Global Aarskog Syndrome Treatment Market

Market Size in USD Billion

USD

3.70 Billion

USD

5.06 Billion

2025

2033

USD

3.70 Billion

USD

5.06 Billion

2025

2033

| 2026 - 2033 | |

| USD 3.70 Billion | |

| USD 5.06 Billion | |

| % | |

|

Aarskog Syndrome Treatment Market Size

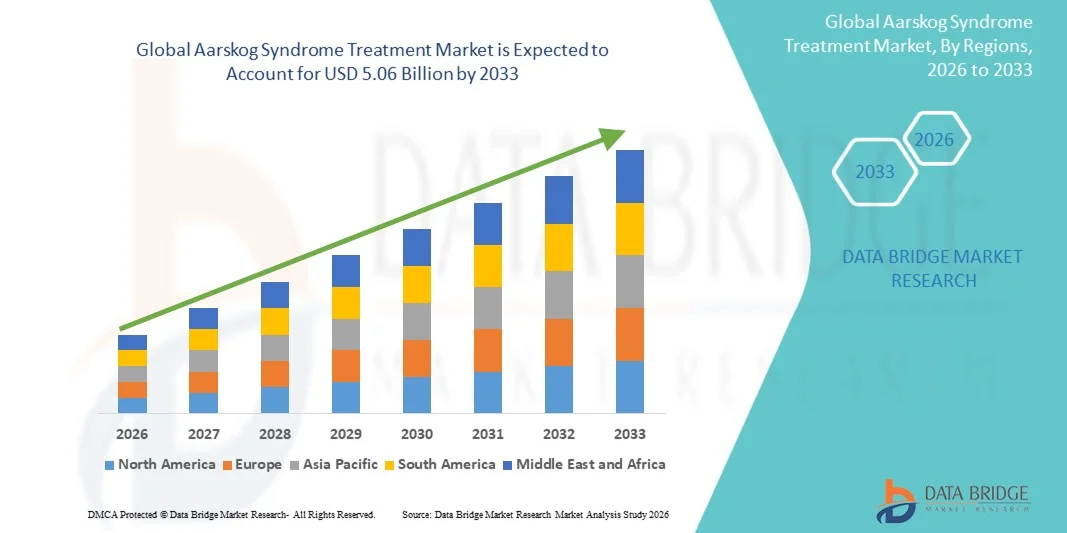

- The global aarskog syndrome treatment market size was valued at USD 3.70 billion in 2025 and is expected to reach USD 5.06 billion by 2033, at a CAGR of 4.00% during the forecast period

- The growth of the Aarskog Syndrome Treatment Market is largely fueled by increasing awareness of rare genetic disorders, advancements in diagnostic technologies, and the development of targeted therapeutic interventions. Rising investments in pediatric healthcare infrastructure and genetic research are supporting early diagnosis and effective management of the syndrome, which is crucial for improving patient outcomes

- Furthermore, growing patient advocacy, improved access to specialized treatment centers, and increasing collaborations between pharmaceutical companies and research institutions are significantly boosting the market's expansion. These converging factors are accelerating the uptake of innovative treatments and care solutions for Aarskog Syndrome, thereby driving substantial growth in the industry

Aarskog Syndrome Treatment Market Analysis

- Aarskog Syndrome Treatment, encompassing specialized therapies and early intervention strategies, is increasingly vital in improving patient outcomes and managing congenital disorder symptoms due to enhanced diagnostic methods, targeted medications, and supportive care

- The escalating demand for Aarskog Syndrome Treatment is primarily fueled by growing awareness among healthcare professionals and patients, increasing access to pediatric and genetic disorder care, and a rising preference for early diagnosis and intervention

- North America dominated the aarskog syndrome treatment market with the largest revenue share of approximately 41% in 2025, supported by advanced healthcare infrastructure, high disease awareness, and strong availability of specialized diagnostic and therapeutic solutions. The U.S. experienced substantial growth due to early diagnosis, increasing adoption of novel therapies, and expanded access to specialized hematology and genetic disorder centers

- Asia-Pacific is projected to be the fastest-growing region in the aarskog syndrome Treatment market during the forecast period, driven by rising healthcare expenditure, increasing prevalence of congenital disorders, improving access to specialized care, and growing awareness about early diagnosis and disease management

