Global Achromatopsia Treatment Market

Market Size in USD Billion

USD

9.30 Billion

USD

15.39 Billion

2025

2033

USD

9.30 Billion

USD

15.39 Billion

2025

2033

| 2026 - 2033 | |

| USD 9.30 Billion | |

| USD 15.39 Billion | |

| % | |

|

Achromatopsia Treatment Market Size

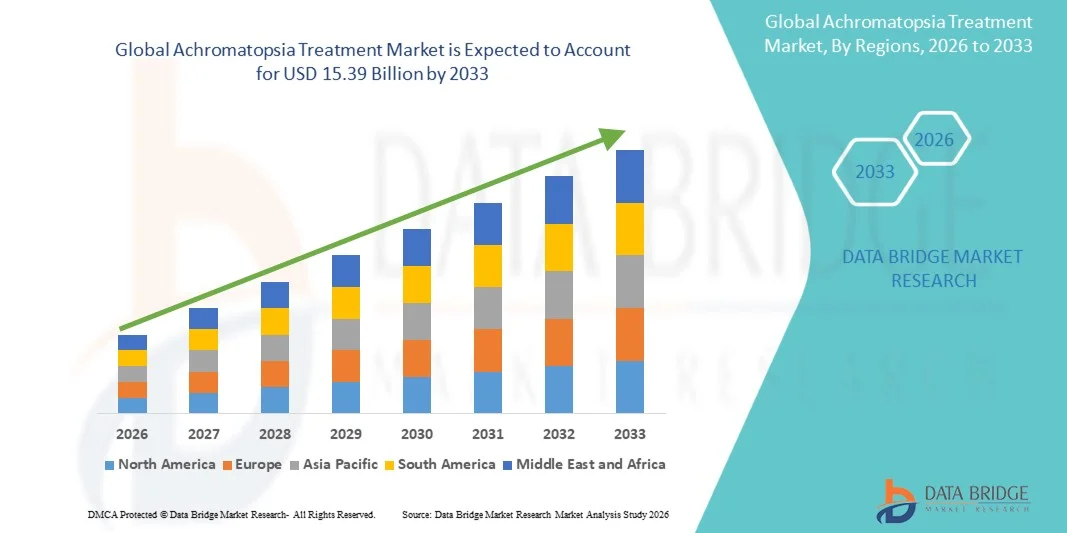

- The global achromatopsia treatment market size was valued at USD 9.30 billion in 2025 and is expected to reach USD 15.39 billion by 2033, at a CAGR of6.50% during the forecast period

- The market growth is largely fueled by the increasing prevalence of inherited retinal disorders, particularly achromatopsia, which causes complete color blindness and visual impairment, driving the demand for effective treatment solutions

- Furthermore, rising demand for advanced gene therapy, pharmacological, and supportive treatment options is establishing achromatopsia treatments as essential solutions for improving vision and quality of life in affected patients, thereby significantly boosting the market’s growth

Achromatopsia Treatment Market Analysis

- Achromatopsia treatments, including gene therapies, pharmacological interventions, and supportive care solutions, are increasingly becoming essential in both clinical and research settings due to the growing prevalence of inherited retinal disorders and the need for improved vision restoration therapies

- The escalating demand for achromatopsia treatments is primarily driven by advancements in gene therapy and targeted pharmacological treatments, increasing awareness among patients and healthcare providers, and rising investments in rare disease therapies

- North America dominated the achromatopsia treatment market with the largest revenue share of 38.4% in 2025, supported by advanced healthcare infrastructure, early adoption of innovative gene therapies, and strong presence of key industry players, with the U.S. witnessing substantial growth in clinical trials and treatment availability

- Asia-Pacific is expected to be the fastest growing region in the achromatopsia treatment market during the forecast period, owing to rising awareness of genetic therapies, increasing healthcare investments, and improving access to specialized ophthalmology care in countries such as China, India, and Japan

- The congenital achromatopsia segment dominated the largest market revenue share of 52.3% in 2025, driven by its lifelong prevalence and genetic origin

Report Scope and Achromatopsia Treatment Market Segmentation

|

Attributes |

Achromatopsia Treatment Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

• Novartis AG (Switzerland) |

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Achromatopsia Treatment Market Trends

“Enhanced Patient Engagement Through AI and Voice-Controlled Treatment Systems”

