Global Adhesive Arachnoiditis Treatment Market

Market Size in USD Million

USD

787.35 Million

USD

1,163.27 Million

2024

2032

USD

787.35 Million

USD

1,163.27 Million

2024

2032

| 2025 - 2032 | |

| USD 787.35 Million | |

| USD 1,163.27 Million | |

| % | |

|

Adhesive Arachnoiditis Treatment Market Size

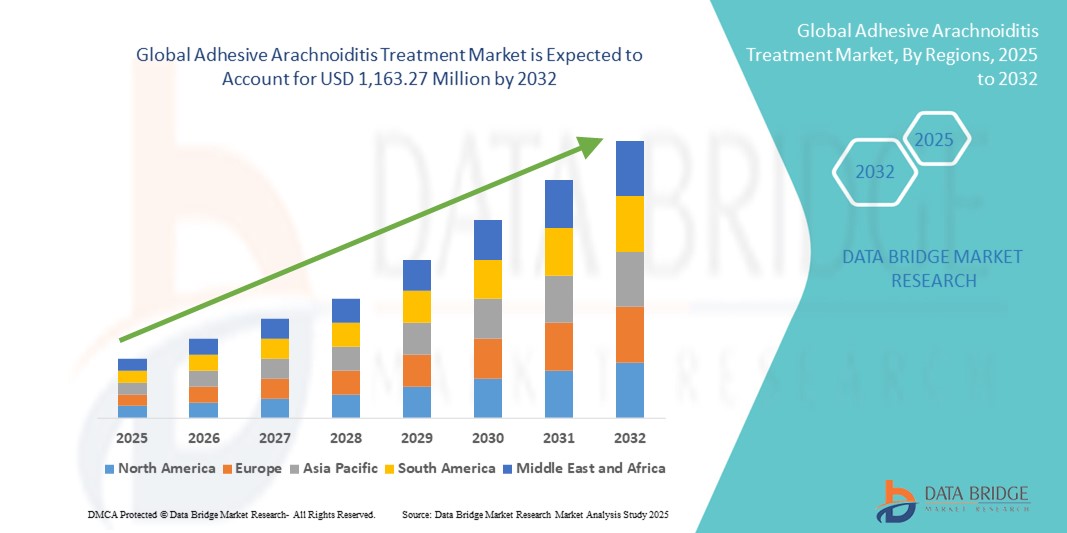

- The global adhesive arachnoiditis treatment market size was valued at USD 787.35 million in 2024 and is expected to reach USD 1,163.27 million by 2032, at a CAGR of 5.0% during the forecast period

- The market growth is largely fueled by the increasing prevalence of adhesive arachnoiditis, coupled with rising awareness about its diagnosis and available treatment options, driving higher demand for effective therapeutic solutions

- Furthermore, continuous advancements in pain management therapies, including the development of novel pharmacological approaches, regenerative medicine, and minimally invasive surgical techniques, are significantly improving patient outcomes

Adhesive Arachnoiditis Treatment Market Analysis

- Adhesive arachnoiditis treatment, encompassing pharmacological therapies, surgical interventions, and advanced pain management strategies, is increasingly recognized as a critical area of neurological healthcare due to its chronic and debilitating nature. Rising awareness among healthcare professionals, improved diagnostic capabilities, and growing patient advocacy are contributing to higher diagnosis rates and treatment adoption in both developed and emerging markets

- The escalating demand for effective adhesive arachnoiditis treatment is primarily fueled by advancements in neuroimaging, the development of targeted drug formulations, and increased research funding aimed at addressing chronic neuropathic pain associated with the condition

- North America dominated the adhesive arachnoiditis treatment market with the largest revenue share of 45% in 2024, driven by a strong presence of specialized neurology centres, high healthcare expenditure, favourable reimbursement policies, and robust clinical research activity. The U.S. leads the region, supported by early adoption of novel pain management techniques, a growing patient registry database, and collaborations between academic institutions and biopharmaceutical companies to develop more effective treatment protocols

- Asia-Pacific is expected to be the fastest-growing region in the adhesive arachnoiditis treatment market during the forecast period due to increasing healthcare infrastructure investment, expanding medical tourism, and rising awareness of rare neurological disorders among both patients and clinicians

- The oral segment dominated the adhesive arachnoiditis treatment market with a share of 57.8% in 2024, driven by the widespread use of NSAIDs, anti-convulsants, and muscle relaxants in pill or capsule form, which provide ease of administration and patient compliance

