Global Advanced Surgical Secondary Segment Market

Market Size in USD Billion

USD

8.16 Billion

USD

13.50 Billion

2025

2033

USD

8.16 Billion

USD

13.50 Billion

2025

2033

Forecast Period |

2026 - 2033 |

Market Size (Base Year) |

USD 8.16 Billion |

Market Size (Forecast Year) |

USD 13.50 Billion |

CAGR |

% |

Major Markets Players |

|

Advanced Surgical Market (Secondary Segment) Overview

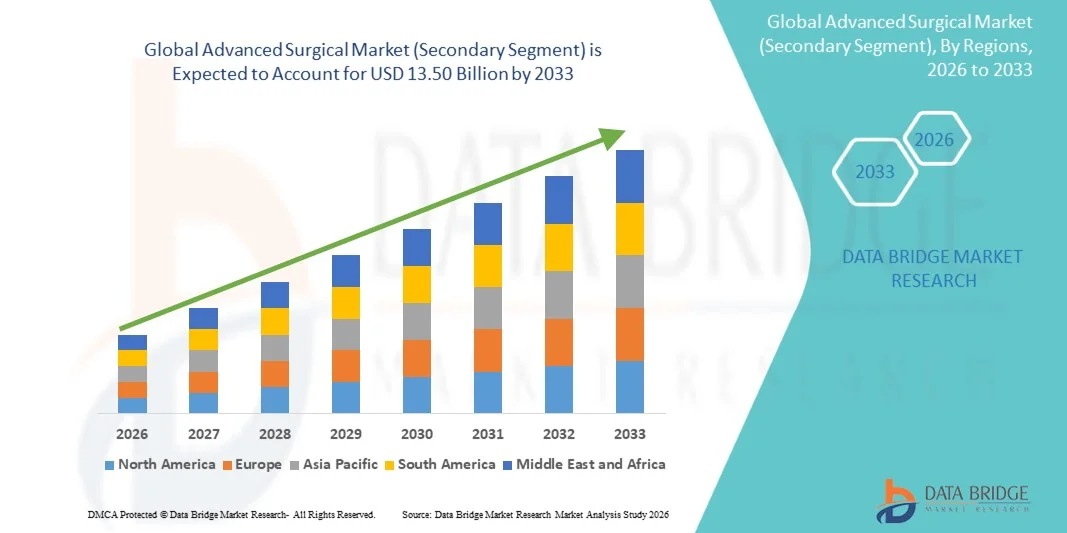

The Advanced Surgical Market (Secondary Segment) was valued at USD 8.16 billion in 2025 and is projected to reach USD 13.50 billion by 2033, growing at a CAGR of 6.50% from 2026 to 2033. The market is experiencing steady growth driven by the rising demand for minimally invasive and precision-based surgical procedures, increasing adoption of robotic-assisted surgical systems, and rapid advancements in surgical technologies such as AI-guided navigation, enhanced imaging systems, and next-generation surgical instruments.

The growing prevalence of chronic diseases, including cardiovascular disorders, cancer, and orthopedic conditions, is significantly increasing the volume of surgical interventions worldwide. In addition, the shift toward value-based healthcare and the need to reduce post-operative complications are encouraging hospitals and surgical centers to adopt advanced surgical techniques that improve patient outcomes and reduce recovery time. Fixed-base and VR/AR-enabled surgical simulation platforms are also increasingly being used in medical training programs, enabling surgeons to practice complex procedures in risk-free, highly realistic environments before performing actual operations.

Key Market Trends & Insights

- North America dominated the Advanced Surgical Market (Secondary Segment) with the largest revenue share of 39.12% in 2025, supported by advanced healthcare infrastructure, high adoption of robotic-assisted and minimally invasive surgical technologies, strong presence of leading medical device companies, and well-established surgical training systems. The region also benefits from a high volume of complex surgical procedures, favorable reimbursement frameworks, and rapid integration of AI-powered imaging and navigation systems in operating rooms, which further strengthens its leadership position in the global market.

- The Open Surgery segment dominated the market with a 39.12% revenue share in 2025, supported by its continued clinical necessity in complex and emergency surgical interventions where advanced robotic or endoscopic tools are not feasible.

