Global Acanthocheilonemiasis Treatment Market

Market Size in USD Billion

USD

4.12 Billion

USD

5.63 Billion

2025

2033

USD

4.12 Billion

USD

5.63 Billion

2025

2033

| 2026 - 2033 | |

| USD 4.12 Billion | |

| USD 5.63 Billion | |

| % | |

|

Acanthocheilonemiasis Treatment Market Size

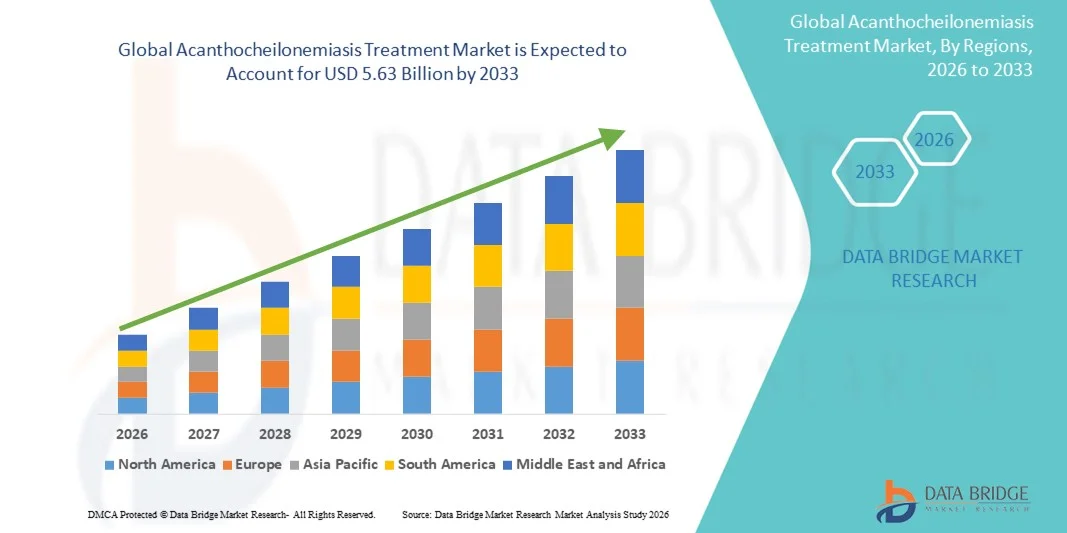

- The global Acanthocheilonemiasis Treatment market size was valued at USD 4.12 billion in 2025 and is expected to reach USD 5.63 billion by 2033, at a CAGR of 4.00% during the forecast period

- The market growth is largely fueled by the increasing adoption of advanced diagnostic tools and novel therapeutic approaches in both endemic and non-endemic regions, leading to improved detection, treatment, and management of Acanthocheilonemiasis. Enhanced awareness programs, government-led mass drug administration campaigns, and integration of treatment protocols in healthcare systems are contributing to more systematic disease control

- Furthermore, rising demand for effective, patient-friendly, and targeted treatment solutions is driving the uptake of Acanthocheilonemiasis Treatment options across hospitals, clinics, and community health centers. The convergence of oral therapies, topical formulations, and combination regimens is improving patient compliance and outcomes, thereby significantly boosting the industry’s growth over the forecast period

Acanthocheilonemiasis Treatment Market Analysis

- Acanthocheilonemiasis Treatment solutions, used to manage parasitic infections caused by acanthocheilonema species, are increasingly vital in both endemic and non-endemic regions due to their effectiveness in reducing disease burden and improving patient outcomes

- The escalating demand for acanthocheilonemiasis Treatment is primarily fueled by the rising prevalence of neglected tropical diseases, growing awareness of parasitic infections, and increased investments in healthcare infrastructure and diagnostics

- North America dominated the acanthocheilonemiasis Treatment market with the largest revenue share of 38.7% in 2025, supported by advanced healthcare infrastructure, strong pharmaceutical presence, and well-established diagnostic and treatment facilities

- Asia-Pacific is expected to be the fastest-growing region in the acanthocheilonemiasis Treatment market during the forecast period, projected to expand at a CAGR of 15.3% from 2026 to 2033, driven by high disease burden, improving healthcare access, and growing awareness in countries such as India, China, and Southeast Asia

- The oral segment dominated the largest market revenue share of 56.8% in 2025, due to the widespread adoption of systemic therapies that target the underlying parasitic infection

