Global Acute Cholecystitis Market

Market Size in USD Billion

USD

6.00 Billion

USD

10.30 Billion

2024

2032

USD

6.00 Billion

USD

10.30 Billion

2024

2032

| 2025 - 2032 | |

| USD 6.00 Billion | |

| USD 10.30 Billion | |

| % | |

|

Acute Cholecystitis Market Size

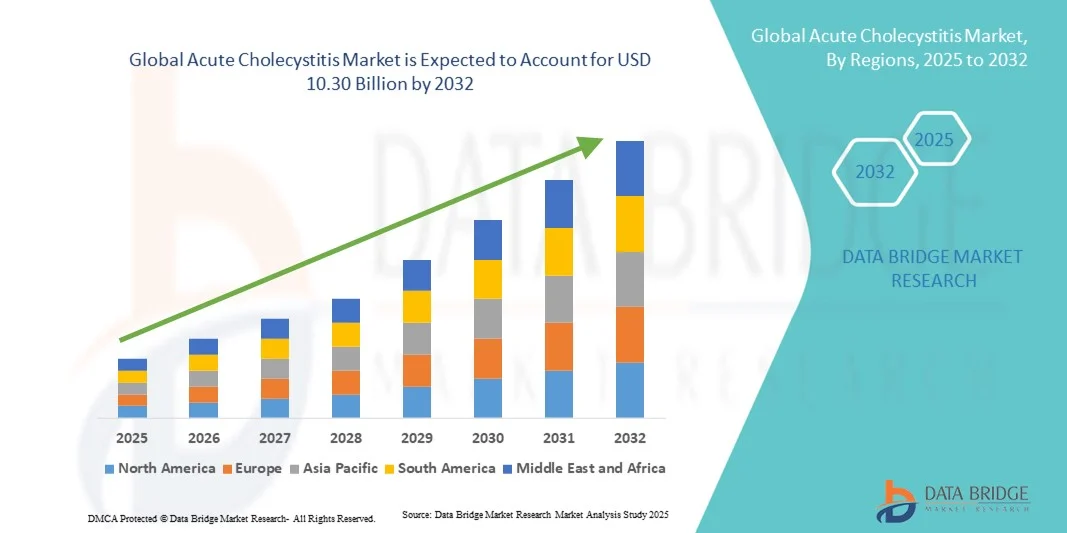

- The global acute cholecystitis market size was valued at USD 6.00 billion in 2024 and is expected to reach USD 10.30 billion by 2032, at a CAGR of 7.00% during the forecast period

- The market growth is largely fueled by the increasing prevalence of gallbladder disorders and gastrointestinal diseases, rising geriatric population, and growing awareness about early diagnosis and treatment of acute cholecystitis. Expanding healthcare infrastructure and easy access to treatment options are further supporting market growth

- Furthermore, the market is driven by advancements in minimally invasive surgical techniques, laparoscopic procedures, and innovative drug therapies for managing acute cholecystitis. Increasing investments by key players in R&D, as well as rising awareness among patients and healthcare providers, are significantly boosting adoption of effective treatments and contributing to overall industry growth

Acute Cholecystitis Market Analysis

- The Acute Cholecystitis Market is witnessing strong growth due to the rising prevalence of gallbladder disorders, increasing geriatric population, and growing awareness about timely diagnosis and treatment. Expanding healthcare infrastructure, easy access to treatment options, and improving insurance coverage are driving market adoption globally

- Furthermore, the market is fueled by advancements in minimally invasive surgical procedures, laparoscopic cholecystectomy techniques, and innovative drug therapies. Increasing investments by key pharmaceutical and medical device companies in R&D, coupled with rising awareness among patients and healthcare providers, are significantly boosting adoption and market growth

- North America dominated the acute cholecystitis market with a revenue share of 39.5% in 2024, driven by advanced healthcare infrastructure, high disposable incomes, and strong adoption of minimally invasive treatment options. The U.S. remains the largest contributor due to high healthcare spending and early access to new therapies

