Global Acute Ocular Pain Market

Market Size in USD Billion

USD

435.83 Billion

USD

879.96 Billion

2024

2032

USD

435.83 Billion

USD

879.96 Billion

2024

2032

| 2025 - 2032 | |

| USD 435.83 Billion | |

| USD 879.96 Billion | |

| % | |

|

Acute Ocular Pain Market Size

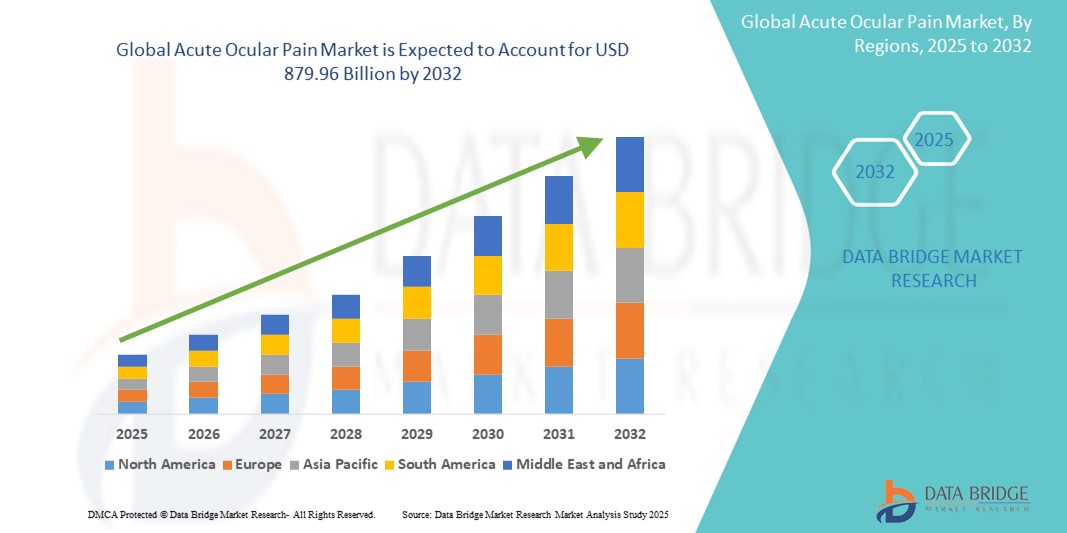

- The global acute ocular pain market size was valued at USD 435.83 billion in 2024 and is expected to reach USD 879.96 billion by 2032, at a CAGR of 9.18% during the forecast period

- The market growth is largely fueled by the rising prevalence of ocular conditions such as uveitis, conjunctivitis, corneal abrasions, and dry eye syndrome, which are major contributors to acute ocular pain across diverse populations

- Furthermore, increasing awareness regarding early diagnosis and the availability of advanced treatment options—such as topical NSAIDs, corticosteroids, and combination therapies—is driving the demand for effective pain management in ophthalmology. These converging factors are accelerating the uptake of acute ocular pain treatments, thereby significantly boosting the industry’s growth

Acute Ocular Pain Market Analysis

- Acute ocular pain, stemming from conditions such as corneal abrasions, infections, and inflammatory disorders, is a growing concern globally, prompting heightened demand for effective analgesic therapies and rapid diagnosis

- The rising prevalence of eye strain due to increased screen time, along with expanding aging populations, significantly contributes to the growth of the Acute Ocular Pain market across both developed and developing nations

- North America dominated the acute ocular pain market with the largest revenue share of 38.7% in 2024, supported by strong healthcare infrastructure, higher awareness, and widespread access to prescription ophthalmic medications and diagnostics

- Asia-Pacific is expected to be the fastest growing region in the acute ocular pain market during the forecast period, with a projected CAGR of 7.9%, driven by rapid urbanization, increasing eye disease burden, and improved access to eye care in emerging economies such as India and China

- The topical NSAIDs segment dominates the acute ocular pain market with a market share of 45.6%, attributed to their efficacy in pain reduction, widespread usage, and strong physician preference in treating inflammation-related eye pain

Report Scope and Acute Ocular Pain Market Segmentation

|

Attributes |

Acute Ocular Pain Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

• Novartis AG (Switzerland) |

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Acute Ocular Pain Market Trends

“Shifting Focus Toward Personalized and Sustained-Release Therapies”

- A significant and accelerating trend in the global acute ocular pain market is the growing focus on personalized and sustained-release ocular therapies tailored to individual patient profiles and treatment timelines. This trend is driven by the limitations of traditional eye drops, including poor bioavailability and frequent dosing requirements