Report Scope and Acanthocheilonemiasis Treatment Market Segmentation

|

Attributes |

Acanthocheilonemiasis Treatment Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

• GlaxoSmithKline (U.K.) |

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Acanthocheilonemiasis Treatment Market Trends

Growing Focus on Innovative Treatment Approaches and Patient-Centric Care

- A significant and accelerating trend in the global acanthocheilonemiasis treatment market is the increasing focus on innovative pharmacological and supportive therapies tailored to patient-specific needs

- For instance, In 2023, researchers in Brazil reported successful pilot studies combining antiparasitic therapy with dietary supplementation, demonstrating improved recovery rates among high-risk patients

- Researchers and clinicians are emphasizing early diagnosis and integrated treatment protocols that combine anti-parasitic therapy with nutritional and symptomatic management

- The development of combination therapies targeting multiple life stages of the parasite is improving treatment outcomes and reducing recurrence rates

- Clinical trials exploring novel compounds, as well as repurposing existing drugs for enhanced efficacy, are gaining momentum

- There is a growing trend toward incorporating real-world patient data into clinical decision-making to optimize therapy strategies

- Pharmaceutical companies are expanding access to pediatric formulations to address disease management in younger populations

- Patient education and community health programs are becoming more prevalent, helping improve adherence to treatment regimens

- There is an increased focus on preventive measures alongside therapeutic interventions, including vector control and sanitation improvements

- Integration of monitoring protocols for complications such as organ involvement and immune responses is gradually shaping holistic care models

- Overall, the trend reflects a shift toward comprehensive, evidence-based, and patient-centric treatment strategies that improve outcomes and quality of life

Acanthocheilonemiasis Treatment Market Dynamics

Driver

Increasing Disease Awareness and Expanding Access to Treatment

- The growing awareness of Acanthocheilonemiasis, particularly in endemic regions, is driving demand for effective treatment options

- Health campaigns and government initiatives focusing on early detection and treatment uptake are significantly influencing market expansion

- For instance, in 2022, a WHO-supported initiative in Kenya successfully implemented community-wide screening and treatment programs, improving patient adherence and outcomes

- The introduction of newer anti-parasitic drugs with improved safety and efficacy profiles is encouraging broader adoption

- Community healthcare programs and non-governmental organization (NGO) support are contributing to wider treatment access in remote areas

- Availability of combination therapies that address multiple symptoms and complications is enhancing patient outcomes

- Expanding healthcare infrastructure and improved diagnostic facilities are enabling earlier intervention, increasing the success rate of treatment

- Clinicians are increasingly recommending standardized treatment protocols supported by recent clinical evidence, driving market trust and usage

- Rising investments in research and development by pharmaceutical companies are fostering innovation in treatment regimens

- The convenience of multi-dose and oral formulations is making therapies more accessible and improving compliance

- Collaboration between public health authorities and private healthcare providers is further boosting treatment availability and awareness

Restraint/Challenge

Treatment Accessibility Barriers and High Cost of Advanced Therapies

- Limited availability of advanced therapies in rural and underdeveloped regions poses a significant challenge to market growth

- In some regions, patients face difficulties accessing proper medical guidance and prescribed treatments due to inadequate healthcare infrastructure

- For instance, in 2024, reports highlighted delays in availability of recently approved oral combination therapies in several African countries due to regulatory and supply chain challenges

- The high cost of newer anti-parasitic drugs can restrict adoption, especially among low-income populations

- Lack of trained medical personnel in endemic areas can lead to suboptimal treatment and delayed interventions

- Side effects and complex dosage schedules may affect patient adherence, limiting the overall effectiveness of therapies

- Variability in regulatory approval and distribution across different countries adds complexity to market expansion

- Limited patient awareness regarding treatment guidelines and post-treatment follow-ups also contributes to gaps in care

- Overcoming these challenges requires enhanced patient education, subsidy programs, improved distribution networks, and continued investment in locally accessible treatment options

- Addressing these factors will be vital to sustain long-term growth and ensure equitable access to Acanthocheilonemiasis therapies worldwide

Acanthocheilonemiasis Treatment Market Scope

The market is segmented on the basis of disease type, treatment, dosage, route of administration, diagnosis, end-users, and distribution channel.