- Asia-Pacific is expected to be the fastest-growing region during the forecast period (2025–2032), with a CAGR, owing to increasing urbanization, growing healthcare expenditure, rising geriatric population, and expanding awareness about gallbladder disorders in countries like China, India, and Japan

- The calculous cholecystitis segment dominated the largest market revenue share of 72.3% in 2024, as gallstones account for most cases globally. High prevalence due to dietary habits, obesity, and aging populations drives adoption

Report Scope and Acute Cholecystitis Market Segmentation

|

Attributes |

Acute Cholecystitis Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Acute Cholecystitis Market Trends

Enhanced Convenience and Improved Patient Care

- A significant and accelerating trend in the global acute cholecystitis market is the increasing focus on patient-centric treatment approaches and advanced clinical management protocols. This trend is significantly enhancing the effectiveness of care delivery and overall patient outcomes

- For instance, in several leading hospitals, multidisciplinary treatment teams are implementing evidence-based guidelines for acute cholecystitis, ensuring timely diagnosis, risk stratification, and appropriate intervention. Similarly, enhanced post-operative care protocols are reducing complications and promoting faster recovery

- Advances in diagnostic imaging, minimally invasive surgical techniques, and targeted therapeutic interventions enable healthcare providers to offer precise and personalized treatment for patients with acute cholecystitis. For instance, laparoscopic cholecystectomy has become the preferred treatment method due to shorter hospital stays, lower complication rates, and faster recovery times. Furthermore, emerging pharmaceutical therapies are being evaluated for reducing inflammation and improving bile flow, enhancing treatment outcomes

- The integration of standardized clinical pathways with digital health records and patient monitoring systems facilitates coordinated care across different departments, enabling timely interventions and improved follow-up. Through these systems, physicians can monitor patient progress, adjust treatment plans, and reduce the risk of readmissions

- This trend towards more efficient, patient-focused, and evidence-based treatment protocols is fundamentally reshaping clinical expectations and standards of care for acute cholecystitis. Consequently, hospitals and healthcare providers are adopting comprehensive treatment plans combining surgical, pharmacological, and supportive care measures to improve patient outcomes

- The demand for improved diagnostic accuracy, minimally invasive procedures, and optimized treatment pathways is growing rapidly across both developed and developing regions, as healthcare institutions increasingly prioritize clinical efficacy and patient satisfaction

Acute Cholecystitis Market Dynamics

Driver

Growing Need Due to Rising Prevalence and Focus on Early Intervention

- The increasing prevalence of acute cholecystitis, coupled with rising awareness about early diagnosis and treatment, is a significant driver for the heightened demand for advanced therapeutic and diagnostic solutions

- For instance, in April 2024, several hospitals in Europe introduced enhanced imaging protocols and early intervention strategies to improve patient management. Such initiatives by key healthcare institutions are expected to drive the Acute Cholecystitis industry growth in the forecast period

- As healthcare providers become more aware of potential complications associated with delayed treatment, there is a growing emphasis on minimally invasive surgical techniques, early pharmacological interventions, and evidence-based clinical pathways to enhance patient outcomes

- Furthermore, the increasing availability of advanced imaging systems, laparoscopy equipment, and specialized surgical tools is making modern treatment of Acute Cholecystitis more efficient and effective, improving both recovery times and patient safety

- The convenience of rapid diagnosis, early therapeutic intervention, and structured post-operative care are key factors propelling the adoption of advanced treatment approaches in both hospitals and specialized care centers. The trend towards improved healthcare infrastructure and clinician training further contributes to market growth

Restraint/Challenge

Concerns Regarding High Treatment Costs and Limited Access to Advanced Facilities

- The high cost of advanced surgical procedures, imaging systems, and specialized care poses a significant challenge to broader market penetration, particularly in low-income and rural regions. As treatment relies on specialized equipment and skilled professionals, the affordability and accessibility of care remain major concerns