- The facial defect segment dominated the largest market revenue share of 45.8% in 2025, driven by the high prevalence of cleft lip, cleft palate, hypertelorism, and widow’s peak hairline in diagnosed patients

Report Scope and Aarskog Syndrome Treatment Market Segmentation

|

Attributes |

Aarskog Syndrome Treatment Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Aarskog Syndrome Treatment Market Trends

“Rising Focus on Early Diagnosis and Personalized Treatment Approaches”

- A significant trend in the global aarskog syndrome treatment market is the increasing focus on early diagnosis and personalized therapeutic strategies. Advancements in genetic testing and molecular diagnostics are enabling clinicians to identify patients with Aarskog Syndrome earlier, which allows for timely interventions and better outcomes

- For instance, multidisciplinary clinics are adopting standardized screening protocols for at-risk populations to ensure early detection of growth, skeletal, and facial anomalies associated with the condition

- The development of patient-specific care plans, including customized medication regimens, physiotherapy, and surgical interventions, is reshaping treatment approaches

- Enhanced diagnostic capabilities are enabling physicians to monitor progression and tailor interventions based on individual genetic profiles and symptom severity

- Research institutions are investing in studies to better understand genotype-phenotype correlations, which support personalized treatment options

- The trend towards individualized therapy improves quality of life by targeting specific symptoms such as short stature, skeletal deformities, and cardiovascular anomalies

- Clinical guidelines are evolving to incorporate early intervention strategies that combine pharmacological, surgical, and supportive therapies

- Early diagnosis programs are being supported by increased awareness among healthcare professionals and patient advocacy groups

- Parental education programs help families recognize symptoms sooner, leading to faster treatment initiation

Aarskog Syndrome Treatment Market Dynamics

Driver

“Growing Demand for Comprehensive Clinical Management and Supportive Therapies”

- The increasing prevalence of Aarskog Syndrome and rising awareness about effective management options is driving market growth. Patients and caregivers are seeking comprehensive treatment plans that address both primary symptoms and associated complications

- For instance, the integration of physiotherapy, orthopedic interventions, and pharmacological treatment in coordinated care models enhances patient outcomes and supports functional independence

- Healthcare providers are emphasizing holistic care approaches that combine medical, surgical, and supportive therapies to manage the diverse manifestations of the syndrome

- Rising access to specialized clinics and centers of excellence is facilitating the delivery of high-quality care and contributing to market expansion

- Medical education initiatives and advocacy programs are increasing awareness of treatment options among healthcare professionals, thereby encouraging early referral and intervention

- The availability of multiple therapeutic modalities, such as corticosteroids, growth-promoting agents, and surgical procedures, supports personalized treatment plans

- Insurance coverage and government healthcare programs are improving patient access to these therapies, particularly in developed regions. Clinical collaborations and partnerships are expanding research and availability of novel treatment strategies

- Patient demand for improved quality of life and functional outcomes drives adoption of combination therapies. Enhanced follow-up and monitoring programs ensure better adherence and long-term management, supporting market growth

Restraint/Challenge

“Limited Awareness, High Treatment Costs, and Variability in Access to Care”

- Despite advancements in diagnosis and treatment, limited awareness of Aarskog Syndrome among general practitioners and rural healthcare providers poses a significant challenge to timely intervention

- For instance, a 2024 report from the European Reference Network highlighted delayed diagnosis in over 40% of patients due to low awareness among primary care physicians

- In many regions, late or missed diagnosis delays treatment, reducing clinical efficacy and contributing to poor patient outcomes. The relatively high cost of genetic testing, specialized medications, and surgical interventions can be prohibitive for patients, particularly in developing countries or for uninsured population

- Availability of multidisciplinary care is often limited to major urban centers, making access difficult for patients in remote areas

- Inconsistent insurance coverage and reimbursement policies for specialized therapies further constrain patient access

- The rarity of the syndrome limits large-scale clinical trials, creating gaps in evidence for treatment efficacy and optimal protocols

- High variability in symptom severity requires individualized treatment, increasing complexity and costs of care

- Patient adherence can be affected by long-term treatment requirements and frequent clinical visits

- Healthcare infrastructure limitations in emerging markets restrict adoption of advanced therapies

- Educational initiatives targeting healthcare providers are required to improve early diagnosis and treatment uptake

Aarskog Syndrome Treatment Market Scope

The market is segmented on the basis of defect type, treatment, symptoms, diagnosis, end-users, and distribution channel.

