Global Active Approximators Vascular Closure Device Vcds Market

Market Size in USD Billion

USD

1.08 Billion

USD

1.94 Billion

2025

2033

USD

1.08 Billion

USD

1.94 Billion

2025

2033

Forecast Period |

2026 - 2033 |

Market Size (Base Year) |

USD 1.08 Billion |

Market Size (Forecast Year) |

USD 1.94 Billion |

CAGR |

% |

Major Markets Players |

|

Active Approximators Vascular Closure Device (VCDs) Market Overview

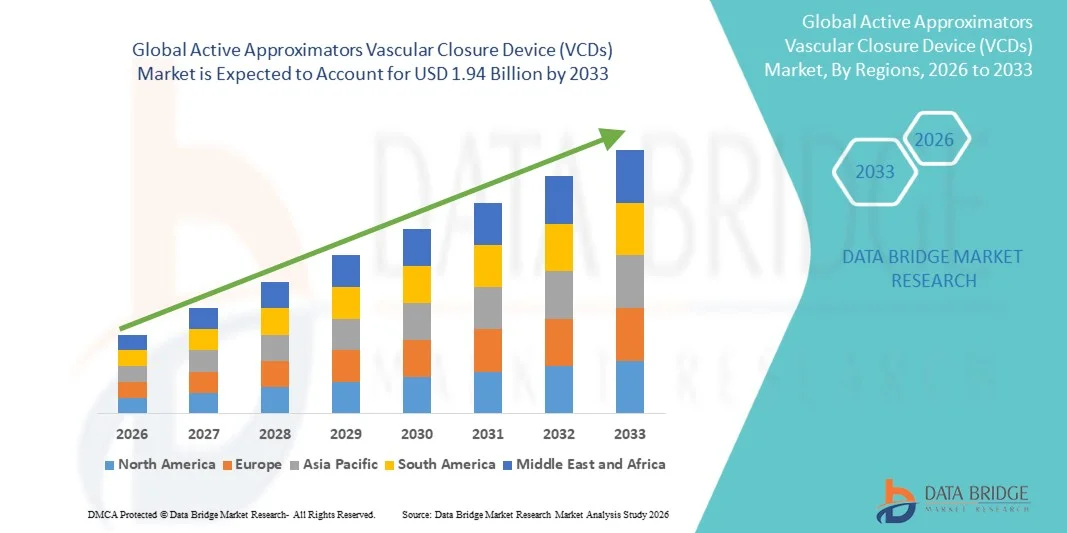

The Active Approximators Vascular Closure Device (VCDs) Market was valued at USD 1.08 billion in 2025 and is projected to reach USD 1.94 billion by 2033, growing at a CAGR of 7.60% from 2026 to 2033. Market growth is driven by increasing procedural volumes in interventional cardiology and radiology, rising adoption of minimally invasive catheter-based procedures, and the expanding geriatric population susceptible to cardiovascular and peripheral vascular diseases.

The clinical advantages of vascular closure devices, including faster hemostasis, reduced time to ambulation, improved patient comfort, and lower complication rates compared to manual compression, are accelerating adoption among interventional specialists and healthcare facilities. Technological advancements in active approximator devices, including enhanced delivery mechanisms, improved collagen-based and suture-mediated closure systems, and expanded compatibility with larger sheath sizes, are broadening clinical applicability across complex interventional procedures. In addition, growing healthcare infrastructure investments globally, favorable reimbursement frameworks in developed markets, and the expansion of ambulatory surgical centers are creating new opportunities for market stakeholders across the forecast period.

Key Market Trends & Insights

- North America dominated the Active Approximators Vascular Closure Device (VCDs) Market with the largest revenue share of 42.8% in 2025, supported by high procedural volumes, advanced healthcare infrastructure, strong reimbursement frameworks, and the presence of leading market players.

- Asia-Pacific is expected to be the fastest-growing region at a CAGR of 9.45% from 2026 to 2033, driven by expanding healthcare infrastructure, rising cardiovascular disease burden, increasing adoption of interventional procedures, and growing healthcare expenditure.

- The Active Approximators segment led the market with a 48.5% market share in 2025, reflecting strong clinical preference for suture-mediated and clip-based closure devices that provide secure arteriotomy closure and enable early ambulation.

