Global Acquired Ichthyosis Treatment Market

Market Size in USD Billion

USD

85.50 Billion

USD

121.58 Billion

2025

2033

USD

85.50 Billion

USD

121.58 Billion

2025

2033

| 2026 - 2033 | |

| USD 85.50 Billion | |

| USD 121.58 Billion | |

| % | |

|

Acquired Ichthyosis Treatment Market Size

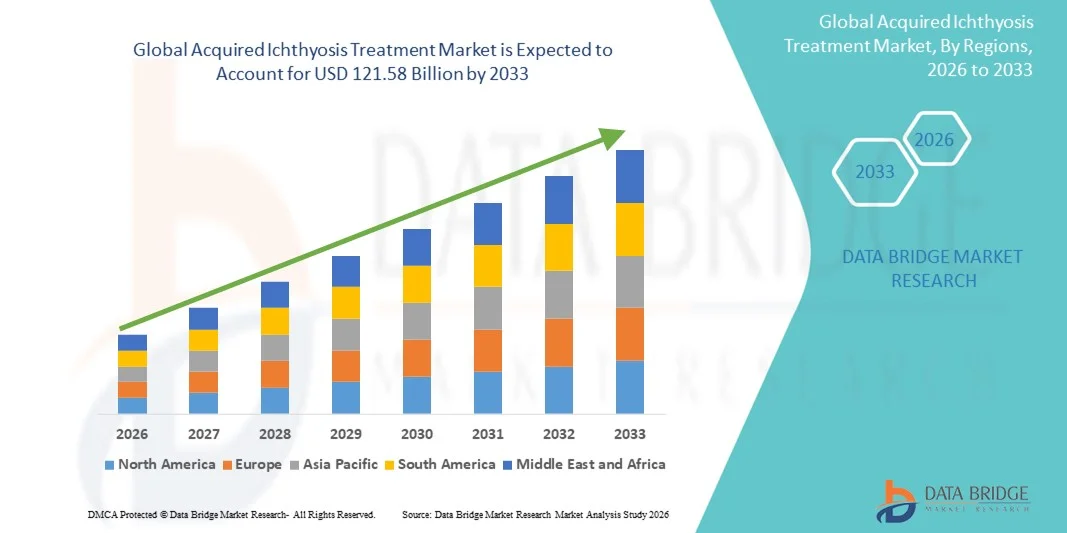

- The global acquired ichthyosis treatment market size was valued at USD 85.50 billion in 2025 and is expected to reach USD 121.58 billion by 2033, at a CAGR of 4.50% during the forecast period

- The market growth is largely fueled by the increasing awareness of rare skin disorders and the rising prevalence of acquired ichthyosis due to underlying conditions such as malignancies, metabolic disorders, and drug-induced cases. Improved diagnostic capabilities and early detection are enabling timely intervention, thereby driving demand for treatment solutions

- Furthermore, growing patient preference for effective, safe, and accessible therapeutic options, including topical treatments, systemic therapies, and supportive care, is establishing modern pharmacologic and non-pharmacologic therapies as the standard of care. These converging factors are accelerating the uptake of Acquired Ichthyosis Treatment solutions, thereby significantly boosting the industry's growth

Acquired Ichthyosis Treatment Market Analysis

- Acquired ichthyosis treatments, aimed at managing abnormal skin thickening and scaling through targeted topical and systemic therapies, are becoming increasingly vital components of modern dermatological care in both hospital and outpatient settings due to growing awareness, improved diagnostic capabilities, and advancements in treatment approaches

- The escalating demand for acquired ichthyosis treatment is primarily driven by the rising prevalence of underlying conditions such as malignancies, autoimmune disorders, and medication-induced triggers, along with increased patient awareness and a growing focus on early diagnosis and effective skin disease management

- North America dominated the acquired ichthyosis treatment market with the largest revenue share of approximately 42.3% in 2025, supported by well-established dermatology care infrastructure, high diagnosis rates, and strong presence of leading pharmaceutical and skin-care companies offering treatments tailored for rare skin disorders in the U.S. and Canada