- Asia-Pacific is the fastest-growing region at a CAGR of 7.9% from 2026 to 2033, driven by rapidly improving healthcare infrastructure, rising healthcare expenditure, increasing prevalence of chronic diseases, and growing demand for advanced surgical procedures. Expanding hospital networks, rising adoption of minimally invasive and robotic surgeries in countries such as China, India, and Japan, and increasing government investments in modernizing surgical care facilities are further accelerating regional market growth.

- Cardiovascular Surgery segment leads the Advanced Surgical Market (Secondary Segment) with a 36.84% revenue share in 2025, driven by the rising prevalence of coronary artery disease, hypertension-related complications, and increasing demand for cardiac interventions such as bypass surgeries and valve replacements. The segment benefits from strong adoption of advanced surgical technologies, including minimally invasive cardiac procedures and image-guided surgical systems.

- Neurological Surgery is the fastest-growing application segment, expected to register a CAGR of 8.1% from 2026 to 2033, fueled by rising incidence of brain tumors, stroke-related complications, and spinal disorders. Continuous advancements in neuronavigation systems, robotic neurosurgery platforms, and intraoperative imaging are enhancing surgical accuracy and safety, driving rapid expansion of this segment across advanced healthcare markets.

Market Size & Forecast

- Global Market Value (2025): USD 8.16 Billion

- Expected Market Value (2033): USD 13.50 Billion

- Forecast CAGR (2026–2033): 6.50%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia-Pacific

Report Scope and Advanced Surgical Market (Secondary Segment) Segmentation

|

Attributes |

Driving Simulators Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

• Medtronic plc (Ireland) |

|

Market Opportunities |

· Expansion of Robotic-Assisted and AI-Guided Surgery Systems · Growth in Ambulatory Surgical Centers (ASCs) and Minimally Invasive Procedures · Rising Healthcare Investment in Emerging Markets |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, geographically represented company-wise production and capacity, network layouts of distributors and partners, detailed and updated price trend analysis and deficit analysis of supply chain and demand. |

Advanced Surgical Market (Secondary Segment) Trends

Trend: Growth in Minimally Invasive and Robotic-Assisted Surgical Procedures

Hospitals and surgical centers are increasingly adopting advanced surgical systems such as robotic-assisted platforms, laparoscopic instruments, and image-guided navigation systems to improve precision and reduce patient recovery time. The integration of real-time imaging, AI-assisted decision support, and high-definition 3D visualization is enabling surgeons to perform highly complex procedures with improved accuracy and reduced complication rates. According to global surgical studies, minimally invasive procedures can reduce hospital stays by up to 30–50% compared to traditional open surgeries, significantly improving healthcare efficiency. Surgical training institutions are also leveraging VR- and AR-based simulation platforms to train surgeons in risk-free environments, enabling standardized skill development for complex procedures such as cardiac, neurological, and oncological surgeries.

Advanced Surgical Market (Secondary Segment) Dynamics

Key Market Driver: Rising Burden of Chronic Diseases and Increasing Surgical Volume

The increasing prevalence of chronic diseases such as cardiovascular disorders, cancer, neurological conditions, and orthopedic complications is significantly driving demand for advanced surgical interventions. According to global health statistics, cardiovascular diseases alone account for nearly 17.9 million deaths annually, making them the leading cause of surgical procedures worldwide. This rising disease burden is pushing hospitals to adopt advanced surgical systems, including robotic-assisted surgery platforms, minimally invasive instruments, and AI-powered surgical navigation tools. Leading medical device companies such as Intuitive Surgical, Medtronic, and Johnson & Johnson are continuously innovating to improve surgical precision, reduce operative risks, and enhance patient outcomes. The expansion of specialized surgical centers and increasing adoption of digital operating rooms are further accelerating market growth globally.