- The global Achromatopsia Treatment market is witnessing a pronounced trend toward AI-powered devices and voice-assisted healthcare management. These technologies are increasingly enabling patients to actively monitor their therapy adherence, receive timely reminders, and track improvements in visual function with minimal manual intervention, improving overall treatment efficiency

- For instance, several devices now integrate seamlessly with Amazon Alexa, Google Assistant, and Apple HomeKit, allowing patients to receive notifications for upcoming treatment sessions, automatically log therapy completion, and even send alerts to caregivers or clinicians if unusual patterns or missed sessions are detected. This integration reduces the burden on healthcare providers and strengthens patient confidence

- AI-enabled analytics are also playing a transformative role by offering predictive insights into therapy outcomes. These systems can analyze patient behavior patterns, historical adherence, and response metrics to suggest personalized adjustments to treatment plans, enhancing clinical decision-making

- Furthermore, voice-controlled features are expanding beyond reminders to include interactive guidance during therapy sessions, hands-free access to treatment logs, and immediate feedback on device usage, which is particularly beneficial for patients with mobility limitations or those managing treatment independently at home

- The trend is also encouraging interoperability with other digital health platforms and wearable devices, allowing patients to monitor their condition alongside other health parameters such as heart rate, sleep quality, or ocular metrics, creating a holistic home healthcare experience

Achromatopsia Treatment Market Dynamics

Driver

“Growing Need for Convenient, Personalized, and Remote Treatment Solutions”

- Rising prevalence of visual impairments, coupled with patient preference for home-based care, is driving the demand for AI-enabled Achromatopsia Treatment solutions. Patients increasingly favor devices that allow for convenient, consistent, and personalized therapy without frequent hospital visits

- For instance, in April 2025, Onity, Inc. (Honeywell International, Inc.) announced advancements in IoT-based health monitoring devices, integrating AI-driven adherence tracking to provide automated feedback and therapy customization. Such innovations are expected to fuel market growth throughout the forecast period

- AI-driven personalization enables treatment devices to adjust therapy intensity, duration, or scheduling according to patient-specific needs, improving outcomes while reducing the risk of over- or under-treatment

- Remote monitoring features allow healthcare providers to supervise patients virtually, facilitating timely interventions and reducing the need for physical consultations. Combined with voice control, this enhances convenience, patient autonomy, and engagement, especially for elderly or mobility-challenged populations

- The rapid adoption of telehealth platforms and mobile health applications complements this growth, enabling patients to sync their devices with smartphones, tablets, and cloud-based portals for real-time data sharing and analytics

- Increasing awareness of early intervention benefits in visual disorders, along with rising investment in digital health infrastructure, is further bolstering the adoption of AI-enabled Achromatopsia Treatment systems

Restraint/Challenge

“Concerns Regarding Data Security, Device Reliability, and High Initial Costs”

- Data privacy and cybersecurity remain critical challenges for connected Achromatopsia Treatment devices. Cloud-connected platforms and AI-enabled systems are vulnerable to unauthorized access or hacking attempts, which can compromise sensitive patient information and reduce trust in digital health technologies

- For instance, several high-profile security breaches in IoT healthcare devices have made patients and providers cautious about adopting fully connected solutions. Companies such as August and Level Home are addressing these concerns by employing end-to-end encryption, multi-factor authentication, and routine firmware updates

- Device reliability and consistency also pose challenges; AI-driven treatment systems require precise calibration and continuous monitoring to ensure therapy accuracy. Technical glitches or device failures can affect patient adherence and outcomes

- The relatively high initial cost of advanced Achromatopsia Treatment devices, particularly those with AI analytics and voice integration, can limit access for price-sensitive patients or smaller healthcare providers. While basic treatment devices are more affordable, premium systems often command significantly higher prices due to sophisticated features

- Patients in developing regions or those without stable internet connectivity may face additional barriers to adopting AI-enabled and voice-integrated solutions, potentially restricting market penetration

- Overcoming these challenges requires multi-pronged strategies, including robust cybersecurity protocols, patient education campaigns on safe device usage, enhanced technical support, and the development of cost-effective AI-enabled treatment options. In addition, partnerships with telehealth providers and insurance coverage for remote monitoring devices may further facilitate adoption and sustained market growth

Achromatopsia Treatment Market Scope

The Achromatopsia Treatment market is segmented on the basis of type, management, end user, and distribution channel.

