Global Acuo Vendor Neutral Archive Market

Market Size in USD Billion

USD

4.18 Billion

USD

6.76 Billion

2025

2033

USD

4.18 Billion

USD

6.76 Billion

2025

2033

| 2026 - 2033 | |

| USD 4.18 Billion | |

| USD 6.76 Billion | |

| % | |

|

Acuo Vendor Neutral Archive Market Overview

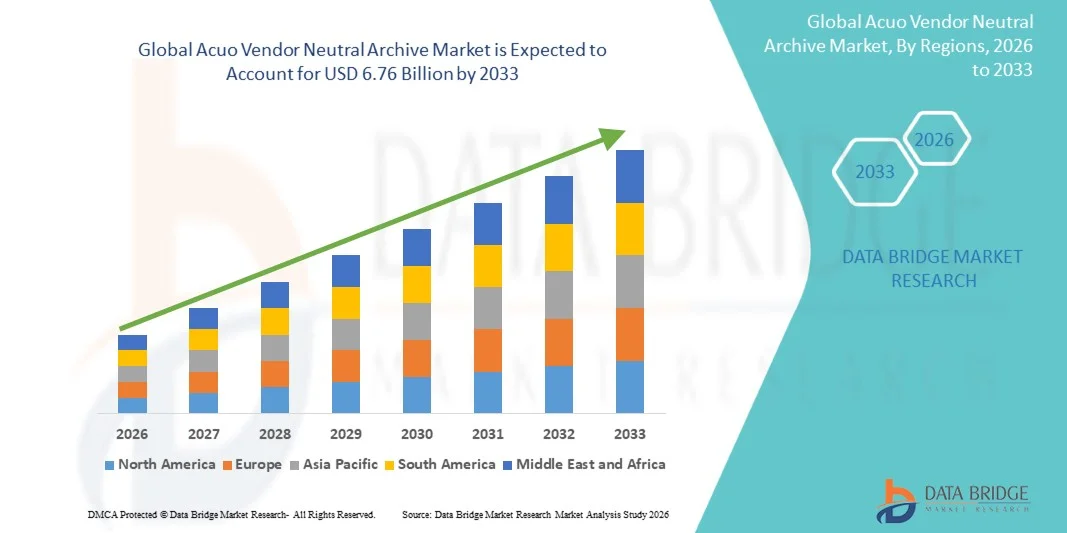

The Acuo Vendor Neutral Archive Market was valued at USD 4.18 billion in 2025 and is projected to reach USD 6.76 billion by 2033, growing at a CAGR of 6.2% from 2026 to 2033. The market is experiencing strong growth driven by the increasing adoption of digital healthcare technologies, rising volumes of medical imaging data, and growing demand for centralized and interoperable healthcare information management systems across hospitals and diagnostic centers.

The rapid expansion of imaging procedures worldwide, combined with the need for long-term storage, seamless data accessibility, and improved clinical workflow efficiency, is compelling healthcare providers to adopt advanced Vendor Neutral Archive (VNA) solutions. Traditional image storage systems are increasingly being replaced by vendor-neutral platforms that enable healthcare organizations to consolidate data from multiple imaging modalities and healthcare IT systems into a single repository. In addition, growing implementation of electronic health records (EHRs), increasing emphasis on healthcare interoperability, and rising adoption of cloud-based storage solutions are accelerating market growth. Advanced VNA platforms support secure data sharing, reduce vendor lock-in, enhance clinical collaboration, and improve patient care outcomes, making them an essential component of modern healthcare infrastructure. Furthermore, increasing investments in healthcare digitization initiatives and the integration of artificial intelligence (AI) and analytics technologies are creating new opportunities for the expansion of the global Vendor Neutral Archive market.

Key Market Trends & Insights

- North America dominated the Acuo Vendor Neutral Archive Market with the largest revenue share of 39.12% in 2025, supported by widespread adoption of healthcare IT solutions, high digital imaging volumes, strong interoperability initiatives, and significant investments in cloud-based healthcare infrastructure.