- Asia-Pacific is expected to be the fastest growing region in the acquired ichthyosis treatment market during the forecast period, with a projected CAGR of around 11% from 2026 to 2033, driven by increasing healthcare investments, growing access to dermatology services, rising awareness of skin conditions, and expanding availability of treatment options in emerging economies like India, China, and Southeast Asia

- The topical segment accounted for the largest market revenue share of 44.8% in 2025, due to its direct application to affected areas and lower risk of systemic side effects

Report Scope and Acquired Ichthyosis Treatment Market Segmentation

|

Attributes |

Acquired Ichthyosis Treatment Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

• Pfizer Inc. (U.S.) |

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Acquired Ichthyosis Treatment Market Trends

Increasing Focus on Symptom Management and Combination Therapy Approaches

- A significant and accelerating trend in the global acquired ichthyosis treatment market is the growing emphasis on symptom-based management combined with treatment of the underlying condition that caused the disorder. Since acquired ichthyosis is often associated with systemic diseases such as lymphoma, hypothyroidism, HIV, and malnutrition, treatment strategies are increasingly personalized and multidisciplinary in nature

- For instance, patients diagnosed with acquired ichthyosis secondary to Hodgkin’s lymphoma or HIV are increasingly being treated with a combination of disease-specific therapy (such as chemotherapy or antiretroviral therapy) along with topical keratolytics and advanced emollients to control severe skin scaling. This integrated approach is showing improved outcomes in managing symptoms and preventing recurrence

- The use of topical retinoids, urea-based formulations, lactic acid, salicylic acid, and ammonium lactate creams continues to expand as dermatologists prefer non-invasive and long-term management options for scaling and dryness. Pharmaceutical companies are also focusing on improving formulation stability, skin penetration, and patient tolerability

- Growing awareness among dermatologists about the link between acquired ichthyosis and internal systemic disorders is also driving early diagnosis and faster treatment intervention. This has increased the demand for prescription-based topical therapies as well as supportive nutritional supplements such as vitamin A and essential fatty acids

- Research efforts are also shifting toward understanding the genetic and cellular pathways behind abnormal skin lipid metabolism in acquired ichthyosis, paving the way for future targeted therapies and biologic treatments

- As a result, the market is witnessing steady growth in demand for combination drug regimens, advanced moisturizers, prescription retinoids, and supportive therapies, making symptom control the central focus of present and future treatment strategies

Acquired Ichthyosis Treatment Market Dynamics

Driver

Rising Prevalence of Underlying Diseases and Growing Dermatology Awareness

- The increasing incidence of chronic systemic conditions such as cancer (especially lymphoma), kidney failure, HIV/AIDS, autoimmune diseases, and endocrine disorders is a major driver for the rising number of acquired ichthyosis cases worldwide, thereby fueling demand for effective treatment options

- For instance, in March 2024, multiple clinical dermatology reviews emphasized the strong association between acquired ichthyosis and malignancies, especially Hodgkin’s lymphoma, encouraging physicians to screen patients with severe unexplained skin scaling for internal diseases. This has led to increased diagnosis rates and earlier treatment intervention

- Increasing awareness among dermatologists and general healthcare providers regarding rare dermatological conditions is promoting early detection and appropriate medical management instead of only cosmetic treatment

- The expansion of dermatology clinics, improved access to prescription skincare products, and rising spending on skin health in both developed and emerging economies are further accelerating market growth

- In addition, advancements in pharmaceutical dermatology, including better-formulated keratolytic agents and retinoid therapies with reduced side effects, are supporting broader patient adoption and long-term usage

- Growing demand for non-invasive, topical, and home-based treatment solutions is also pushing pharmaceutical companies to expand their ichthyosis-related product pipelines

Restraint/Challenge

Limited Awareness, Misdiagnosis, and Lack of Curative Therapies

- A major challenge in the acquired ichthyosis treatment market is the lack of public awareness and frequent misdiagnosis, as the condition is often confused with common dry skin disorders or genetic ichthyosis, resulting in delayed or improper treatment

- For instance, patients suffering from acquired ichthyosis linked to underlying malignancies are sometimes treated only with cosmetic moisturizers without identifying the root cause, which can worsen both dermatological and systemic outcomes if the primary disease remains untreated