• By Type

On the basis of type, the Achromatopsia Treatment market is segmented into Acquired Achromatopsia/Dyschromatopsia, Cerebral Achromatopsia, Congenital Achromatopsia, and Others. The congenital achromatopsia segment dominated the largest market revenue share of 52.3% in 2025, driven by its lifelong prevalence and genetic origin. Patients often require continuous monitoring, adaptive interventions, and assistive devices from early childhood, which sustains demand. Hospitals and specialty clinics widely adopt diagnostic and management solutions to improve patient quality of life. Gene therapy research programs targeting congenital cases are contributing to advanced treatment adoption. Technological improvements in visual aids, eye-tracking devices, and neuro-ophthalmic support tools enhance patient outcomes. Clinical awareness and genetic screening programs further reinforce market dominance. Government and private healthcare support for rare congenital disorders promotes accessibility. Insurance coverage for specialized interventions also contributes to revenue growth. Continuous research and clinical trials in congenital achromatopsia maintain strong adoption rates. Emerging markets with improved ophthalmic care infrastructure are increasingly accessing treatment. The segment also benefits from advocacy and patient support organizations promoting awareness.

The acquired achromatopsia/dyschromatopsia segment is expected to witness the fastest CAGR of 18.5% from 2026 to 2033, fueled by rising awareness of trauma- or disease-induced color vision deficiencies. Increasing diagnosis of cerebral or retinal injuries, along with workplace and automotive safety requirements, drives demand. Hospitals, homecare providers, and specialty clinics are adopting visual aids and assistive technologies for adult patients. Technological innovations in wearable devices, smartphone-based applications, and adaptive lenses facilitate adoption. The segment also benefits from growth in teleophthalmology and remote patient monitoring. Clinical research identifying reversible or treatable causes contributes to early interventions. Awareness campaigns among neurologists and ophthalmologists support increased diagnosis. Growth is further supported by emerging economies investing in ophthalmic care. Expansion of online platforms for patient education and device distribution accelerates adoption. Patients increasingly seek non-invasive solutions and gene therapy where applicable. Continuous innovation in rehabilitation and visual training programs supports segment growth.

• By Management

On the basis of management, the market is segmented into gene therapy, visual aids (Eyeborg), and others. The visual aids segment dominated the largest market revenue share of 47.8% in 2025, driven by its non-invasive nature and immediate benefits for color vision compensation. Hospitals, specialty clinics, and homecare providers adopt visual aids such as Eyeborg devices, spectral filters, and augmented reality applications for daily use. Rising awareness among patients and caregivers contributes to consistent demand. Technological improvements enhance device usability, portability, and real-time color adaptation. Government initiatives for rare disease support and patient accessibility strengthen adoption. Visual aids are widely recommended for children and adults unable to access gene therapy. Integration with smartphones, apps, and assistive tools further boosts convenience. High prevalence of congenital achromatopsia reinforces market dominance. Clinical guidance and teleophthalmology monitoring improve compliance and outcomes. Research into adaptive lenses and wearable AR solutions sustains innovation. Multinational device manufacturers ensure wide geographic distribution. Specialty clinics often offer combined therapy packages with visual aids.

The gene therapy segment is expected to witness the fastest CAGR of 21.2% from 2026 to 2033, fueled by breakthroughs in genetic research targeting mutations causing achromatopsia. Clinical trials and regulatory approvals in developed markets accelerate adoption. Hospitals and specialty clinics are increasingly adopting gene therapy for long-term solutions. Rising investment in rare disease therapeutics by biotechnology companies drives growth. Patient demand for curative solutions, rather than adaptive interventions, supports rapid adoption. Expanded research in gene editing and viral vector delivery enhances efficacy and safety. Emerging economies are gradually introducing gene therapy under pilot programs. Increased awareness among ophthalmologists and neurologists facilitates adoption. Integration with genetic testing ensures precise targeting of patients. Telemedicine and remote monitoring complement therapy management. Successful case studies and publications strengthen physician confidence. Insurance coverage in select regions further supports uptake.

