Global Acute Lymphocytic Lymphoblastic Leukemia All Diagnostics Market

Market Size in USD Billion

USD

1.35 Billion

USD

2.38 Billion

2024

2032

USD

1.35 Billion

USD

2.38 Billion

2024

2032

| 2025 - 2032 | |

| USD 1.35 Billion | |

| USD 2.38 Billion | |

| % | |

|

Acute Lymphocytic/Lymphoblastic Leukemia (ALL) Diagnostics Market Size

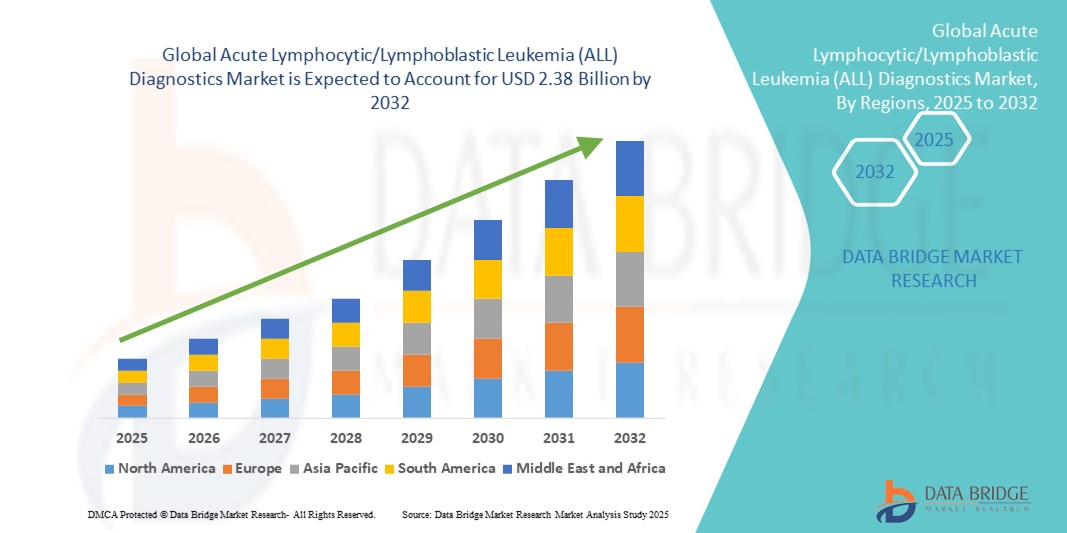

- The global acute lymphocytic/lymphoblastic leukemia (ALL) diagnostics market size was valued at USD 1.35 billion in 2024 and is expected to reach USD 2.38 billion by 2032, at a CAGR of 7.40% during the forecast period

- The market growth is largely fueled by the increasing prevalence of Acute Lymphocytic/Lymphoblastic Leukemia (ALL) globally, coupled with rising awareness about early diagnosis and the benefits of timely treatment

- Technological advancements in diagnostic methods, including flow cytometry, molecular testing, and immunophenotyping, are improving the accuracy, speed, and reliability of ALL detection, thereby supporting market expansion

Acute Lymphocytic/Lymphoblastic Leukemia (ALL) Diagnostics Market Analysis

- The acute lymphocytic/lymphoblastic leukemia (ALL) diagnostics market is witnessing significant growth due to rising prevalence of leukemia, increasing awareness about early diagnosis, and the growing adoption of advanced diagnostic technologies in both hospital and laboratory settings.

- Enhanced precision, faster turnaround times, and integration with personalized treatment approaches are driving demand for these solutions globally

- North America dominated the acute lymphocytic/lymphoblastic leukemia (ALL) diagnostics market with the largest revenue share of 42.10% in 2024. This growth is supported by advanced healthcare infrastructure, high healthcare expenditure, and strong adoption of both point-of-care and clinical laboratory analyzers. The U.S. accounted for a major portion of this share, fueled by rapid implementation of innovative diagnostic platforms, ongoing research initiatives, and increasing focus on early detection and personalized treatment plans

- Asia-Pacific is projected to be the fastest-growing region in the acute lymphocytic/lymphoblastic leukemia (ALL) diagnostics market during the forecast period, driven by rising healthcare investment, expanding hospital networks, rapid urbanization, and growing awareness about leukemia diagnostics in countries such as China, Japan, and India