• By Defect Type

On the basis of defect type, the Aarskog Syndrome Treatment market is segmented into facial, limb, genital, and others. The facial defect segment dominated the largest market revenue share of 45.8% in 2025, driven by the high prevalence of cleft lip, cleft palate, hypertelorism, and widow’s peak hairline in diagnosed patients. Early detection and corrective surgeries for facial anomalies are prioritized due to their significant impact on patient quality of life, aesthetics, and social interaction. Advanced surgical interventions and supportive therapies are widely adopted in developed regions, contributing to strong demand. Clinics and hospitals invest in specialized craniofacial teams to manage complex facial deformities, and increasing awareness among parents and caregivers boosts early intervention. The segment also benefits from government and non-profit support programs promoting congenital facial defect correction. Genetic testing advances facilitate targeted treatment planning, enhancing treatment outcomes. Awareness campaigns and clinical guidelines reinforce early management strategies. The growing adoption of multidisciplinary treatment approaches in pediatric and surgical care further strengthens the segment. Global collaborations in craniofacial research improve surgical techniques and postoperative care. Insurance coverage for facial defect correction also promotes accessibility and adoption. Educational initiatives on congenital facial anomalies enhance early diagnosis rates. Technological advances in surgical planning and minimally invasive techniques support long-term market growth.

The genital defect segment is expected to witness the fastest CAGR of 19.3% from 2026 to 2033, fueled by increasing detection of cryptorchidism and other genital anomalies in newborns and young children. Rising awareness among parents and healthcare providers about the importance of early intervention is contributing to higher treatment adoption. Minimally invasive surgical techniques, coupled with postoperative monitoring, are gaining preference due to reduced recovery time and complications. The segment also benefits from growth hormone therapy integration to support developmental outcomes alongside corrective surgery. Emerging markets are witnessing increased investments in pediatric surgical centers, expanding treatment accessibility. The availability of genetic testing enhances early diagnosis and individualized care planning. Supportive therapies and follow-up programs improve overall patient outcomes and encourage adoption. Awareness campaigns by pediatric associations and patient advocacy groups boost early detection and treatment compliance. Insurance coverage and government-funded healthcare programs are gradually expanding to include genital defect correction procedures. Rising research focus on congenital genital anomalies contributes to clinical innovation. Technological advancements in surgical tools and imaging techniques improve procedural precision. Early intervention initiatives in neonatal care units further drive segment growth.

• By Treatment

On the basis of treatment, the market is segmented into inguinal hernia repair surgery, growth hormone therapy, cryptorchidism surgery, cleft lip or palate surgery, nystagmus treatment, strabismus treatment, and auxiliary treatment. The cleft lip or palate surgery segment dominated with 42.6% revenue share in 2025, driven by the high prevalence of these congenital anomalies. Surgical correction is often combined with speech therapy and orthodontic management, enhancing patient outcomes. Early corrective surgery reduces long-term complications and improves social integration. Developed regions benefit from well-established craniofacial surgical centers with advanced facilities. Awareness campaigns by NGOs and pediatric healthcare networks improve early detection and intervention rates. Government funding for pediatric surgeries enhances affordability. Technological advances in minimally invasive surgical techniques reduce operative risks and recovery time. Multidisciplinary teams, including surgeons, orthodontists, and speech therapists, provide comprehensive care. Genetic screening prior to surgery allows precise treatment planning. Rising parental awareness and proactive healthcare policies further drive adoption. Collaboration among pediatric hospitals enhances standardized treatment protocols. Clinical research on surgical outcomes improves success rates and long-term efficacy. Increasing number of specialized pediatric surgical centers globally boosts segment dominance.

The growth hormone therapy segment is anticipated to witness the fastest CAGR of 18.9% from 2026 to 2033, fueled by its role in managing short stature and developmental delays associated with Aarskog Syndrome. Increasing adoption in pediatric endocrinology clinics is contributing to rapid uptake. Clinical guidelines emphasize early initiation for optimal growth outcomes. Emerging markets are expanding access to hormone therapy through government and insurance programs. Rising awareness among parents and healthcare providers drives compliance and long-term treatment success. Availability of recombinant growth hormone and improved dosing regimens enhances patient outcomes. Integration with nutritional and physical therapy programs supports comprehensive management. Technological advancements in drug delivery methods improve patient adherence and convenience. Healthcare infrastructure improvements enable wider access to endocrinology services. Research in long-term efficacy and safety fosters confidence in therapy adoption. Public-private partnerships facilitate subsidized treatment access in low-income regions. Ongoing clinical trials for optimized growth hormone protocols contribute to future growth. Early diagnosis and treatment monitoring enhance therapy effectiveness and adoption rates.