Report Scope and Adhesive Arachnoiditis Treatment Market Segmentation

|

Attributes |

Adhesive Arachnoiditis Treatment Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Adhesive Arachnoiditis Treatment Market Trends

Enhanced Convenience Through Advanced Therapeutic Approaches

- A significant and accelerating trend in the global adhesive arachnoiditis treatment market is the adoption of advanced therapeutic approaches, including targeted drug delivery systems, regenerative medicine techniques, and minimally invasive surgical interventions. These innovations are enhancing treatment precision, reducing recovery time, and improving patient quality of life

- For instance, ongoing clinical research on intrathecal drug pumps and biologic agents is demonstrating promising outcomes in reducing chronic pain and inflammation associated with adhesive arachnoiditis, while minimizing systemic side effects

- Advances in neuroimaging and diagnostic tools are enabling earlier detection and more tailored treatment planning. For instance, high-resolution MRI protocols can help identify subtle nerve root clumping, allowing for earlier intervention before symptoms progress severely

- Multimodal treatment approaches combining pharmacological therapy, physical rehabilitation, and neuromodulation techniques are gaining traction. Some healthcare centers are integrating spinal cord stimulation (SCS) with targeted pain management regimens to improve functional outcomes in refractory cases

- The integration of telemedicine into follow-up care allows patients to receive regular monitoring and adjustments to their treatment plans without the need for frequent hospital visits, improving accessibility for those in remote areas

- This shift toward more personalized, technology-assisted, and less invasive treatment modalities is reshaping patient expectations and clinical practice standards. Consequently, pharmaceutical and medical device companies are expanding their R&D investments in next-generation pain management and neurorestorative therapies for adhesive arachnoiditis

- The demand for effective, patient-centric treatment solutions is expected to grow rapidly across both specialized neurology centers and general hospitals, driven by rising awareness, improved diagnostic capabilities, and an increasing global incidence of spinal injuries and complications leading to adhesive arachnoiditis

Adhesive Arachnoiditis Treatment Market Dynamics

Driver

Growing Need Due to Increasing Chronic Pain Cases and Advancements in Neurotherapy

- The rising global prevalence of chronic pain conditions, particularly those resulting from spinal injuries, surgeries, or infections, is a significant driver for the heightened demand for adhesive arachnoiditis treatment

- For instance, in April 2024, Pfizer Inc. announced advancements in targeted anti-inflammatory and neuroprotective drug research, aiming to improve outcomes for patients with adhesive arachnoiditis. Such strategic R&D initiatives by leading companies are expected to drive the adhesive arachnoiditis treatment industry growth in the forecast period

- As patients and healthcare providers become more aware of adhesive arachnoiditis symptoms and its debilitating impact, demand for effective pain management solutions and minimally invasive interventions is increasing. Treatments such as neurostimulation, targeted drug delivery, and advanced physiotherapy are offering improved quality of life for affected individual.

- Furthermore, technological advancements in spinal imaging, such as high-resolution MRI and AI-assisted diagnostics, are enabling earlier detection and more personalized treatment planning. This trend is driving hospitals, specialty pain clinics, and research institutions to adopt advanced therapeutic options for adhesive arachnoiditis

- The growing availability of multidisciplinary pain management programs, as well as increased healthcare access in developing markets, is further contributing to industry expansion. Rising patient preference for non-opioid treatments and regenerative medicine approaches is also creating new growth avenues for the market

Restraint/Challenge

Concerns Regarding Treatment Accessibility and High Procedure Costs

- Limited accessibility to specialized pain management centers, especially in rural and underserved regions, poses a significant challenge to broader adoption of adhesive arachnoiditis treatment solutions. Patients often face delays in diagnosis and lack of access to advanced therapies, hindering optimal outcomes

- For instance, high-profile reports on the shortage of pain specialists and long waiting times for interventional procedures have highlighted systemic healthcare gaps that restrict timely treatment

- The high cost of advanced interventions such as spinal cord stimulators, intrathecal drug delivery systems, and regenerative therapies can also be a barrier to adoption for patients without comprehensive insurance coverage. In some cases, treatment expenses can run into thousands of dollars, creating affordability issues in low- and middle-income countries

- Overcoming these challenges will require broader reimbursement coverage, increased training for healthcare providers in pain management, and development of cost-effective therapeutic alternatives. Companies are focusing on offering tiered pricing strategies and localized manufacturing to make treatments more accessible

- While affordability is gradually improving, the perceived premium nature of advanced interventions can still hinder widespread adoption, particularly among patients with mild to moderate symptoms who may opt for conservative management instead

Adhesive Arachnoiditis Treatment Market Scope

The market is segmented on the basis of treatment, diagnosis, dosage, route of administration, distribution channel, and end user.