- The absence of a permanent cure for acquired ichthyosis further limits market potential, as current therapies mainly focus on symptom management rather than complete disease resolution

- The long-term use of strong keratolytic agents and retinoids may also lead to side effects such as skin irritation, redness, and increased sensitivity, discouraging consistent treatment usage among some patients

- In addition, limited availability of dermatology specialists in rural and underdeveloped regions, coupled with the high cost of prescription-based treatments in certain countries, can restrict widespread access to advanced therapies

- Overcoming these challenges by increasing clinical awareness, improving diagnostic practices, expanding dermatology infrastructure, and developing more affordable and safer treatment alternatives will be essential for the sustainable growth of the Acquired Ichthyosis Treatment market

Acquired Ichthyosis Treatment Market Scope

The market is segmented on the basis of treatment, diagnosis, dosage, route of administration, symptoms, end-users, and distribution channel.

- By Treatment

On the basis of treatment, the Acquired Ichthyosis Treatment market is segmented into Antibiotic, Retinoid, Alpha-Hydroxy Acid Lotions, Vitamin D Supplements, and Others. The retinoid segment dominated the largest market revenue share of 38.6% in 2025, primarily due to its proven effectiveness in reducing hyperkeratosis, regulating abnormal skin cell production, and improving overall skin texture in acquired ichthyosis patients. Retinoids, both oral and topical, are widely prescribed for moderate to severe cases as they directly address the abnormal keratinization process. Dermatologists prefer retinoid therapy because it provides faster visible results when compared with basic emollients or moisturizers. In addition, the rising availability of advanced retinoid formulations with reduced side effects has expanded patient acceptance. Increased awareness among physicians about the clinical benefits of retinoids in ichthyosis-related conditions further strengthens their dominance in hospital and clinic prescriptions. Moreover, retinoids are often used in combination with antifungal or antibacterial treatments when secondary infections occur, which further increases their overall utilization rate. Continuous research in retinoid-based compounds is also contributing to the segment’s long-term leadership.

The Alpha-Hydroxy Acid (AHA) lotions segment is expected to register the fastest CAGR of 9.8% from 2026 to 2033, driven by the growing preference for non-invasive and skin-friendly topical solutions. AHA-based products, including lactic acid and glycolic acid formulations, are gaining attention for their ability to gently exfoliate the skin, improve hydration, and reduce visible scaling without major side effects. These lotions are increasingly recommended for long-term daily management, particularly in mild to moderate cases of acquired ichthyosis. The demand is also rising due to increased consumer awareness regarding chemical exfoliation and skin renewal therapies. Furthermore, their easy availability in both prescription and over-the-counter formats supports widespread adoption. Pharmaceutical and cosmeceutical companies are investing in innovative AHA blends, making this category highly attractive for future growth.

- By Diagnosis

On the basis of diagnosis, the market is segmented into Skin Biopsy, CT Scan, Physical Examination, and Others. The skin biopsy segment dominated the largest market revenue share of 41.4% in 2025, as it provides the most definitive confirmation of acquired ichthyosis and helps in distinguishing it from genetic or other skin disorders. Dermatologists often rely on biopsy results to assess abnormal keratinization, epidermal thickening, and associated pathological changes. The ability of skin biopsy to identify underlying diseases such as malignancies or autoimmune disorders linked to acquired ichthyosis further strengthens its importance. As diagnostic accuracy becomes more critical for targeted treatment planning, hospitals and diagnostic centers increasingly prefer biopsy-based confirmation. In complex cases, biopsy also helps in identifying underlying systemic conditions such as lymphoma or metabolic disorders, making it a crucial diagnostic tool. The expansion of dermatopathology labs globally is further supporting the dominance of this segment in the market.

The physical examination segment is projected to witness the fastest CAGR of 10.3% from 2026 to 2033, owing to its cost-effectiveness and accessibility in both urban and rural healthcare settings. Primary care physicians and dermatologists are increasingly trained to identify the characteristic signs of acquired ichthyosis such as symmetrical scaling and hyperkeratosis through visual assessment. Growing awareness, improved dermatology training, and the rise of teledermatology consultations are significantly supporting growth in this segment. Many patients are now diagnosed at early stages through routine checkups, enabling quicker treatment initiation. The increasing use of dermatoscopes and digital imaging tools is also improving the accuracy of physical examination, contributing to higher adoption and faster growth.