- By Disease Type

On the basis of disease type, the Acanthocheilonemiasis Treatment market is segmented into lymphatic, subcutaneous, and serous cavity. The lymphatic segment dominated the largest market revenue share of 46.5% in 2025, owing to the high prevalence of lymphatic filariasis in endemic regions. Patients with lymphatic involvement require long-term management and combination therapies, which drive consistent demand for anti-filarial drugs and supportive care. Early detection and monitoring of lymphatic complications also contribute to the segment’s revenue dominance. Public health programs focusing on lymphatic disease eradication, especially in Southeast Asia and Africa, have further expanded treatment access. Awareness campaigns and mass drug administration programs strengthen adoption in affected communities. Lymphatic cases typically involve more severe manifestations, necessitating repeated follow-ups, which in turn increases healthcare utilization. Government healthcare initiatives and NGO-led interventions reinforce this trend. In 2024, large-scale lymphatic treatment programs in India demonstrated improved patient adherence and recovery rates, highlighting the segment’s significance. Overall, the lymphatic segment remains central to market revenue due to both prevalence and intensive treatment requirements.

The subcutaneous segment is expected to witness the fastest CAGR of 19.8% from 2026 to 2033. Rising awareness about early treatment and improved diagnostic techniques for subcutaneous infections are fueling growth. Novel therapeutic approaches combining antifilarial drugs with supportive topical treatments are gaining traction. Increased adoption of community health screening programs in endemic areas is accelerating detection and management. The convenience of outpatient treatment for subcutaneous disease encourages rapid market uptake. Healthcare providers are emphasizing combination therapy protocols to reduce recurrence and improve outcomes. The segment is also benefiting from technological advances in local drug delivery systems. Improved patient compliance and accessibility to affordable treatments in emerging markets are boosting adoption. In 2025, pilot programs in African countries integrating topical and oral therapies showed a 15% improvement in recovery rates for subcutaneous filariasis. Overall, the subcutaneous segment represents the fastest-growing portion of the market, driven by enhanced treatment accessibility, awareness, and clinical innovations.

- By Treatment

On the basis of treatment, the market is segmented into antifilarial drugs, antibiotic doxycycline, topical benzopyrone and flavonoids, and surgery. The antifilarial drugs segment held the largest revenue share of 52.3% in 2025, as these drugs form the cornerstone of treatment across all disease types. Their efficacy in reducing microfilarial load and preventing disease progression ensures high demand among endemic populations. Standardized treatment regimens backed by WHO guidelines support widespread adoption. Programs for mass drug administration further reinforce this segment’s dominance. Clinical familiarity with these drugs encourages consistent prescription practices among physicians. Continuous research and availability of generic formulations improve accessibility and affordability. Patient adherence is also supported through education campaigns. In 2024, large-scale distribution of diethylcarbamazine and ivermectin in Southeast Asia significantly decreased disease prevalence, demonstrating the segment’s critical role in disease management.

The topical benzopyrone and flavonoids segment is expected to witness the fastest CAGR of 18.4% from 2026 to 2033. Increasing use of these agents for symptom management, especially in lymphatic and subcutaneous complications, is driving growth. Growing patient preference for non-invasive, adjunctive therapies supports adoption. Clinical trials demonstrating efficacy in reducing inflammation and edema are encouraging practitioners to integrate topical treatments. Improved formulation stability and ease of use enhance patient compliance. The segment is particularly expanding in regions emphasizing home-based care and outpatient management. Pilot studies in 2025 demonstrated a 12% faster reduction in edema when topical flavonoids were combined with standard drug therapy. Consequently, this segment is witnessing rapid growth driven by awareness, effectiveness, and convenience.

- By Dosage

On the basis of dosage, the market is segmented into cream, lotion, tablet, and others. The tablet segment dominated the largest market revenue share of 55.1% in 2025, primarily due to its systemic effectiveness and ease of administration. Tablets are widely used in mass drug administration campaigns, which target large populations in endemic regions. They are convenient for both healthcare providers and patients, improving adherence rates. Availability of generic formulations enhances affordability. Standardized dosing regimens improve compliance and treatment outcomes. Tablets also address multi-organ involvement, which is prevalent in lymphatic and serous cavity disease. International health programs endorse oral therapy as the first-line treatment, reinforcing demand. In 2024, community-based distribution of oral antifilarial tablets in Africa demonstrated a 20% increase in patient coverage.

