessment, hardware installation, and long-term service support.

• By End-User

On the basis of end-user, the warehouse management system market is segmented into food and beverage, e-commerce, automotive, third-party logistics, healthcare, electrical and electronics, metals and machinery, chemicals, and others. The e-commerce segment held the largest market revenue share of approximately 28.9% in 2025, driven by rising online order volumes, growing consumer expectations for same-day delivery, and increasing need for accurate inventory visibility. E-commerce companies are deploying WMS platforms to automate picking, packing, returns processing, and real-time order tracking across high-volume fulfillment centers.

The third-party logistics segment is projected to register the fastest growth at a CAGR of 24.8% from 2026 to 2033, driven by expanding outsourcing of warehousing and fulfillment activities by retailers, manufacturers, and consumer goods companies. Third-party logistics providers are increasingly adopting WMS platforms to manage multi-client inventory, improve billing accuracy, optimize warehouse capacity, and provide real-time operational visibility to customers.

Europe Warehouse Management System Market Regional Analysis

Germany Warehouse Management System Market Insight

Germany dominated the Europe warehouse management system market with the largest revenue share of approximately 28.6% in 2025, supported by its strong manufacturing base, advanced logistics infrastructure, and high concentration of automotive, machinery, chemicals, and industrial goods producers. Companies across the country are increasingly investing in warehouse management systems to streamline inventory handling, reduce fulfillment errors, and improve coordination between production facilities, distribution centers, and transportation networks. The growing integration of automated storage and retrieval systems, autonomous mobile robots, and data analytics platforms is further strengthening demand for advanced warehouse management solutions across German industrial and commercial operations.

U.K. Warehouse Management System Market Insight

The U.K. warehouse management system market is expected to witness the fastest growth rate from 2026 to 2033, recording a CAGR of approximately 14.2%, fueled by the rapid expansion of e-commerce, increasing demand for same-day and next-day delivery services, and the rising need for efficient warehouse operations. Retailers, logistics providers, and consumer goods companies are adopting cloud-based warehouse management systems to enhance inventory accuracy, improve order processing speed, and manage growing volumes of online orders. In addition, the expansion of third-party logistics networks, increasing investment in smart fulfillment centers, and rising adoption of automated picking and sorting technologies are expected to continue driving market growth in the U.K.

Europe Warehouse Management System Market Share

The Europe Warehouse Management System industry is primarily led by well-established companies, including:

• Körber AG (Germany)

• SSI SCHÄFER Group (Germany)

• Mecalux S.A. (Spain)

• Consafe Logistics AB (Sweden)

• Hardis Group (France)

• KNAPP AG (Austria)

• Swisslog Holding AG (Switzerland)

• Jungheinrich AG (Germany)

• viastore SOFTWARE GmbH (Germany)

• inconso AG (Germany)

• Ehrhardt Partner Group (Germany)

• Acteos SA (France)

• Generix Group SA (France)

• Mantis Informatics S.A. (Greece)

• Ongoing Warehouse AB (Sweden)

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.