- The B-cell lymphoblastic leukemia/lymphoma segment dominated the acute lymphocytic/lymphoblastic leukemia (ALL) diagnostics market with a market share of 68.3% in 2024. This leadership is attributed to the higher incidence of B-cell leukemia, prompting increased research focus, development of targeted diagnostic tools, and the adoption of advanced molecular and flow cytometry-based testing methods specific to this subtype

Report Scope and Acute Lymphocytic/Lymphoblastic Leukemia (ALL) Diagnostics Market Segmentation

|

Attributes |

Acute Lymphocytic/Lymphoblastic Leukemia (ALL) Diagnostics Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Acute Lymphocytic/Lymphoblastic Leukemia (ALL) Diagnostics Market Trends

Advancements Driving Accuracy and Efficiency in ALL Diagnostics

- A significant and accelerating trend in the global acute lymphocytic/lymphoblastic leukemia (ALL) diagnostics market is the integration of advanced technologies such as artificial intelligence (AI), machine learning, and automated data analysis tools. These innovations are enhancing the speed, accuracy, and reliability of leukemia detection, enabling earlier diagnosis and more effective treatment planning

- For instance, AI-powered diagnostic platforms can analyze complex patient data from flow cytometry, immunophenotyping, and molecular assays to identify leukemia subtypes with high precision, supporting clinicians in making informed decisions quickly

- Automation and advanced analytics in laboratory workflows are streamlining processes, reducing human error, and improving overall efficiency. These systems can also flag abnormal patterns and generate predictive insights for disease progression, enabling personalized treatment strategies

- The adoption of integrated diagnostic solutions that combine molecular testing, genetic profiling, and high-throughput analysis is reshaping standards of care in leukemia diagnostics. Hospitals, clinical laboratories, and research institutes are increasingly relying on such solutions to enhance patient outcomes and optimize treatment protocols

- Growing demand for rapid, reliable, and cost-effective ALL diagnostic solutions, particularly in emerging markets with rising leukemia incidence, is further propelling market expansion. Technological innovation, combined with increased awareness of early detection and precision medicine, is fundamentally driving growth in the ALL diagnostics industry

Acute Lymphocytic/Lymphoblastic Leukemia (ALL) Diagnostics Market Dynamics

Driver

Growing Need Due to Rising Leukemia Incidence and Early Diagnosis Awareness

- The increasing prevalence of acute lymphocytic/lymphoblastic leukemia (ALL) across both developed and developing regions, coupled with heightened awareness about the critical importance of early diagnosis and timely treatment interventions, is a major driver for the growing demand for ALL diagnostic solutions

- For instance, in 2024, leading diagnostic companies launched advanced flow cytometry and molecular testing platforms capable of rapidly detecting leukemia subtypes with high accuracy. Such strategic product innovations and technological advancements are expected to significantly propel growth in the ALL diagnostics market during the forecast period

- As healthcare providers focus on improving patient safety and therapeutic outcomes, the adoption of rapid, highly precise, and reliable diagnostic technologies has become essential. ALL diagnostics now enable clinicians to identify disease at earlier stages, facilitate risk stratification, and guide personalized treatment plans more effectively

- Furthermore, the growing emphasis on precision medicine, where treatment decisions are informed by detailed genetic, molecular, and immunophenotypic profiling, is driving increased utilization of comprehensive diagnostic solutions. These technologies not only improve clinical decision-making but also enhance monitoring of treatment response and disease progression

- The convenience of automated testing platforms, faster turnaround times, integration with hospital information systems, and broader accessibility of ALL diagnostic solutions across hospitals, clinical laboratories, and research institutes are key factors supporting market expansion. The trend toward enhancing operational efficiency and patient-centric care further contributes to the sustained growth of the market

Restraint/Challenge

Challenges Related to High Costs and Technical Expertise Requirements

- The relatively high upfront cost of advanced acute lymphocytic/lymphoblastic leukemia (ALL) diagnostic systems, when compared to conventional hematology testing methods, continues to present a substantial barrier to adoption. This is especially pronounced in smaller hospitals, clinics, and healthcare facilities located in emerging markets, where budget constraints and limited capital expenditure often restrict access to cutting-edge diagnostic technologies

