Global Activated Carbon For Mercury Control Market

Market Size in USD Billion

USD

9.13 Billion

USD

28.91 Billion

2025

2033

USD

9.13 Billion

USD

28.91 Billion

2025

2033

| 2026 - 2033 | |

| USD 9.13 Billion | |

| USD 28.91 Billion | |

| % | |

|

Activated Carbon for Mercury Control Market Size

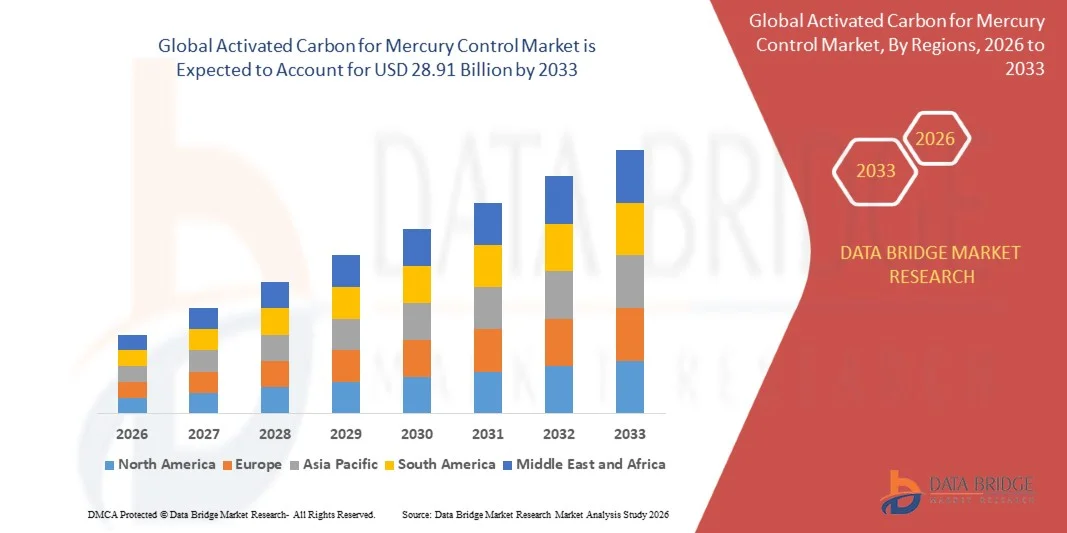

- The global activated carbon for mercury control market size was valued at USD 9.13 billion in 2025 and is expected to reach USD 28.91 billion by 2033, at a CAGR of 15.5% during the forecast period

- The market growth is largely fueled by the increasing enforcement of stringent environmental regulations aimed at reducing mercury emissions from coal-fired power plants and industrial sources, driving widespread adoption of activated carbon injection systems across power generation and manufacturing sectors

- Furthermore, rising industrialization and growing energy demand, particularly in emerging economies, are increasing reliance on coal and heavy industrial processes, thereby necessitating effective mercury control solutions. These factors are accelerating the deployment of activated carbon technologies, significantly boosting market growth

Activated Carbon for Mercury Control Market Analysis

- Activated carbon for mercury control refers to specialized carbon materials used to capture and remove mercury emissions from flue gases in power plants and industrial facilities. These materials are widely applied through injection systems or filtration processes, ensuring compliance with environmental standards and improving air quality

- The escalating demand for activated carbon is primarily driven by increasing regulatory pressure, expansion of coal-based power generation, and growing awareness regarding environmental and health impacts of mercury emissions, leading to higher adoption across power, cement, and refining industries

- Asia-Pacific dominated the activated carbon for mercury control market with a share of around 50% in 2025, due to high reliance on coal-fired power generation, increasing industrial emissions, and stringent environmental regulations across developing economies

- North America is expected to be the fastest growing region in the activated carbon for mercury control market during the forecast period due to stringent environmental regulations and strong adoption of advanced emission control technologies

- Powdered segment dominated the market with a market share of 66% in 2025, due to its high surface area and superior adsorption efficiency for capturing mercury emissions from flue gases. Industries widely prefer powdered variants due to their ease of injection into emission control systems and rapid reaction kinetics, which enhance removal efficiency in coal-fired power plants and industrial boilers

