Global 5g Substrate Materials Market

Market Size in USD Million

USD

408.52 Million

USD

2,595.30 Million

2025

2033

USD

408.52 Million

USD

2,595.30 Million

2025

2033

| 2026 - 2033 | |

| USD 408.52 Million | |

| USD 2,595.30 Million | |

| % | |

|

5G Substrate Materials Market Size

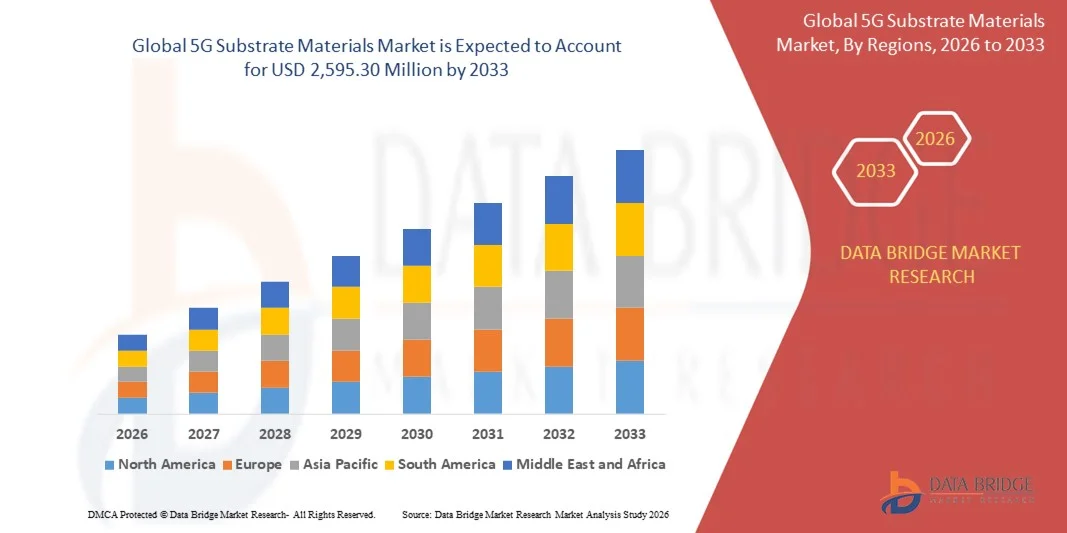

- The global 5G substrate materials market size was valued at USD 408.52 million in 2025 and is expected to reach USD 2,595.30 million by 2033, at a CAGR of 26.00% during the forecast period

- The market growth is largely fuelled by the rapid deployment of 5G networks, increasing demand for high-speed data transmission, and the rising adoption of advanced communication devices

- Growing investment in next-generation mobile infrastructure and expansion of data centers are further driving demand for high-performance substrate materials

5G Substrate Materials Market Analysis

- Increasing focus on low-loss, high-reliability substrates for 5G applications is fostering innovation and product development in the market

- The trend toward compact, high-performance electronics and growing adoption of mmWave and massive MIMO technologies are shaping market dynamics

- North America dominated the 5G substrate materials market with the largest revenue share in 2025, driven by rapid 5G network deployment, increasing adoption of high-frequency devices, and strong technological infrastructure

- Asia-Pacific region is expected to witness the highest growth rate in the global 5G substrate materials market, driven by increasing urbanization, rising demand for high-speed connectivity, and rapid adoption of 5G technology in countries such as China, Japan, and South Korea

- The Organic Laminates segment held the largest market revenue share in 2025, driven by their excellent signal integrity, low dielectric loss, and ease of mass production. Organic laminates are widely used in base station modules and smartphone PCBs, providing cost-effective solutions with consistent high-frequency performance

Report Scope and 5G Substrate Materials Market Segmentation

|

Attributes |

5G Substrate Materials Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

5G Substrate Materials Market Trends

Advancements in High-Performance Substrate Materials for 5G

- The increasing demand for high-performance substrate materials is transforming the 5G ecosystem by enabling faster signal transmission, higher bandwidth, and improved device efficiency. Advanced materials such as high-frequency laminates and low-loss substrates are critical for supporting next-generation network infrastructure, enhancing connectivity, and reducing signal attenuation. This trend is further driven by the need for miniaturized devices and lightweight components in consumer electronics and telecom hardware