- Many ALL-diagnostic platforms require specialized technical training and expertise to operate with precision and to accurately interpret complex test results. The limited availability of trained laboratory personnel and clinical experts can therefore significantly hinder widespread adoption, particularly in regions with underdeveloped healthcare infrastructure

- Ensuring consistent device calibration, achieving reproducible and high-quality test outcomes, and effectively managing complex data outputs over extended periods can pose operational and logistical challenges. These challenges are especially acute in high-volume testing environments or resource-limited settings, where staff workload and equipment maintenance demands are high

- Overcoming these barriers will require the development of cost-effective, intuitive, and user-friendly diagnostic solutions that minimize the need for specialized training. Additionally, the implementation of comprehensive clinician training programs, coupled with instruments featuring enhanced reliability, automated calibration, and streamlined workflow integration, will be essential to support the sustained growth and broader adoption of ALL diagnostics across diverse healthcare settings globally

Acute Lymphocytic/Lymphoblastic Leukemia (ALL) Diagnostics Market Scope

The market is segmented on the basis of product type, test type, cancer type, age group, gender, end user, and distribution channel.

- By Product Type

On the basis of product type, the global acute lymphocytic/lymphoblastic leukemia (ALL) diagnostics market is segmented into instruments and consumables & accessories. In 2024, the instruments segment dominated the market with a substantial revenue share of 62.4%. This dominance is primarily driven by the widespread use of sophisticated diagnostic instruments, including flow cytometers, PCR machines, and next-generation sequencing platforms, which are essential for the accurate and early detection of Acute Lymphocytic/Lymphoblastic Leukemia (ALL). These advanced instruments play a crucial role in monitoring disease progression and enabling personalized treatment approaches.

Conversely, the consumables & accessories segment is projected to register the fastest CAGR of 9.2% between 2025 and 2032, fueled by rising demand for critical reagents, diagnostic kits, and disposable laboratory supplies that support high-throughput testing and ensure precise diagnostic results.

- By Test Type

On the basis of test type, the global acute lymphocytic/lymphoblastic leukemia (ALL) diagnostics market is segmented into imaging test, biopsy, blood test, and others. The Blood Test segment led the market in 2024 with a revenue share of 45.6%, largely due to its minimally invasive procedure, cost-effectiveness, and broad applicability across screening, initial diagnosis, and ongoing monitoring of disease progression in ALL patients.

Meanwhile, the Biopsy segment is expected to achieve the fastest growth with a CAGR of 10.1% over the forecast period, reflecting its indispensable role in confirming ALL diagnoses, providing detailed pathological insights, and facilitating the development of tailored treatment plans for patients.

- By Cancer Type

On the basis of cancer type, the global acute lymphocytic/lymphoblastic leukemia (ALL) diagnostics market is segmented into B-cell lymphoblastic leukemia/lymphoma and T-cell lymphoblastic leukemia. In 2024, the B-cell lymphoblastic leukemia/lymphoma segment held a dominated position with a substantial market share of 68.3%. This leadership is primarily attributed to its higher incidence rate across the region, which has prompted increased research focus and significant advancements in diagnostic technologies specifically targeting this subtype.

Meanwhile, the T-cell lymphoblastic leukemia segment, although less common, is anticipated to grow steadily at a CAGR of 7.4% between 2025 and 2032. This growth is supported by continuous improvements in immunophenotyping techniques and molecular diagnostics, enabling more accurate detection and tailored treatment approaches for this clinically important but relatively rarer leukemia subtype.

- By Age Group

On the basis of age group, the global acute lymphocytic/lymphoblastic leukemia (ALL) diagnostics market is segmented into Below 21, 21-29, 30-65, and 65 and above. The Below 21 age group accounted for the largest revenue share of 38.7% in 2024, reflecting the well-documented higher prevalence of Acute Lymphoblastic Leukemia (ALL) among children and adolescents within the region. This high prevalence drives demand for pediatric-specific diagnostic solutions and early intervention therapies.