- By Treatment

On the basis of treatment, the adhesive arachnoiditis treatment market is segmented into nonsteroidal anti-inflammatory drugs (NSAIDs), corticosteroids, analgesics, physiotherapy, nerve stimulation, psychotherapy, and others. The NSAIDs segment accounted for the largest market revenue share of 37.6% in 2024, owing to their extensive use in managing pain, inflammation, and discomfort associated with spinal muscular atrophy. These medications are widely preferred due to their accessibility, affordability, and effectiveness in controlling mild-to-moderate symptoms across different patient groups.

Physiotherapy is anticipated to witness the fastest CAGR of 9.8% from 2025 to 2032, supported by the increasing emphasis on non-pharmacological interventions. Rehabilitation programs, mobility enhancement therapies, and personalized physiotherapy regimens are helping improve patient functionality, strength, and overall quality of life, driving its adoption across clinics and hospitals.

- By Diagnosis

On the basis of diagnosis, the adhesive arachnoiditis treatment market is segmented into MRI, CAT scan, electromyogram, and others. The MRI segment dominated the market with a revenue share of 44.2% in 2024, due to its high accuracy in detecting neuromuscular degeneration and monitoring disease progression. The adoption of advanced imaging technologies such as high-resolution MRI and 3D reconstruction is enabling clinicians to provide timely and precise treatment interventions.

The electromyogram (EMG) segment is expected to register the fastest CAGR of 8.7% from 2025 to 2032 in the market, driven by its growing adoption in clinical practice. EMG plays a vital role in assessing nerve root irritation, muscle weakness, and neurological impairments associated with adhesive arachnoiditis. Its ability to provide objective measurements supports early disease detection, monitoring of progression, and tailoring of personalized therapeutic strategies. Moreover, technological advancements in EMG devices are enhancing diagnostic precision, making it a preferred tool among neurologists and pain specialists.

- By Dosage

On the basis of dosage, the adhesive arachnoiditis treatment market is segmented into tablet, injection, and others. The injection segment held the largest share of 53.5% in 2024, primarily due to the widespread use of injectable therapies such as corticosteroids and biologics. Injectable formulations offer targeted delivery, rapid onset of action, and enhanced efficacy, especially in severe cases requiring hospital-based administration.

The tablet segment is projected to record the fastest CAGR of 7.9% from 2025 to 2032 in the market, owing to the rising preference for oral therapies by both patients and healthcare providers. Tablets offer ease of administration, portability, and improved patient adherence compared to injectables or complex therapies, making them highly suitable for long-term management of chronic conditions such as adhesive arachnoiditis. Additionally, advancements in drug formulations, extended-release mechanisms, and the availability of generic options are further boosting their adoption across global healthcare settings.

- By Route of Administration

On the basis of route of administration, the adhesive arachnoiditis treatment market is segmented into oral, intravenous, intramuscular, and others. The oral segment accounted for the largest share of 57.8% in 2024, reflecting the widespread preference for pills and capsules among patients for chronic management and symptomatic relief. Oral therapies are favored due to their ease of use, convenience for long-term treatment, and improved patient adherence, making them the most commonly prescribed route in outpatient and homecare settings.

The intravenous segment is anticipated to register the fastest CAGR of 9.2% from 2025 to 2032, driven by the increasing adoption of hospital-administered therapies, biologics, and infusion-based treatments. This growth is supported by the need for precise, controlled, and rapid drug delivery in severe or complex cases, as well as advancements in infusion technologies and hospital infrastructure that enable safe and effective administration.

- By End Users

On the basis of end users, the adhesive arachnoiditis treatment market is segmented into clinic, hospital, and others. Hospitals accounted for the largest market revenue share of 48.7% in 2024, owing to their comprehensive treatment facilities, availability of multidisciplinary care teams, and access to advanced diagnostic and therapeutic modalities required for managing complex cases of adhesive arachnoiditis treatment market. Hospitals also provide integrated care, including monitoring, therapy administration, and follow-up, which contributes to their dominant market position.