- Growing deployment of 5G base stations and small cell networks is accelerating the adoption of advanced substrate materials across telecom and electronics industries. These materials are particularly essential in urban areas and high-density deployments, ensuring consistent network performance and reliability. Continuous innovation in substrate design is helping meet the increasing data traffic demands and diverse application requirements

- The affordability and scalability of novel substrate materials, including Rogers, PTFE, and composite laminates, are encouraging widespread adoption in consumer electronics, telecom equipment, and automotive applications. Manufacturers benefit from consistent material quality and enhanced signal integrity, supporting large-scale production. In addition, improved thermal stability and mechanical strength of these materials extend device longevity and reduce maintenance costs

- For instance, in 2023, several telecom equipment manufacturers in North America and Europe reported increased use of high-frequency laminates for 5G antennas and modules, resulting in improved device performance and network efficiency. Enhanced material properties also enabled better integration of complex circuit designs for high-speed applications

- While advanced substrate materials are driving 5G deployment, market growth depends on continued R&D, cost optimization, and integration with emerging technologies. Material suppliers must focus on innovation, standardized quality, and strategic partnerships to fully capitalize on this trend. Long-term adoption will also rely on addressing environmental sustainability and recyclability of substrate materials

5G Substrate Materials Market Dynamics

Driver

Rapid Expansion of 5G Infrastructure and Rising Demand for High-Speed Connectivity

- The global rollout of 5G networks is driving the adoption of advanced substrate materials, as telecom operators require high-performance components to support faster data transfer, low latency, and massive connectivity. This has accelerated investments in substrate research and production. Growing consumer demand for seamless connectivity and cloud-based services further reinforces the need for reliable substrate solutions

- Manufacturers are increasingly integrating advanced substrates in smartphones, base stations, and IoT devices to meet growing consumer and enterprise demand for seamless connectivity. This is fostering innovation in low-loss laminates, high-frequency PCBs, and hybrid material solutions. In addition, compatibility with next-generation wireless standards such as mmWave and sub-6GHz bands is pushing material enhancements

- Government initiatives and private sector investments to expand 5G coverage in emerging and developed markets are further boosting substrate demand. Programs supporting smart cities, autonomous vehicles, and industrial automation are increasing reliance on advanced materials. Strategic partnerships between network operators and material suppliers are also accelerating product development cycles

- For instance, in 2022, several Asian countries, including China and South Korea, launched 5G expansion projects using advanced substrate solutions to improve network reliability and coverage. The adoption of high-performance substrates in telecom hubs has led to reduced signal loss and better energy efficiency in large-scale deployments

- While 5G adoption is fueling demand, there is a need for materials with better thermal stability, miniaturization compatibility, and cost-efficiency to ensure sustainable growth. Continuous innovation in material chemistry and laminating processes is critical to meet evolving market requirements

Restraint/Challenge

High Cost of Advanced Substrate Materials and Manufacturing Complexity

- The high price of specialty substrate materials, such as PTFE composites and ceramic-filled laminates, limits accessibility for smaller device manufacturers and emerging market telecom operators. Cost remains a key barrier to widespread adoption. In addition, limited availability of high-quality raw materials further exacerbates pricing pressures for end manufacturers

- Complex manufacturing processes and stringent quality control requirements increase production challenges and can lead to delays in scaling operations. Precision in material formulation and laminating techniques is critical for ensuring performance consistency. Manufacturing defects or minor variations in substrate properties can significantly impact high-frequency signal transmission, increasing rejection rates

- Supply chain constraints, including raw material shortages and reliance on specialized equipment, affect timely delivery and large-scale deployment. This is particularly impactful in regions with nascent 5G infrastructure or limited local manufacturing capabilities. Global disruptions, including geopolitical tensions or natural disasters, may further constrain the supply chain and slow market expansion