Meanwhile, the 30-65 age group is projected to show robust market growth with a CAGR of 8.3% over the forecast period. This growth is largely driven by rising awareness of ALL symptoms in adults, improved diagnostic capabilities that facilitate earlier detection, and a growing focus on adult patient populations that were historically underdiagnosed.

- By Gender

On the basis of gender, the global acute lymphocytic/lymphoblastic leukemia (ALL) diagnostics market is segmented into male and female. The Male segment dominated the market in 2024, holding a revenue share of 53.2%. This predominance aligns with epidemiological data indicating a marginally higher incidence of ALL in males across the region. Factors such as genetic predisposition and environmental influences are being studied to understand this gender disparity better.

Conversely, the Female segment is expected to experience steady growth with a CAGR of 7.9% throughout the forecast period. This trend is reflective of improvements in healthcare access, increased health awareness among women, and advancements in diagnostic technologies that facilitate earlier and more accurate detection of ALL in female patients.

- By End User

On the basis of end user, the global acute lymphocytic/lymphoblastic leukemia (ALL) diagnostics market is segmented into hospitals, associated labs, independent diagnostic laboratories, diagnostic imaging centers, cancer research institutes, and others. In 2024, Hospitals dominated the market with a significant share of 57.6%, largely due to their well-established and advanced diagnostic infrastructure, ability to provide integrated patient care, and capacity to manage complex and severe leukemia cases efficiently.

Meanwhile, independent diagnostic laboratories are poised to experience the fastest growth, registering CAGRs of 9.5% and 9.2%, respectively. This rapid expansion is driven by the increasing trend of outsourcing diagnostic services by healthcare providers and a surge in investments directed towards research and clinical trials focused on leukemia diagnostics, enhancing capabilities and service reach in these specialized settings.

- By Distribution Channel

On the basis of distribution channel, the global acute lymphocytic/lymphoblastic leukemia (ALL) diagnostics market is segmented into direct tender and retail sales. Direct tender held the largest market share of 54.3% in 2024, supported primarily by bulk procurement activities conducted by government healthcare agencies and large hospital networks aiming to fulfill the escalating demand for leukemia diagnostic solutions.

On the other hand, the retail sales segment is anticipated to witness the fastest CAGR of 10.3% during the forecast period from 2025 to 2032. This rapid growth is propelled by the expansion of online sales platforms, an increasing footprint in smaller clinics, and improved accessibility of diagnostic products and services in semi-urban and rural areas, enabling wider reach and convenience for end users.

Acute Lymphocytic/Lymphoblastic Leukemia (ALL) Diagnostics Market Regional Analysis

- North America dominated the acute lymphocytic/lymphoblastic leukemia (ALL) diagnostics market with the largest revenue share of 42.10% in 2024, driven by increasing incidence of leukemia, rising awareness about early detection, and the availability of advanced diagnostic technologies

- The region benefits from well-established healthcare infrastructure, high healthcare spending, and widespread adoption of both point-of-care and clinical laboratory analyzers

- In addition, strong research initiatives, funding for leukemia diagnostics, and the focus on precision medicine further support market growth

U.S. Acute Lymphocytic/Lymphoblastic Leukemia (ALL) Diagnostics Market Insight

The U.S. acute lymphocytic/lymphoblastic leukemia (ALL) diagnostics market captured the largest revenue share of 46% in 2024 within North America, fueled by the rapid adoption of both point-of-care and clinical laboratory analyzers. Technological advancements in detection methods, faster turnaround times for results, and growing emphasis on personalized anticoagulation and treatment monitoring are key factors contributing to market expansion. Moreover, increasing awareness among healthcare professionals about real-time leukemia monitoring and patient safety is significantly supporting market growth.

Europe Acute Lymphocytic/Lymphoblastic Leukemia (ALL) Diagnostics Market Insight

The Europe acute lymphocytic/lymphoblastic leukemia (ALL) diagnostics market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by increasing healthcare expenditure, the presence of advanced diagnostic laboratories, and initiatives supporting early cancer detection. Rising incidence of leukemia and growing adoption of automated and high-throughput diagnostic platforms in hospitals and clinical laboratories are fostering market growth across major European countries.