- The On-Premise Vendor Neutral Archive segment led the market with a 46.85% share in 2025, driven by healthcare organizations' preference for enhanced data control, regulatory compliance, security, and seamless integration with existing hospital IT systems.

- Asia-Pacific is expected to be the fastest-growing region at a CAGR of 8.4% from 2026 to 2033, fueled by rapid healthcare digitization, expanding healthcare infrastructure, increasing medical imaging volumes, and rising investments in cloud-based healthcare technologies across China, India, Japan, and Southeast Asia.

- The Fully Cloud-Hosted Vendor Neutral Archive segment is the fastest-growing delivery mode, projected to register a CAGR of 9.1% from 2026 to 2033, reflecting growing demand for scalable storage solutions, remote accessibility, disaster recovery capabilities, and reduced infrastructure costs.

- The Multi-Site Vendor Neutral Archive segment dominates the procurement model category with a 42.37% revenue share in 2025, led by increasing adoption among integrated healthcare networks seeking centralized image management and seamless data sharing across multiple facilities.

- PACS Vendors account for 48.63% of the market, benefiting from their established customer base, strong integration capabilities, and extensive experience in medical imaging workflow management.

- The Independent Software Vendors (ISVs) segment is the fastest-growing type category, with a CAGR of 8.8%, driven by increasing demand for vendor-agnostic interoperability solutions, cloud-native architectures, AI-enabled imaging workflows, and advanced healthcare data management platforms.

- The PACS Vendors segment dominated the market with a 63% share in 2025 due to their extensive experience in medical imaging workflow management and strong relationships with healthcare providers worldwide.

Market Size & Forecast

- Global Market Value (2025): USD 4.18 Billion

- Expected Market Value (2033): USD 6.76 Billion

- Forecast CAGR (2026–2033): 6.2%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia-Pacific

Report Scope and Acuo Vendor Neutral Archive Market Segmentation

|

Attributes |

Acuo Vendor Neutral Archive Key Market Insights |

|

Segments Covered |

· By Delivery Mode: On-Premise Vendor Neutral Archive, Hybrid Vendor Neutral Archive, Fully Cloud-Hosted Vendor Neutral Archive · By Procurement Model: Departmental Vendor Neutral Archive, Multi-Departmental Vendor Neutral Archive, Multi-Site Vendor Neutral Archive · By Type: PACS Vendors, Independent Software Vendors, Infrastructure Vendors |

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

· FUJIFILM Holdings Corporation (Japan) · Hyland Software, Inc. (U.S.) · Merative (formerly IBM Watson Health) (U.S.) · Agfa-Gevaert Group (Belgium) · GE HealthCare Technologies Inc. (U.S.) · Koninklijke Philips N.V. (Netherlands) · Sectra AB (Sweden) · Change Healthcare (U.S.) · Dell Technologies Inc. (U.S.) · Oracle Corporation (U.S.) · Microsoft Corporation (U.S.) · BridgeHead Software Ltd. (U.K.) · Novarad Corporation (U.S.) · Canon Medical Systems Corporation (Japan) · INFINITT Healthcare Co., Ltd. (South Korea) · Mach7 Technologies Ltd. (Australia) · Lexmark Healthcare (U.S.) · Visage Imaging Inc. (U.S.) · Carestream Health, Inc. (U.S.) · OpenText Corporation (Canada) · Arcadia.io, Inc. (U.S.) · Dedalus Group (Italy) · InterSystems Corporation (U.S.) · Iron Mountain Incorporated (U.S.) · Commvault Systems, Inc. (U.S.) · Hitachi Digital Services (Japan) · Pure Storage, Inc. (U.S.) · Nutanix, Inc. (U.S.) · Amazon Web Services, Inc. (U.S.) · Google Cloud (U.S.) · VMware LLC (U.S.) · CereCore LLC (U.S.) · Acuo Technologies (now part of Hyland) (U.S.) · Paragon Consulting Partners (U.S.) |

|

Market Opportunities |

· Growing Adoption of Cloud-Based Healthcare Data Management Solutions · Rising Demand for Healthcare Interoperability and Enterprise Imaging · Integration of Artificial Intelligence and Advanced Analytics |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, geographically represented company-wise production and capacity, network layouts of distributors and partners, detailed and updated price trend analysis and deficit analysis of supply chain and demand. |

