Europe Whole Exome Sequencing Market

Market Size in USD Billion

USD

407.98 Billion

USD

2,161.11 Billion

2025

2033

USD

407.98 Billion

USD

2,161.11 Billion

2025

2033

| 2026 - 2033 | |

| USD 407.98 Billion | |

| USD 2,161.11 Billion | |

| % | |

|

Europe Whole Exome Sequencing Market Overview

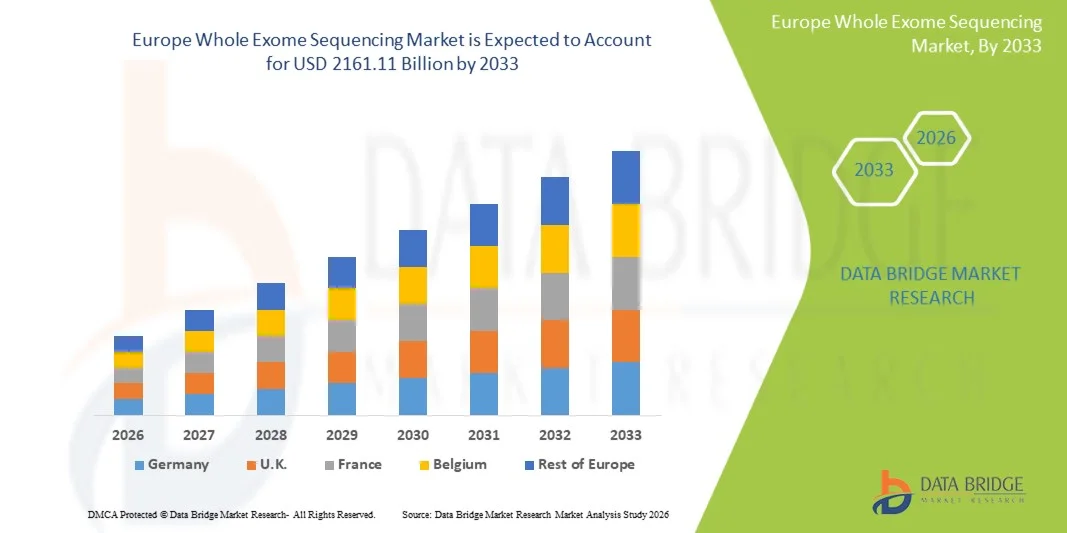

The Europe Whole Exome Sequencing market was valued at USD 407.98 billion in 2025 and is projected to reach USD 2161.11 billion by 2033, growing at a CAGR of 23.17% from 2026 to 2033. The market is experiencing consistent growth driven by rising demand for precision medicine and advanced genomic diagnostics, rapid advancements in next-generation sequencing (NGS) technologies, and expanding applications across oncology, rare disease diagnosis, reproductive health, and personalized medicine.

The increasing prevalence of genetic disorders and cancer globally, combined with growing adoption of genomic testing in clinical and research settings, is compelling hospitals, diagnostic laboratories, pharmaceutical companies, and research institutes to adopt advanced whole exome sequencing technologies. High-throughput and AI-integrated sequencing platforms are increasingly replacing conventional genetic testing methods in many healthcare environments, offering cost-effective, accurate, and comprehensive analysis of protein-coding regions for disease identification, biomarker discovery, and therapeutic decision-making.

Key Market Trends & Insights

- K. dominated the Europe Whole Exome Sequencing market with the largest revenue share of 36.95% in 2025, supported by expanding genomic research infrastructure, strong government investments in precision medicine initiatives, and increasing adoption of next-generation sequencing (NGS) technologies across hospitals, academic institutes, and biotechnology companies. The region also benefits from rising prevalence of cancer and rare genetic disorders, growing demand for personalized medicine, and increasing integration of AI-based genomic analytics in clinical diagnostics and drug discovery applications

- The second-generation sequencing segment dominated the market with a share of 68.42% in 2025 due to its widespread adoption across clinical diagnostics, academic research, and pharmaceutical applications.