- By Dosage

On the basis of dosage, the market is segmented into Tablet, Cream, Lotion, Ointment, and Others. The cream segment held the largest market revenue share of 36.9% in 2025, as creams provide a balanced combination of hydration, penetration, and prolonged skin retention, making them ideal for treating widespread scaling and dryness. Medicinal creams containing retinoids, urea, or lactic acid are extensively prescribed due to their easy application and better patient compliance. Creams are less greasy than ointments, making them more acceptable for daily use, especially in warm climates. They are also preferred for combination therapy, where multiple active ingredients can be incorporated into a single formulation. Dermatology clinics largely recommend creams due to their versatility in both mild and severe conditions. Furthermore, increasing product availability across pharmacies and online channels supports the dominance of this segment.

The lotion segment is expected to register the fastest CAGR of 11.2% from 2026 to 2033, driven by its lightweight texture and suitability for long-term maintenance therapy. Lotions are widely used for larger body areas and provide easier spreading over the affected skin. Consumers show growing preference for fast-absorbing and non-sticky formulations, making lotions a more convenient option. Pharmaceutical companies are also launching enhanced lotion-based products enriched with vitamins and natural lipids. Rising awareness about daily skincare routines and preventive management further strengthens the growth potential of this segment.

- By Route of Administration

On the basis of route of administration, the market is segmented into Oral, Topical, and Others. The topical segment accounted for the largest market revenue share of 44.8% in 2025, due to its direct application to affected areas and lower risk of systemic side effects. Topical treatments such as creams, lotions, and ointments with keratolytic agents and retinoids form the first-line therapy. High patient compliance, ease of use, and suitability for long-term application support their widespread usage. Topical treatments are also commonly recommended for pediatric and elderly patients, increasing the overall demand. Moreover, improvements in topical drug delivery systems such as liposomal and nano-based carriers enhance their efficacy, reinforcing market dominance.

The oral segment is projected to witness the fastest CAGR of 8.7% from 2026 to 2033, driven by increasing use of systemic retinoids and vitamin supplements in severe cases. Oral therapy is typically prescribed for patients with extensive body coverage or underlying systemic conditions. Advancements in oral drug formulations with controlled release properties are promoting wider acceptance. Increased diagnosis of chronic and secondary ichthyosis conditions also contributes to the rising need for systemic treatment approaches.

- By Symptoms

On the basis of symptoms, the market is segmented into Dry Skin, Scaly Scalp, Hyperkeratosis, Symmetrical Scaling of the Skin, Keratosis Pilaris, and Others. The symmetrical scaling of the skin segment dominated the largest market revenue share of 39.2% in 2025, as it is the most recognizable and clinically significant manifestation of acquired ichthyosis. This symptom typically appears in extensive, uniform patterns that cover large portions of the body, including the arms, legs, and torso, making it visually prominent and physically uncomfortable for patients. The presence of widespread scaling often results in severe dryness, itching, and skin tightening, which significantly affects daily quality of life and personal confidence. As a result, individuals experiencing symmetrical scaling are more likely to seek immediate medical help, increasing patient inflow across dermatology centers. Physicians tend to prioritize therapies targeting extensive scaling, including high-potency emollients, keratolytic agents, and retinoid formulations. The psychological and social impact of visible scaling also compels patients to spend more on long-term treatment solutions. Furthermore, greater awareness campaigns for rare dermatological conditions have improved early identification rates, leading to increased diagnosis of cases exhibiting symmetrical scaling. Pharmaceutical companies continue to develop advanced topical formulations focused on managing severe scaling conditions. Clinical research and improved diagnostic techniques have further strengthened the focus on this symptom. These factors combined have firmly positioned symmetrical scaling as the dominant symptom segment in the global acquired ichthyosis treatment market.