- For instance, in 2023, several European and North American telecom equipment suppliers reported delays in procurement of high-frequency laminates due to global supply chain disruptions. These delays not only affected production schedules but also delayed the launch of 5G-enabled devices and network equipment

- While material innovations continue, addressing cost pressures, process complexity, and supply chain resilience is essential. Stakeholders must invest in efficient production, material standardization, and strategic sourcing to unlock long-term market potential. Collaboration between substrate manufacturers, telecom providers, and equipment makers will be critical to sustaining growth and meeting global 5G deployment targets

5G Substrate Materials Market Scope

The market is segmented on the basis of substrate type and application.

- By Substrate Type

On the basis of substrate type, the 5G substrate materials market is segmented into Organic Laminates, Ceramics, Glass, and Others. The Organic Laminates segment held the largest market revenue share in 2025, driven by their excellent signal integrity, low dielectric loss, and ease of mass production. Organic laminates are widely used in base station modules and smartphone PCBs, providing cost-effective solutions with consistent high-frequency performance.

The Ceramics segment is expected to witness the fastest growth rate from 2026 to 2033, propelled by their superior thermal stability, mechanical strength, and low signal attenuation at high frequencies. Ceramic substrates are increasingly preferred for high-performance 5G antennas and critical telecom equipment, enabling compact designs and reliable operation in dense network deployments.

- By Application

On the basis of application, the market is segmented into Base Station Antennas and Smartphone Antennas. The Base Station Antennas segment held the largest market revenue share in 2025, driven by rapid deployment of 5G infrastructure globally and the need for durable, high-frequency materials in telecom towers. Base station applications require substrates that support massive MIMO and small cell networks, ensuring stable and efficient network coverage.

The Smartphone Antennas segment is expected to witness the fastest growth rate from 2026 to 2033, driven by increasing smartphone penetration and consumer demand for faster, high-bandwidth mobile connectivity. Substrates for smartphone antennas must balance miniaturization, high-frequency performance, and low power loss, which is accelerating the adoption of advanced laminates and ceramic-based materials.

5G Substrate Materials Market Regional Analysis

- North America dominated the 5G substrate materials market with the largest revenue share in 2025, driven by rapid 5G network deployment, increasing adoption of high-frequency devices, and strong technological infrastructure

- The region’s advanced telecom ecosystem, combined with high demand for low-latency communication and high-speed connectivity, is propelling investments in advanced substrate materials

- High adoption of smartphones, IoT devices, and base stations further supports the growth of the 5G substrate materials market, establishing North America as a leading hub for innovation and production

U.S. 5G Substrate Materials Market Insight

The U.S. 5G substrate materials market captured the largest revenue share in 2025 within North America, fueled by the accelerated rollout of 5G infrastructure and rising demand for high-performance electronic components. Telecom operators and smartphone manufacturers are increasingly investing in advanced substrates to support enhanced bandwidth, low latency, and high-frequency applications. Furthermore, growing government and private sector initiatives aimed at smart cities and industrial automation are significantly contributing to market expansion.

Europe 5G Substrate Materials Market Insight

The Europe 5G substrate materials market is expected to witness the fastest growth rate from 2026 to 2033, driven by increasing government support for 5G adoption and the need for advanced telecommunication infrastructure. The region is also focusing on energy-efficient, low-loss substrates to meet sustainability and performance requirements. Key countries such as Germany, France, and the U.K. are investing in 5G networks and encouraging innovation in substrate technologies, fostering significant market growth across both consumer electronics and telecom equipment segments.

U.K. 5G Substrate Materials Market Insight

The U.K. 5G substrate materials market is expected to witness robust growth from 2026 to 2033, propelled by the rising adoption of 5G-enabled devices and network expansion projects. Increased focus on digital transformation, IoT applications, and smart city initiatives is stimulating demand for high-performance substrate materials. Furthermore, strong research and development capabilities and collaborations between manufacturers and telecom providers are expected to accelerate market penetration and technological advancement.

