Global 3d Printing Medical Devices Market

Market Size in USD Billion

USD

4.01 Billion

USD

15.83 Billion

2024

2032

USD

4.01 Billion

USD

15.83 Billion

2024

2032

| 2025 - 2032 | |

| USD 4.01 Billion | |

| USD 15.83 Billion | |

| % | |

|

3D Printing Medical Devices Market Size

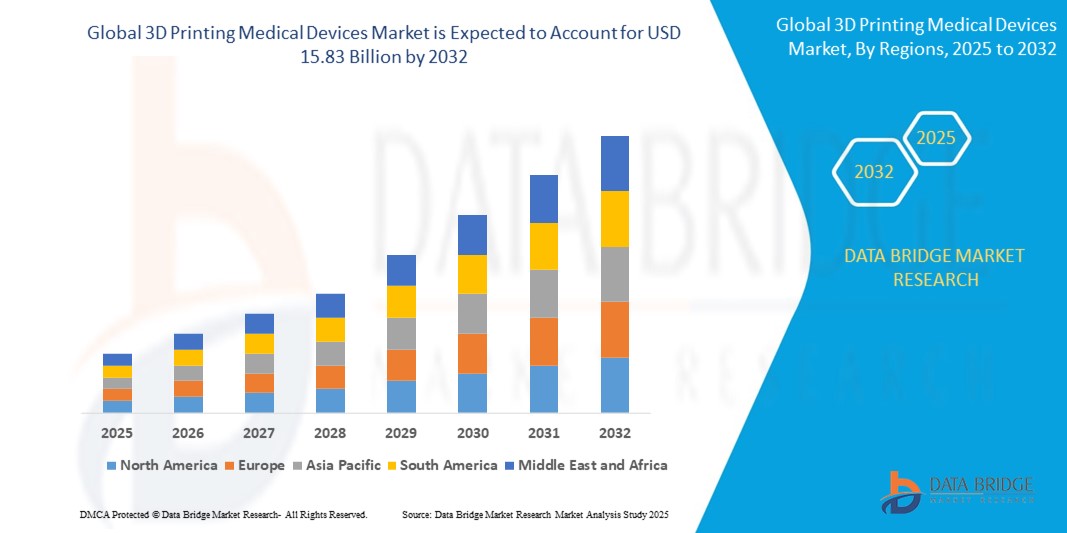

- The global 3D printing medical devices market size was valued at USD 4.01 billion in 2024 and is expected to reach USD 15.83 billion by 2032, at a CAGR of 18.72% during the forecast period

- The market growth is largely fueled by advancements in biocompatible materials and rising demand for patient-specific medical solutions

- Increasing adoption of customized prosthetics, orthopedic implants, and dental devices is improving clinical outcomes and enhancing patient comfort and satisfaction

- Continuous innovations in 3D printing technologies, such as bio-printing and multi-material printing, are enabling the production of complex, high-precision medical devices at reduced costs and lead times

3D Printing Medical Devices Market Analysis

- The 3D printing medical devices market is witnessing strong growth due to the increasing integration of advanced printing technologies that enable the production of highly customized medical solutions tailored to individual patient needs

- This trend is reshaping the healthcare manufacturing landscape by allowing faster prototyping, reduced waste, and cost-effective small-batch production of complex medical components

- North America dominates the 3d printing medical devices market with the share of 45.05% in 2024, driven by rapid technological advancements and strong investment in personalized healthcare solutions

- Asia-pacific is expected to be the fastest growing region in the 3d printing medical devices market during the forecast period due to increasing urbanization and rising [VL1] [MS2] disposable incomes

- The custom prosthetics and implants segment dominates the market share of 55.05% in 2024, attributed to the increasing demand for patient-specific solutions that enhance fit, comfort, and clinical outcomes

Report Scope and 3D Printing Medical Devices Market Segmentation

|

Attributes |

3D Printing Medical Devices Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, geographically represented company-wise production and capacity, network layouts of distributors and partners, detailed and updated price trend analysis and deficit analysis of supply chain and demand. |

3D Printing Medical Devices Market Trends

“Rise of Personalized Solutions in Medical Device Printing”

- The current market for 3D printing medical devices is increasingly shaped by the trend of patient-specific customization in medical care

- Healthcare providers are adopting 3D printing technologies to design implants and instruments tailored to individual anatomical needs

- This trend supports faster treatment planning and enhances surgical precision by offering better fitting medical components

- Customization also reduces the risk of complications and improves patient recovery times through more effective device performance

- Manufacturers are investing in research and development to expand the range of customizable materials and designs in line with patient-specific demands

- In conclusion, this growing emphasis on personalization is setting a new standard in medical device manufacturing, aligning technology with the need for better patient outcomes and efficient healthcare delivery

3D Printing Medical Devices Market Dynamics

Driver

“Growing Demand for Patient-Specific Medical Solutions”

- Rising demand for patient-specific medical solutions is driving the adoption of 3D printing in healthcare as it enables the creation of implants and surgical tools tailored to individual anatomy using imaging data such as computed tomography and magnetic resonance imaging

