Global Advanced Structural Ceramics Market

Market Size in USD Billion

USD

7.15 Billion

USD

11.92 Billion

2024

2032

USD

7.15 Billion

USD

11.92 Billion

2024

2032

| 2025 - 2032 | |

| USD 7.15 Billion | |

| USD 11.92 Billion | |

| % | |

|

Advanced Structural Ceramics Market Size

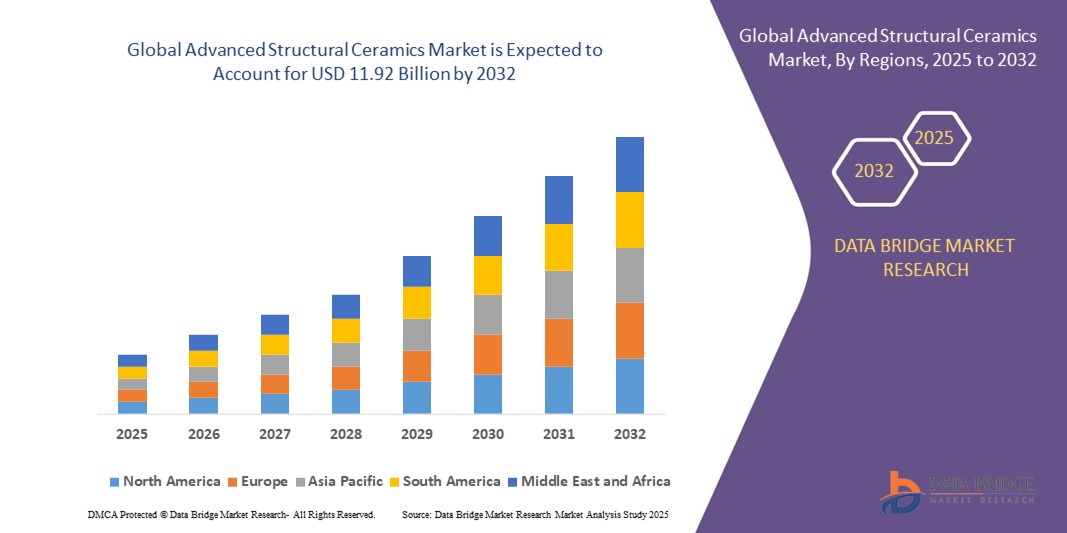

- The global advanced structural ceramics market size was valued at USD 7.15 billion in 2024 and is expected to reach USD 11.92 billion by 2032, at a CAGR of 6.60% during the forecast period

- The market growth is largely fuelled by the rising demand for lightweight, high-strength materials in aerospace, automotive, and industrial manufacturing applications

- Increasing adoption of ceramics for wear-resistant and high-temperature components is driving the expansion of the market across multiple sectors

Advanced Structural Ceramics Market Analysis

- Growing requirement for high-performance materials in electronics, medical devices, and energy sectors is supporting market growth

- Technological innovations and continuous R&D in ceramic composites and nanostructured ceramics are enhancing product performance and application scope

- North America dominated the advanced structural ceramics market with the largest revenue share in 2024, driven by the growing adoption of high-performance materials in aerospace, automotive, and industrial machinery. The presence of leading manufacturers and robust R&D infrastructure further strengthens market growth

- Asia-Pacific region is expected to witness the highest growth rate in the global advanced structural ceramics market, driven by rising demand from automotive, aerospace, and energy sectors, coupled with favorable government policies, increasing urbanization, and the presence of emerging ceramic component manufacturers

- The Alumina Ceramics segment held the largest market revenue share in 2024, driven by its widespread use in automotive, electronics, and industrial applications due to high wear resistance, thermal stability, and cost-effectiveness. Alumina ceramics are widely adopted for components requiring durability and long service life, making them a preferred choice across multiple industries.