Acuo Vendor Neutral Archive Market Trends

Trend: Growing Adoption of Cloud-Based and Enterprise Imaging Solutions

The Acuo Vendor Neutral Archive (VNA) market is witnessing a strong shift toward cloud-based deployment models and enterprise imaging strategies as healthcare organizations seek scalable, interoperable, and cost-efficient solutions for managing rapidly growing medical imaging datasets. Hospitals and integrated delivery networks are increasingly consolidating imaging data from radiology, cardiology, pathology, oncology, and other departments into centralized vendor-neutral repositories. Cloud-enabled VNA platforms facilitate seamless image sharing across healthcare facilities, support remote clinical access, and improve disaster recovery capabilities. In addition, the growing adoption of enterprise imaging initiatives and value-based healthcare models is accelerating demand for VNA solutions that enable longitudinal patient records and improved care coordination across healthcare systems.

Acuo Vendor Neutral Archive Market Dynamics

Key Market Driver: Increasing Volume of Medical Imaging Data and Demand for Healthcare Interoperability

The rapid growth in diagnostic imaging procedures worldwide is a major factor driving demand for Acuo Vendor Neutral Archive solutions. Healthcare providers generate billions of medical images annually from modalities such as MRI, CT, X-ray, ultrasound, mammography, and PET scans. As imaging volumes continue to rise, healthcare organizations are increasingly seeking centralized platforms capable of securely storing, managing, and sharing imaging data across multiple departments and locations.

The growing emphasis on interoperability is further accelerating market growth. Healthcare providers are adopting VNA platforms to eliminate data silos, reduce vendor lock-in, and facilitate seamless integration with Picture Archiving and Communication Systems (PACS), Electronic Health Records (EHRs), and enterprise imaging platforms. According to industry estimates, medical imaging data accounts for nearly 90% of healthcare data generated globally, highlighting the critical need for scalable archive solutions capable of supporting long-term data retention and accessibility requirements.

Key Restraint/Challenge: Data Security, Privacy Concerns, and Complex System Integration

A significant challenge in the Acuo Vendor Neutral Archive Market is ensuring data security and regulatory compliance while managing large volumes of sensitive patient information. Healthcare organizations must comply with strict regulations regarding patient privacy, data protection, and information governance, which can increase implementation complexity and operational costs.

In addition, integrating VNA platforms with legacy PACS systems, hospital information systems, and multiple imaging modalities often requires substantial technical expertise and infrastructure investment. Data migration projects involving millions of imaging studies can be time-consuming and resource-intensive. The transition to cloud-based archives also raises concerns regarding cybersecurity risks, unauthorized access, and data breaches, particularly among healthcare providers handling highly sensitive patient records. These challenges can slow adoption, especially among smaller healthcare facilities with limited IT resources.

Key Market Opportunity: Integration of Artificial Intelligence and Advanced Imaging Analytics

The integration of artificial intelligence (AI), machine learning, and advanced analytics capabilities into Vendor Neutral Archive platforms presents a significant market opportunity. AI-enabled VNA solutions can automate image classification, metadata extraction, workflow optimization, and clinical decision support, enhancing both operational efficiency and diagnostic accuracy.

For instance, healthcare organizations are increasingly deploying AI-powered imaging platforms to assist radiologists in detecting abnormalities, prioritizing urgent cases, and improving reporting efficiency. The growing adoption of cloud-native VNA architectures is further supporting AI integration by providing scalable computing resources and centralized access to imaging datasets required for algorithm training and validation. Furthermore, increasing investments in digital healthcare transformation, telemedicine, precision medicine, and enterprise imaging initiatives are creating new opportunities for VNA providers. The development of interoperable, AI-enabled imaging ecosystems capable of supporting multi-site healthcare networks is expected to drive substantial growth across North America, Europe, Asia-Pacific, Latin America, and the Middle East during the forecast period.