- For instance, reports of high out-of-pocket expenses for laparoscopic procedures have made some patients hesitant to seek timely treatment, leading to potential complications and prolonged hospitalization

- Addressing these challenges through subsidized healthcare programs, insurance coverage, and expanded access to advanced treatment facilities is crucial for improving patient reach. Healthcare providers are increasingly offering cost-effective bundles and outpatient management options to enhance affordability

- In addition, disparities in infrastructure and availability of specialized care between urban and rural areas can hinder timely intervention

- While costs are gradually decreasing through technological advancements and increased adoption of minimally invasive procedures, perceived high treatment expenses can still restrict access, especially for patients without adequate insurance coverage or in developing regions

- Overcoming these challenges through enhanced healthcare funding, awareness campaigns about early diagnosis, and development of cost-effective treatment approaches will be vital for sustained market growth

Acute Cholecystitis Market Scope

The market is segmented on the basis of treatment, symptoms, causes, diagnosis, end-users, and distribution channel

- By Treatment

On the basis of treatment, the Acute Cholecystitis market is segmented into fluids, antibiotics, pain relievers, and cholecystectomy. The antibiotics segment dominated the largest market revenue share of 41.5% in 2024, driven by their use in mild to moderate infections to prevent complications. Broad-spectrum antibiotics are widely administered initially, followed by targeted therapies. Adoption is supported by hospital protocols, early diagnosis, and clinical guidelines. Both inpatient and outpatient care contribute to the segment’s dominance. Oral and intravenous formulations provide flexibility. The availability in hospital pharmacies and retail chains ensures easy access. High patient compliance and effectiveness increase physician preference. Growing awareness of infection control enhances usage. Combination therapy with fluids and pain relievers further strengthens adoption. Increasing prevalence of bacterial cholecystitis worldwide sustains the segment’s market share. Repeated treatment cycles in recurrent cases also drive consumption.

The cholecystectomy segment is expected to witness the fastest CAGR of 19.2% from 2025 to 2032, driven by rising minimally invasive procedures. Laparoscopic surgeries offer reduced recovery time and lower complications. Adoption is supported by surgical infrastructure improvements, trained surgeons, and hospital capacity expansion. Increasing patient preference for definitive treatment over prolonged medical therapy fuels growth. Awareness campaigns highlight benefits of early surgical intervention. Growth is further enhanced in emerging markets due to healthcare modernization. Guidelines recommend early cholecystectomy in acute calculous cases. Technological advances in robotic-assisted surgery expand procedural options. Higher reimbursement rates for surgical procedures increase adoption. Hospital-based implementation is rising. The segment benefits from increased outpatient surgery centers and enhanced recovery protocols.

- By Symptoms

On the basis of symptoms, the market is segmented into abdominal pain, fever, nausea, clay-colored stool, jaundice, loss of appetite, and others. The abdominal pain segment dominated the largest market revenue share of 46.7% in 2024, as it is the primary symptom prompting clinical evaluation. Pain intensity often dictates urgency of care. Both emergency and outpatient facilities rely on pain assessment for diagnosis. Analgesic management supports supportive care protocols. High prevalence of severe abdominal pain among patients drives pharmaceutical and procedural adoption. Early detection and treatment improve patient outcomes. Hospitals and clinics focus on pain as a key triage factor. Awareness of pain patterns among patients leads to earlier hospital visits. Repeat visits due to chronic gallstone disease reinforce segment demand. Diagnostic imaging complements pain evaluation. Pain severity influences both inpatient stay and outpatient follow-up care. Standard treatment protocols incorporate pain relief in all cases.