- The External Hemostatic Devices segment is anticipated to be the fastest-growing type category, driven by increasing demand for non-invasive closure alternatives, technological innovations, and expanding applications in radial access procedures.

- The Femoral Access segment dominated the access category with a 67.2% market share in 2025, supported by high procedure volumes in interventional cardiology and established clinical protocols for femoral arteriotomy closure.

- The Radial Access segment is expected to witness the fastest growth during the forecast period, driven by growing preference for transradial approaches due to lower bleeding complications and improved patient comfort.

- The Interventional Cardiology segment dominated the procedure category with a 62.5% market share in 2025, driven by high volumes of percutaneous coronary interventions, structural heart procedures, and electrophysiology ablations requiring vascular access site management.

- The Hospitals and Clinics segment dominated the end-user category with a 58.4% market share in 2025, supported by access to comprehensive catheterization laboratories, multidisciplinary interventional teams, and advanced perioperative care infrastructure.

- The Ambulatory Surgery Centres segment is expected to witness strong growth during the forecast period, driven by cost-effective procedural delivery, same-day discharge protocols, and expanding outpatient interventional programs.

Market Size & Forecast

- Global Market Value (2025): USD 1.08 Billion

- Expected Market Value (2033): USD 1.94 Billion

- Forecast CAGR (2026–2033): 7.60%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia-Pacific

Report Scope and Active Approximators Vascular Closure Device (VCDs) Market Segmentation

|

Attributes |

Active Approximators Vascular Closure Device (VCDs) Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

· Abbott Laboratories (U.S.) · Teleflex Incorporated (U.S.) · Cardinal Health Inc. (U.S.) · Morris Innovative Inc. (U.S.) · Transluminal Technologies LLC (U.S.) · Medtronic plc (Ireland) · Terumo Corporation (Japan) · Cordis (U.S.) · Merit Medical Systems Inc. (U.S.) · Vasorum Ltd. (Ireland) · Essential Medical Inc. (U.S.) · Vivasure Medical Limited (Ireland) |

|

Market Opportunities |

· Expansion of vascular closure device adoption into emerging markets with growing interventional cardiology and radiology procedure volumes · Development of next-generation bioresorbable and sutureless closure systems enabling improved patient outcomes and reduced vascular complications |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Active Approximators Vascular Closure Device (VCDs) Market Trends

Trend: Technological Advancements in Closure Mechanisms and Bioresorbable Materials

Clinical adoption of active approximators vascular closure devices continues to accelerate as technological innovations improve closure efficacy, safety profiles, and procedural efficiency. Advanced suture-mediated closure systems, clip-based approximators, and next-generation collagen plug devices enable secure arteriotomy closure across a range of sheath sizes, supporting complex interventional procedures including transcatheter aortic valve replacement (TAVR), endovascular aneurysm repair (EVAR), and percutaneous coronary interventions (PCI). Development of fully bioresorbable closure devices is addressing concerns regarding permanent implant retention, reducing long-term vascular complications and enabling repeat access site utilization.

For instance,

The MANTA Vascular Closure Device has gained significant market traction due to its ability to close large-bore arteriotomies (up to 25F) with a collagen-based bioresorbable implant, providing secure hemostasis and enabling early ambulation following complex structural heart and endovascular procedures.

In addition, research demonstrates that active approximator devices reduce time to hemostasis and ambulation compared to manual compression, improving patient throughput and satisfaction while reducing nursing workload in catheterization laboratories. Technological advancements in closure mechanisms and bioresorbable materials are expected to strengthen market growth and expand clinical applicability across interventional specialties.

Active Approximators Vascular Closure Device (VCDs) Market Dynamics

Key Market Driver: Rising Procedural Volumes in Interventional Cardiology and Radiology

The growing volume of minimally invasive catheter-based procedures in interventional cardiology and radiology is a primary driver of market growth. Vascular closure devices enable faster hemostasis, shorter compression times, and earlier patient ambulation compared to manual compression, improving catheterization laboratory efficiency and patient outcomes. The increasing prevalence of cardiovascular diseases, peripheral arterial disease, and conditions requiring diagnostic and therapeutic catheterization is expanding the patient population requiring vascular access site management.

For instance,

A 2025 multicenter registry study confirmed that active approximator vascular closure devices reduced time to hemostasis by 78% and time to ambulation by 65% compared to manual compression following percutaneous coronary interventions, demonstrating significant clinical and operational advantages.