- Germany is expected to be the fastest-growing region at a CAGR of 8.6% from 2026 to 2033, fueled by expanding healthcare infrastructure, increasing investments in genomics and biotechnology research, and rising adoption of precision medicine technologies across hospitals and diagnostic laboratories. Growing awareness regarding early disease diagnosis, increasing prevalence of inherited disorders, and strong government support for genomic medicine initiatives are further accelerating market growth in Germany.

- The Third-Generation Sequencing segment is the fastest-growing component category, projected to register a CAGR of 8.4%, reflecting increasing demand for long-read sequencing technologies capable of delivering improved structural variant detection, faster sequencing workflows, and enhanced genomic accuracy in complex disease analysis.

- The Diagnostics segment dominates the application category with a 39.27% revenue share in 2025, led by increasing use of whole exome sequencing in cancer diagnostics, rare disease identification, prenatal screening, and hereditary disorder analysis across hospitals, clinical laboratories, and specialized genomic centers.

- Direct Trade distribution channel accounts for 57.36% of the market, preferred by pharmaceutical companies, research institutions, and large healthcare organizations requiring customized sequencing solutions, direct technical support, and long-term procurement agreements for advanced genomic systems and consumables.

- The Services segment is the fastest-growing product and service category, with a CAGR of 8.0%, driven by rising outsourcing of sequencing workflows, increasing demand for bioinformatics analysis, cloud-based genomic interpretation services, and growing reliance on specialized genomic service providers for clinical and research applications.

Market Size & Forecast

- Europe Market Value (2025): USD 407.98 Billion

- Expected Market Value (2033): USD 2161.11 Billion

- Forecast CAGR (2026–2033): 23.17%

- Leading Region in 2025: U.K.

- Fastest Growing Region: Germany

Report Scope and Europe Whole Exome Sequencing Market Segmentation

|

Attributes |

Whole Exome Sequencing Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe |

|

Key Market Players |

• Illumina, Inc. (U.S.) |

|

Market Opportunities |

· Increasing Adoption of Precision Medicine and Companion Diagnostics · Expansion of Genomic Research and Rare Disease Diagnosis · Growth Opportunities in Emerging Markets and AI-Driven Genomics |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, geographically represented company-wise production and capacity, network layouts of distributors and partners, detailed and updated price trend analysis and deficit analysis of supply chain and demand. |

Europe Whole Exome Sequencing Market Trends

Trend: Rising Adoption of Precision Medicine and Genomic Research

Healthcare providers, pharmaceutical companies, and research institutes are increasingly adopting Whole Exome Sequencing (WES) technologies to improve disease diagnosis, support precision medicine initiatives, and accelerate genomic research. WES enables comprehensive analysis of protein-coding regions of the genome, helping clinicians identify disease-causing mutations associated with cancer, rare genetic disorders, cardiovascular diseases, and inherited conditions. Academic and clinical research centers are similarly leveraging next-generation sequencing (NGS) platforms integrated with AI-driven bioinformatics tools to improve variant interpretation and personalized treatment planning. In addition, cloud-based genomic analytics and automated sequencing workflows are enhancing data processing efficiency and reducing turnaround time for clinical diagnostics. According to global genomic research studies, over 80–85% of known disease-causing mutations are located within the exome, significantly increasing the clinical importance of WES technologies. The growing adoption of precision oncology programs and national genome sequencing initiatives across countries such as China, India, Japan, and South Korea continues to strengthen market expansion across the Europe region.

Europe Whole Exome Sequencing Market Dynamics

Key Market Driver: Growing Demand for Precision Medicine and Genetic Disease Diagnosis

The increasing prevalence of cancer, rare genetic disorders, and inherited diseases is significantly driving demand for Whole Exome Sequencing technologies across the Europe region. Hospitals, clinical laboratories, pharmaceutical companies, and academic research institutes are increasingly relying on WES platforms for mutation analysis, biomarker discovery, and personalized treatment development. According to global health studies, rare diseases affect more than 300 million people worldwide, with a substantial patient population residing in Europe countries. In oncology applications, WES is increasingly being used to identify actionable mutations and guide targeted therapies in cancers such as lung cancer, breast cancer, and colorectal cancer. Countries including China, Japan, India, and South Korea are expanding investments in precision medicine programs and genomic research infrastructure to improve early disease diagnosis and treatment outcomes. In addition, increasing government-funded genome sequencing projects and rising adoption of next-generation sequencing technologies in clinical diagnostics are further accelerating market growth across the region.