Acuo Vendor Neutral Archive Market Scope

The Acuo Vendor Neutral Archive market is segmented on the basis of delivery mode, procurement model, and type.

- By Delivery Mode

On the basis of delivery mode, the Acuo Vendor Neutral Archive Market is segmented into On-Premise Vendor Neutral Archive, Hybrid Vendor Neutral Archive, and Fully Cloud-Hosted Vendor Neutral Archive. The On-Premise Vendor Neutral Archive segment dominated the market with a 46.85% share in 2025 due to its widespread adoption among large hospitals, integrated delivery networks, and healthcare systems that require maximum control over patient data, storage infrastructure, and regulatory compliance processes. Healthcare providers continue to prefer on-premise deployments for managing highly sensitive medical imaging data while maintaining strict adherence to data privacy regulations. The segment benefits from strong cybersecurity controls, reduced dependency on external service providers, and seamless integration with existing PACS, RIS, EHR, and hospital information systems. In addition, many healthcare organizations have significant legacy infrastructure investments, making on-premise deployment a practical long-term solution. The ability to provide low-latency access to imaging studies and ensure uninterrupted clinical workflows further supports adoption. Growing imaging volumes across radiology, cardiology, oncology, and pathology departments also reinforce demand. Furthermore, large healthcare institutions often possess the technical expertise and capital resources required to manage on-premise VNA environments effectively, strengthening the segment's leading position globally.

The Fully Cloud-Hosted Vendor Neutral Archive segment is projected to register the fastest growth at a CAGR of 9.1% from 2026 to 2033, driven by increasing demand for scalable, flexible, and cost-efficient healthcare data storage solutions. Cloud-hosted VNA platforms eliminate the need for extensive onsite infrastructure while enabling rapid deployment and simplified maintenance. Healthcare providers are increasingly adopting cloud architectures to support enterprise imaging initiatives, remote clinical access, telehealth expansion, and disaster recovery capabilities. The growing need to manage exponentially increasing medical imaging datasets is encouraging migration toward cloud-based platforms. In addition, advancements in healthcare cybersecurity, cloud compliance frameworks, and secure data encryption technologies are improving confidence in cloud deployments. The ability to support multi-site healthcare networks, facilitate seamless image sharing, and integrate advanced AI analytics further accelerates adoption. Rising investments in digital healthcare transformation across emerging and developed markets are expected to drive substantial segment growth throughout the forecast period.

- By Procurement Model

On the basis of procurement model, the Acuo Vendor Neutral Archive Market is segmented into Departmental Vendor Neutral Archive, Multi-Departmental Vendor Neutral Archive, and Multi-Site Vendor Neutral Archive. The Multi-Site Vendor Neutral Archive segment dominated the market with a 42.37% share in 2025 due to the increasing need for centralized image management across large healthcare networks and hospital systems. Healthcare organizations are actively consolidating imaging data from multiple facilities into unified archives to improve accessibility, operational efficiency, and continuity of care. The segment benefits from growing enterprise imaging initiatives that require secure access to patient records across geographically dispersed locations. Multi-site VNAs enable healthcare providers to reduce duplicate imaging procedures, streamline clinical workflows, and improve collaboration among physicians and specialists. Additionally, healthcare mergers and acquisitions are creating larger provider networks that require centralized imaging repositories. The increasing adoption of cloud and hybrid infrastructure further supports implementation across multiple facilities. Improved disaster recovery capabilities and long-term data retention strategies also contribute to segment growth. These advantages continue to position multi-site deployments as the preferred procurement model among large healthcare systems globally.

