Global Acanthocytosis Chorea Market

Market Size in USD Million

USD

800.50 Million

USD

1,147.13 Million

2024

2032

USD

800.50 Million

USD

1,147.13 Million

2024

2032

| 2025 - 2032 | |

| USD 800.50 Million | |

| USD 1,147.13 Million | |

| % | |

|

Acanthocytosis Chorea Market Size

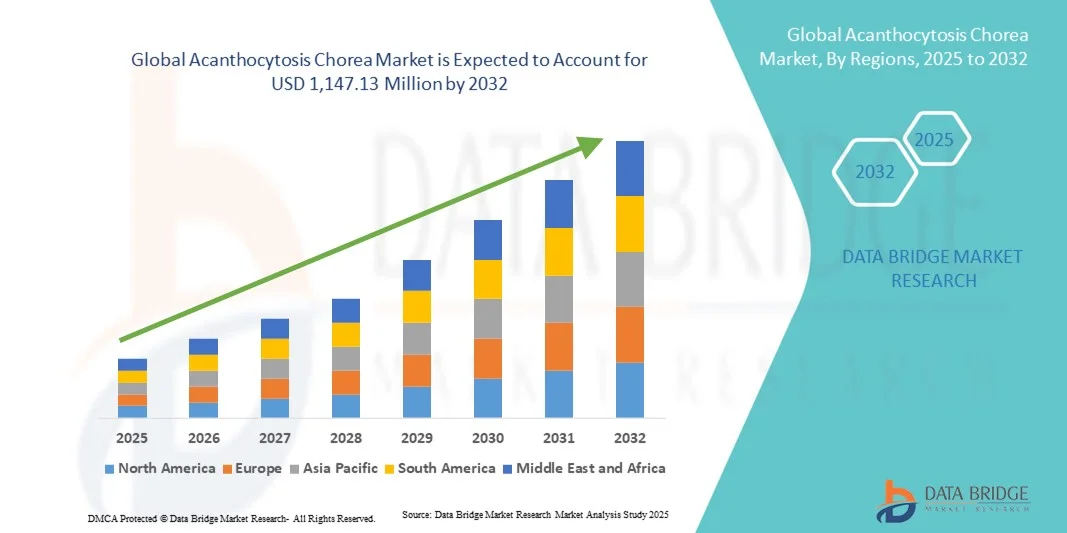

- The global Acanthocytosis Chorea market size was valued at USD 800.50 million in 2024 and is expected to reach USD 1,147.13 million by 2032, at a CAGR of 4.60% during the forecast period

- The market growth is largely fueled by the increasing prevalence of acanthocytosis chorea globally and the rising demand for advanced diagnostic and treatment options for rare neurological disorders

- Furthermore, growing awareness among healthcare providers and patients, coupled with ongoing research and development for effective therapies, is establishing targeted interventions as the preferred management approach. These converging factors are accelerating the uptake of diagnostic and treatment solutions, thereby significantly boosting the industry's growth

Acanthocytosis Chorea Market Analysis

- Acanthocytosis chorea, a rare neurodegenerative disorder characterized by abnormal red blood cells and involuntary movements, is increasingly recognized as a critical area of focus in the development of targeted therapies and supportive care solutions, owing to its complex pathophysiology and limited treatment options

- The rising demand for effective diagnostics and therapeutic interventions is primarily fueled by increased awareness among healthcare providers, advances in genetic testing, and the pursuit of personalized treatment approaches for rare neurological disorders

- North America dominated the acanthocytosis chorea market with the largest revenue share of 38.5% in 2024, attributed to advanced healthcare infrastructure, higher disease awareness, and the presence of key industry players engaged in R&D for novel treatment options, with the U.S. leading in clinical trials and early adoption of innovative diagnostic methods

- Asia-Pacific is expected to be the fastest-growing region in the acanthocytosis chorea market during the forecast period due to increasing patient awareness, expanding healthcare infrastructure, and rising investments in rare disease research

- The MRI segment dominated the market with a share of 41.7% in 2024, driven by its critical role in accurate identification of neurological anomalies

Report Scope and Acanthocytosis Chorea Market Segmentation

|

Attributes |

Acanthocytosis Chorea Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Acanthocytosis Chorea Market Trends