Report Scope and Activated Carbon for Mercury Control Market Segmentation

|

Attributes |

Activated Carbon for Mercury Control Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Activated Carbon for Mercury Control Market Trends

“Increasing Adoption of Stringent Mercury Emission Control Regulations”

- A significant trend in the activated carbon for mercury control market is the increasing enforcement of stringent environmental regulations aimed at reducing mercury emissions from coal-fired power plants and industrial facilities. Regulatory bodies across major economies are mandating the installation of emission control technologies, positioning activated carbon as a critical solution for compliance and environmental protection

- For instance, the U.S. Environmental Protection Agency implemented the Mercury and Air Toxics Standards (MATS), which require power plants to significantly reduce mercury emissions using technologies such as activated carbon injection. This regulation has directly accelerated the adoption of mercury control solutions across utilities and industrial operators

- The growing global focus on reducing hazardous air pollutants is encouraging industries to adopt advanced air purification systems that incorporate activated carbon for efficient mercury capture. This is strengthening the role of activated carbon as a key component in emission control strategies

- Industries such as cement, metal processing, and waste incineration are increasingly integrating mercury control technologies to meet tightening emission norms. This trend is expanding the application scope of activated carbon beyond traditional power generation sectors

- Developing economies are also implementing stricter environmental policies, which is driving the installation of mercury control systems in newly established industrial facilities. This is contributing to the steady expansion of the market across emerging regions

- The continuous evolution of regulatory frameworks and environmental standards is reinforcing long-term demand for activated carbon solutions. This trend is expected to sustain market growth by ensuring consistent adoption of mercury control technologies across diverse industrial sectors

Activated Carbon for Mercury Control Market Dynamics

Driver

“Rising Demand from Coal-Fired Power Plants and Industrial Emission Sources”

- The rising demand for electricity and industrial output is significantly increasing the use of coal-fired power plants and heavy industrial processes, which are major sources of mercury emissions. This is driving the need for effective mercury control technologies such as activated carbon injection systems to ensure regulatory compliance and environmental safety

- For instance, National Thermal Power Corporation has been implementing flue gas treatment systems, including activated carbon-based solutions, across its coal-fired power plants to comply with emission norms. Such initiatives are boosting the adoption of mercury control technologies in large-scale energy production facilities

- The continued reliance on coal as a primary energy source in emerging economies is sustaining demand for mercury removal solutions. Power plants are increasingly investing in emission control upgrades to reduce environmental impact and meet regulatory requirements

- Industrial sectors such as cement production, oil refining, and metal processing are also contributing to rising mercury emissions, creating additional demand for activated carbon solutions. These industries require efficient and scalable technologies to manage emissions effectively

- The increasing focus on environmental sustainability and regulatory adherence is strengthening this driver. The need for reliable and efficient mercury control solutions continues to support steady market expansion across power and industrial sectors

Restraint/Challenge

“High Cost of Activated Carbon and Operational Constraints”

- The activated carbon for mercury control market faces challenges due to the high cost associated with activated carbon production and its continuous consumption in emission control processes. Industries must manage recurring expenses related to carbon replenishment and system maintenance, which can impact overall operational budgets

- For instance, Cabot Corporation produces advanced activated carbon solutions for emission control, but the cost of high-performance materials and processing technologies can increase overall implementation expenses for end users. This creates financial constraints for small and medium-scale industries adopting mercury control systems

- The requirement for continuous injection and replacement of activated carbon adds to operational complexity and increases long-term costs. Facilities must ensure consistent supply and efficient system management to maintain performance levels

- Fluctuations in raw material prices, such as coal and coconut shells used for carbon production, further impact cost stability and profitability. These variations create challenges in maintaining competitive pricing for activated carbon products

- These cost-related and operational challenges continue to restrain market growth. Industries are seeking more efficient and sustainable solutions to balance compliance requirements with economic feasibility

Activated Carbon for Mercury Control Market Scope

The market is segmented on the basis of type and application.