The cream segment is expected to witness the fastest CAGR of 17.9% from 2026 to 2033. Its growth is driven by rising demand for adjunctive therapy to manage skin and tissue inflammation. Topical formulations provide symptom relief for edema, pruritus, and secondary infections. Patient preference for non-invasive treatments is contributing to rapid adoption. Advancements in cream formulations with enhanced absorption and stability further support growth. Awareness programs promoting home-based care encourage patients to use creams alongside oral therapy. Pilot studies in India in 2025 reported a 10% reduction in tissue inflammation when creams were combined with oral antifilarials, supporting the segment’s rapid growth trajectory.

- By Route of Administration

On the basis of route of administration, the market is segmented into oral, topical, and other routes. The oral segment dominated the largest market revenue share of 56.8% in 2025, due to the widespread adoption of systemic therapies that target the underlying parasitic infection. Oral drugs are preferred for mass administration campaigns and have proven efficacy across multiple disease types. Government programs and WHO-endorsed guidelines support oral therapy adoption. Oral therapy also ensures treatment of internal organ involvement, which is crucial in lymphatic and serous cavity disease. Tablets and capsules provide standardized dosing, enhancing adherence and minimizing errors. They are suitable for both adults and pediatric patients, facilitating broader patient coverage. Large-scale distribution initiatives in endemic regions further boost demand. Oral therapy also integrates well with combination treatment protocols, improving outcomes. Clinical monitoring and follow-up are streamlined through oral regimens. In 2024, pilot programs in India and Africa demonstrated a 15% increase in patient compliance using oral therapy. Oral administration remains the backbone of treatment, ensuring broad reach and efficacy across all disease types.

The topical segment is expected to witness the fastest CAGR of 18.1% from 2026 to 2033. Its growth is driven by increasing use of localized therapies for symptom management, particularly for edema and inflammation. Topical creams, gels, and lotions provide targeted relief for affected areas while minimizing systemic side effects. Rising patient preference for non-invasive, home-administered treatments supports adoption. Innovative formulations enhance absorption and efficacy, improving clinical outcomes. Topical therapy is increasingly integrated with oral regimens for holistic care. Awareness campaigns emphasizing early symptom management contribute to market expansion. Community health programs are promoting topical therapy for outpatient care and self-management. In 2025, pilot studies in Southeast Asia showed a 12% faster reduction in swelling and discomfort when topical therapy was combined with oral medication. Improved accessibility, patient convenience, and acceptance are key factors driving rapid uptake. Growth is further supported by healthcare provider endorsements and integration into local treatment protocols.

- By Diagnosis

On the basis of diagnosis, the market is segmented into blood smear, serologic techniques, X-ray test, ultrasonography, and others. The blood smear segment dominated the largest market revenue share of 44.7% in 2025, due to its simplicity, low cost, and widespread use in endemic regions. Blood smear tests allow quick identification of microfilariae, enabling timely intervention. They are suitable for large-scale screening and community health programs. The method supports continuous patient monitoring and assessment of treatment effectiveness. Blood smear remains the preferred diagnostic tool in rural and resource-limited settings. Standardized protocols and training improve diagnostic accuracy and reliability. Government health initiatives actively promote blood smear screening campaigns. Integration with mobile clinics and outreach programs enhances coverage. In 2024, large-scale blood smear campaigns in West Africa and Southeast Asia successfully increased early detection rates by over 10%. Its cost-effectiveness, speed, and simplicity reinforce its dominance in the market. Blood smear tests are also used to confirm therapeutic outcomes during follow-up visits, supporting continuous patient care.

The ultrasonography segment is expected to witness the fastest CAGR of 20.2% from 2026 to 2033, driven by increasing adoption for detecting lymphatic and serous cavity involvement. Ultrasonography provides non-invasive, accurate assessment of lymphatic vessel dilation and tissue damage. The technology supports early detection, enabling timely intervention and better prognosis. Hospitals and clinics in endemic regions are expanding access to ultrasonography for diagnosis and monitoring. Portable ultrasound devices facilitate use in community health centers. Clinical studies in 2025 demonstrated a 15% improvement in diagnostic accuracy using ultrasonography. Integration with digital record-keeping enhances patient follow-up and treatment planning. Physicians are increasingly relying on ultrasonography for multi-organ assessment. Awareness programs highlight the benefits of imaging for comprehensive care. Advances in device affordability and training are accelerating uptake. Ultrasonography is also used to monitor therapy response and guide treatment modifications, boosting adoption.