• By Symptoms

On the basis of symptoms, the market is segmented into hypertelorism, philtrum, widow's peak hairline, brachydactyly, fifth finger clinodactyly, cutaneous syndactyly, cleft lip, cleft palate, and others. The hypertelorism segment dominated with 41.3% market share in 2025, due to its high visibility and associated psychological impact, prompting early surgical intervention. Multidisciplinary care combining surgical correction, ophthalmologic assessment, and genetic counseling supports high adoption. Awareness initiatives in pediatric and craniofacial clinics enhance detection rates. Government-supported health programs facilitate access to corrective procedures. Clinical guidelines recommend early management to prevent long-term functional and cosmetic issues. Technological advances in 3D imaging improve surgical planning and outcomes. Insurance coverage for craniofacial surgeries boosts accessibility. Increasing collaborations among pediatric centers improve standardized care. Parent and caregiver education supports timely intervention. Genetic testing aids in precise diagnosis and personalized treatment plans. Research initiatives improve surgical techniques and post-operative outcomes. Long-term monitoring and follow-up programs enhance quality of life for patients.

The brachydactyly segment is expected to witness the fastest CAGR of 17.8% from 2026 to 2033, driven by increasing demand for corrective orthopedic and reconstructive surgeries. Awareness of functional and cosmetic implications encourages early medical attention. Pediatric orthopedic clinics are expanding services for congenital hand anomalies. Surgical innovations and minimally invasive techniques improve recovery outcomes. Genetic testing facilitates targeted intervention. Parental education campaigns support early recognition and care adherence. Insurance coverage and government-funded healthcare programs are gradually including corrective procedures. Follow-up and rehabilitation programs enhance treatment success. Clinical research on congenital hand anomalies drives procedural improvements. Integration with supportive therapy programs optimizes outcomes. Emerging markets witness growing investments in pediatric orthopedic centers. Technological improvements in prosthetics and surgical tools support long-term growth. Early intervention initiatives further strengthen segment adoption.

• By Diagnosis

On the basis of diagnosis, the market is segmented into genetic testing, X-ray, and others. The genetic testing segment dominated with 44.5% revenue share in 2025, due to its role in early detection, risk assessment, and personalized treatment planning. Increasing awareness among healthcare providers and parents drives adoption. Integration with prenatal screening programs enhances early diagnosis rates. Advances in next-generation sequencing improve accuracy and reduce turnaround times. Government-funded genetic testing programs in developed countries facilitate accessibility. Multidisciplinary care teams rely on genetic insights to plan corrective treatments. Research collaborations improve mutation detection protocols. Clinical guidelines recommend early genetic testing for suspected cases. Insurance coverage in key markets supports widespread adoption. Public health campaigns raise awareness about the importance of genetic screening. Technological improvements reduce costs and enhance precision. Early detection allows timely therapeutic interventions, improving outcomes.

The X-ray segment is expected to witness the fastest CAGR of 16.7% from 2026 to 2033, driven by its accessibility, low cost, and utility in diagnosing skeletal anomalies associated with Aarskog Syndrome. Rising adoption in hospitals, clinics, and diagnostic centers supports growth. Integration with other imaging modalities improves diagnostic accuracy. Awareness campaigns by pediatric and orthopedic associations encourage early use. Technological advancements reduce radiation exposure and improve image clarity. Emerging markets are expanding access to radiology infrastructure. Insurance coverage and healthcare initiatives support X-ray adoption. Early skeletal assessment informs timely intervention planning. Orthopedic specialists rely on X-ray for treatment follow-up and progress monitoring. Increasing prevalence of congenital skeletal anomalies supports demand. Cost-effectiveness makes X-ray a preferred initial diagnostic tool. Research initiatives improve radiographic assessment techniques. Clinical integration with genetic testing enhances diagnostic accuracy.