Key Restraint/Challenge: High Cost of Sequencing Technologies and Complex Data Interpretation

A significant restraint in the Europe Whole Exome Sequencing market is the high cost associated with advanced sequencing systems, bioinformatics infrastructure, and genomic data analysis. Modern WES platforms require sophisticated sequencing instruments, high-performance computing infrastructure, and specialized laboratory expertise, resulting in substantial capital investment and operational costs for hospitals and research laboratories. In addition, interpretation of large genomic datasets remains highly complex and requires trained bioinformaticians and genetic specialists, limiting accessibility in smaller healthcare facilities and developing economies. Although sequencing costs have declined significantly over the last decade, comprehensive exome sequencing and downstream analysis still remain relatively expensive for routine clinical adoption in several emerging markets. Furthermore, concerns related to genomic data privacy, ethical considerations, and lack of standardized reimbursement policies continue to create operational and regulatory challenges for healthcare providers and diagnostic laboratories across Europe countries.

Key Market Opportunity: Integration of AI, Cloud Genomics, and Personalized Healthcare Platforms

The integration of artificial intelligence, cloud-based bioinformatics platforms, and precision healthcare systems presents a significant growth opportunity for the Whole Exome Sequencing market. AI-enabled genomic analysis platforms can accelerate variant interpretation, improve mutation detection accuracy, and reduce diagnostic turnaround times for clinical applications. Cloud-based genomic data management systems are further enabling secure storage, collaborative research, and large-scale population genomics analysis across healthcare networks and research organizations. Pharmaceutical and biotechnology companies are increasingly utilizing WES data to support drug discovery, biomarker identification, and companion diagnostic development for targeted therapies. In addition, expanding national genome projects and increasing adoption of personalized medicine initiatives across China, India, Japan, and Southeast Asia are creating strong long-term growth opportunities for sequencing technology providers. The growing use of AI-assisted clinical interpretation tools and automated sequencing workflows is also improving accessibility and operational efficiency, enabling wider adoption of Whole Exome Sequencing technologies across hospitals, clinical laboratories, and academic research institutions.

Europe Whole Exome Sequencing Market Scope

The Whole Exome Sequencing market is segmented on the basis of component, product and service, application, end user, and distribution channel.

By Component

On the basis of component, the Whole Exome Sequencing market is segmented into second-generation sequencing and third-generation sequencing. The second-generation sequencing segment dominated the market with a share of 68.42% in 2025 due to its widespread adoption across clinical diagnostics, academic research, and pharmaceutical applications. High throughput capacity, improved sequencing accuracy, and cost-effectiveness compared to conventional sequencing methods are major factors supporting segment dominance. In addition, the increasing use of second-generation sequencing platforms in cancer genomics, rare disease diagnosis, and precision medicine programs is accelerating adoption globally. Pharmaceutical and biotechnology companies are increasingly utilizing these technologies for biomarker discovery, drug target identification, and genomic profiling studies. The availability of advanced sequencing platforms with automated workflows and cloud-based bioinformatics integration is further improving operational efficiency and reducing turnaround time. Academic and research institutes are also expanding investments in large-scale genomic projects and population sequencing initiatives, further reinforcing segment growth. Moreover, growing healthcare expenditure and increasing government support for genomic medicine programs continue to strengthen the market position of second-generation sequencing technologies across clinical and research environments.

The third-generation sequencing segment is expected to witness the fastest CAGR of 9.1% from 2026 to 2033, driven by increasing demand for long-read sequencing technologies capable of delivering higher genomic resolution and improved structural variant detection. These platforms provide advantages such as real-time sequencing, enhanced detection of complex genomic regions, and reduced amplification bias, making them highly attractive for advanced genomics research and personalized medicine applications. In addition, ongoing technological advancements, declining sequencing costs, and increasing adoption in translational research and rare disease analysis are further accelerating segment growth.