The hyperkeratosis segment is expected to witness the fastest CAGR of 10.6% from 2026 to 2033, due to its rising prevalence and increasing clinical attention. Hyperkeratosis is characterized by abnormal thickening of the outer skin layer, leading to painful cracks, restricted mobility, and increased susceptibility to infections. The condition is increasingly associated with underlying metabolic disorders, cancer therapies, autoimmune diseases, and chronic inflammatory conditions. Rising incidences of such systemic diseases are contributing to a steady increase in hyperkeratosis-related complications. As a result, demand for targeted treatments such as salicylic acid, urea-based creams, and advanced retinoid medications is expanding rapidly. The development of novel keratolytic and anti-proliferative drugs is further accelerating the growth of this segment. Increasing clinical trials focused on reducing abnormal skin cell buildup are supporting innovation in treatment options. In addition, improved patient awareness and willingness to pursue specialized treatment methods are promoting early intervention. Dermatology clinics and hospitals are now offering customized therapy plans for hyperkeratosis management. These combined medical and technological advancements are expected to drive this segment’s rapid market expansion over the forecast period.

- By End-Users

On the basis of end-users, the market is segmented into Clinics, Hospitals, and Others. The hospital segment accounted for the largest market revenue share of 46.1% in 2025, owing to its advanced medical infrastructure and comprehensive treatment capabilities. Hospitals are equipped with specialized dermatology departments that handle complex and severe cases of acquired ichthyosis, especially those linked to systemic illnesses such as lymphoma, autoimmune disorders, or severe nutritional deficiencies. They provide access to high-end diagnostic tools, skin biopsy facilities, and laboratory testing that support accurate disease identification. Multidisciplinary teams, including dermatologists, oncologists, and immunologists, collaborate to create integrated treatment plans. Hospitals also administer combination therapies, including both oral and topical medications, phototherapy, and intravenous interventions when required. Due to their ability to manage complications, including infections and comorbidities, hospitals remain the preferred option for advanced-stage patients. Increased hospitalization associated with cancer treatments has also led to a rise in acquired ichthyosis cases, boosting hospital-based care demand. Furthermore, government and private investments in healthcare infrastructure have strengthened hospital networks globally. A large number of referrals from primary care centers further increases hospital patient volumes. Insurance coverage and reimbursement policies also favor hospital treatments in many regions. These combined factors continue to secure the hospital segment’s dominant position in the overall market.

The clinic segment is expected to grow at the fastest CAGR of 11.5% from 2026 to 2033, driven by the rapid expansion of specialized dermatology clinics worldwide. Clinics provide easy access to outpatient care, shorter waiting times, and more personalized treatment plans. Patients prefer clinics for follow-up visits, routine check-ups, and long-term skin management therapies. The growing urban population and increasing disposable income are supporting the rise of private dermatology practices. Many clinics are now equipped with modern diagnostic tools and offer advanced therapies such as chemical peels, laser treatments, and customized topical solutions. The shift towards decentralized healthcare and greater patient convenience is also fueling reliance on clinic-based treatment. Technological integration, such as tele-dermatology and online appointment systems, enhances patient flow in clinics. Increased awareness of skin hygiene and aesthetics is leading individuals to choose clinics for early treatment. In addition, clinics offer more affordable treatment packages compared to large hospitals. Partnerships with pharmaceutical brands are helping clinics expand their service offerings. These advantages collectively position clinics as the fastest-growing end-user segment in the coming years.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into Hospital Pharmacy, Retail Pharmacy, and Online Pharmacy. The hospital pharmacy segment held the dominant market share of 42.7% in 2025, mainly due to its direct integration with clinical treatment procedures. Patients admitted for acquired ichthyosis-related complications receive their medications through hospital pharmacies, ensuring immediate access to prescribed therapies. These pharmacies stock specialized and prescription-only medicines, including high-strength keratolytics and systemic retinoids that may not be widely available elsewhere. Physicians working within hospitals often prefer in-house pharmacies to ensure treatment accuracy and patient safety. The close monitoring of medication usage and adverse effects also enhances the importance of hospital-based dispensing. In severe cases, where constant dosage adjustment is required, hospital pharmacists work closely with dermatologists to optimize treatment outcomes. Hospital protocols and treatment guidelines further reinforce the use of internal pharmacy services. In addition, critical cases related to cancer or immune disorders require controlled drug administration, which is only possible in hospital settings. The presence of advanced storage facilities for sensitive medications also supports this segment. Increased patient trust in hospital-supplied medication contributes to its higher adoption. These factors together have enabled hospital pharmacies to secure the leading revenue position in the global market.