• By End-Users

On the basis of end-users, the market is segmented into clinics, hospitals, surgical centers, and others. The hospitals segment dominated with 46.2% revenue share in 2025, owing to availability of multidisciplinary teams, advanced surgical infrastructure, and integrated pediatric care facilities. Hospitals offer comprehensive management, including surgery, therapy, and follow-up. Developed countries show strong adoption due to high hospital coverage and healthcare spending. Insurance coverage and government programs increase patient access. Research collaborations in hospitals improve treatment protocols. Patient education initiatives in hospitals support adherence. Clinical trials and pediatric care innovations enhance outcomes. Hospitals invest in advanced imaging, genetic testing, and rehabilitation services. Long-term monitoring programs improve quality of life. Partnerships with specialized clinics facilitate referrals. Telemedicine integration improves follow-up care. Awareness campaigns strengthen early detection and treatment adoption.

The surgical centers segment is anticipated to witness the fastest CAGR of 18.2% from 2026 to 2033, driven by rising investments in specialized pediatric and craniofacial surgical centers. Minimally invasive procedures, rapid recovery, and targeted interventions encourage adoption. Emerging markets are expanding specialized surgical services. Collaboration with hospitals and clinics enhances patient access. Technological advances in surgical equipment improve outcomes. Awareness among parents and healthcare providers boosts utilization. Insurance coverage and funding programs gradually support surgical centers. Integrated postoperative care programs improve adherence. Clinical research fosters innovation in pediatric surgical techniques. Telehealth and follow-up programs enhance patient management. High demand for individualized care promotes center expansion. Training programs increase specialized workforce availability. Early intervention initiatives drive adoption in private and urban settings.

• By Distribution Channel

On the basis of distribution channel, the market is segmented into hospital pharmacy, retail pharmacy, and online pharmacy. The hospital pharmacy segment dominated with 48.0% revenue share in 2025, owing to direct access to prescribed treatments, specialized medication management, and integration with inpatient and outpatient services. Hospitals ensure timely availability of medications for surgeries and supportive therapies. Government hospitals support subsidized access. Clinical teams collaborate with hospital pharmacies for treatment planning. Developed regions have standardized hospital pharmacy operations. Patient counseling and adherence programs are integrated. Research hospitals contribute to awareness and protocol adoption. Technology-enabled inventory management ensures consistent supply. Multidisciplinary care is streamlined through hospital pharmacies. Insurance coverage supports medication procurement. Pharmaceutical companies collaborate with hospitals for supply chain optimization. Hospitals play a critical role in ensuring treatment continuity.

The online pharmacy segment is expected to witness the fastest CAGR of 19.5% from 2026 to 2033, driven by rising e-commerce adoption, convenience, and increasing awareness of rare disease treatments. Online pharmacies provide access to specialized medications in remote regions. Subscription-based delivery and teleconsultation services improve adherence. Price transparency and discounts enhance affordability. Integration with digital healthcare platforms supports prescription verification. Emerging markets witness rapid growth in online pharmacy adoption. Patient education programs encourage online ordering for continuous therapy. Government and private initiatives enhance medication accessibility. Home delivery reduces treatment interruptions. Secure payment and delivery mechanisms improve trust. Research on rare disease drug supply chains supports online expansion. Partnerships with hospitals and clinics enable streamlined prescriptions. Growing smartphone penetration and internet access further boost adoption globally.

Aarskog Syndrome Treatment Market Regional Analysis

- North America dominated the aarskog syndrome treatment market with the largest revenue share of approximately 41% in 2025, supported by advanced healthcare infrastructure, high disease awareness, and strong availability of specialized diagnostic and therapeutic solutions

- The market experienced substantial growth due to early diagnosis, increasing adoption of novel therapies, and expanded access to specialized hematology and genetic disorder centers

- The presence of leading pharmaceutical companies and ongoing research initiatives further reinforces the region’s strong market position

U.S. Aarskog Syndrome Treatment Market Insight

The U.S. aarskog syndrome treatment market captured the largest revenue share within North America in 2025. The growth is fueled by widespread access to cutting-edge diagnostic tools, increased physician awareness, and government-supported early detection programs. Patients benefit from a range of specialized therapies, including growth hormone therapy, surgical interventions for congenital defects, and multidisciplinary care approaches, all contributing to a robust market expansion.