• By End User

On the basis of end user, the market is segmented into hospitals, homecare, specialty clinics, and others. The hospitals segment dominated the largest market revenue share of 55.4% in 2025, driven by high patient inflow, availability of specialized ophthalmic departments, and access to gene therapy and diagnostic infrastructure. Hospitals provide comprehensive care, including genetic testing, visual aid prescription, and rehabilitation. Government and private healthcare support for rare congenital disorders reinforces hospital adoption. Integration of multidisciplinary care, including ophthalmology and neurology, enhances patient outcomes. Reimbursement policies and insurance coverage for hospital-based interventions support market dominance. Continuous clinical trials conducted in hospitals further strengthen adoption. Hospitals also play a key role in patient awareness and post-treatment monitoring. Technological advancements integrated within hospitals improve diagnostic accuracy. The segment benefits from long-term patient follow-up and academic collaborations. Clinical guidelines recommending structured achromatopsia management reinforce hospital utilization.

The specialty clinics segment is expected to witness the fastest CAGR of 19.8% from 2026 to 2033, driven by rising demand for personalized, non-invasive care and adaptive devices. Specialty clinics offer visual aids, wearable technology, and gene therapy consultation services. Patients prefer clinics for targeted interventions, faster access, and expert guidance. Teleophthalmology adoption and homecare integration accelerate growth. Clinics provide training for visual compensation techniques, enhancing patient compliance. Emerging markets are witnessing a rise in dedicated ophthalmic and neurological specialty centers. Clinics also collaborate with device manufacturers for demonstration and distribution. Expansion of patient education programs and online consultations supports rapid adoption. Specialty clinics cater to both pediatric and adult populations. The segment benefits from increasing patient preference for outpatient-based solutions. Innovative therapies and wearable visual aids introduced by clinics accelerate market penetration.

• By Distribution Channel

On the basis of distribution channel, the market is segmented into hospital pharmacy, online pharmacy, retail pharmacy, and others. The hospital pharmacy segment dominated the largest market revenue share of 50.6% in 2025, driven by direct access to hospital patients and integration with prescribed gene therapy or visual aid devices. Hospital pharmacies ensure regulated dispensing, patient counseling, and therapy monitoring. Close collaboration with ophthalmology and neurology departments reinforces adoption. Availability of subsidized programs and reimbursement policies further support market dominance. Hospitals remain the primary point of care for both acute and chronic achromatopsia management.

The online pharmacy segment is expected to witness the fastest CAGR of 20.9% from 2026 to 2033, fueled by increasing e-commerce adoption, patient preference for home delivery, and digital healthcare integration. Online pharmacies distribute visual aids, assistive devices, and supportive supplements. Ease of ordering, access to product reviews, and doorstep delivery encourage patient adoption. Integration with telemedicine platforms enhances prescription accuracy and compliance. Online channels also allow wider geographic reach, particularly in rural and remote areas. Growth is supported by rising digital literacy and expanding internet access globally. Partnerships between device manufacturers and e-pharmacies further boost segment growth. Emerging markets are increasingly relying on online distribution for rare disease support. Patients benefit from affordability, convenience, and access to updated device versions. Online platforms complement homecare and specialty clinic services, ensuring continuity of care.

Achromatopsia Treatment Market Regional Analysis

- North America dominated the achromatopsia treatment market with the largest revenue share of 38.4% in 2025, supported by advanced healthcare infrastructure, early adoption of innovative gene therapies, and a strong presence of key industry players. The U.S. is witnessing substantial growth in clinical trials, expanded treatment availability, and patient access to novel therapies, which is driving adoption and market expansion

- Consumers in the region are increasingly aware of genetic and advanced treatment options, prioritizing access to specialized ophthalmology centers and early intervention programs

- High disposable incomes, supportive reimbursement policies, and a technologically inclined patient population are further encouraging adoption of advanced Achromatopsia therapies across both urban and semi-urban regions

U.S. Achromatopsia Treatment Market Insight

The U.S. achromatopsia treatment market captured the largest revenue share in 2025 within North America, fueled by the rapid uptake of innovative gene therapy solutions and clinical trial programs. Patients and healthcare providers are increasingly focusing on early intervention, personalized therapy plans, and long-term visual rehabilitation programs. Moreover, robust collaboration between biotech companies, research institutions, and ophthalmology clinics is accelerating therapy availability and adoption.

Europe Achromatopsia Treatment Market Insight

The Europe achromatopsia treatment market is projected to expand at a substantial CAGR throughout the forecast period, driven by increasing patient awareness of genetic therapies, well-established healthcare systems, and the rising number of specialized ophthalmology centers. Countries such as Germany, France, and Italy are witnessing growth in patient enrollment in clinical trials and adoption of novel gene therapies.