Clinics are expected to witness the fastest CAGR of 10.5% from 2025 to 2032, supported by the increasing number of outpatient visits, expansion of specialty and private care centers, and growing patient awareness about early detection and disease management. Clinics are increasingly adopting patient-centric care models, providing personalized therapies and follow-up services, which is driving their rapid growth in the market.

- By Distribution Channel

On the basis of distribution channel, the adhesive arachnoiditis treatment market is segmented into hospital pharmacy, retail pharmacy, and online pharmacy. Hospital pharmacies dominated the market with a revenue share of 45.0% in 2024, as patients often receive initial prescriptions, follow-up medications, and critical therapies directly within hospital settings. These pharmacies also benefit from bulk procurement, integrated supply chains, and direct access to inpatient care needs, reinforcing their leading market share.

The online pharmacy segment is projected to register the fastest CAGR of 11.3% during the forecast period, propelled by rising telemedicine adoption, growing e-commerce penetration, and increasing patient preference for convenient, home-delivered access to prescription medications and specialty therapies. The segment’s growth is further enhanced by the demand for discreet purchasing and flexible delivery options, especially among patients requiring long-term treatment.

Adhesive Arachnoiditis Treatment Market Regional Analysis

- North America dominated the adhesive arachnoiditis treatment market in 2024, accounting for the largest revenue share of 45%. This dominance is primarily attributed to the region’s advanced healthcare infrastructure, higher diagnosis rates of rare spinal disorders, and strong presence of specialized pain management centers

- The availability of cutting-edge diagnostic imaging tools, combined with multidisciplinary treatment approaches—including pharmacological therapies, targeted drug delivery systems, and neuromodulation devices—has significantly improved patient outcomes

- Furthermore, supportive reimbursement policies, a well-established network of neurological specialists, and continuous R&D funding from both public and private sectors are driving consistent market expansion in the region

U.S. Adhesive Arachnoiditis Treatment Market Insight

The U.S. adhesive arachnoiditis treatment market held the largest share of 66% in 2024, driven by early adoption of innovative therapies and advanced interventional pain management techniques. A strong ecosystem of academic research institutions, biotechnology companies, and specialized hospitals supports the development and commercialization of novel treatment modalities. In addition, heightened patient awareness, growing advocacy from rare disease organizations, and wider insurance coverage for both pharmacological and non-pharmacological interventions are creating favorable conditions for market growth. Government-funded research grants and clinical trial activities are also enabling the introduction of next-generation therapeutics tailored for chronic spinal inflammation.

Europe Adhesive Arachnoiditis Treatment Market Insight

The Europe adhesive arachnoiditis treatment market is expected to expand steadily over the forecast period, supported by rising clinical recognition of the condition and increasing investment in specialized care pathways. The region benefits from robust public healthcare systems, extensive cross-border collaborations, and well-established research networks dedicated to rare neurological diseases. Technological advancements in spinal imaging, greater adoption of minimally invasive interventions, and government-backed funding for pain management programs are further enhancing patient access to quality care. Growing patient advocacy movements across Europe are also contributing to earlier diagnosis and better treatment adherence.

U.K. Adhesive Arachnoiditis Treatment Market Insight

The U.K. adhesive arachnoiditis treatment market is anticipated to witness notable growth, supported by a sophisticated healthcare infrastructure and proactive government policies aimed at improving chronic pain management. Expansion of specialized pain clinics, coupled with the adoption of regenerative medicine and precision therapy techniques, is fostering improved treatment outcomes. Furthermore, increasing collaboration between the National Health Service (NHS), research institutions, and patient support organizations is facilitating the development of comprehensive care models tailored to individual patient needs.

Germany Adhesive Arachnoiditis Treatment Market Insight

The Germany adhesive arachnoiditis treatment market growth is underpinned by its advanced medical technology sector, network of neurological specialists, and a patient-centered approach to chronic pain care. The strong country’s commitment to medical innovation—particularly in neurorehabilitation, biologic therapies, and minimally invasive spinal procedures—is driving adoption of new treatment solutions. Furthermore, government incentives for rare disease research and active participation in multinational clinical trials are positioning Germany as a leader in advancing therapeutic options for adhesive arachnoiditis.