- For instance, companies are investing in the development of drug-eluting contact lenses and intracanalicular inserts that can release medication over an extended period, providing consistent therapeutic effects while improving patient adherence. These innovations also help minimize side effects by targeting drug delivery more precisely to the affected area

- The move toward patient-centric treatment is further supported by advancements in diagnostic tools that allow ophthalmologists to better assess pain severity and tailor treatment plans accordingly. This level of precision is critical in acute pain scenarios where timely relief is essential

- Moreover, sustained-release platforms are being tested not just for pain relief, but also for co-management of underlying inflammatory or post-surgical conditions, offering multifunctional treatment avenues

- This ongoing shift is reshaping both clinical practice and market offerings, prompting pharmaceutical companies and medtech innovators to prioritize long-acting formulations and combination therapies in their development pipelines

- The demand for more effective, low-maintenance treatments is particularly high among aging populations and post-operative patients, making personalized, sustained-release solutions a pivotal growth engine in the acute ocular pain landscape

Acute Ocular Pain Market Dynamics

Driver

“Rising Prevalence of Ocular Conditions and Increased Surgical Interventions”

- The increasing incidence of eye-related disorders, including corneal abrasions, infections, and post-surgical complications, is a key driver fueling the demand for effective acute ocular pain management solutions

- For instance, the growing number of cataract surgeries and laser-assisted procedures globally is contributing to a surge in post-operative ocular pain cases, necessitating the use of topical anesthetics, NSAIDs, and corticosteroids

- In addition, rising awareness regarding eye health and the availability of specialized ophthalmic care are accelerating early diagnosis and timely treatment of acute eye pain, further supporting market growth

- Pharmaceutical innovations and the launch of new formulations with improved ocular penetration and minimal side effects are enhancing the efficacy of available treatments, driving their adoption in both hospital and homecare settings

- Moreover, the increasing geriatric population, which is more susceptible to ocular diseases, is expanding the patient pool, thereby contributing to the growing demand for acute ocular pain therapies

Restraint/Challenge

“Limited Availability of Targeted Therapies and Side Effects of Existing Treatments”

- Despite technological advancements, the acute ocular pain market faces challenges due to the limited availability of highly targeted and long-lasting therapeutic options. Many currently available medications provide only short-term relief and may require frequent administration, leading to issues with patient compliance

- For Instance, overuse of topical anesthetics can lead to corneal toxicity, while prolonged use of corticosteroids may result in elevated intraocular pressure or cataract formation, discouraging long-term use

- Furthermore, in some low- and middle-income regions, access to advanced ophthalmic treatments remains restricted due to limited healthcare infrastructure and affordability issues, hindering market penetration

- The lack of definitive treatment guidelines and varying physician preferences also create inconsistencies in the management of acute ocular pain

- Addressing these challenges will require increased investment in R&D for developing sustained-release formulations and safer alternatives, along with initiatives to expand healthcare access and education in underserved regions

Acute Ocular Pain Market Scope

The market is segmented on the basis of type, medical condition, route of administration, end-user, and distribution channel.

- By Type

On the basis of type, the acute ocular pain market is segmented into topical NSAIDs, corticosteroids, analgesics, antibiotics, and others. The topical NSAIDs segment held the largest market revenue share of 45.6% in 2024, driven by their widespread prescription for reducing inflammation and pain post-surgery or due to various ocular conditions. Healthcare professionals often prioritize topical NSAIDs for their localized action and effectiveness in managing acute ocular discomfort. The market also sees strong demand for topical NSAID types due to their favorable safety profile and broad applicability across different etiologies of ocular pain.

The analgesics segment is anticipated to witness the fastest growth rate from 2025 to 2032, fueled by increasing demand for rapid pain relief and the development of new, more targeted analgesic formulations. Analgesics offer immediate symptomatic relief, making them suitable for patients experiencing significant discomfort, and their integration into multi-modal pain management strategies provides healthcare providers with versatile solutions. The ease of administration and quick action of oral and topical analgesics also contribute to their growing popularity.

- By Medical Condition

On the basis of medical condition, the acute ocular pain market is segmented into glaucoma, conjunctivitis, uveitis, corneal abrasions, and others. The conjunctivitis segment held the largest market revenue share of 33.6% in 2024, driven by the widespread prevalence of various forms of conjunctivitis (viral, bacterial, allergic), which commonly present with acute ocular pain and discomfort. Conjunctivitis cases often require immediate symptomatic relief and treatment, making it a frequent cause for patients seeking acute ocular pain solutions.