Advancements in Genetic Testing and Early Diagnosis

- A significant and accelerating trend in the global acanthocytosis chorea market is the increasing adoption of advanced genetic testing and early diagnostic tools, enabling accurate detection of disease variants at an earlier stage

- For instance, next-generation sequencing (NGS) panels allow clinicians to identify VPS13A gene mutations rapidly, improving diagnostic accuracy and reducing the time to treatment initiation

- Integration of AI and bioinformatics in diagnostic workflows allows prediction of disease progression and patient-specific therapy planning, enhancing clinical decision-making

- Digital health platforms and telemedicine are increasingly being used to monitor patient symptoms remotely, allowing for continuous tracking and timely intervention

- Multi-center collaborations and international patient registries are facilitating the collection of comprehensive data, supporting improved understanding of disease patterns and therapy outcomes

- Increasing research into biomarker discovery is enabling the development of more precise diagnostic and prognostic tools for acanthocytosis chorea

- This trend towards more precise, data-driven diagnostics is fundamentally reshaping expectations for clinical care and management of acanthocytosis chorea

- The demand for diagnostic solutions that combine genetic testing, imaging, and clinical monitoring is growing rapidly across specialized clinics and research centers, as healthcare providers increasingly prioritize early and accurate detection

Acanthocytosis Chorea Market Dynamics

Driver

Rising Need Due to Increasing Awareness and Research Funding

- The increasing awareness of rare neurodegenerative disorders and growing funding for research on acanthocytosis chorea is a significant driver of market growth

- For instance, the U.S. National Institutes of Health (NIH) has expanded grants for rare disease research, facilitating the development of new therapies and clinical trials for acanthocytosis chorea

- As physicians and patients become more informed about available diagnostic tools and supportive treatments, the adoption of advanced interventions has accelerated

- Furthermore, collaborations between pharmaceutical companies, research institutions, and patient advocacy groups are enabling faster development of targeted therapeutics

- Availability of patient registries and real-world data is supporting clinical research and market expansion, providing insights for better disease management. Increased public-private partnerships are funding innovative therapy development and patient support programs, enhancing market growth opportunities

- Growing initiatives by rare disease foundations to educate and empower patients contribute to earlier diagnosis and increased demand for treatment solutions

- The increasing focus on personalized medicine, combined with investments in rare disease research, is propelling the market across North America, Europe, and emerging Asia-Pacific regions

Restraint/Challenge

Limited Treatment Options and High Therapy Costs

- The lack of curative therapies and the high cost of available treatments remain major challenges limiting market growth. For instance, botulinum toxin injections and specialized supportive care can be expensive and may not be accessible to all patients, particularly in developing regions

- Limited awareness among healthcare providers in some regions delays diagnosis and initiation of treatment, affecting patient outcomes and market uptake

- Regulatory hurdles for rare disease drug approval can slow down the introduction of new therapies, reducing treatment availability

- High dependency on specialized diagnostic tools such as MRI or genetic testing can restrict market penetration in low-resource settings

- Variability in healthcare infrastructure and reimbursement policies across regions can limit patient access to therapies, impacting market expansion

- Challenges in conducting large-scale clinical trials due to the rarity of the disease impede the timely introduction of new treatments

- Overcoming these challenges through affordable therapies, wider access to diagnostic tools, and increased awareness will be critical for sustainable market growth

Acanthocytosis Chorea Market Scope

The market is segmented on the basis of diagnosis, treatment, route of administration, end-users, and distribution channel.

- By Diagnosis

On the basis of diagnosis, the acanthocytosis chorea market is segmented into MRI, CT-Scan, biopsy, and others. The MRI segment dominated the market with the largest market revenue share of 41.7% in 2024, driven by its critical role in accurately detecting neurological anomalies associated with acanthocytosis chorea. MRI provides high-resolution imaging of the brain and basal ganglia, which is essential for identifying disease progression and supporting differential diagnosis. Clinicians prefer MRI due to its non-invasive nature and ability to visualize subtle structural changes. In addition, the growing number of specialized neurology centers and increasing awareness about early detection have strengthened the adoption of MRI as the primary diagnostic tool. Its compatibility with advanced imaging software and integration with patient monitoring systems further enhances its utility in clinical practice. MRI also facilitates longitudinal studies, helping researchers track disease progression and evaluate therapeutic efficacy over time.