Rising procedural volumes in interventional cardiology and radiology are expected to strengthen adoption of vascular closure technologies globally.

Key Restraint/Challenge: Risk of Vascular Complications and Device-Related Adverse Events

Despite clinical advantages, vascular closure devices carry inherent risks of device-related complications, including access site hematoma, retroperitoneal bleeding, pseudoaneurysm formation, arterial stenosis, and device failure. The learning curve associated with proper device deployment and patient selection criteria presents challenges for interventional teams adopting new closure technologies.

For instance,

Clinical registries report vascular complication rates of 2–5% following VCD deployment, with higher rates observed in patients with peripheral arterial disease, obesity, and challenging vascular anatomy. Risk of vascular complications and device-related adverse events may constrain adoption among risk-averse interventional teams and patients with unfavorable vascular characteristics.

Key Market Opportunity: Expansion of Large-Bore Closure Applications and Outpatient Interventional Programs

The development of closure devices capable of managing large-bore arteriotomies (14F–25F) is creating opportunities for adoption in structural heart interventions, endovascular aortic repair, and mechanical circulatory support procedures. Simultaneously, expanding outpatient interventional programs in ambulatory surgical centers are driving demand for closure devices enabling same-day discharge protocols.

For instance,

The global vascular closure device market is projected to experience sustained growth through 2033, driven by increasing adoption of transcatheter structural heart procedures, expanding ambulatory interventional programs, and technological innovations in large-bore closure systems.

Expansion of large-bore closure applications and outpatient interventional programs represents a significant growth opportunity for market stakeholders.

Active Approximators Vascular Closure Device (VCDs) Market Scope

The active approximators vascular closure device (VCDs) market is segmented on the basis of type, access, procedure, distribution channel, application, and end user.

By Type

On the basis of type, the Active Approximators Vascular Closure Device (VCDs) Market is segmented into passive approximators, active approximators, and external hemostatic devices. The Active Approximators segment dominated the market with a 48.5% market share in 2025, reflecting strong clinical preference for suture-mediated and clip-based closure devices that provide secure arteriotomy closure and enable early patient ambulation. Active approximator devices, including the Perclose ProGlide, MANTA, and Angio-Seal systems, deliver reliable hemostasis across standard and large-bore arteriotomies, supporting complex interventional procedures. High procedural volumes in interventional cardiology and established clinical protocols contribute to segment leadership.

The External Hemostatic Devices segment is anticipated to be the fastest-growing type category at a CAGR of 9.12% from 2026 to 2033. Growth is driven by increasing demand for non-invasive closure alternatives, technological innovations in compression-based hemostatic systems, and expanding applications in radial access procedures where internal closure devices are not required.

By Access

On the basis of access, the Active Approximators Vascular Closure Device (VCDs) Market is segmented into femoral access and radial access. The Femoral Access segment dominated the market with a 67.2% market share in 2025, supported by high procedure volumes in interventional cardiology, structural heart interventions, and peripheral vascular procedures requiring femoral arteriotomy closure. Established clinical protocols, extensive device compatibility, and the need for hemostasis following larger sheath insertions drive segment leadership.

The Radial Access segment is expected to witness the fastest growth during the forecast period at a CAGR of 9.85% from 2026 to 2033. Growth is driven by increasing preference for transradial approaches in percutaneous coronary interventions due to lower bleeding complications, reduced vascular access site morbidity, and improved patient comfort. Development of radial-specific hemostatic compression devices and expanding operator proficiency with transradial techniques are supporting segment expansion.

By Procedure

On the basis of procedure, the Active Approximators Vascular Closure Device (VCDs) Market is segmented into interventional cardiology and interventional radiology/vascular surgery. The Interventional Cardiology segment dominated the market with a 62.5% market share in 2025, driven by high volumes of percutaneous coronary interventions, transcatheter aortic valve replacements, structural heart procedures, and electrophysiology ablations requiring vascular access site management. The concentration of complex catheter-based cardiac procedures within hospital catheterization laboratories contributes to segment leadership.

The Interventional Radiology/Vascular Surgery segment is expected to witness steady growth from 2026 to 2033, driven by increasing volumes of endovascular aneurysm repair, peripheral arterial interventions, and diagnostic angiography procedures. Expanding applications of vascular closure devices in non-cardiac interventional procedures are supporting segment expansion.