By Product and Service

On the basis of product and service, the Whole Exome Sequencing market is segmented into systems, kits, and services. The kits segment dominated the market with a share of 44.38% in 2025 due to increasing demand for standardized sample preparation, target enrichment, and library preparation workflows across hospitals, clinical laboratories, and research institutes. High adoption of ready-to-use sequencing kits is improving operational efficiency, reducing workflow complexity, and enhancing sequencing accuracy in genomic analysis applications. In addition, rising use of exome enrichment kits for oncology testing, inherited disease screening, and precision medicine programs is supporting segment expansion globally. Pharmaceutical and biotechnology companies are increasingly relying on advanced sequencing kits to improve reproducibility and scalability in genomic research projects. The growing availability of customized and automation-compatible kits is also enabling laboratories to streamline sequencing operations and reduce turnaround time. Furthermore, increasing investments in genomic diagnostics infrastructure and growing adoption of next-generation sequencing technologies continue to reinforce the leading position of the kits segment across the global market.

The services segment is expected to witness the fastest CAGR of 9.4% from 2026 to 2033, driven by rising outsourcing of genomic sequencing and bioinformatics analysis services by healthcare providers, pharmaceutical companies, and research organizations. Service providers are increasingly offering integrated sequencing, data interpretation, and cloud-based genomic analytics solutions, enabling cost-effective and scalable genomic testing capabilities. In addition, increasing demand for specialized bioinformatics expertise, rapid turnaround time, and advanced clinical interpretation services is further accelerating growth across sequencing service platforms.

By Application

On the basis of application, the Whole Exome Sequencing market is segmented into drug discovery and development, agriculture & animal research, diagnostics, personalized medicine, and others. The diagnostics segment dominated the market with a share of 39.67% in 2025 due to increasing adoption of whole exome sequencing technologies for identifying genetic mutations associated with cancer, rare diseases, neurological disorders, and inherited conditions. Hospitals, clinical laboratories, and diagnostic centers are increasingly integrating WES platforms into routine clinical workflows to improve diagnostic accuracy and support precision healthcare initiatives. In addition, rising prevalence of chronic and genetic diseases, combined with increasing awareness regarding early disease detection and personalized treatment planning, is significantly driving segment growth. Growing government investments in genomic medicine and national sequencing programs are further accelerating adoption across healthcare systems worldwide. The integration of AI-powered bioinformatics tools and cloud-based genomic analytics is also improving variant interpretation efficiency and supporting broader clinical utilization of WES technologies.

The personalized medicine segment is expected to witness the fastest CAGR of 9.6% from 2026 to 2033, driven by increasing demand for individualized treatment approaches based on patient-specific genomic information. Healthcare providers and pharmaceutical companies are increasingly utilizing exome sequencing to identify actionable mutations, optimize targeted therapies, and improve patient outcomes in oncology and rare disease management. In addition, advancements in precision medicine infrastructure, growing use of companion diagnostics, and increasing adoption of pharmacogenomics are further contributing to rapid segment expansion.

By End User

On the basis of end user, the Whole Exome Sequencing market is segmented into pharmaceutical & biotechnology companies, academic & research institutes, hospitals and clinics, clinical laboratories, and others. The pharmaceutical & biotechnology companies segment dominated the market with a share of 36.84% in 2025 due to increasing use of whole exome sequencing technologies in drug discovery, biomarker identification, precision medicine development, and clinical trial research activities. These companies are heavily investing in genomic research platforms to accelerate therapeutic development and improve understanding of disease pathways. In addition, increasing collaborations between sequencing technology providers and pharmaceutical firms are supporting adoption of advanced sequencing workflows and bioinformatics solutions across research and development operations. Rising demand for genomic profiling in oncology and rare disease drug development is further strengthening the segment’s leading position in the market. Moreover, advancements in high-throughput sequencing systems and integration of AI-driven genomic analytics are enabling more efficient interpretation of large-scale genomic datasets.

The hospitals and clinics segment is expected to witness the fastest CAGR of 8.9% from 2026 to 2033, driven by increasing adoption of genomic testing in routine clinical diagnostics and personalized treatment planning. Hospitals are increasingly implementing whole exome sequencing technologies for early disease detection, cancer genomics, neonatal screening, and rare disease diagnosis. In addition, rising healthcare investments, improving reimbursement frameworks, and growing availability of precision medicine programs are further accelerating segment growth globally.