The CT-Scan segment is expected to witness the fastest growth during the forecast period due to its affordability and wider availability in developing regions. CT-Scan provides rapid imaging and is increasingly used as an initial diagnostic tool where MRI access is limited. Its ability to detect gross neurological abnormalities quickly makes it suitable for screening suspected cases. Integration with digital imaging archives and tele-radiology platforms supports remote consultations and improves diagnosis efficiency. The growing focus on improving diagnostic infrastructure in emerging markets is fueling the adoption of CT-Scan. Moreover, technological advancements, such as low-dose CT imaging, enhance patient safety while maintaining diagnostic accuracy.

- By Treatment

On the basis of treatment, the market is segmented into botulinum toxin, antidepressants, antipsychotics, and others. The Botulinum Toxin segment dominated the market with a share of 39.8% in 2024, driven by its effectiveness in managing involuntary movements and improving patient quality of life. Botulinum toxin injections are widely used to treat dystonia and other hyperkinetic symptoms associated with acanthocytosis chorea. Its targeted approach reduces adverse effects compared to systemic medications. Hospitals and specialty clinics favor botulinum toxin therapy due to its predictable outcomes and established clinical protocols. Furthermore, ongoing research into optimized dosing schedules and novel formulations continues to strengthen its market position. Patient preference for minimally invasive therapies also supports the sustained demand for botulinum toxin.

The Antidepressants segment is expected to witness the fastest growth during the forecast period due to increasing recognition of neuropsychiatric symptoms in acanthocytosis chorea. Antidepressants help manage mood disorders, anxiety, and associated behavioral complications, improving overall patient compliance and quality of life. Rising awareness among physicians about holistic patient care and the growing adoption of combination therapies contribute to this growth. Clinical guidelines increasingly recommend early psychiatric intervention alongside motor symptom management. In addition, telemedicine and remote prescription platforms are facilitating access to antidepressant therapy for patients in remote areas.

- By Route of Administration

On the basis of route of administration, the market is segmented into oral, parenteral, and others. The Oral segment dominated the market with a share of 42.5% in 2024, primarily due to convenience, ease of administration, and patient adherence. Oral therapies, including antidepressants and antipsychotics, are widely preferred for long-term symptom management and can be administered without specialized equipment. Their availability in various dosage forms, such as tablets and capsules, further supports patient compliance. Healthcare providers often recommend oral treatments as part of a comprehensive care plan alongside supportive therapies. Integration with pharmacy services and digital adherence monitoring tools enhances treatment effectiveness. Oral administration also facilitates therapy in outpatient settings, reducing hospitalization needs.

The Parenteral segment is expected to witness the fastest growth during the forecast period, driven by the increasing adoption of botulinum toxin and other injectable therapies. Parenteral administration allows precise dosing, rapid onset of action, and targeted symptom relief. Specialized clinics and hospitals are expanding injectable therapy offerings to meet patient demand. Growing awareness among neurologists about optimized injection techniques contributes to adoption. The development of longer-acting formulations and improved delivery systems further fuels market growth.

- By End-Users

On the basis of end-users, the market is segmented into clinics, hospitals, diagnostic centers, and others. The Hospitals segment dominated the market with a share of 44.1% in 2024, owing to the availability of specialized neurology departments, advanced imaging facilities, and trained staff to manage complex cases. Hospitals provide comprehensive care combining diagnostics, treatment, and rehabilitation under one roof. They are also hubs for clinical trials and research, further driving market adoption. Patient preference for hospital-based care for rare disorders enhances revenue share. In addition, hospitals facilitate multidisciplinary care coordination, improving treatment outcomes. Telehealth integration within hospital systems supports follow-up and remote monitoring.