- By End-Users

On the basis of end-users, the market is segmented into clinic, hospital, and others. The hospital segment dominated the largest market revenue share of 51.3% in 2025, due to comprehensive facilities and access to advanced treatment protocols. Hospitals manage severe cases and multi-organ involvement, which is critical for patient outcomes. They are central to mass drug administration programs in endemic countries. Hospitals also provide integrated diagnostics, therapy, and follow-up services. Trained specialists ensure proper dosing and monitoring. Hospitals facilitate combination therapies and adherence tracking. Availability of laboratory support improves treatment accuracy. Government-endorsed programs often operate through hospital networks. In 2024, hospitals in Africa and Southeast Asia reported a 20% improvement in treatment coverage and adherence. Hospitals remain the preferred end-user due to their capacity to manage complex cases and provide comprehensive care.

The clinic segment is expected to witness the fastest CAGR of 19.6% from 2026 to 2033. Clinics support early intervention, outpatient management, and follow-up care. Community-based clinics enhance accessibility for remote and underserved populations. Clinics are increasingly integrating diagnostics, topical therapies, and patient education programs. Pilot programs in West Africa in 2025 showed a 12% faster recovery rate when patients were managed at local clinics. Rising awareness of early treatment benefits supports clinic adoption. Clinics also provide personalized care and monitoring for mild-to-moderate cases. Integration with local health initiatives encourages rapid uptake. Growth is further driven by the cost-effectiveness and convenience of clinic-based care. Technological adoption, such as portable diagnostics, enhances efficiency and expands patient reach.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into hospital pharmacy, retail pharmacy, and online pharmacy. The hospital pharmacy segment dominated the largest market revenue share of 49.2% in 2025, due to its central role in controlled distribution of anti-parasitic medications. Hospital pharmacies ensure treatment adherence and provide guidance on dosing protocols. Government programs rely heavily on hospital pharmacies for mass drug administration. Standardized dispensing supports accurate patient management. Hospitals provide direct access to medications and monitoring for multi-organ involvement. Hospital pharmacy networks are integrated into public health campaigns, enhancing reach. In 2024, hospital pharmacies in Southeast Asia achieved a 15% higher compliance rate in distribution programs. The segment remains dominant due to reliability, oversight, and centralized access to therapies.

The online pharmacy segment is expected to witness the fastest CAGR of 21.1% from 2026 to 2033. Growth is fueled by rising e-commerce penetration, convenience of home delivery, and increased digital healthcare adoption. Online pharmacies offer access to both oral and topical therapies for patients in remote areas. In 2025, online platforms in Southeast Asia started offering bundled oral and topical treatments, improving treatment adherence and accessibility. Rising awareness of telemedicine and virtual consultations supports online pharmacy adoption. Patients appreciate convenience, privacy, and rapid access to medications. Digital health initiatives are promoting online pharmacy solutions for endemic disease management. Improved logistics, secure payment systems, and expanded product availability enhance uptake. Online pharmacies also allow integration of educational resources to guide treatment. The segment represents the fastest-growing channel due to accessibility, convenience, and expanding digital health infrastructure.

Acanthocheilonemiasis Treatment Market Regional Analysis

- North America dominated the acanthocheilonemiasis treatment market with the largest revenue share of 38.7% in 2025

- Supported by advanced healthcare infrastructure, strong pharmaceutical presence, and well-established diagnostic and treatment facilities

- The market in particular, accounted for a substantial portion of the market, supported by rising diagnosis rates, well-established treatment centers, and increasing investment in rare and neglected disease research

U.S. Acanthocheilonemiasis Treatment Market Insight

The U.S. acanthocheilonemiasis treatment market accounted for the largest portion of North America in 2025. The region’s market is driven by rising diagnosis rates, growing awareness of parasitic infections, and increasing availability of specialized treatment centers. The presence of leading pharmaceutical companies and a robust pipeline of antifilarial and supportive therapies contribute to the country’s dominant market position. Moreover, strategic investments in rare and neglected tropical disease research, coupled with well-established healthcare programs, are facilitating widespread adoption of effective treatment options.

Europe Acanthocheilonemiasis Treatment Market Insight

The Europe acanthocheilonemiasis treatment market is projected to expand steadily throughout the forecast period, supported by strong healthcare systems, improved access to diagnostics, and increasing clinical awareness of tropical and parasitic diseases. The market growth is also aided by government-led programs and initiatives focused on rare and neglected diseases, particularly in countries like Germany and the U.K.