By Distribution Channel

On the basis of distribution channel, the Whole Exome Sequencing market is segmented into direct trade, retail sales, and others. The direct trade segment dominated the market with a share of 61.25% in 2025 due to strong partnerships between sequencing technology manufacturers, hospitals, research institutes, and pharmaceutical companies. Direct trade channels provide advantages such as customized sequencing solutions, technical support, training services, and long-term supply agreements, making them the preferred distribution model for high-value genomic technologies. In addition, increasing demand for integrated sequencing platforms and specialized laboratory solutions is encouraging manufacturers to strengthen direct sales networks globally. Pharmaceutical and biotechnology companies are also relying on direct procurement strategies to ensure consistent access to advanced sequencing systems, reagents, and bioinformatics tools. Furthermore, growing investments in genomic research infrastructure and increasing adoption of precision medicine initiatives continue to reinforce the dominance of the direct trade segment.

The retail sales segment is expected to witness the fastest CAGR of 8.3% from 2026 to 2033, driven by increasing accessibility of genomic testing products and growing expansion of online and third-party laboratory supply channels. Smaller research laboratories, academic institutions, and diagnostic centers are increasingly adopting retail procurement models for sequencing consumables and accessories due to improved availability and competitive pricing. In addition, rising awareness regarding genomic diagnostics and expanding distribution networks across emerging markets are further supporting segment growth.

Europe Whole Exome Sequencing Market Regional Analysis

The Europe Whole Exome Sequencing market is expected to witness rapid growth, driven by expanding genomic research infrastructure, increasing adoption of next-generation sequencing (NGS) technologies, and rising investments in precision medicine initiatives across countries such as the U.K., Germany, France, and Italy. Growing prevalence of cancer, rare genetic disorders, and inherited diseases, along with increasing demand for personalized medicine and advanced molecular diagnostics, is supporting regional market expansion. In addition, rising government funding for genomics research, increasing integration of AI-based bioinformatics platforms, and expanding pharmaceutical and biotechnology research activities are accelerating the adoption of Whole Exome Sequencing technologies across clinical, academic, and research sectors.

U.K. Whole Exome Sequencing Market Insight

U.K. dominated the Europe Whole Exome Sequencing market with the largest revenue share of 36.95% in 2025, supported by expanding genomic research infrastructure, strong government investments in precision medicine initiatives, and increasing adoption of next-generation sequencing (NGS) technologies across hospitals, academic institutes, and biotechnology companies. The country also benefits from rising prevalence of cancer and rare genetic disorders, growing demand for personalized medicine, and increasing integration of AI-based genomic analytics in clinical diagnostics and drug discovery applications. In addition, expanding national genome sequencing programs, rising investments in advanced molecular diagnostics, and increasing collaborations between research institutes and pharmaceutical companies are further reinforcing the U.K.’s leading position in the regional market.

Germany Whole Exome Sequencing Market Insight

Germany is expected to be the fastest-growing region at a CAGR of 8.6% from 2026 to 2033, fueled by expanding healthcare infrastructure, increasing investments in genomics and biotechnology research, and rising adoption of precision medicine technologies across hospitals and diagnostic laboratories. Growing awareness regarding early disease diagnosis, increasing prevalence of inherited disorders, and strong government support for genomic medicine initiatives are further accelerating market growth in Germany. In addition, increasing implementation of AI-enabled genomic analytics platforms, expansion of clinical research activities, and rising adoption of advanced sequencing technologies across pharmaceutical and academic sectors are supporting rapid regional market expansion.

Europe Whole Exome Sequencing Market Share

The Whole Exome Sequencing industry is primarily led by well-established companies, including:

- Illumina, Inc. (U.S.)

- Thermo Fisher Scientific Inc. (U.S.)

- QIAGEN N.V. (Netherlands)

- Agilent Technologies, Inc. (U.S.)

- Pacific Biosciences of California, Inc. (U.S.)

- Oxford Nanopore Technologies plc (U.K.)

- BGI Genomics Co., Ltd. (China)

- Roche Holding AG (Switzerland)

- Danaher Corporation (U.S.)

- PerkinElmer, Inc. (U.S.)