Germany 5G Substrate Materials Market Insight

The Germany 5G substrate materials market is expected to witness significant growth from 2026 to 2033, fueled by investments in 5G infrastructure, industrial automation, and connected technologies. The country’s emphasis on innovation and advanced manufacturing capabilities supports the adoption of high-frequency laminates, low-loss substrates, and hybrid materials. Integration of these materials in both telecom and consumer electronics applications is driving demand, with a particular focus on performance, reliability, and sustainability.

Asia-Pacific 5G Substrate Materials Market Insight

The Asia-Pacific 5G substrate materials market is expected to witness the fastest growth rate from 2026 to 2033, driven by rapid urbanization, rising smartphone penetration, and large-scale deployment of 5G base stations in countries such as China, Japan, and South Korea. Government initiatives promoting digitalization, smart cities, and IoT infrastructure are further accelerating the adoption of high-performance substrates. In addition, the region is emerging as a manufacturing hub for advanced substrate materials, improving affordability and accessibility for telecom and consumer electronics companies.

Japan 5G Substrate Materials Market Insight

The Japan 5G substrate materials market is expected to witness strong growth from 2026 to 2033 due to high technological adoption, extensive 5G infrastructure expansion, and increasing demand for connected devices. Japanese manufacturers are investing in low-loss, high-frequency laminates to enhance network performance, IoT applications, and industrial automation. Furthermore, integration of these materials into smartphones, automotive electronics, and base station antennas is fueling the market, while aging populations drive demand for reliable, high-speed connectivity solutions in residential and commercial sectors.

China 5G Substrate Materials Market Insight

The China 5G substrate materials market accounted for the largest market revenue share in Asia-Pacific in 2025, attributed to massive 5G rollout, rapid urbanization, and strong government support for digital infrastructure. China is a leading market for high-frequency laminates and advanced substrate materials, with widespread adoption in base station antennas, smartphones, and consumer electronics. Availability of domestic manufacturers and competitive pricing further propel market growth, positioning China as a key driver in the global 5G substrate materials industry.

5G Substrate Materials Market Share

The 5G Substrate Materials industry is primarily led by well-established companies, including:

- Showa Denko Materials Co., Ltd. (Japan)

- DuPont (U.S.)

- BASF SE (Germany)

- AGC Inc. (Japan)

- Taiwan Union Technology Corporation (Taiwan)

- Kuraray Europe GmbH (Germany)

- Avient Corporation (U.S.)

- Rogers Corporation (U.S.)

- DAIKIN INDUSTRIES, Ltd. (Japan)

- Panasonic Corporation (Japan)

- ITEQ CORPORATION (Taiwan)

- KANEKA CORPORATION (Japan)

- The Chemours Company (U.S.)

- Ventec International Group (Taiwan)

- TORAY INDUSTRIES, INC. (Japan)

- ZTE Corporation (China)

- KYOCERA Corporation (Japan)

- Murata Manufacturing Co., Ltd. (Japan)

- MARUWA Co., Ltd. (Japan)

- KOA Corporation (Japan)

Latest Developments in Global 5G Substrate Materials Market

- In March 2025, DuPont launched the Riston DWB8100M dry film photoresist, an advanced direct imaging material designed for fine copper pillar and thick copper mSAP (modified semi-additive process) applications. The material enhances fine line and via resolution, provides robust bottom adhesion to reduce underplating risks, and ensures consistent yield stability. By enabling precise copper trace profiles with minimal voids, it supports next-generation IC substrate manufacturing. This development is expected to improve production reliability and efficiency, positively impacting the 5G substrate materials market

- In May 2024, leading companies in antenna packaging technologies introduced innovations to tackle signal attenuation challenges in high-frequency 5G millimeter-wave (mmWave) systems and emerging 6G networks. These advancements aim to enhance signal integrity, reduce transmission losses, and ensure reliable wireless performance. The improvements are expected to accelerate the deployment of next-generation communication devices, boosting demand for advanced substrate materials in telecom and electronics industries

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global 5g Substrate Materials Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global 5g Substrate Materials Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global 5g Substrate Materials Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.