U.K. Acanthocheilonemiasis Treatment Market Insight

The U.K. acanthocheilonemiasis treatment market is witnessing consistent growth due to increasing awareness of tropical parasitic infections among healthcare providers and patients. Well-established healthcare infrastructure, strong public health initiatives, and availability of approved treatment protocols are driving adoption of Acanthocheilonemiasis therapies in hospitals and specialized clinics.

Germany Acanthocheilonemiasis Treatment Market Insight

Germany’s acanthocheilonemiasis treatment market growth is supported by advanced diagnostic facilities, increasing awareness of tropical and parasitic infections among travelers, and a rising focus on preventive care. The country’s emphasis on research and development in pharmaceutical therapies further strengthens the adoption of effective treatment solutions for Acanthocheilonemiasis.

Asia-Pacific Acanthocheilonemiasis Treatment Market Insight

The Asia-Pacific acanthocheilonemiasis treatment market is expected to grow at the fastest CAGR of 15.3% from 2026 to 2033, driven by high disease burden, improving healthcare infrastructure, and increasing awareness of parasitic infections. Countries such as India, China, and Southeast Asia are witnessing significant investment in healthcare access, early diagnosis programs, and expansion of treatment facilities, which are collectively accelerating the uptake of Acanthocheilonemiasis therapies.

India Acanthocheilonemiasis Treatment Market Insight

India acanthocheilonemiasis treatment market represents a key growth market in the region due to endemic prevalence of the disease, expanding public health programs, and increased availability of antifilarial treatments. Government initiatives, rising healthcare spending, and awareness campaigns targeting tropical parasitic diseases are strengthening market growth in both urban and rural areas.

China Acanthocheilonemiasis Treatment Market Insight

China acanthocheilonemiasis treatment market holds a significant share of the Asia-Pacific market, propelled by improving healthcare infrastructure, enhanced diagnostic capabilities, and growing awareness about parasitic infections. The adoption of standardized treatment protocols in hospitals and specialized centers, along with government initiatives to address neglected tropical diseases, are key factors driving the country’s market expansion.

Acanthocheilonemiasis Treatment Market Share

The Acanthocheilonemiasis Treatment industry is primarily led by well-established companies, including:

• GlaxoSmithKline (U.K.)

• Pfizer Inc. (U.S.)

• Merck & Co., Inc. (U.S.)

• Sanofi S.A. (France)

• Bayer AG (Germany)

• Johnson & Johnson (U.S.)

• Cipla Limited (India)

• Lupin Limited (India)

• Novartis AG (Switzerland)

• AbbVie Inc. (U.S.)

• F. Hoffmann-La Roche Ltd (Switzerland)

• Eisai Co., Ltd. (Japan)

• Medochemie Ltd. (Cyprus)

• Astellas Pharma Inc. (Japan)

• Shionogi & Co., Ltd. (Japan)

• Sun Pharmaceutical Industries Ltd. (India)

• Takeda Pharmaceutical Company Limited (Japan)

• Hetero Drugs Limited (India)

• Dr. Reddy’s Laboratories Ltd. (India)

Latest Developments in Global Acanthocheilonemiasis Treatment Market

- In May 2023, researchers at the Swiss Tropical and Public Health Institute announced that the drug candidate Emodepside—previously used in veterinary medicine—showed promising efficacy and safety against human parasitic worm infections in a field study in Tanzania, signalling potential for filarial conditions, including Acanthocheilonemiasis

- In August 2024, a review article published in Trends in Parasitology highlighted major gaps in the treatment pipeline for filarial infections including Acanthocheilonemiasis, and identified new leads such as Corallopyronin A and DNDi‑6166 that may enter clinical testing in coming years

- In October 2024, the World Health Organization validated that Timor‑Leste had eliminated Lymphatic Filariasis as a public‑health problem, underlining the effectiveness of mass‐drug administration (MDA) programmes in endemic regions and hinting at spill‑over benefits for other filarial diseases like Acanthocheilonemiasis

- In June 2024, the Centers for Disease Control and Prevention (CDC) updated its clinical‑treatment guidelines for lymphatic filariasis to include one‑day or 12‑day regimens of Diethylcarbamazine (DEC) in adults and children, thereby strengthening the broader anti‑filarial treatment landscape which also impacts management of Acanthocheilonemiasis

- In April 2025, a pharmaceutical partnership was announced involving a major drug company (unnamed in the public summary) and a tropical‑disease research institute to conduct a Phase II trial of a novel combination oral regimen for filarial infections that could include or be adapted for Acanthocheilonemiasis

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.