U.K. Acute Lymphocytic/Lymphoblastic Leukemia (ALL) Diagnostics Market Insight

The U.K. acute lymphocytic/lymphoblastic leukemia (ALL) diagnostics market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by increasing demand for rapid and accurate leukemia diagnostics, well-established healthcare systems, and government support for cancer research programs. Enhanced clinical awareness and growing investments in diagnostic infrastructure are expected to further propel market expansion.

Germany Acute Lymphocytic/Lymphoblastic Leukemia (ALL) Diagnostics Market Insight

The Germany acute lymphocytic/lymphoblastic leukemia (ALL) diagnostics market is expected to expand at a considerable CAGR during the forecast period, fueled by technological advancements, growing emphasis on early-stage cancer detection, and the presence of highly skilled medical professionals. The adoption of automated and integrated diagnostic solutions in hospitals and research institutes is further driving market growth.

Asia-Pacific Acute Lymphocytic/Lymphoblastic Leukemia (ALL) Diagnostics Market Insight

The Asia-Pacific acute lymphocytic/lymphoblastic leukemia (ALL) diagnostics market is poised to grow at the fastest CAGR of 24% during the forecast period of 2025 to 2032, driven by increasing healthcare expenditure, expansion of hospital networks, rapid urbanization, and rising awareness about early leukemia detection in countries such as China, Japan, and India. Technological advancements, government initiatives promoting healthcare access, and the increasing adoption of advanced diagnostic platforms are further fueling market growth.

Japan Acute Lymphocytic/Lymphoblastic Leukemia (ALL) Diagnostics Market Insight

The Japan acute lymphocytic/lymphoblastic leukemia (ALL) diagnostics market is gaining momentum due to the country’s high healthcare standards, strong focus on research and development, and the increasing demand for precision medicine. The adoption of automated diagnostic platforms, molecular testing, and rapid point-of-care solutions in hospitals and research institutes is driving market growth.

China Acute Lymphocytic/Lymphoblastic Leukemia (ALL) Diagnostics Market Insight

The China acute lymphocytic/lymphoblastic leukemia (ALL) diagnostics market accounted for the largest revenue share in Asia-Pacific in 2024, attributed to the country’s expanding healthcare infrastructure, rising healthcare expenditure, rapid urbanization, and increased adoption of advanced diagnostic technologies. Growing government initiatives for cancer detection and strong domestic manufacturing of diagnostic systems are key factors propelling market growth.

Acute Lymphocytic/Lymphoblastic Leukemia (ALL) Diagnostics Market Share

The acute lymphocytic/lymphoblastic leukemia (ALL) diagnostics industry is primarily led by well-established companies, including:

- F. Hoffmann-La Roche Ltd. (Switzerland)

- Thermo Fisher Scientific, Inc. (U.S.)

- QIAGEN (Netherlands)

- Abbott (U.S.)

- Merck KGaA (Germany)

- Siemens Healthineers AG (U.S.)

- Hologic, Inc. (U.S.)

- Agilent Technologies, Inc. (U.S.)

- DiaSorin S.p.A. (Italy)

- Illumina, Inc. (U.S.)

- Myriad Genetics, Inc. (U.S.)

- BIOMÉRIEUX (France)

- Quest Diagnostics Incorporated (U.S.)

- Bio-Rad Laboratories, Inc. (U.S.)

- Koninklijke Philips N.V. (Netherlands)

- BD (U.S.)

- Exact Sciences Corporation (U.S.)

- Time Medical Holding (China)

- PlexBio (China)

- MinFound Medical Systems Co., Ltd (China)

- Medonica Co. LTD (Israel)

Latest Developments in Global Acute Lymphocytic/Lymphoblastic Leukemia (ALL) Diagnostics Market

- In December 2024, Illumina was named a sequencing partner in major South Korean national genomics initiatives (Macrogen Consortium / National Bio Big Data project) — an expansion of large-scale genomics infrastructure in APAC that will accelerate oncology genomics, variant interpretation and assay development useful for leukemia diagnostics (including ALL research and NGS panel development)

- In August 2022, F. Hoffmann-La Roche launched the Digital LightCycler System, its first commercial digital PCR (dPCR) platform — a high-sensitivity system intended for absolute quantification of DNA/RNA targets and well-suited for minimal residual disease (MRD) and ultra-rare variant detection workflows relevant to ALL diagnostics

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.