• By Type

On the basis of type, the activated carbon for mercury control market is segmented into powdered, granular, and others. The powdered activated carbon segment dominated the largest market revenue share of 66% in 2025, driven by its high surface area and superior adsorption efficiency for capturing mercury emissions from flue gases. Industries widely prefer powdered variants due to their ease of injection into emission control systems and rapid reaction kinetics, which enhance removal efficiency in coal-fired power plants and industrial boilers. The segment also benefits from cost-effectiveness and operational flexibility, as it can be easily integrated into existing air pollution control technologies without major infrastructure modifications. Increasing regulatory pressure to reduce mercury emissions further strengthens the adoption of powdered activated carbon across multiple industrial applications.

The granular activated carbon segment is anticipated to witness the fastest growth rate from 2026 to 2033, fueled by its reusability and effectiveness in continuous filtration systems. Granular forms are increasingly used in fixed-bed reactors and long-term treatment processes where durability and extended operational life are critical. Industries are adopting granular activated carbon for applications requiring stable performance and lower replacement frequency, which reduces operational costs over time. The growing focus on sustainable and efficient mercury control solutions is further supporting the expansion of this segment across power generation and industrial sectors.

• By Application

On the basis of application, the activated carbon for mercury control market is segmented into coal burning, oil and natural gas burning, cement production, oil refining, and others. The coal burning segment held the largest market revenue share in 2025 driven by the high volume of mercury emissions generated from coal-fired power plants. Regulatory mandates across major economies require strict emission control from coal-based facilities, leading to widespread adoption of activated carbon injection systems. The significant reliance on coal for energy generation in emerging economies further contributes to the dominance of this segment, as power plants invest in advanced emission control technologies to comply with environmental standards. Continuous upgrades in pollution control infrastructure also reinforce demand within this segment.

The cement production segment is expected to witness the fastest CAGR from 2026 to 2033, driven by increasing environmental scrutiny and the need to control mercury emissions from clinker manufacturing processes. Cement plants are adopting activated carbon solutions to meet stringent emission norms while maintaining operational efficiency. The rising global demand for cement in infrastructure development is prompting manufacturers to implement cleaner production technologies, thereby boosting the adoption of mercury control solutions. Advancements in injection systems and growing awareness regarding industrial emissions are further accelerating growth in this segment.

Activated Carbon for Mercury Control Market Regional Analysis

- Asia-Pacific dominated the activated carbon for mercury control market with the largest revenue share of around 50% in 2025, driven by high reliance on coal-fired power generation, increasing industrial emissions, and stringent environmental regulations across developing economies

- The region’s expanding power sector, growing cement and metal production industries, and rising investments in emission control technologies are accelerating market growth

- Availability of low-cost raw materials, rapid industrialization, and supportive government initiatives for pollution control are further strengthening demand for activated carbon solutions

China Activated Carbon for Mercury Control Market Insight

China held the largest share in the Asia-Pacific activated carbon for mercury control market in 2025, owing to its extensive coal-based power generation capacity and strong regulatory push to reduce mercury emissions. The country’s large industrial base, continuous upgrades in air pollution control systems, and government policies targeting cleaner production are key growth drivers. High demand from cement and power sectors, along with domestic production capabilities, further supports market expansion.

India Activated Carbon for Mercury Control Market Insight

India is witnessing the fastest growth in the Asia-Pacific region, fueled by increasing electricity demand, expansion of coal-fired power plants, and tightening emission standards. Government initiatives focused on reducing industrial pollution and improving air quality are driving the adoption of mercury control technologies. Growing investments in power infrastructure and rising awareness regarding environmental compliance are contributing to strong market growth.

Europe Activated Carbon for Mercury Control Market Insight

The Europe activated carbon for mercury control market is expanding steadily, supported by strict environmental regulations and strong emphasis on emission reduction from industrial sources. The region’s focus on sustainable industrial practices and advanced pollution control technologies is driving the adoption of activated carbon solutions. Increasing modernization of existing plants and transition toward cleaner production methods are further enhancing market demand.