The Multi-Departmental Vendor Neutral Archive segment is anticipated to witness the fastest CAGR of 8.7% from 2026 to 2033, driven by growing adoption of enterprise imaging strategies within individual healthcare facilities. Hospitals are increasingly integrating imaging data from radiology, cardiology, pathology, oncology, dermatology, and other departments into centralized archives. This approach improves interoperability, reduces data silos, and enhances clinical decision-making. Increasing demand for comprehensive patient records and coordinated care delivery is accelerating implementation. Furthermore, multi-departmental VNAs support improved workflow efficiency, lower storage costs, and easier compliance management. Growing investments in digital transformation initiatives and interoperability frameworks are expected to further stimulate demand during the forecast period.

- By Type

On the basis of type, the Acuo Vendor Neutral Archive Market is segmented into PACS Vendors, Independent Software Vendors, and Infrastructure Vendors. The PACS Vendors segment dominated the market with a 48.63% share in 2025 due to their extensive experience in medical imaging workflow management and strong relationships with healthcare providers worldwide. These vendors possess large installed customer bases and offer integrated imaging solutions that combine PACS functionality with advanced VNA capabilities. Their ability to deliver comprehensive imaging ecosystems, including image acquisition, storage, visualization, and data management, strengthens their market position. Healthcare organizations often prefer established PACS vendors because of proven reliability, strong technical support, and seamless integration capabilities. Additionally, ongoing investments in enterprise imaging, cloud migration, and interoperability solutions continue to expand opportunities for PACS vendors. Growing demand for centralized imaging archives and long-term image retention further supports segment dominance. Strategic partnerships, product innovations, and acquisitions within the healthcare IT sector also contribute to continued market leadership.

The Independent Software Vendors (ISVs) segment is expected to witness the fastest CAGR of 8.8% from 2026 to 2033, driven by increasing demand for vendor-agnostic and interoperable imaging solutions. Healthcare providers are increasingly seeking flexible platforms that can integrate with multiple PACS systems, EHR platforms, and imaging modalities without creating vendor lock-in. ISVs offer specialized software solutions designed to enhance interoperability, improve workflow efficiency, and support enterprise-wide imaging strategies. Growing adoption of cloud-native architectures, AI-powered analytics, and advanced data management capabilities is further accelerating segment growth. In addition, healthcare organizations undergoing digital transformation initiatives are increasingly choosing independent software platforms that provide scalability and customization. The rising focus on open standards, data accessibility, and long-term healthcare interoperability is expected to drive strong growth for ISVs throughout the forecast period.

Acuo Vendor Neutral Archive Market Regional Analysis

North America dominated the Acuo Vendor Neutral Archive market and accounted for the largest revenue share of 39.12% in 2025, supported by widespread adoption of healthcare IT solutions, high digital imaging volumes, strong interoperability initiatives, and significant investments in cloud-based healthcare infrastructure. The region benefits from advanced healthcare systems, widespread implementation of electronic health records (EHRs), and increasing demand for enterprise imaging solutions. Healthcare providers are increasingly adopting Vendor Neutral Archive platforms to improve data accessibility, eliminate vendor lock-in, and support long-term medical image management. In addition, growing utilization of artificial intelligence, cloud computing, and enterprise imaging strategies continues to strengthen North America's leadership position in the global market.

U.S. Acuo Vendor Neutral Archive Market Insight

The U.S. Acuo Vendor Neutral Archive market is witnessing strong growth due to increasing adoption of enterprise imaging platforms, growing volumes of diagnostic imaging procedures, and rising investments in healthcare digital transformation initiatives. The country's highly developed healthcare infrastructure, combined with widespread EHR implementation and interoperability requirements, is driving demand for advanced VNA solutions. In addition, increasing adoption of cloud-based healthcare storage platforms, AI-enabled imaging workflows, and value-based care models is accelerating market expansion across hospitals, imaging centers, and integrated healthcare networks.