The online pharmacy segment is projected to register the fastest CAGR of 13.4% from 2026 to 2033, driven by the rapid digitization of the healthcare sector. The convenience of ordering medications from home is attracting patients, especially those undergoing long-term treatment for chronic skin disorders. The rise in smartphone penetration and internet access has strengthened the popularity of e-pharmacy platforms. Many online pharmacies offer discounts, subscription models, and doorstep delivery, making them highly attractive to cost-conscious consumers. Patients with mobility challenges or those living in remote regions benefit significantly from these services. The integration of telemedicine consultations with e-pharmacy platforms is also supporting online medicine purchases. Continuous improvements in digital payment systems and secure transactions are increasing consumer confidence. Many governments have started regulating and legalizing online pharmacies, further boosting market growth. Companies are also investing in fast delivery networks and reliable packaging solutions for dermatological products. The availability of authentic prescription drugs with proper verification systems enhances platform credibility. These technological and consumer behavior shifts are expected to position online pharmacies as the most rapidly expanding distribution channel in the forecast period.

Acquired Ichthyosis Treatment Market Regional Analysis

- North America dominated the acquired ichthyosis treatment market with the largest revenue share of approximately 42.3% in 2025, supported by a well-established dermatology care infrastructure, high diagnosis rates for rare skin conditions, and the strong presence of leading pharmaceutical and skincare companies offering specialized therapies across the U.S. and Canada

- Patients and healthcare providers in the region highly value the availability of advanced topical and systemic treatment options, access to specialty dermatology clinics, and increasing awareness of rare dermatological disorders, which together contribute to higher treatment adoption rates

- This widespread adoption is further supported by favorable reimbursement policies, continuous research and development initiatives, and the presence of advanced diagnostic technologies, establishing North America as a key revenue-generating region for the Acquired Ichthyosis Treatment market

U.S. Acquired Ichthyosis Treatment Market Insight

The U.S. acquired ichthyosis treatment market captured the largest share within North America in 2025, driven by early diagnosis, high healthcare spending, and access to advanced dermatology services. The country benefits from a strong network of dermatologists, specialized hospitals, and research institutions actively engaged in the development of innovative treatment approaches. Increasing awareness of rare skin conditions, along with higher patient willingness to seek medical treatment for chronic dermatological symptoms, continues to support market growth in the U.S.

Europe Acquired Ichthyosis Treatment Market Insight

The Europe acquired ichthyosis treatment market is projected to expand at a substantial CAGR throughout the forecast period, supported by growing awareness of rare dermatological disorders and the availability of advanced treatment options. Strong healthcare systems in countries such as Germany, the U.K., and France, along with rising government initiatives for rare disease management, are encouraging early diagnosis and consistent treatment. The demand for prescription-based topical therapies and dermatological care is increasing across both urban and semi-urban regions.

U.K. Acquired Ichthyosis Treatment Market Insight

The U.K. acquired ichthyosis treatment market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by improved access to dermatology specialists and increased focus on managing chronic skin conditions through timely interventions. Public healthcare initiatives, strong research collaborations, and rising patient awareness regarding rare skin disorders are supporting the market’s expansion.

Germany Acquired Ichthyosis Treatment Market Insight

The Germany acquired ichthyosis treatment market is expected to witness considerable growth, fueled by its advanced healthcare infrastructure, strong pharmaceutical industry presence, and emphasis on dermatological research. The country’s increasing investment in rare disease diagnosis and treatment programs, along with growing adoption of evidence-based therapies, is promoting steady market expansion.

Asia-Pacific Acquired Ichthyosis Treatment Market Insight

The Asia-Pacific acquired ichthyosis treatment market is expected to be the fastest growing region, registering a projected CAGR of around 11% from 2026 to 2033. This growth is driven by increasing healthcare investments, improving access to dermatology services, rising awareness of rare skin disorders, and expanding availability of treatment options in emerging economies such as India, China, and Southeast Asia. The gradual strengthening of healthcare infrastructure in rural and urban regions is further supporting market development.