Asia-Pacific Adhesive Arachnoiditis Treatment Market Insight

The Asia-Pacific adhesive arachnoiditis treatment market is projected to record the fastest CAGR from 2025 to 2032, fueled by growing awareness of spinal health, expansion of healthcare infrastructure, and rising accessibility to advanced diagnostic services. Countries in the region are increasingly investing in medical technology upgrades, enabling earlier detection and intervention. Emerging economies such as India and Indonesia are improving patient outreach through public health initiatives, while developed markets like Japan and Australia are leveraging high-end imaging and regenerative therapies for complex spinal conditions. Strategic partnerships between local providers and global medical device companies are also accelerating market penetration.

Japan Adhesive Arachnoiditis Treatment Market Insight

The Japan adhesive arachnoiditis treatment market growth is driven by its aging population, high adoption rate of advanced medical technologies, and strong focus on personalized pain management solutions. The country’s healthcare system emphasizes precision diagnosis through state-of-the-art imaging techniques, enabling timely initiation of targeted therapies. Additionally, the integration of regenerative medicine approaches and the expansion of specialized spinal care centers are significantly enhancing patient care standards.

China Adhesive Arachnoiditis Treatment Market Insight

The China adhesive arachnoiditis treatment market accounted for the largest share of the Asia-Pacific market in 2024, supported by rapid healthcare modernization, growing middle-class access to specialty treatments, and increasing government investment in rare disease programs. Domestic pharmaceutical and medical device manufacturers are introducing more affordable therapeutic options, improving treatment accessibility in both urban and rural areas. National awareness campaigns, coupled with expanded diagnostic capabilities in tier-2 and tier-3 cities, are driving higher diagnosis rates and fostering market growth.

Adhesive Arachnoiditis Treatment Market Share

The adhesive arachnoiditis treatment industry is primarily led by well-established companies, including:

- Takeda Pharmaceutical Company Limited (Japan)

- Sumitomo Dainippon Pharma Co., Ltd. (Japan)

- Sun Pharmaceutical Industries Ltd. (India)

- Pfizer Inc. (U.S.)

- Novartis AG (Switzerland)

- Sanofi (France)

- Bristol-Myers Squibb Company (U.S.)

- AstraZeneca (U.K.)

- Johnson & Johnson and its affiliates (U.S.)

- Baxter (U.S.)

- B. Braun SE (Germany)

- Sandoz International GmbH (Germany)

- Viatris Inc. (U.S.)

- Teva Pharmaceutical Industries Ltd. (Israel)

- Endo International plc (Ireland)

- Hikma Pharmaceuticals PLC (Jordan)

- Mallinckrodt (U.S.)

- Apotex Inc. (Canada)

- Abbott (U.S.)

- Bayer AG (Germany)

- LEO Pharma A/S (Denmark)

- Merck & Co., Inc. (U.S.)

- GSK plc (U.K.)

- Cipla Inc. (India)

Latest Developments in Global Adhesive Arachnoiditis Treatment Market

- In July 2021, Nevro received FDA approval for its 10 kHz Senza SCS therapy to treat painful diabetic neuropathy (PDN), expanding the U.S. SCS market; while not arachnoiditis-specific, SCS is a key modality for refractory neuropathic pain often seen in adhesive arachnoiditis

- In August 2022, Abbott announced FDA approval of Proclaim Plus SCS with FlexBurst360 therapy, a next-gen burst platform designed for broader, individualized pain coverage—relevant to complex neuropathic pain management pathways used for arachnoiditis

- In January 2023, Abbott reported the U.S. launch of its Eterna SCS system (the industry’s smallest, rechargeable implantable pulse generator at launch), advancing patient comfort and long-term neuromodulation options for chronic pain populations that include arachnoiditis patients

- In May 2023, Abbott received FDA approval to expand SCS indications to nonsurgical back pain—broadening access to neuromodulation for patients with intractable axial/radicular pain, a cohort that overlaps with adhesive arachnoiditis management in multidisciplinary pain programs

- In April 2024, the FDA approved Medtronic’s Inceptiv closed-loop SCS system (the first that automatically adjusts stimulation in real time based on the body’s signals), improving individualized therapy delivery for chronic pain, including difficult neuropathic conditions

- In May 2024, an update from the Polyanalgesic Consensus Conference (PACC) was released, providing contemporary, expert-driven guidance on intrathecal drug delivery (ITDD) for chronic pain—directly informing care pathways for adhesive arachnoiditis where ITDD can be considered after conservative measures

- In January 2025, Saluda Medical received FDA approval for EVA, an AI-enabled programming platform for its ECAP-controlled Evoke® SCS system, aimed at faster, more precise pain relief optimization—further modernizing neuromodulation options used across refractory neuropathic pain indications

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.