- Customization through 3D printing enhances surgical precision and patient comfort by improving device fit and clinical outcomes with reduced recovery time

- For instance, Mayo Clinic uses 3D-printed anatomical models to plan complex surgeries improving both accuracy and success rates in real time scenarios

- The dental and orthopedic sectors are seeing increased use of 3D printing with companies like Align Technology producing millions of customized dental aligners annually based on patient-specific data

- 3D printing accelerates design-to-delivery timelines allowing rapid production in emergency or time-sensitive situations while cutting down on excess inventory and waste

- In conclusion, this growing adoption is transforming traditional medical manufacturing into a more agile and patient-centered approach aligned with the future of personalized care

Restraint/Challenge

“High Regulatory and Quality Compliance Burden”

- The 3D printing medical devices market faces a major challenge in navigating strict regulatory and quality compliance standards due to the highly customized nature of the products

- Unlike traditional manufacturing where uniform devices can be mass-produced patient-specific devices vary in shape design and material requiring individual assessment and documentation

- For instance, the U.S. Food and Drug Administration has issued guidelines for 3D printed devices but real-time product approvals still demand rigorous validation processes which can delay market entry

- Hospital-based 3D printing labs face additional difficulties in meeting centralized regulatory standards due to decentralized workflows and variable oversight structures

- Variability in printer technologies materials and settings can lead to inconsistent product outcomes making it necessary for manufacturers to conduct extensive quality checks and testing

- In conclusion, these regulatory and quality barriers raise development costs limit scalability and create entry obstacles especially for smaller players slowing down broader adoption despite technological advancements

3D Printing Medical Devices Market Scope

The market is segmented on the basis of product, technology, application, and end user.

- By Product

On the basis of product, the 3D printing medical devices market is segmented into equipment, materials, and services and software. The equipment segment dominates the largest market revenue share in 2024, driven by widespread use of 3D printers in hospital-based labs, research institutions, and manufacturing setups. These machines are essential for producing prototypes, patient-specific models, and final-use devices, making them central to the workflow. Demand remains strong due to continuous advancements in printer precision, multi-material capabilities, and affordability.

The software segment is anticipated to witness the fastest growth rate from 2025 to 2032, supported by the growing need for specialized design tools and simulation programs. These software solutions enable highly accurate modeling of complex anatomical structures, which improves surgical planning and reduces trial-and-error in device development.

- By Technology

On the basis of technology, the 3D printing medical devices market is segmented into laser beam melting, photopolymerization, droplet deposition/extrusion-based technologies, electron beam melting, three-dimensional printing/adhesion bonding/binder jetting, and other technologies. The photopolymerization segment dominates the market share of 48.05% in 2024, favored for its high resolution and suitability for dental, prosthetic, and hearing aid applications. It offers excellent surface finish and dimensional accuracy, which are essential for devices with intricate designs.

The laser beam melting segment is anticipated to witness the fastest growth rate from 2025 to 2032, driven by its ability to process high-strength metals such as titanium and cobalt-chrome. This makes it ideal for orthopedic implants and complex surgical instruments that demand durability and precision.

- By Application

On the basis of application, the 3D printing medical devices market is segmented into surgical guides, surgical instruments, standard prosthetics and implants, custom prosthetics and implants, tissue-engineered products, hearing aids, wearable medical devices, and other applications. The custom prosthetics and implants segment dominates the market share of 55.05% in 2024, attributed to the increasing demand for patient-specific solutions that enhance fit, comfort, and clinical outcomes. These applications are widely adopted in orthopedics, cranial surgeries, and dental care.

The tissue-engineered products segment is expected to register the fastest growth from 2025 to 2032, driven by ongoing advancements in bio-printing and regenerative medicine. Research institutions and biotech firms are increasingly exploring the creation of tissue scaffolds and organ models using 3D printing, aiming to address long-term shortages in transplant materials.

- By End User

On the basis of end user, the 3D printing medical devices market is segmented into hospitals and surgical centers, dental and orthopedic clinics, academic institutions and research laboratories, pharma-biotech and medical device companies, clinical research organizations. The hospitals and surgical centers segment dominates the largest market revenue share in 2024, supported by the growing integration of in-house 3D printing labs that support pre-surgical planning, anatomical modeling, and implant fabrication. These centers benefit from faster patient turnaround and cost savings.

The academic institutions and research laboratories segment is anticipated to grow at the fastest rate from 2025 to 2032, as universities and research groups increasingly adopt 3D printing for innovation, prototyping, and experimental procedures. Government grants and academic-industry collaborations further support this growth.