Europe Aarskog Syndrome Treatment Market Insight

The Europe aarskog syndrome treatment market is expected to witness steady growth throughout the forecast period. Key drivers include high patient awareness of congenital disorders, well-developed healthcare infrastructure, and increasing availability of advanced treatment modalities. Countries like Germany and the U.K. are actively implementing early diagnosis programs and expanding access to specialized care centers, ensuring timely intervention for patients.

U.K. Aarskog Syndrome Treatment Market Insight

The U.K. aarskog syndrome treatment market is projected to grow at a noteworthy CAGR, supported by government initiatives promoting congenital disorder awareness and early detection programs. Healthcare providers are increasingly adopting comprehensive treatment approaches, including surgical correction of physical anomalies and hormone therapies, which are improving patient outcomes and driving market adoption.

Germany Aarskog Syndrome Treatment Market Insight

Germany’s aarskog syndrome treatment market growth is expected to remain steady, driven by its advanced healthcare system, focus on research and development in genetic therapies, and high patient awareness. The country’s emphasis on innovation, preventive care, and personalized treatment plans enhances the accessibility and effectiveness of Aarskog Syndrome treatments.

Asia-Pacific Aarskog Syndrome Treatment Market Insight

The Asia-Pacific aarskog syndrome treatment market region is poised to register the fastest growth, supported by expanding healthcare infrastructure, rising per capita income, and increasing government focus on congenital disorder management. Nations such as China, Japan, and India are witnessing a surge in specialized clinics, improved diagnostic facilities, and greater patient awareness programs, which together contribute to rapid market expansion.

Japan Aarskog Syndrome Treatment Market Insight

Japan’s aarskog syndrome treatment market is gaining traction due to the country’s well-established healthcare system, growing focus on early diagnosis, and adoption of advanced treatment options. The aging population and the increasing prevalence of congenital disorders drive demand for easier-to-access, specialized care, including hormone therapy, surgical interventions, and multidisciplinary management strategies.

China Aarskog Syndrome Treatment Market Insight

China aarskog syndrome treatment market accounted for the largest revenue share in the Asia-Pacific region in 2025. The market growth is supported by the country’s expanding middle-class population, rising healthcare expenditure, rapid urbanization, and government-led initiatives promoting early diagnosis and treatment accessibility. Additionally, increasing awareness about congenital disorders among patients and healthcare providers is fostering adoption of specialized treatments.

Aarskog Syndrome Treatment Market Share

The Aarskog Syndrome Treatment industry is primarily led by well-established companies, including:

- BioMarin Pharmaceutical Inc. (U.S.)

- Pfizer Inc. (U.S.)

- Novartis AG (Switzerland)

- F. Hoffmann-La Roche Ltd. (Switzerland)

- Eli Lilly and Company (U.S.)

- Sanofi S.A. (France)

- AbbVie Inc. (U.S.)

- GlaxoSmithKline plc (U.K.)

- Amgen Inc. (U.S.)

- Ipsen Pharma (France)

- Ascendis Pharma A/S (Denmark)

- Horizon Therapeutics (U.S.)

- Sobi AB (Sweden)

- Shire Pharmaceuticals (U.K.)

- Johnson & Johnson (U.S.)

- Mitsubishi Tanabe Pharma Corporation (Japan)

- Ferring Pharmaceuticals (Switzerland)

- Cempra, Inc. (U.S.)

- Chugai Pharmaceutical Co., Ltd. (Japan)

- Spectrum Pharmaceuticals (U.S.)

Latest Developments in Global Aarskog Syndrome Treatment Market

- In February 2024, a study published in European Journal of Pediatrics reported the identification of four novel pathogenic variants in the gene FGD1 among patients clinically suspected of Aarskog‑Scott syndrome. The authors also presented follow‑up data showing that growth hormone therapy in three of the patients resulted in improved height outcomes, supporting the efficacy and safety of rhGH in FGD1‑related AAS

- In July 2025, a case‑report published in Pediatric Reports described for the first time the co‑occurrence of Autism Spectrum Disorder (ASD) in a patient with genetically confirmed Aarskog–Scott syndrome. The report raised awareness of possible neurodevelopmental comorbidities in AAS, highlighting the need for broader neuropsychiatric assessment in patients beyond the classical skeletal and physical manifestations

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.