The corneal abrasions segment is expected to witness the fastest CAGR from 2025 to 2032, driven by the increasing incidence of eye injuries (including sports-related and occupational injuries) and the immediate need for effective pain management to facilitate healing. Advances in treatment protocols for corneal injuries and heightened awareness regarding prompt care for ocular trauma are also contributing to its growth.

- By Route of Administration

On the basis of route of administration, the acute ocular pain market is segmented into topical, oral, parenteral, and others. The topical segment held the largest market revenue share of 65.7% in 2024, driven by the direct and localized delivery of medication to the eye, minimizing systemic side effects. Topical administration offers convenience for patients and allows for precise dosing at the site of pain, making it a highly preferred and user-friendly option for various ocular conditions.

The parenteral segment is expected to witness the fastest CAGR from 2025 to 2032, favored for its use in severe cases, post-surgical pain management, or when systemic administration is required for conditions such as severe uveitis. This route provides rapid onset of action and controlled drug release, offering a reliable and effective solution for intense or persistent acute ocular pain, particularly in hospital or specialty clinic settings.

- By End User

On the basis of end-user, the acute ocular pain market is segmented into hospitals, homecare, specialty clinics, and others. The specialty clinics segment held the largest market revenue share in 2024, driven by the increasing number of dedicated ophthalmology clinics and eye care centers that provide specialized diagnosis and treatment for ocular conditions, including acute pain. These clinics offer expert consultations, advanced diagnostic tools, and in-office procedures for comprehensive management.

The homecare segment is expected to witness the fastest CAGR from 2025 to 2032, driven by the growing preference for managing chronic or post-treatment ocular pain at home, enabled by telemedicine consultations and convenient access to prescribed medications. The focus on patient comfort and the increasing availability of user-friendly topical applications and oral analgesics are encouraging the adoption of home-based pain management.

- By Distribution Channel

On the basis of distribution channel, the acute ocular pain market is segmented into hospital pharmacy, online pharmacy, and retail pharmacy. The retail pharmacy segment accounted for the largest market revenue share in 2024, driven by its widespread accessibility, convenience for patients to purchase over-the-counter medications and fill prescriptions, and extensive geographical reach. Retail pharmacies serve as the primary point of access for a vast majority of patients seeking immediate relief from acute ocular pain.

The online pharmacy segment is expected to witness the fastest CAGR from 2025 to 2032, driven by the increasing digitalization of healthcare, the convenience of home delivery, and competitive pricing. The growing preference for online shopping and the ease of comparing products and prices are accelerating the adoption of online pharmacies for purchasing acute ocular pain medications.

Acute Ocular Pain Market Regional Analysis

- North America is anticipated to dominate the acute ocular pain market with the largest revenue share, estimated to be around 38.7% in 2024. This is driven by a well-established healthcare infrastructure, high prevalence of eye disorders (including age-related conditions such as glaucoma and cataracts), and significant investment in research and development in ophthalmology

- Consumers and healthcare providers in the region highly value the availability of advanced diagnostic tools, innovative drug formulations (such as sustained-release topical therapies), and favorable reimbursement policies for ocular pain management

- This widespread adoption is further supported by a technologically inclined population, increasing awareness about ocular health, and a strong presence of major pharmaceutical companies, establishing North America as a leading market for both existing and emerging treatments for acute ocular pain

U.S. Acute Ocular Pain Market Insight

The U.S. acute ocular pain market captured the largest revenue share of 48.7% in 2024 within North America, fueled by a high prevalence of various ocular conditions leading to pain, sophisticated healthcare infrastructure, and significant research & development investments in ophthalmology. Consumers and healthcare providers are increasingly prioritizing effective and rapid pain management through advanced topical and systemic treatments. The growing preference for specialized ophthalmic care, combined with robust demand for novel drug formulations and efficient diagnostic tools, further propels the Acute Ocular Pain industry. Moreover, the increasing integration of targeted therapies and patient-centric care models is significantly contributing to the market's expansion.

Europe Acute Ocular Pain Market Insight

The Europe acute ocular pain market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by the rising geriatric population, increasing incidence of eye infections and injuries, and the escalating need for effective pain management solutions. The increase in healthcare expenditure, coupled with the demand for advanced ophthalmic drugs and procedures, is fostering the adoption of acute ocular pain treatments. European consumers are also drawn to the availability of innovative therapies and favorable reimbursement policies for ocular conditions. The region is experiencing significant growth across hospital, specialty clinic, and homecare settings, with a focus on both new drug approvals and optimized treatment protocols.