By Distribution Channel

On the basis of distribution channel, the Active Approximators Vascular Closure Device (VCDs) Market is segmented into direct tenders and retail. The Direct Tenders segment dominated the market with a 72.4% market share in 2025, reflecting the predominance of institutional procurement through hospital purchasing agreements, group purchasing organizations (GPOs), and government tender processes. High-volume procedural centers negotiate directly with manufacturers for favorable pricing, service agreements, and product training support.

The Retail segment held 27.6% of the market share in 2025, driven by distribution through medical device distributors and specialty cardiovascular product suppliers serving smaller healthcare facilities and outpatient centers. The retail channel is expected to witness moderate growth as ambulatory surgical centers expand interventional capabilities.

By Application

On the basis of application, the Active Approximators Vascular Closure Device (VCDs) Market is segmented into diagnostic intervention and therapeutic intervention. The Therapeutic Intervention segment dominated the market with a 58.6% market share in 2025, driven by high volumes of therapeutic catheter-based procedures including percutaneous coronary interventions, structural heart interventions, and peripheral vascular treatments requiring secure arteriotomy closure. Complex therapeutic procedures often utilize larger sheath sizes, necessitating reliable vascular closure technologies.

The Diagnostic Intervention segment is expected to witness the fastest growth at a CAGR of 8.25% from 2026 to 2033, driven by increasing cardiovascular disease screening, expanding outpatient diagnostic programs, and growing adoption of same-day discharge protocols enabled by vascular closure devices.

By End User

On the basis of end user, the Active Approximators Vascular Closure Device (VCDs) Market is segmented into hospitals and clinics, specialty centres, ambulatory surgery centres, and others. The Hospitals and Clinics segment dominated the market with a 58.4% market share in 2025, driven by access to comprehensive catheterization laboratories, multidisciplinary interventional teams, and advanced perioperative care infrastructure. Hospitals serve as primary centers for complex interventional procedures requiring extended monitoring and specialized postoperative care.

The Ambulatory Surgery Centres segment is expected to witness the fastest growth at a CAGR of 10.15% from 2026 to 2033, driven by cost-effective procedural delivery, same-day discharge protocols, and expanding outpatient interventional cardiology and radiology programs. Development of closure devices optimized for ambulatory settings is enabling rapid patient turnover and improved operational efficiency.

Active Approximators Vascular Closure Device (VCDs) Market Regional Analysis

North America dominated the active approximators vascular closure device (VCDs) market with a revenue share of 42.8% in 2025, supported by high procedural volumes in interventional cardiology, advanced healthcare infrastructure, strong reimbursement frameworks, and the presence of leading market players including Abbott Laboratories, Teleflex Incorporated, and Cardinal Health. Favorable regulatory pathways, extensive interventional training programs, and established clinical protocols contribute to regional market leadership.

U.S. Active Approximators Vascular Closure Device (VCDs) Market Insight

The U.S. active approximators vascular closure device (VCDs) market benefits from the highest procedural volumes in interventional cardiology globally, extensive catheterization laboratory infrastructure, and strong clinical evidence supporting vascular closure device adoption. Academic medical centers, large health systems, and specialty cardiovascular practices continue to expand interventional programs utilizing advanced closure technologies. Favorable Medicare and commercial payer reimbursement supports procedural volumes and equipment investment. The U.S. dominated the North American market with a share of 86.5% in 2025.

Europe Active Approximators Vascular Closure Device (VCDs) Market Insight

The Europe active approximators vascular closure device (VCDs) market remains a major contributor, with strong hospital-based interventional cardiology and radiology programs across Germany, the U.K., France, and Italy. Growing adoption of transradial access and large-bore closure technologies is expanding the addressable market. Cross-disciplinary guidelines and structured training pathways are improving procedural outcomes and standardizing care delivery.

U.K. Active Approximators Vascular Closure Device (VCDs) Market Insight

The U.K. active approximators vascular closure device (VCDs) market is characterized by expanding interventional programs within NHS hospitals and private healthcare facilities. Investment in advanced closure technologies for structural heart and endovascular procedures is improving access to minimally invasive options and supporting same-day discharge initiatives.