Key Restraint/Challenge: High Cost of Advanced Surgical Systems and Limited Accessibility

A major challenge in the advanced surgical market is the high cost associated with acquiring, installing, and maintaining advanced surgical systems, particularly robotic-assisted and image-guided platforms. A single robotic surgical system can cost between USD 1 million to USD 2.5 million, excluding maintenance and disposable instrument costs, making it difficult for small and mid-sized hospitals to adopt these technologies. In addition, ongoing expenses related to surgeon training, system upgrades, and consumables increase the total cost of ownership. Limited reimbursement coverage in developing regions further restricts adoption. Healthcare infrastructure gaps, especially in rural and low-income areas, also limit access to advanced surgical care, resulting in uneven global distribution of these technologies.

Key Market Opportunity: Expansion of Robotic Surgery, AI Integration, and Digital Operating Rooms

The advanced surgical market presents significant growth opportunities through the expansion of robotic-assisted surgery, AI-powered surgical planning, and fully integrated digital operating rooms. AI-based systems are increasingly being used for preoperative planning, intraoperative guidance, and postoperative analysis, improving surgical precision and reducing complications. The adoption of robotic surgery is growing at a strong pace, with robotic procedures increasing by over 15–20% annually in leading healthcare markets such as the United States and Europe. In addition, emerging economies in Asia-Pacific and the Middle East are heavily investing in modern hospital infrastructure and surgical training programs. The development of hybrid operating rooms equipped with advanced imaging, robotics, and real-time data analytics is further transforming surgical workflows and creating long-term growth opportunities for market players.

Advanced Surgical Market (Secondary Segment) Scope

The Advanced Surgical Market (Secondary Segment) is segmented on the basis of surgical type and application.

By Surgical Type

On the basis of surgical type, the Advanced Surgical Market (Secondary Segment) is segmented into open surgery, minimally invasive surgery, robotic-assisted surgery, and endoscopic surgery. The Open Surgery segment dominated the market with a 39.12% revenue share in 2025, supported by its continued clinical necessity in complex and emergency surgical interventions where advanced robotic or endoscopic tools are not feasible. It remains widely used in trauma care, oncology, and cardiovascular emergencies, particularly in developing regions where healthcare infrastructure is still evolving. Hospitals continue to rely on open procedures due to their versatility across multiple surgical specialties and lower dependency on expensive infrastructure. In addition, training familiarity among surgeons and established procedural protocols further reinforce its dominance. Despite technological advancements, open surgery maintains strong demand due to its critical role in life-saving operations.

The Minimally Invasive Surgery segment is expected to witness the fastest CAGR of 7.9% from 2026 to 2033, driven by increasing patient preference for reduced pain, minimal scarring, and faster recovery times. Hospitals are rapidly adopting laparoscopic, endoscopic, and robotic-assisted surgical systems to improve procedural precision and clinical outcomes. Advancements in 3D imaging, AI-assisted navigation, and high-definition visualization are significantly improving surgical accuracy. In addition, minimally invasive techniques reduce hospital stay duration by up to 30–50%, lowering healthcare costs and improving operational efficiency. Rising prevalence of chronic diseases requiring surgical intervention is further boosting demand. Growing investments in robotic surgical platforms such as Intuitive Surgical systems are accelerating adoption globally. Expanding surgical training programs in emerging economies are also supporting market expansion.

By Application

On the basis of application, the Advanced Surgical Market (Secondary Segment) is segmented into general surgery, cardiovascular surgery, orthopedic surgery, and neurological surgery. The Cardiovascular Surgery segment dominated the market with a 36.84% revenue share in 2025, driven by the high global burden of cardiovascular diseases, which account for nearly 17.9 million deaths annually according to global health statistics. Increasing prevalence of coronary artery disease, heart failure, and valvular disorders is significantly driving surgical demand. Hospitals are increasingly performing bypass surgeries, angioplasty support procedures, and valve replacements using advanced surgical systems. The integration of minimally invasive cardiac surgery and hybrid operating rooms is improving procedural efficiency and patient outcomes. In addition, rising geriatric population globally is increasing cardiovascular surgical volumes. Strong adoption of image-guided surgical tools and robotic assistance is further strengthening segment dominance.