Report Scope and Advanced Structural Ceramics Market Segmentation

|

Attributes |

Advanced Structural Ceramics Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

• Increasing Adoption In Aerospace And Automotive Applications |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Advanced Structural Ceramics Market Trends

Increasing Adoption of High-Performance Ceramics Across Industries

• The growing shift toward advanced structural ceramics is transforming multiple industries by enabling high-strength, lightweight, and heat-resistant components. The superior mechanical properties and durability of these ceramics allow for enhanced performance in aerospace, automotive, and industrial applications, improving efficiency, reducing maintenance costs, and supporting sustainability goals. Industries increasingly rely on ceramics to achieve better operational reliability under extreme conditions

• The high demand for wear-resistant and corrosion-resistant components is accelerating the adoption of ceramic materials in machinery, tooling, and electronics. These materials are particularly effective where metal alternatives fail under extreme conditions, supporting longer equipment lifespan, reducing downtime, and minimizing replacement costs. This trend is driving research into hybrid ceramic composites for specialized applications

• Advancements in manufacturing techniques, including additive manufacturing, precision machining, and advanced sintering processes, are making complex ceramic components more accessible and cost-effective. These innovations are enabling the production of intricate designs, enhancing performance consistency, and widening application across aerospace, medical, and electronics industries

• For instance, in 2023, several European and North American aerospace manufacturers reported increased use of ceramic engine components, leading to improved fuel efficiency, reduced emissions, and lower maintenance requirements. The integration of ceramics into high-stress parts is also fostering innovation in component design and lightweight solutions

• While advanced structural ceramics are driving performance improvements and operational efficiency, their market potential depends on continued innovation, cost optimization, and awareness campaigns. Manufacturers must focus on application-specific solutions, regulatory compliance, and quality assurance to fully capitalize on growing demand

Advanced Structural Ceramics Market Dynamics

Driver

Rising Demand for Lightweight, High-Strength, and Heat-Resistant Materials

• The increasing need for lightweight and durable materials in aerospace, automotive, and industrial machinery is pushing manufacturers to adopt advanced structural ceramics. These materials provide enhanced performance under high stress and temperature conditions, helping reduce fuel consumption, improve safety, and extend equipment lifespan. Rising adoption is also driven by stringent industry standards for reliability

• Industries are increasingly aware of the benefits of ceramics, including reduced weight, improved wear resistance, and longer component lifespan, leading to higher adoption across various applications. Companies are leveraging ceramics to reduce operational costs, enhance product performance, and gain a competitive edge in technology-driven markets

• Government initiatives promoting energy efficiency, emissions reduction, and sustainability in manufacturing are supporting the adoption of lightweight and high-performance materials. Incentives and grants for industrial innovation are encouraging more widespread deployment of ceramics in strategic applications

• For instance, in 2022, multiple automotive OEMs in Europe and Asia integrated ceramic components into engines and braking systems, resulting in lower emissions, higher vehicle efficiency, and improved safety. The trend is also influencing supply chain strategies and partnerships with material technology providers

• While industrial demand is driving growth, consistent material quality, production scalability, and cost-effective manufacturing remain essential for sustained adoption and market expansion. Focus on R&D and standardization of processes will be critical for long-term industry growth

Restraint/Challenge

High Production Costs and Technical Complexity of Advanced Ceramics

• The high cost of raw materials and precision manufacturing processes makes advanced structural ceramics less accessible for price-sensitive industries and small-scale manufacturers. Cost remains a major limiting factor for widespread usage, and pricing pressures may slow adoption in developing markets

• In many regions, a lack of skilled personnel, specialized machinery, and advanced facilities capable of producing complex ceramic components limits adoption. This results in dependence on conventional materials or imported components, slowing local market growth, and creating challenges for regional supply chains

• Supply chain challenges and limited availability of specialized ceramic powders or composites restrict production capacity, delaying delivery to end users and impacting industrial adoption. In addition, quality control and reproducibility of ceramic components pose technical hurdles for manufacturers targeting high-performance sectors

• For instance, in 2023, several manufacturers in Asia and Europe reported delays in meeting industrial demand due to high production costs and technical complexity of ceramic components. This highlighted the need for investment in advanced fabrication techniques, workforce training, and process optimization

• While material innovations continue, addressing cost, technical expertise, infrastructure, and manufacturing scalability is crucial for unlocking the long-term growth potential of the global advanced structural ceramics market. Companies focusing on hybrid materials, modular production, and strategic collaborations are likely to gain a competitive advantage

Advanced Structural Ceramics Market Scope

The market is segmented on the basis of type and application.