The Diagnostic Centers segment is expected to witness the fastest growth during the forecast period due to the increasing number of specialized imaging and genetic testing facilities in emerging regions. Diagnostic centers offer focused services, shorter waiting times, and flexible scheduling, making them attractive for patients seeking early diagnosis. Rising investments in private diagnostic chains and advanced imaging equipment further fuel this growth. Collaboration with hospitals and clinics for referrals enhances market penetration. Adoption of AI-assisted diagnostics and cloud-based imaging platforms improves service efficiency.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into direct tender, hospital pharmacy, retail pharmacy, online pharmacy, and others. The Direct Tender segment dominated the market with a share of 40.3% in 2024, driven by procurement of therapies and diagnostic tools directly by hospitals and large healthcare institutions. Direct tender ensures timely supply, bulk purchasing, and often preferential pricing agreements, making it a preferred channel for institutional buyers. Pharmaceutical companies and medical device manufacturers focus on this channel to maintain strong relationships with major hospitals. In addition, direct tender facilitates the introduction of innovative therapies and diagnostic tools into key facilities. Compliance with regulatory requirements and streamlined logistics further strengthen this channel.

The Online Pharmacy segment is expected to witness the fastest growth during the forecast period, fueled by increasing adoption of digital health platforms, convenience of home delivery, and broader access to therapies for patients in remote regions. Online pharmacies are expanding their offerings to include prescription medications, rare disease therapies, and patient support programs. Integration with telemedicine platforms allows seamless prescription management and refills. Improved logistics and regulatory frameworks supporting e-pharmacies accelerate adoption. Growing awareness and trust in digital healthcare solutions contribute to sustained growth of this channel.

Acanthocytosis Chorea Market Regional Analysis

- North America dominated the acanthocytosis chorea market with the largest revenue share of 38.5% in 2024, attributed to advanced healthcare infrastructure, higher disease awareness, and the presence of key industry players engaged in R&D for novel treatment options, with the U.S. leading in clinical trials and early adoption of innovative diagnostic methods

- Patients and healthcare providers in the region highly value access to specialized diagnostic tools, such as MRI and genetic testing, as well as effective treatment options such as botulinum toxin therapy, which improve disease management and patient outcomes

- This widespread adoption is further supported by well-established healthcare systems, higher per capita healthcare spending, and strong government and private funding for rare disease research, establishing North America as a key hub for both treatment and clinical development of therapies for acanthocytosis chorea

U.S. Acanthocytosis Chorea Market Insight

The U.S. acanthocytosis chorea market captured the largest revenue share of 40% in 2024 within North America, fueled by advanced healthcare infrastructure, high awareness of rare neurological disorders, and increasing investments in research and clinical trials. Patients and clinicians prioritize access to specialized diagnostic tools, including MRI and genetic testing, alongside targeted therapies such as botulinum toxin injections. The growing emphasis on personalized medicine and early diagnosis further propels market growth. Moreover, strong collaborations between pharmaceutical companies, research institutions, and patient advocacy groups are significantly contributing to the market’s expansion.

Europe Acanthocytosis Chorea Market Insight

The Europe acanthocytosis chorea market is projected to expand at a substantial CAGR during the forecast period, primarily driven by increasing investments in rare disease research and the presence of specialized neurology centers. Rising awareness among healthcare providers and patients about diagnostic and treatment options is fostering adoption. European countries are also enhancing healthcare infrastructure and promoting access to advanced therapies. The market is experiencing significant growth across hospitals, diagnostic centers, and specialty clinics, with acanthocytosis chorea care being incorporated into both established and emerging healthcare facilities.

U.K. Acanthocytosis Chorea Market Insight

The U.K. acanthocytosis chorea market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by the increasing focus on rare neurological disorders and the need for specialized diagnostic and treatment services. Concerns regarding delayed diagnosis and inadequate symptom management are encouraging both hospitals and clinics to adopt advanced diagnostic tools and therapies. The U.K.’s robust healthcare system, combined with growing awareness and advocacy for rare disease patients, is expected to continue to stimulate market growth.

Germany Acanthocytosis Chorea Market Insight

The Germany acanthocytosis chorea market is expected to expand at a considerable CAGR during the forecast period, fueled by increasing awareness of rare neurological disorders and demand for advanced therapeutic interventions. Germany’s well-established healthcare infrastructure, emphasis on research and innovation, and availability of specialized neurology centers promote the adoption of diagnostic and treatment solutions. Integration of genetic testing and personalized therapy approaches is becoming increasingly prevalent, with strong preference for early detection and effective symptom management aligning with local healthcare priorities.