The Neurological Surgery segment is expected to witness the fastest CAGR of 8.1% from 2026 to 2033, driven by rising cases of brain tumors, spinal cord injuries, epilepsy, and neurovascular disorders. Increasing adoption of advanced neuronavigation systems, intraoperative MRI, and robotic-assisted neurosurgical tools is significantly improving surgical precision. AI-powered imaging and real-time brain mapping technologies are enhancing decision-making during complex procedures. The growing burden of neurological disorders due to aging populations is further accelerating demand. Hospitals are increasingly investing in specialized neurosurgical centers of excellence. Rising awareness and improved diagnostic capabilities are also increasing early surgical interventions. Expanding healthcare infrastructure in Asia-Pacific and the Middle East is further supporting rapid growth.

Advanced Surgical Market (Secondary Segment) Regional Analysis

North America dominated the Advanced Surgical Market (Secondary Segment) and accounted for the largest revenue share of 39.12% in 2025, supported by advanced healthcare infrastructure, high adoption of robotic-assisted and minimally invasive surgical technologies, strong presence of leading medical device companies, and well-established surgical training systems. The region benefits from a high volume of complex surgical procedures across cardiovascular, orthopedic, and oncology specialties, which drives consistent demand for advanced surgical platforms. Favorable reimbursement frameworks and strong insurance coverage further support patient access to high-cost surgical procedures. In addition, rapid integration of AI-powered imaging, robotic navigation systems, and digital operating rooms is transforming surgical precision and workflow efficiency. The presence of major players such as Medtronic, Intuitive Surgical, and Johnson & Johnson strengthens technological innovation and adoption rates. Continuous investment in surgical robotics and hybrid operating rooms is improving clinical outcomes. High awareness among healthcare professionals and early adoption of next-generation surgical technologies further reinforce North America’s leadership in the global market.

U.S. Advanced Surgical Market (Secondary Segment) Insight

The U.S. Advanced Surgical Market (Secondary Segment) is witnessing strong growth due to rising burden of chronic diseases such as cardiovascular disorders, cancer, and neurological conditions, which significantly increase surgical volumes. The country’s mature healthcare system and strong hospital infrastructure enable rapid adoption of robotic-assisted surgical systems and minimally invasive procedures. Increasing use of AI-powered surgical planning, real-time imaging, and navigation technologies is enhancing procedural accuracy and reducing complications. Hospitals and ambulatory surgical centers are increasingly investing in digital operating rooms and hybrid surgical suites. Strong presence of global medical device manufacturers is accelerating innovation and technology penetration. In addition, favorable reimbursement policies and increasing patient preference for minimally invasive procedures are further driving market growth across the U.S.

Europe Advanced Surgical Market (Secondary Segment) Insight

The Europe Advanced Surgical Market (Secondary Segment) remains a major contributor to global revenue, driven by strong public healthcare systems, rising demand for advanced surgical procedures, and high adoption of minimally invasive technologies. Countries such as Germany, France, and the U.K. are leading in robotic-assisted surgery adoption and surgical innovation. The region benefits from strict regulatory standards that ensure high-quality surgical care and patient safety. Increasing investments in hospital modernization and digital operating rooms are supporting market expansion. Growing geriatric population is further increasing demand for complex surgical interventions. In addition, strong collaboration between academic institutions and medical device companies is accelerating surgical technology development across Europe.

U.K. Advanced Surgical Market (Secondary Segment) Insight

The U.K. Advanced Surgical Market (Secondary Segment) is experiencing steady growth, supported by rising adoption of minimally invasive and robotic-assisted surgical procedures across NHS and private hospitals. Increasing investment in surgical innovation hubs and training programs is enhancing surgeon expertise and procedural efficiency. The country is also witnessing growing adoption of AI-assisted imaging and navigation systems in operating rooms. Demand for faster recovery and reduced hospital stays is driving minimally invasive surgery uptake. In addition, expansion of specialized surgical centers is improving access to advanced procedures. Continuous digital transformation of healthcare infrastructure is further strengthening market growth in the U.K.

Germany Advanced Surgical Market (Secondary Segment) Insight

The Germany Advanced Surgical Market (Secondary Segment) is expanding steadily due to the country’s strong medical technology ecosystem, advanced hospital infrastructure, and leadership in surgical robotics innovation. High adoption of minimally invasive and image-guided surgical systems is improving surgical precision and patient outcomes. Germany’s strong focus on research and development is accelerating innovation in robotic-assisted surgical platforms. Hospitals are increasingly integrating AI-based imaging and navigation systems into operating rooms. Rising demand for orthopedic and cardiovascular surgeries is further driving market growth. In addition, strong government support for healthcare modernization is reinforcing Germany’s position as a key surgical technology hub in Europe.