The jaundice segment is expected to witness the fastest CAGR of 18.5% from 2025 to 2032, driven by rising incidence of complicated cholecystitis and bile duct obstruction. Early detection through liver function tests and imaging accelerates intervention. Hospitals increasingly prioritize management of jaundiced patients. Awareness campaigns and patient education increase hospital visits. Adoption of rapid diagnostic techniques supports timely treatment. Growth is driven by hospital admissions for obstructive complications. Clinicians use jaundice as a key marker for urgent procedures. Development of minimally invasive treatment strategies accelerates adoption. Rising global prevalence of complicated cases contributes to segment expansion. Expansion of diagnostic imaging in emerging markets supports growth. Telemedicine and early consultation further drive uptake. Patient demand for safe and quick treatment promotes intervention.

- By Causes

On the basis of causes, the market is segmented into calculous cholecystitis, acalculous cholecystitis, and others. The calculous cholecystitis segment dominated the largest market revenue share of 72.3% in 2024, as gallstones account for most cases globally. High prevalence due to dietary habits, obesity, and aging populations drives adoption. Hospitals prioritize diagnostic imaging for stone detection. Early intervention improves outcomes and reduces complications. Minimally invasive surgery adoption is higher in calculous cases. Awareness among at-risk populations increases hospital visits. Outpatient and inpatient treatments reinforce segment growth. Treatment guidelines recommend early intervention in symptomatic cases. Repeat incidence of gallstone-related episodes boosts demand. Clinician preference for evidence-based therapy sustains market share. Combination treatment with fluids, antibiotics, and analgesics strengthens segment adoption. Surgical interventions in calculous cases dominate revenue due to higher treatment cost.

The acalculous cholecystitis segment is expected to witness the fastest CAGR of 20.1% from 2025 to 2032, mainly in critically ill or post-surgical patients. Hospitalized patients in ICU settings often require early detection and aggressive intervention. Adoption of diagnostic imaging and lab tests accelerates treatment. Awareness of risk factors among clinicians drives early treatment. Growth is fueled by rising prevalence in post-operative and critically ill populations. Minimally invasive management approaches are increasing. ICU and hospital-based care ensure higher treatment volumes. Early intervention reduces mortality, boosting adoption. Emerging markets are witnessing higher detection rates due to improved hospital facilities. Physician training programs emphasize rapid recognition of acalculous cases. Technological advances in bedside imaging support early diagnosis. Insurance coverage and guideline-based care reinforce growth.

- By Diagnosis

On the basis of diagnosis, the market is segmented into blood tests, hepatobiliary scintigraphy, ultrasound scan, X-ray, CT scan, MRI, liver function test, and others. The ultrasound scan segment dominated the largest market revenue share of 55.6% in 2024, due to its non-invasive nature, cost-effectiveness, and high diagnostic accuracy. Ultrasound is the standard initial imaging for gallstones and inflammation. Rapid bedside diagnostics enhance adoption. Hospitals and clinics widely use ultrasound. Portable devices improve accessibility in emergency settings. Patient preference for non-invasive methods increases utilization. Repeated testing in recurrent or chronic cases boosts market volume. Integration with treatment planning supports clinical decision-making. High availability in emerging markets drives penetration. Training programs for technicians improve operational efficiency. Insurance reimbursement further supports usage.

The CT scan segment is expected to witness the fastest CAGR of 17.4% from 2025 to 2032, driven by detection of complicated or atypical cases. CT aids in early detection of perforation, abscesses, and severe inflammation. Increasing availability of advanced imaging equipment in hospitals accelerates adoption. Emerging markets show higher uptake due to new hospital infrastructure. Hospital and specialty clinics implement CT for complex cases. Rapid diagnosis leads to timely surgical intervention. Insurance coverage supports adoption. Rising awareness among clinicians and patients drives demand. Integration with AI-assisted diagnostic software is increasing.