Asia-Pacific Acanthocytosis Chorea Market Insight

The Asia-Pacific acanthocytosis chorea market is poised to grow at the fastest CAGR during the forecast period of 2025 to 2032, driven by increasing healthcare investments, growing awareness of rare diseases, and expansion of diagnostic and specialty treatment facilities in countries such as China, India, and Japan. The region’s focus on improving access to advanced diagnostic tools and therapies is accelerating adoption. Furthermore, as APAC emerges as a hub for clinical research and rare disease initiatives, the availability and accessibility of diagnostic and therapeutic solutions are expanding to a wider patient base.

Japan Acanthocytosis Chorea Market Insight

The Japan acanthocytosis chorea market is gaining momentum due to the country’s advanced healthcare system, high patient awareness, and increasing number of specialized neurology centers. Adoption is driven by early diagnosis through MRI and genetic testing, as well as the availability of targeted therapies for symptom management. Moreover, Japan’s aging population is such asly to spur demand for improved disease monitoring and supportive care solutions in both residential and clinical settings. Integration with telemedicine platforms further facilitates patient access to specialized care.

India Acanthocytosis Chorea Market Insight

The India acanthocytosis chorea market accounted for the largest market revenue share in Asia-Pacific in 2024, attributed to expanding healthcare infrastructure, growing patient awareness, and rising investments in rare disease diagnostics and treatments. India is witnessing an increasing number of specialty clinics and diagnostic centers offering MRI, CT-Scan, and genetic testing services. Government initiatives promoting rare disease research, along with the availability of affordable therapeutic options, are key factors propelling the market. The expanding middle class and urban population are also contributing to the growing adoption of advanced care solutions.

Acanthocytosis Chorea Market Share

The Acanthocytosis Chorea industry is primarily led by well-established companies, including:

- Pfizer Inc. (U.S.)

- Lupin (India)

- Sun Pharmaceutical Industries Ltd. (India)

- Lundbeck A/S (Denmark)

- Rosemont Pharmaceuticals Limited (U.K.)

- CoreRx, Inc. (U.S.)

- Hikma Pharmaceuticals PLC (U.K.)

- Amneal Pharmaceuticals, Inc. (U.S.)

- Vibcare Pharma Pvt. Ltd. (India)

- MODASA (India)

- Sanofi (France)

- UCB S.A. (Belgium)

- Dr. Reddy’s Laboratories Ltd. (India)

- Lannett (U.S.)

- Aster Pharma (U.S.)

- Aurobindo Pharma (U.S.)

- Nexus Pharmaceuticals, LLC (U.S.)

- Upsher-Smith Laboratories, LLC (U.S.)

- AbbVie Inc (Ireland)

- Sandoz Group AG (Switzerland)

What are the Recent Developments in Global Acanthocytosis Chorea Market?

- In August 2025, research published in Frontiers in Neurology highlighted novel loss-of-function mutations in the VPS13A gene, providing deeper insights into the genetic underpinnings of ChAc. These findings are crucial for early diagnosis and personalized treatment approaches

- In April 2025, a study in Frontiers in Neurology examined red blood cell lipid distribution in ChAc patients, offering potential biomarkers for early diagnosis and monitoring disease progression. This research could lead to improved diagnostic tools and therapeutic strategies

- In July 2024, a study published in Frontiers in Neurology reported significant symptomatic improvement in a ChAc patient after one year of deep brain stimulation (DBS). This case underscores DBS's potential in managing movement disorders associated with ChAc

- In September 2023, the 11th International Symposium on Neuroacanthocytosis Syndromes introduced the term "VPS13A disease" to replace "Chorea-Acanthocytosis," reflecting a shift towards a more precise genetic classification. This change aims to enhance understanding and research focus on the VPS13A gene's role in the disease

- In May 2021, a study by Quanterix Corporation identified Lyn kinase as a potential therapeutic target in ChAc. This discovery could lead to novel treatment strategies aimed at modulating this kinase to alleviate disease symptom

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.