Germany Active Approximators Vascular Closure Device (VCDs) Market Insight

Germany's robust hospital infrastructure and advanced interventional capabilities support comprehensive vascular closure programs across cardiology, radiology, and vascular surgery. Strong clinical training networks and favorable reimbursement frameworks contribute to high procedure volumes and technology adoption. Germany dominated the European market with a share of 24.6% in 2025.

Asia-Pacific Active Approximators Vascular Closure Device (VCDs) Market Insight

The Asia-Pacific active approximators vascular closure device (VCDs) market is poised for rapid growth with a CAGR of 9.45% during the forecast period, driven by expanding healthcare infrastructure, rising cardiovascular disease burden, increasing adoption of interventional procedures, and growing healthcare expenditure. Private healthcare systems in China, Japan, India, and South Korea are investing in interventional cardiology and radiology capabilities to meet growing patient demand.

Japan Active Approximators Vascular Closure Device (VCDs) Market Insight

The Japan active approximators vascular closure device (VCDs) market benefits from advanced healthcare infrastructure, strong interventional expertise, and favorable reimbursement for catheter-based procedures. Vascular closure device adoption is well-established across interventional cardiology and radiology applications. Japan dominated the Asia-Pacific market with a share of 28.4% in 2025.

China Active Approximators Vascular Closure Device (VCDs) Market Insight

The China active approximators vascular closure device (VCDs) market is experiencing rapid growth driven by healthcare modernization initiatives, expanding hospital catheterization laboratory networks, and increasing patient demand for advanced interventional options. Domestic medical device development is complementing imported platforms, improving market accessibility. China is expected to be the fastest-growing country in the Asia-Pacific region at a CAGR of 10.85% from 2026 to 2033.

Active Approximators Vascular Closure Device (VCDs) Market Share

The active approximators vascular closure device (VCDs) industry is primarily led by well-established companies, including:

- Abbott Laboratories (U.S.)

- Teleflex Incorporated (U.S.)

- Cardinal Health Inc. (U.S.)

- Morris Innovative Inc. (U.S.)

- Transluminal Technologies LLC (U.S.)

- Medtronic plc (Ireland)

- Terumo Corporation (Japan)

- Cordis, a Cardinal Health company (U.S.)

- Merit Medical Systems Inc. (U.S.)

- Vasorum Ltd. (Ireland)

- Essential Medical Inc. (U.S.)

- Vivasure Medical Limited (Ireland)

Latest Developments in Active Approximators Vascular Closure Device (VCDs) Market

- In March 2026, Abbott Laboratories announced the expanded indication clearance from the U.S. FDA for its Perclose ProGlide Suture-Mediated Closure System for use in large-bore arteriotomies up to 21F following transcatheter structural heart procedures. The expanded indication strengthens Abbott's position in the growing large-bore vascular closure market segment.

- In January 2026, Teleflex Incorporated reported positive 12-month outcomes data from its MANTA IDE clinical trial, demonstrating sustained safety and efficacy of the MANTA Vascular Closure Device for large-bore femoral arteriotomy closure. The data supports ongoing market expansion and clinical adoption in structural heart and endovascular procedures.

- In November 2025, Vivasure Medical Limited received CE Mark approval for its PerQseal fully bioresorbable vascular closure device for femoral arteriotomies up to 18F. The approval enables European commercialization of a next-generation closure technology designed to leave no permanent implant at the access site.

- In September 2025, Cardinal Health Inc. announced the global commercial launch of the Cordis EXOSEAL PLUS Vascular Closure Device featuring an enhanced bioabsorbable plug design for improved deployment and hemostasis. The launch expands Cardinal Health's vascular closure portfolio across interventional cardiology and radiology applications.

- In June 2025, Terumo Corporation announced strategic investments to expand its vascular closure device manufacturing capacity in Japan and the United States, addressing growing global demand for hemostatic technologies in interventional procedures.

- In April 2025, Merit Medical Systems Inc. received U.S. FDA 510(k) clearance for its MYNX CONTROL Vascular Closure Device featuring enhanced delivery system ergonomics and improved extravascular sealant deployment. The clearance supports Merit Medical's expansion in the active vascular closure market.

- In February 2025, Essential Medical Inc. announced completion of enrollment in its pivotal clinical trial evaluating the next-generation MANTA 2.0 Vascular Closure Device for large-bore arteriotomy closure. The trial supports planned regulatory submissions in the United States and Europe.

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.