U.K. Acute Ocular Pain Market Insight

The U.K. acute ocular pain market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by the increasing burden of ocular diseases and a desire for heightened patient comfort and rapid pain relief. Additionally, concerns regarding ocular health and the impact of pain on daily life are encouraging both patients and healthcare providers to choose advanced treatment solutions. The UK’s commitment to ophthalmic research, alongside its robust healthcare system and increasing access to specialized eye care, is expected to continue to stimulate market growth.

Germany Acute Ocular Pain Market Insight

The Germany acute ocular pain market is expected to expand at a considerable CAGR during the forecast period, fueled by increasing awareness of ocular health conditions and the demand for technologically advanced, effective therapeutic solutions. Germany’s well-developed healthcare infrastructure, combined with its emphasis on precision medicine and patient-centric treatment, promotes the adoption of a wide range of acute ocular pain treatments, particularly in specialized ophthalmology centers. The integration of advanced diagnostics with personalized treatment plans is also becoming increasingly prevalent, with a strong preference for high-quality, evidence-based solutions aligning with local medical standards.

Asia-Pacific Acute Ocular Pain Market Insight

The Asia-Pacific acute ocular pain market is poised to grow at the fastest CAGR of 7.9% during the forecast period of 2025 to 2032, driven by increasing urbanization, rising disposable incomes, and technological advancements in healthcare in countries such as China, Japan, and India. The region's growing prevalence of ophthalmic disorders, supported by government initiatives promoting eye health and access to medical services, is driving the adoption of acute ocular pain treatments. Furthermore, as APAC emerges as a significant hub for pharmaceutical manufacturing and clinical research, the affordability and accessibility of novel ocular pain solutions are expanding to a wider patient base.

Japan Acute Ocular Pain Market Insight

The Japan acute ocular pain market is gaining momentum due to the country’s advanced healthcare system, rapidly aging population, and high demand for specialized ophthalmic care. The Japanese market places a significant emphasis on precise diagnosis and effective treatment for ocular pain, and the adoption of innovative drugs and therapies is driven by continuous medical innovation. The integration of advanced imaging and diagnostic techniques with treatment planning, alongside a strong focus on improving quality of life for patients, is fueling growth. Moreover, Japan's robust research and development activities are likely to spur demand for cutting-edge, secure treatment solutions in the coming years.

China Acute Ocular Pain Market Insight

The China acute ocular pain market accounted for the largest market revenue share in Asia Pacific in 2024, attributed to the country's vast population, increasing prevalence of eye conditions, rapid advancements in its domestic pharmaceutical industry, and significant government investment in healthcare infrastructure. China stands as one of the largest markets for ophthalmic drugs and treatments, and acute ocular pain solutions are becoming increasingly available across various healthcare settings. The push towards national health awareness campaigns and the availability of affordable and increasingly innovative treatment options, alongside strong domestic research and manufacturing capabilities, are key factors propelling the market in China.

Acute Ocular Pain Market Share

The acute ocular pain industry is primarily led by well-established companies, including:

- Novartis AG (Switzerland)

- Pfizer Inc. (U.S.)

- Sun Pharmaceutical Industries Ltd. (India)

- Bausch + Lomb (Canada)

- Alcon Inc. (Switzerland)

- Regeneron Pharmaceuticals, Inc. (U.S.)

- OCUGEN, INC. (U.S.)

- Santen Pharmaceutical Co., Ltd. (Japan)

- Ocular Therapeutix, Inc. (U.S.)

- EyePoint Pharmaceuticals, Inc. (U.S.)

- Johnson & Johnson Services, Inc. (U.S.)

- Dr. Reddy’s Laboratories Ltd. (India)

- Oculis (Switzerland)

Latest Developments in Global Acute Ocular Pain Market

- In January 2021, IACTA Pharmaceuticals, Inc. and Pharmaleads (including Pharmaleads Greater China) entered into an exclusive global licensing agreement for Dual Enkephalinase Inhibitors (DENKI), targeting both acute (IC800) and chronic (IC805) ocular pain. The therapy aims to be the world’s first topical, epithelial‑protective drug that harnesses endogenous enkephalin‑mediated analgesia, offering a non‑opioid alternative for treating acute and chronic ocular pain. Under the agreement, Pharmaleads may receive up to USD 100 million through upfront, development, regulatory, and commercial milestones

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.