- By End-Users

On the basis of end-users, the market is segmented into clinics, hospitals, surgical centers, and others. The hospitals segment dominated the largest market revenue share of 63.1% in 2024, driven by high patient inflow, availability of surgical facilities, and comprehensive treatment protocols. Hospitals provide integrated care, including diagnostics, pharmaceuticals, and surgical interventions. Adoption is supported by inpatient admissions and emergency care protocols. Advanced equipment and trained staff enhance treatment efficiency. Hospital networks ensure reliable supply of medications and consumables. Repeat admissions for recurrent or complicated cases strengthen market share. Government and private hospitals both contribute significantly. Insurance coverage increases affordability. Clinical guidelines promote hospital-based treatment. Hospitals also drive research and adoption of minimally invasive procedures.

The surgical centers segment is expected to witness the fastest CAGR of 19.8% from 2025 to 2032, fueled by increasing preference for minimally invasive laparoscopic surgeries in outpatient or day-care setups. Expansion of private surgical facilities supports adoption. Patient demand for shorter recovery times and lower hospital stays drives growth. Surgeons adopt advanced techniques, increasing procedural volume. Awareness campaigns highlight benefits of early surgical intervention. Private hospitals and specialty centers contribute to growth. Emerging markets see higher adoption with improved infrastructure. Insurance and reimbursement policies favor outpatient surgery.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into hospital pharmacy, retail pharmacy, and online pharmacy. The hospital pharmacy segment dominated the largest market revenue share of 48.5% in 2024, as most treatments and antibiotics are dispensed directly in hospitals. Hospitals ensure treatment adherence and proper dosage. Integrated supply chains enhance reliability. Inpatient and outpatient services drive volume. Government and private hospitals ensure steady procurement. Patient trust and convenience reinforce usage. Clinical protocols guide hospital pharmacy dispensing. Revenue is higher due to bulk institutional purchase.

The online pharmacy segment is expected to witness the fastest CAGR of 22.1% from 2025 to 2032, fueled by growing e-pharmacy platforms, home delivery, and telehealth adoption. Convenience and accessibility increase demand. Awareness of medication availability online accelerates growth. Digital payment options support adoption. Emerging markets show higher penetration with rising internet access. Online platforms offer both prescription and OTC medications. Patient preference for contactless delivery boosts the segment. The segment also benefits from targeted marketing, subscription services, and loyalty programs that encourage repeat purchases and long-term customer retention.

Acute Cholecystitis Market Regional Analysis

- North America dominated the acute cholecystitis market with the largest revenue share of 39.5% in 2024, driven by advanced healthcare infrastructure, high disposable incomes, and strong adoption of minimally invasive treatment options

- The market remains the largest contributor due to high healthcare spending, early access to innovative therapies, and a well-established network of specialized hospitals and surgical centers.

- The region’s strong clinical research environment, widespread use of advanced diagnostic technologies, and growing patient preference for laparoscopic and non-invasive procedures further support market growth. Moreover, early adoption of novel pharmacological therapies for managing acute cholecystitis complications is enhancing treatment outcomes and patient satisfaction

U.S. Acute Cholecystitis Market Insight

The U.S. acute cholecystitis market captured the largest revenue share in 2024 within North America, fueled by a well-developed healthcare ecosystem, high per capita healthcare expenditure, and the presence of leading hospitals specializing in gastrointestinal and hepatobiliary disorders. The country’s early adoption of minimally invasive procedures, coupled with advanced post-operative care protocols, is significantly contributing to market expansion. Increasing awareness among patients about early diagnosis and timely treatment is further driving the uptake of Acute Cholecystitis therapies.

Europe Acute Cholecystitis Market Insight

The Europe acute cholecystitis market is projected to expand at a substantial CAGR during the forecast period, primarily driven by an increasing focus on advanced treatment options, high healthcare standards, and growing patient awareness about gallbladder disorders. The region is witnessing robust demand for minimally invasive surgical interventions and optimized pharmacological management, supported by strong healthcare infrastructure and government initiatives promoting early diagnosis.