U.K. Achromatopsia Treatment Market Insight

The U.K. achromatopsia treatment market is expected to grow steadily, supported by the National Health Service’s focus on rare ocular disorders, increasing investments in genetic therapy programs, and the demand for personalized treatment plans. Patient advocacy and awareness campaigns are further boosting therapy adoption.

Germany Achromatopsia Treatment Market Insight

Germany’s achromatopsia treatment market is expanding due to strong healthcare infrastructure, a focus on precision medicine, and widespread access to clinical trials. The country’s emphasis on innovation and patient safety encourages early adoption of emerging Achromatopsia therapies.

Asia-Pacific Achromatopsia Treatment Market Insight

The Asia-Pacific achromatopsia treatment market is expected to be the fastest-growing region during the forecast period, driven by rising awareness of genetic therapies, increasing healthcare investments, and improving access to specialized ophthalmology care in countries such as China, India, and Japan. Government initiatives promoting rare disease treatment, growing private healthcare infrastructure, and increasing patient education are accelerating adoption of advanced therapies.

Japan Achromatopsia Treatment Market Insight

Japan’s achromatopsia treatment market is gaining momentum due to a high-tech healthcare ecosystem, widespread urbanization, and growing focus on gene therapy-based visual rehabilitation. The aging population and increasing access to specialized ophthalmology care support therapy adoption in both residential and clinical settings.

China Achromatopsia Treatment Market Insight

China achromatopsia treatment market accounted for the largest market revenue share in Asia Pacific in 2025, supported by rapid urbanization, rising middle-class healthcare spending, and increasing access to advanced ophthalmology care. Expansion of specialized treatment centers, growing patient awareness, and government initiatives for rare disease management are further propelling market growth. The presence of domestic biotech companies developing gene therapy solutions also enhances treatment accessibility and affordability.

Achromatopsia Treatment Market Share

The Achromatopsia Treatment industry is primarily led by well-established companies, including:

• Novartis AG (Switzerland)

• MeiraGTx Holdings plc (U.K.)

• GenSight Biologics (France)

• Spark Therapeutics, Inc. (U.S.)

• Homestead Technologies, Inc. (U.S.)

• RetroSense Therapeutics, Inc. (U.S.)

• AGTC Therapeutics, Inc. (U.S.)

• Roche Holding AG (Switzerland)

• Editas Medicine, Inc. (U.S.)

• REGENXBIO Inc. (U.S.)

• Audentes Therapeutics, Inc. (U.S.)

• 4D Molecular Therapeutics, Inc. (U.S.)

• Biogen Inc. (U.S.)

• MeiraGTx US Inc. (U.S.)

• Janssen Pharmaceuticals (U.S.)

• Pfizer Inc. (U.S.)

• Novartis Gene Therapy Division (Switzerland)

• Applied Genetic Technologies Ltd. (U.S.)

Latest Developments in Global Achromatopsia Treatment Market

- In June 2024, AGTC completed enrollment in its Phase I/II clinical trial evaluating AGTC‑402 for CNGB3‑related achromatopsia, treating 21 patients across multiple clinical sites, and announced plans to initiate a pivotal Phase III trial in early 2025 based on encouraging safety and efficacy signals observed in the ongoing study

- In March 2024, Nanoscope Therapeutics received FDA Fast Track designation for its MCO‑010 optogenetic therapy targeting achromatopsia treatment, recognizing the therapy’s potential to address significant unmet needs in inherited retinal disorders and expediting regulatory interactions

- In January 2024, ProQR Therapeutics announced a strategic partnership with Laboratoires Théa to develop and commercialize RNA‑based therapies for inherited retinal diseases, including achromatopsia, in a collaboration worth up to €200 million in milestone payments and shared development responsibilities

- In November 2023, Coave Therapeutics completed a €38 million Series A financing round to advance its dual‑AAV vector gene delivery platform, with lead programs targeting CNGB3 achromatopsia and other inherited retinal diseases requiring delivery of large therapeutic genes

- In June 2024, clinical research reviews reported that five gene therapy clinical trials were registered for achromatopsia as of mid‑2024, including multiple Phase I/II programs testing AAV‑based gene replacement therapies targeting CNGA3 or CNGB3 mutations, showing preliminary safety and early efficacy outcomes

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.