- Eurofins Scientific (Luxembourg)

- Macrogen, Inc. (South Korea)

- Novogene Co., Ltd. (China)

- GATC Biotech AG (Germany)

- Azenta Life Sciences (U.S.)

- Twist Bioscience Corporation (U.S.)

- 10x Genomics, Inc. (U.S.)

- F. Hoffmann-La Roche Ltd. (Switzerland)

- Bio-Rad Laboratories, Inc. (U.S.)

- Beijing Genomics Institute (BGI) (China)

- Myriad Genetics, Inc. (U.S.)

- Gene by Gene, Ltd. (U.S.)

- Natera, Inc. (U.S.)

- SOPHiA GENETICS SA (Switzerland)

- Fabric Genomics, Inc. (U.S.)

- Centogene N.V. (Germany)

- Integrated DNA Technologies, Inc. (U.S.)

- Personalis, Inc. (U.S.)

- Genewiz, Inc. (U.S.)

- Partek Incorporated (U.S.)

Latest Developments in Europe Whole Exome Sequencing Market

- In January 2021, Illumina, Inc. announced the launch of the TruSight Software Suite, an integrated bioinformatics solution designed to streamline whole exome and whole genome sequencing analysis for clinical laboratories. The platform enhances variant interpretation, workflow automation, and genomic data management, enabling healthcare providers and researchers to improve diagnostic efficiency and accelerate precision medicine applications

- In September 2021, Thermo Fisher Scientific Inc. announced the expansion of its Ion Torrent Genexus System capabilities with advanced Oncomine precision oncology assays supporting whole exome sequencing workflows. The development was aimed at improving rapid genomic profiling and enabling more accurate cancer mutation analysis in clinical and translational research settings

- In March 2022, Agilent Technologies, Inc. launched its SureSelect Cancer CGP Assay, a comprehensive genomic profiling solution designed for whole exome sequencing and targeted oncology research applications. The assay provides enhanced coverage for clinically relevant cancer biomarkers and supports precision oncology initiatives through improved sequencing accuracy and data reliability

- In October 2022, PacBio announced the commercial release of the Revio long-read sequencing system, designed to deliver higher throughput and improved accuracy for complex genomic analysis, including whole exome sequencing applications. The platform enables researchers to better identify structural variants and rare genetic mutations while reducing sequencing costs and turnaround times

- In February 2023, QIAGEN N.V. announced the launch of the QIAseq Multimodal DNA/RNA Kits to support advanced next-generation sequencing workflows, including whole exome sequencing for oncology and inherited disease research. The new kits enhance library preparation efficiency and enable simultaneous genomic and transcriptomic analysis for improved biomarker discovery

- In June 2023, Oxford Nanopore Technologies plc announced enhancements to its PromethION sequencing platform with upgraded chemistry and higher accuracy basecalling capabilities for large-scale genomic and whole exome sequencing projects. The development supports faster sequencing turnaround and improved detection of rare and complex genomic variants in clinical research applications

- In January 2024, Roche Holding AG announced a collaboration with PathAI to advance AI-powered digital pathology and genomic sequencing integration for precision medicine applications, including whole exome sequencing-based oncology diagnostics. The partnership aims to improve biomarker identification and support personalized treatment decision-making through advanced genomic analytics

- In May 2024, Illumina, Inc. announced the launch of the NovaSeq X Plus production-scale sequencing platform in additional global markets, expanding access to high-throughput whole exome sequencing for clinical genomics, population sequencing, and pharmaceutical research applications. The platform significantly improves sequencing speed, scalability, and sustainability while lowering genomic analysis costs.

- In August 2024, BGI Genomics announced the expansion of its whole exome sequencing services portfolio with enhanced AI-enabled bioinformatics analysis solutions for rare disease detection and oncology research. The upgraded services improve genomic interpretation efficiency and support precision medicine initiatives across hospitals and research institutions globally

- In February 2025, Element Biosciences announced advancements to its AVITI sequencing platform with upgraded chemistry and expanded compatibility for high-accuracy whole exome sequencing workflows. The development enhances sequencing flexibility, improves data quality, and supports cost-effective genomic research across academic, clinical, and pharmaceutical applications

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.