3D Printing Medical Devices Market Regional Analysis

- North America dominates the 3D printing medical devices market with the share of 45.05% in 2024, driven by rapid technological advancements and strong investment in personalized healthcare solutions

- The region benefits from the presence of major medical device manufacturers and research institutions that actively adopt 3D printing for developing patient-specific implants, prosthetics, and surgical instruments

- Strong regulatory support, increasing healthcare expenditure, and the widespread integration of advanced imaging technologies such as computed tomography and magnetic resonance imaging further boost the clinical application of 3D printed solutions

U.S. 3D Printing Medical Devices Market Insight

The U.S. 3D printing medical devices market scope is extensive, driven by advanced healthcare infrastructure and rapid adoption of innovative printing technologies across hospitals and research centers. Integration of 3D printing for custom implants, surgical tools, and prosthetics is expanding patient-specific care capabilities. Collaboration between medical device companies and technology firms is fostering new material developments and design software tailored for medical applications. The growing presence of in-house 3D printing labs in hospitals is also broadening access and speeding treatment workflows, enhancing the overall market potential.

Europe 3D Printing Medical Devices Market Insight

The European market scope for 3D printing medical devices includes strong emphasis on regulatory compliance and technological innovation, supporting adoption across clinical and manufacturing settings with market share of 29.10% in 2024. The market covers custom prosthetics, implants, and tissue-engineered products, meeting stringent safety and quality standards. Growth is supported by collaborative research between academia and industry, with focus on sustainable and biocompatible materials. Expansion into new applications like wearable medical devices is also broadening the regional scope, alongside established surgical and dental applications.

U.K. 3D Printing Medical Devices Market Insight

In the U.K., the market scope for 3D printing medical devices is shaped by increasing demand for personalized healthcare solutions and technological integration within the National Health Service. Focus areas include custom surgical guides, implants, and prosthetics, with growing use of advanced software for anatomical modeling. Public-private partnerships and innovation funding support expansion in research and clinical adoption, increasing market reach in both hospital and specialized clinic environments.

Germany 3D Printing Medical Devices Market Insight

Germany’s 3D printing medical devices market scope is underpinned by a strong industrial base and commitment to innovation and sustainability. The market spans custom orthopedic implants, surgical instruments, and bio-printing research, with emphasis on eco-friendly materials and precise manufacturing. Well-established healthcare infrastructure and integration of automated production systems are enhancing device quality and availability, widening applications across hospital and outpatient care sectors.

Asia-Pacific 3D Printing Medical Devices Market Insight

The Asia-Pacific market scope is rapidly expanding due to rising healthcare investments and technological modernization in countries like China, Japan, and India. The region is seeing broad adoption in custom prosthetics, dental devices, and emerging bio-printing fields. Government initiatives promoting digital health and smart manufacturing increase accessibility to 3D printing services. The manufacturing hub status also supports cost-effective device production and wider distribution, enhancing market penetration across urban and rural healthcare centers.

Japan 3D Printing Medical Devices Market Insight

Japan’s market scope focuses on leveraging advanced technology culture and aging population needs to drive demand for customized medical devices. Key segments include patient-specific implants, surgical tools, and integration with Internet of Things healthcare devices. Emphasis on precision, ease of use, and security aligns with the country’s healthcare priorities, promoting growth in hospitals, eldercare facilities, and research institutions.

China 3D Printing Medical Devices Market Insight

China’s market scope encompasses a large and growing base driven by urbanization, expanding middle class, and state-supported smart city projects. The focus is on affordable, scalable production of custom prosthetics, implants, and surgical models. Domestic manufacturers and healthcare providers collaborate to improve quality and accessibility. The strong ecosystem of 3D printing hardware and material suppliers supports rapid innovation and adoption in both residential and commercial medical settings.

3D Printing Medical Devices Market Share

The 3D Printing Medical Devices industry is primarily led by well-established companies, including:

- Stratasys Ltd. (Israel)

- EnvisionTEC (U.S.)

- Koninklijke Philips N.V. (Netherlands)

- 3D Systems, Inc. (U.S.)

- EOS (U.S.)

- Renishaw plc (U.K.)

- Materialise (Belgium)

- 3T Additive Manufacturing Ltd. (U.S.)

- GENERAL ELECTRIC COMPANY (U.S.)

- Carbon, Inc. (U.S.)

- Prodways Group (France)

- SLM Solutions (Germany)

- Organovo Holdings Inc. (U.S.)

- Anatomics Pty Ltd (Australia)

- Groupe Gorgé (France)

- Cyfuse Biomedical K.K. (Tokyo)

- FIT AG (Germany)

- Wacker Chemie AG (Germany)

Latest Developments in Global 3D Printing Medical Devices Market

- In August 2023, Materialise opened a new 3D printing facility in Plymouth, Michigan to speed up the delivery of patient-specific medical implants. The facility will focus on 3D printing personalized titanium craniomaxillofacial (CMF) implants, which are used in facial reconstructive surgeries

- In June 2023, Precision ADM, Orthopaedic Innovation Centre (OIC), Tecomet, and EOS announced a partnership to provide an end-to-end solution for medical device additive manufacturing. The partnership will enable rapid development of additively manufactured medical devices

- In September 2020, nTopology (U.S.) raised funding of USD 40 million for the development of the nTop software platform for additive manufacturing processes. This will prove to be profitable in the long run

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global 3d Printing Medical Devices Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global 3d Printing Medical Devices Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global 3d Printing Medical Devices Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.