Japan Acquired Ichthyosis Treatment Market Insight

The Japan acquired ichthyosis treatment market is gaining traction due to the country’s advanced medical system, strong focus on research and innovation, and increasing prevalence of diagnosed rare skin disorders. The demand for effective, long-term management solutions, combined with high healthcare standards and access to specialized professionals, is contributing to the steady expansion of the market.

China Acquired Ichthyosis Treatment Market Insight

The China acquired ichthyosis treatment market accounted for the largest revenue share in Asia-Pacific in 2025, supported by its large patient population, rapid development of healthcare infrastructure, and growing awareness of dermatological conditions. The availability of both international and domestic pharmaceutical products, along with expanding dermatology services in urban areas, is significantly propelling market growth in the country.

Acquired Ichthyosis Treatment Market Share

The Acquired Ichthyosis Treatment industry is primarily led by well-established companies, including:

• Pfizer Inc. (U.S.)

• Johnson & Johnson Services, Inc. (U.S.)

• F. Hoffmann-La Roche Ltd. (Switzerland)

• GlaxoSmithKline plc (U.K.)

• Sanofi S.A. (France)

• AbbVie Inc. (U.S.)

• Novartis AG (Switzerland)

• Sun Pharmaceutical Industries Ltd. (India)

• LEO Pharma A/S (Denmark)

• Almirall S.A. (Spain)

• Galderma S.A. (Switzerland)

• Amgen Inc. (U.S.)

• Merck & Co., Inc. (U.S.)

• Bausch Health Companies Inc. (Canada)

• Perrigo Company plc (Ireland)

• Cipla Ltd. (India)

• Aurobindo Pharma (India)

• Glenmark Pharmaceuticals (India)

Latest Developments in Global Acquired Ichthyosis Treatment Market

- In May 2022, Timber Pharmaceuticals announced that the TMB-001 — an investigational topical isotretinoin ointment formulated using its proprietary IPEG™ delivery system — received U.S. Food and Drug Administration (FDA) Breakthrough Therapy designation for the treatment of moderate‑to‑severe congenital ichthyosis. The designation recognised the potential of TMB-001 to address a high unmet need in skin‑keratinization disorders where currently no approved topical therapies exist

- In February 2023, Timber Pharmaceuticals received an orphan‑drug designation from the European Commission (EC) for TMB-001 for the treatment of X‑Linked Recessive Ichthyosis (XLRI), adding to its prior orphan status for autosomal recessive congenital ichthyosis (ARCI). This status underscores regulatory recognition of the severe unmet needs in rare ichthyosis disorders and supported the company’s global phase 3 trial plans

- In March 2023, Timber Pharmaceuticals published a sub‑analysis of its Phase 2b CONTROL study in the peer‑reviewed journal Clinical and Experimental Dermatology. The paper reported that TMB-001 demonstrated statistically significant improvements over vehicle (placebo) in reducing skin scaling and other clinical signs in patients with congenital ichthyosis — regardless of subtype (ARCI or XLRI). The results offered hope that a topical retinoid might become a non-systemic alternative to oral retinoids, which often have significant side‑effects

- In March 2024, at the American Academy of Dermatology Annual Meeting (AAD), the sponsor presented late-breaking preliminary data from the open‑label maximal‑use arm of the Phase 3 ASCEND trial of TMB-001, involving adult and adolescent participants with moderate‑to‑severe congenital ichthyosis. The data showed meaningful reductions in skin scaling and fissuring (measured by investigator global assessment scores), along with minimal systemic absorption of isotretinoin — a favorable safety signal considering isotretinoin’s risks when used systemically

- In August 2024, however, it was announced that TMB-001 failed to meet the primary and key secondary endpoints of the randomized, double‑blind 12‑week portion of the ASCEND Phase 3 trial. The proportion of patients showing clinically significant improvement was not statistically different between the TMB-001 group and the vehicle group, largely due to a high placebo (vehicle) response rate. As a result, the sponsor declared it would not file for regulatory approval. This outcome was widely reported, underlining the continuing challenge in developing effective topical therapies for ichthyosis

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.