U.K. Acute Cholecystitis Market Insight

The U.K. acute cholecystitis market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by increasing awareness about gallbladder disorders, rising incidence of comorbidities such as obesity and diabetes, and a strong focus on early intervention. Adoption of laparoscopic surgeries and standardized clinical care pathways is contributing to better treatment outcomes, further stimulating market growth.

Germany Acute Cholecystitis Market Insight

The Germany acute cholecystitis market is expected to expand at a considerable CAGR during the forecast period, fueled by advanced healthcare infrastructure, emphasis on minimally invasive treatment techniques, and widespread availability of specialized gastrointestinal centers. The country’s focus on patient safety, clinical research, and healthcare innovation is supporting the adoption of advanced diagnostic and therapeutic solutions for Acute Cholecystitis.

Asia-Pacific Acute Cholecystitis Market Insight

The Asia-Pacific acute cholecystitis market is poised to grow at the fastest CAGR during the forecast period of 2025 to 2032, driven by increasing urbanization, rising healthcare expenditure, growing geriatric population, and expanding awareness about gallbladder disorders in countries such as China, India, and Japan. The region’s adoption of advanced diagnostic techniques, minimally invasive procedures, and enhanced healthcare infrastructure is significantly contributing to market growth.

Japan Acute Cholecystitis Market Insight

The Japan acute cholecystitis market is gaining momentum due to a rapidly aging population, high incidence of gallbladder-related disorders, and increasing adoption of minimally invasive surgeries. Rising awareness of early diagnosis, coupled with advanced healthcare infrastructure and technological integration in hospitals, is driving market growth.

China Acute Cholecystitis Market Insight

The China acute cholecystitis market accounted for the largest revenue share in Asia-Pacific in 2024, attributed to expanding healthcare infrastructure, rising prevalence of gallbladder disorders, increasing geriatric population, and growing patient access to advanced treatment options. The government’s focus on improving healthcare delivery and the widespread availability of minimally invasive procedures are key factors propelling market expansion in China.

Acute Cholecystitis Market Share

The Acute Cholecystitis industry is primarily led by well-established companies, including:

- Boston Scientific Corporation (U.S.)

- Fresenius Kabi AG (Germany)

- Pfizer Inc. (U.S.)

- Teva Pharmaceutical Industries Ltd. (Israel)

- Glenmark Pharmaceuticals Limited (India)

- Merck & Co., Inc. (U.S.)

- AbbVie Inc. (U.S.)

- Dornier MedTech GmbH (Germany)

- Johnson & Johnson Services, Inc. (U.S.)

- B. Braun SE (Germany)

- Sagent Pharmaceuticals, Inc. (U.S.)

- Takeda Pharmaceutical Company Ltd. (Japan)

Latest Developments in Global Acute Cholecystitis Market

- In September 2022, an international Delphi consensus was published by three professional surgical societies addressing the management of percutaneous cholecystostomy in acute cholecystitis. The consensus clarified that in high‑risk surgical patients, gallbladder drainage via percutaneous cholecystostomy (PC) can be undertaken within 24–48 hours and that following PC, laparoscopic cholecystectomy remains the preferred definitive treatment

- In September 2024, a practice bulletin titled “Conversations in Acute Cholecystitis Management” was released, examining evolving best practices. The bulletin emphasized that early laparoscopic cholecystectomy (within 2 days of diagnosis) is increasingly regarded as optimal, highlighting the timing of intervention, use of robotic assistance, and the shift toward outpatient surgical centers

- In April 2024, the Infectious Diseases Society of America (IDSA) published an updated clinical practice guideline for suspected acute cholecystitis in non‑pregnant adults, recommending that if initial ultrasound is inconclusive and clinical suspicion remains high, further imaging using CT or MRI/MRCP should be performed rather than delaying diagnosis

- In May 2025, a study in the International Journal of Surgery detailed management strategies for high‑surgical‑risk patients, proposing criteria for when to use percutaneous cholecystostomy as a bridge therapy and when to proceed with delayed laparoscopic cholecystectomy

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.