Europe Acuo Vendor Neutral Archive Market Insight

The Europe Acuo Vendor Neutral Archive market remains a major contributor to global revenue, driven by growing healthcare digitization efforts, increasing adoption of enterprise imaging strategies, and strong regulatory support for healthcare interoperability. Healthcare providers across the region are investing in centralized imaging repositories to improve clinical collaboration and patient care continuity. Increasing implementation of cloud-enabled healthcare solutions, coupled with rising demand for long-term image archiving and secure data exchange, continues to enhance adoption of Vendor Neutral Archive platforms throughout Europe.

U.K. Acuo Vendor Neutral Archive Market Insight

The U.K. Acuo Vendor Neutral Archive market is experiencing steady growth, supported by ongoing National Health Service (NHS) digital transformation initiatives and increasing demand for integrated healthcare information systems. Healthcare organizations are adopting VNA solutions to consolidate imaging data across multiple facilities and improve accessibility for clinicians. Furthermore, growing investments in cloud healthcare infrastructure, cybersecurity, and interoperability technologies are contributing significantly to market growth and innovation in the country.

Germany Acuo Vendor Neutral Archive Market Insight

The Germany Acuo Vendor Neutral Archive market is expanding steadily due to the country's advanced healthcare infrastructure, strong focus on healthcare digitization, and increasing adoption of enterprise imaging solutions. Hospitals and healthcare networks are increasingly implementing VNA platforms to improve medical image accessibility, streamline workflows, and support interoperability requirements. In addition, rising investments in cloud computing, healthcare analytics, and digital health technologies are further driving market growth in Germany.

Asia-Pacific Acuo Vendor Neutral Archive Market Insight

The Asia-Pacific Acuo Vendor Neutral Archive market is expected to witness the fastest growth at a CAGR of 8.4% from 2026 to 2033, driven by rapid healthcare digitization, expanding healthcare infrastructure, increasing medical imaging volumes, and rising investments in cloud-based healthcare technologies across China, India, Japan, and Southeast Asia. Growing healthcare expenditure, rising adoption of electronic medical records, and increasing awareness regarding data interoperability are supporting regional market expansion. Furthermore, government initiatives focused on healthcare modernization and digital transformation are accelerating VNA adoption across hospitals and diagnostic centers.

Japan Acuo Vendor Neutral Archive Market Insight

The Japan Acuo Vendor Neutral Archive market is witnessing consistent growth due to increasing adoption of advanced healthcare IT systems, rising diagnostic imaging volumes, and growing demand for efficient healthcare data management solutions. Healthcare providers are investing in enterprise imaging platforms to improve operational efficiency and patient care outcomes. Moreover, the country's strong focus on healthcare innovation, aging population management, and digital health transformation is contributing significantly to market growth.

China Acuo Vendor Neutral Archive Market Insight

The China Acuo Vendor Neutral Archive market is growing rapidly, driven by expanding healthcare infrastructure, increasing healthcare digitization initiatives, and rising demand for advanced medical imaging management solutions. Growing adoption of cloud computing, artificial intelligence, and interoperable healthcare platforms is significantly boosting market demand. In addition, government investments in healthcare modernization, increasing imaging procedure volumes, and rising implementation of electronic health record systems are positioning China as one of the fastest-growing markets for Acuo Vendor Neutral Archive solutions globally.

Acuo Vendor Neutral Archive Market Share

The Acuo Vendor Neutral Archive industry is primarily led by well-established companies, including:

- FUJIFILM Holdings Corporation (Japan)

- Hyland Software, Inc. (U.S.)

- Merative (formerly IBM Watson Health) (U.S.)

- Agfa-Gevaert Group (Belgium)

- GE HealthCare Technologies Inc. (U.S.)

- Koninklijke Philips N.V. (Netherlands)

- Sectra AB (Sweden)

- Change Healthcare (U.S.)

- Dell Technologies Inc. (U.S.)

- Oracle Corporation (U.S.)

- Microsoft Corporation (U.S.)

- BridgeHead Software Ltd. (U.K.)

- Novarad Corporation (U.S.)

- Canon Medical Systems Corporation (Japan)

- INFINITT Healthcare Co., Ltd. (South Korea)

- Mach7 Technologies Ltd. (Australia)

- Lexmark Healthcare (U.S.)