- By Type

On the basis of type, the advanced structural ceramics market is segmented into Alumina Ceramics, Silicon Carbide Ceramics, Zirconia Ceramics, Titanium Carbide Ceramics, and Others. The Alumina Ceramics segment held the largest market revenue share in 2024, driven by its widespread use in automotive, electronics, and industrial applications due to high wear resistance, thermal stability, and cost-effectiveness. Alumina ceramics are widely adopted for components requiring durability and long service life, making them a preferred choice across multiple industries.

The Silicon Carbide Ceramics segment is expected to witness the fastest growth rate from 2025 to 2032, driven by its exceptional hardness, high-temperature tolerance, and chemical stability, making it ideal for high-performance applications in aerospace, energy, and industrial machinery. Silicon carbide ceramics are particularly preferred for components exposed to extreme conditions, enabling improved efficiency, reduced maintenance, and enhanced operational reliability.

- By Application

On the basis of application, the market is segmented into Automotive, Electronics and Electricals, Aerospace & Defense, Medical, Energy and Power, Industrial Machinery, and Others. The Automotive segment held the largest revenue share in 2024, owing to the increasing integration of lightweight, heat-resistant, and wear-resistant ceramic components in engines, brakes, and sensors to improve efficiency and reduce emissions.

The Aerospace & Defense segment is expected to witness the fastest growth rate from 2025 to 2032, driven by rising demand for lightweight, high-strength, and heat-resistant materials in aircraft engines, armor systems, and satellite components. Ceramics in aerospace applications help improve fuel efficiency, reduce component weight, and enhance operational safety under extreme conditions.

Advanced Structural Ceramics Market Regional Analysis

• North America dominated the advanced structural ceramics market with the largest revenue share in 2024, driven by the growing adoption of high-performance materials in aerospace, automotive, and industrial machinery. The presence of leading manufacturers and robust R&D infrastructure further strengthens market growth

• Consumers and industries in the region highly value the durability, lightweight nature, and heat-resistant properties of advanced structural ceramics, which enhance equipment performance and reduce maintenance costs

• This widespread adoption is further supported by government initiatives promoting energy efficiency, sustainability, and advanced manufacturing technologies, establishing structural ceramics as a preferred solution across multiple industrial sectors

U.S. Advanced Structural Ceramics Market Insight

The U.S. advanced structural ceramics market captured the largest revenue share in North America in 2024, fueled by strong demand from aerospace, defense, and automotive industries. Manufacturers are increasingly prioritizing lightweight, durable, and heat-resistant ceramic components to improve efficiency and reduce operational costs. Technological advancements, coupled with investments in precision manufacturing and additive manufacturing techniques, are further propelling market growth. Moreover, collaborations between industrial players and research institutions are accelerating the development of application-specific ceramic materials, expanding market opportunities.

Europe Advanced Structural Ceramics Market Insight

The Europe advanced structural ceramics market is expected to witness the fastest growth rate from 2025 to 2032, primarily driven by the adoption of high-performance ceramics in automotive, aerospace, and industrial machinery sectors. Stringent regulations on emissions, energy efficiency, and safety are pushing manufacturers to integrate lightweight and durable ceramic components. European industries are also drawn to the superior wear and corrosion resistance of structural ceramics, fostering increased adoption across applications such as electronics, medical, and energy systems.

Germany Advanced Structural Ceramics Market Insight

The Germany advanced structural ceramics market is expected to witness the fastest growth rate from 2025 to 2032, fueled by the country’s strong emphasis on industrial innovation and precision engineering. German manufacturers are increasingly integrating ceramics into automotive engines, braking systems, and high-temperature industrial machinery. The combination of advanced manufacturing capabilities, research and development infrastructure, and focus on sustainable materials drives higher adoption of structural ceramics across domestic and export-oriented industries.