Germany Activated Carbon for Mercury Control Market Insight

Germany’s market is driven by its advanced industrial sector, stringent emission control policies, and strong commitment to environmental sustainability. The country emphasizes high-efficiency pollution control systems across power plants and manufacturing facilities. Continuous technological advancements and investments in clean energy transition are supporting steady demand for mercury control solutions.

U.K. Activated Carbon for Mercury Control Market Insight

The U.K. market is supported by regulatory compliance requirements, gradual transition away from coal-based power generation, and increasing focus on industrial emission control. Demand is driven by the need to upgrade existing facilities with efficient mercury removal technologies. Growing emphasis on sustainability and environmental protection is contributing to stable market development.

North America Activated Carbon for Mercury Control Market Insight

North America is projected to grow at the fastest CAGR from 2026 to 2033, driven by stringent environmental regulations and strong adoption of advanced emission control technologies. Increasing investments in upgrading aging power infrastructure and focus on reducing hazardous air pollutants are supporting market growth. The presence of established industrial players and ongoing technological innovations further enhance demand.

U.S. Activated Carbon for Mercury Control Market Insight

The U.S. accounted for the largest share in the North America market in 2025, underpinned by strict mercury emission standards and widespread implementation of activated carbon injection systems. The country’s strong regulatory framework, advanced power generation infrastructure, and focus on environmental compliance are key growth factors. Continuous investments in pollution control technologies and industrial emission reduction initiatives further reinforce market dominance in the region.

Activated Carbon for Mercury Control Market Share

The activated carbon for mercury control industry is primarily led by well-established companies, including:

- CarboTech AC GmbH (Germany)

- Albemarle Corporation (U.S.)

- Calgon Carbon Corporation (U.S.)

- NUCON International Inc. (U.S.)

- ADA-ES, Inc. (U.S.)

- Oxbow Corporation (U.S.)

- Indo German Carbons Limited (India)

- Osaka Gas Co., Ltd. (Japan)

- Siemens Water Technologies Corp. (U.S.)

- Carbon Activated Corporation (U.S.)

- Jacobi Carbons AB (Sweden)

- Kureha Corporation (Japan)

- Haycarb PLC (Sri Lanka)

Latest Developments in Global Activated Carbon for Mercury Control Market

- In January 2024, Jacobi Carbons Group expanded its production facilities in Asia to strengthen the supply of specialty activated carbon used in mercury removal, which is expected to enhance regional availability and support rising demand driven by stricter emission regulations across power and industrial sectors. This expansion enables faster delivery timelines, reduces supply chain constraints, and allows industries to adopt mercury control solutions more efficiently, thereby accelerating market growth in high-demand regions

- In 2024, Norit Activated Carbon advanced its investments in reactivation and production capabilities to promote sustainable mercury control solutions, which is contributing to increased adoption of circular carbon technologies and improving long-term cost efficiency for industrial users. The focus on reactivation also reduces dependency on virgin raw materials, supports environmental sustainability goals, and strengthens the company’s position in providing cost-effective emission control solutions

- In 2023, Calgon Carbon Corporation expanded its activated carbon production capacity in the U.S. to meet growing demand from emission control applications, which is reinforcing supply stability and supporting the implementation of mercury reduction technologies across power plants. This development enhances the company’s ability to cater to large-scale industrial clients, ensures consistent product availability, and supports compliance with stringent environmental regulations

- In 2023, Cabot Corporation enhanced its activated carbon product portfolio focused on air purification and mercury capture, which is strengthening its competitive positioning and enabling industries to comply with evolving environmental standards. The expanded portfolio offers improved performance characteristics, allowing end-users to achieve higher mercury removal efficiency while optimizing operational costs

- In 2023, Donau Carbon GmbH expanded its global distribution network and partnerships to improve the availability of activated carbon for emission control, which is facilitating wider adoption of mercury removal solutions across power generation and cement industries. This strategic move enhances market reach, ensures timely product access in emerging regions, and supports industries in meeting tightening emission norms more effectively

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Activated Carbon For Mercury Control Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Activated Carbon For Mercury Control Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Activated Carbon For Mercury Control Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.