- Visage Imaging Inc. (U.S.)

- Carestream Health, Inc. (U.S.)

- OpenText Corporation (Canada)

- Arcadia.io, Inc. (U.S.)

- Dedalus Group (Italy)

- InterSystems Corporation (U.S.)

- Iron Mountain Incorporated (U.S.)

- Commvault Systems, Inc. (U.S.)

- Hitachi Digital Services (Japan)

- Pure Storage, Inc. (U.S.)

- Nutanix, Inc. (U.S.)

- Amazon Web Services, Inc. (U.S.)

- Google Cloud (U.S.)

- VMware LLC (U.S.)

- CereCore LLC (U.S.)

- Acuo Technologies (now part of Hyland) (U.S.)

- Paragon Consulting Partners (U.S.)

Latest Developments in Acuo Vendor Neutral Archive Market

- In September 2021, Hyland Healthcare announced support for the AWS for Health initiative to accelerate deployment of its Acuo Vendor Neutral Archive (VNA) and NilRead enterprise diagnostic viewer on Amazon Web Services (AWS). The collaboration was designed to help healthcare organizations scale cloud-based enterprise imaging environments, improve interoperability, and manage rapidly growing medical imaging datasets more efficiently. This development highlighted the increasing shift toward cloud-enabled VNA infrastructure across healthcare systems

- In December 2021, Mach7 Technologies partnered with ImageMover to enhance encounter-based imaging capabilities within its Enterprise Imaging Solution. The partnership integrated ImageMover’s point-of-care imaging workflow technology with Mach7’s Vendor Neutral Archive platform, enabling healthcare providers to capture, archive, and manage both DICOM and non-DICOM medical images through a unified enterprise imaging ecosystem

- In April 2021, Mach7 Technologies received Frost & Sullivan’s 2021 Global Enterprise Imaging Solutions Product Leadership Award for its Vendor Neutral Archive and enterprise imaging platform. The recognition highlighted Mach7’s innovation in healthcare imaging interoperability, enterprise-wide image management, and vendor-neutral data management capabilities that support healthcare organizations transitioning from legacy PACS environments

- In February 2023, Mach7 Technologies was recognized as a Top Performer in the Best in KLAS 2023 Report for its enterprise imaging and Vendor Neutral Archive solutions. The recognition reflected strong customer satisfaction, interoperability capabilities, and the company’s growing role in supporting healthcare providers with centralized image management, enterprise viewing, and cloud-connected imaging workflows

- In January 2023, Mach7 Technologies secured a multi-year contract valued at approximately AU$16.7 million with Akumin Inc. for deployment of its Enterprise Imaging Platform, including Vendor Neutral Archive (VNA), eUnity Diagnostic Viewer, and workflow applications. The agreement demonstrated increasing healthcare demand for cloud-based enterprise imaging platforms capable of supporting large-scale imaging data management and interoperability requirements

- In September 2023, Mach7 Technologies was selected as a solution provider for the U.S. Veterans Health Administration’s National Teleradiology Program (NTP) NextGen PACS initiative. Under the multi-phase program, Mach7 provided its Vendor Neutral Archive (VNA), eUnity Diagnostic Viewer, and professional services to support next-generation imaging workflows across one of the largest healthcare systems in the United States

- In February 2024, Hyland Healthcare announced a strategic partnership with iTernity to strengthen healthcare data archiving and enterprise imaging management. The collaboration combined Hyland’s Acuo Vendor Neutral Archive platform with iTernity’s secure archiving technologies to improve healthcare data protection, long-term retention, interoperability, and regulatory compliance across healthcare organizations

- In July 2024, the U.S. Department of Veterans Affairs Technology Reference Model (TRM) reaffirmed approval and recognition of Hyland’s Acuo Vendor Neutral Archive technology for healthcare imaging environments. The update reinforced the platform’s continued relevance in supporting secure medical image management, interoperability, and enterprise imaging infrastructure across large healthcare networks

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.