U.K. Advanced Structural Ceramics Market Insight

The U.K. advanced structural ceramics market is expected to witness the fastest growth rate from 2025 to 2032, driven by increasing demand from aerospace, automotive, and industrial machinery sectors. The adoption of high-performance, lightweight, and heat-resistant ceramic components is being accelerated by stringent safety and environmental regulations. In addition, the U.K.’s focus on innovation, research, and development, along with collaborations between manufacturers and academic institutions, is fostering the development of application-specific ceramics, further boosting market growth across domestic and export industries.

Asia-Pacific Advanced Structural Ceramics Market Insight

The Asia-Pacific advanced structural ceramics market is expected to witness the fastest growth rate from 2025 to 2032, driven by rapid industrialization, growing automotive and electronics production, and increasing adoption in aerospace and defense sectors in countries such as China, Japan, and India. The region’s expanding manufacturing base, availability of cost-effective raw materials, and government support for advanced material technologies are boosting market penetration.

Japan Advanced Structural Ceramics Market Insight

The Japan advanced structural ceramics market is expected to witness the fastest growth rate from 2025 to 2032 due to the country’s high-tech industrial ecosystem, strong automotive and electronics sectors, and demand for durable, lightweight, and heat-resistant components. Integration of ceramics in machinery, engines, and industrial equipment is expanding, while collaborations between manufacturers and research institutions drive product innovation. Japan’s focus on sustainable and high-efficiency materials is expected to further propel market growth in both domestic and export markets.

China Advanced Structural Ceramics Market Insight

The China advanced structural ceramics market accounted for the largest market revenue share in Asia-Pacific in 2024, attributed to the country’s rapidly growing industrial, automotive, and electronics sectors. High adoption of ceramics in energy, aerospace, and machinery manufacturing is driven by the availability of affordable raw materials, domestic manufacturing capabilities, and government initiatives promoting advanced material technologies. The push toward smart manufacturing and high-performance industrial solutions further supports the expansion of the advanced structural ceramics market in China.

Advanced Structural Ceramics Market Share

The Advanced Structural Ceramics industry is primarily led by well-established companies, including:

- Kyocera Corporation (Japan)

- Saint-Gobain (France)

- Morgan Advanced Materials plc (U.K.)

- CoorsTek, Inc. (U.S.)

- CeramTec GmbH (Germany)

- 3M (U.S.)

- McDanel Advanced Ceramic Technologies (U.S.)

- Rauschert GmbH (Germany)

- NGK Spark Plug Co., Ltd. (Japan)

- KEMET Corporation (U.S.)

- Blasch Precision Ceramics, Inc. (U.S.)

- SCHOTT AG (Germany)

- Superior Technical Ceramics Corporation (U.S.)

- Sumitomo Electric Industries, Ltd. (Japan)

- Ortech Advanced Ceramics (Canada)

- Murata Manufacturing Co., Ltd. (Japan)

- Advanced Ceramics Manufacturing, LLC (U.S.)

- SCO Tech LLC (U.S.)

- Insaco, Inc. (U.S.)

Latest Developments in Global Advanced Structural Ceramics Market

- In July 2024, Kyocera Corporation launched its Fine Cordierite ceramic mirror, specifically developed for use in experimental equipment to enable optical communication between the International Space Station (ISS) and a mobile optical station on Earth. This innovation marks the first use of cordierite in this application, offering high thermal stability and precision performance. The development is expected to enhance optical communication reliability and promote Kyocera’s presence in advanced aerospace ceramic solutions, positively impacting market perception and adoption in high-tech sectors

- In June 2024, CeramTec developed Sinalit, a high-performance silicon nitride ceramic substrate designed for electric mobility and power electronics applications. The new product provides superior mechanical strength, thermal stability, and electrical insulation, supporting efficient performance in demanding environments. Sinalit is anticipated to drive market growth by addressing the rising demand for advanced ceramics in electric vehicles and energy-efficient power systems, strengthening CeramTec’s portfolio in the mobility and electronics segments

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.