Asia-Pacific Advanced Surgical Market (Secondary Segment) Insight

The Asia-Pacific Advanced Surgical Market (Secondary Segment) is expected to witness rapid growth, driven by improving healthcare infrastructure, rising healthcare expenditure, and increasing prevalence of chronic diseases. Countries such as China, India, and Japan are investing heavily in modernizing hospital facilities and expanding surgical care capabilities. Growing adoption of minimally invasive and robotic-assisted surgeries is significantly improving treatment outcomes. Increasing patient awareness and demand for advanced surgical procedures are further supporting market expansion. In addition, government initiatives to strengthen healthcare access and expand insurance coverage are boosting surgical procedure volumes. Rapid urbanization and expansion of private healthcare providers are also contributing to regional growth.

Japan Advanced Surgical Market (Secondary Segment) Insight

The Japan Advanced Surgical Market (Secondary Segment) is witnessing consistent growth due to strong adoption of advanced surgical robotics, precision medicine, and minimally invasive techniques. The country’s aging population is significantly increasing demand for cardiovascular, orthopedic, and neurological surgeries. Hospitals are increasingly integrating AI-assisted surgical navigation and high-definition imaging systems. Strong focus on surgical precision and patient safety is driving early adoption of innovative technologies. In addition, Japan’s advanced medical device manufacturing ecosystem supports continuous innovation in surgical systems. Growing use of robotic-assisted surgery is further enhancing clinical outcomes across major hospitals.

China Advanced Surgical Market (Secondary Segment) Insight

The China Advanced Surgical Market (Secondary Segment) is growing rapidly, driven by rising healthcare investments, increasing surgical volumes, and expanding hospital infrastructure. The country is witnessing strong adoption of minimally invasive and robotic-assisted surgical procedures across major urban hospitals. Government initiatives to modernize healthcare facilities and improve surgical capabilities are accelerating market growth. Increasing prevalence of chronic diseases such as cancer and cardiovascular disorders is driving demand for advanced surgical interventions. In addition, rising availability of skilled surgeons and expansion of medical training programs are supporting adoption of new technologies. Continuous innovation in domestic medical device manufacturing is further strengthening China’s position as one of the fastest-growing markets globally.

Advanced Surgical Market (Secondary Segment) Share

The driving simulators industry is primarily led by well-established companies, including:

- Medtronic plc (Ireland)

- Johnson & Johnson (U.S.)

- Intuitive Surgical, Inc. (U.S.)

- Stryker Corporation (U.S.)

- GE HealthCare Technologies Inc. (U.S.)

- Siemens Healthineers AG (Germany)

- Karl Storz SE & Co. KG (Germany)

- Olympus Corporation (Japan)

- B. Braun Melsungen AG (Germany)

- Smith & Nephew plc (U.K.)

- Zimmer Biomet Holdings, Inc. (U.S.)

- CONMED Corporation (U.S.)

- Boston Scientific Corporation (U.S.)

- Canon Medical Systems Corporation (Japan)

- Fujifilm Holdings Corporation (Japan)

- Medtronic Surgical Technologies (U.S.)

- Arthrex, Inc. (U.S.)

- Richard Wolf GmbH (Germany)

- Smiths Medical (U.S.)

- MicroPort Scientific Corporation (China)

- Getinge AB (Sweden)

- Karl Storz Endoscopy (Germany)

- Lepu Medical Technology (China)

- Meril Life Sciences Pvt. Ltd. (India)

- TransEnterix (Asensus Surgical) (U.S.)

- Brainlab AG (Germany)

- Corindus Vascular Robotics (U.S.)

- NuVasive, Inc. (U.S.)

- Olympus Medical Systems (Japan)

- Heal Force Bio-Meditech Holdings Limited (China)

Latest Developments in Global Advanced Surgical Market (Secondary Segment)

- In March 2021, NVIDIA Corporation, a global leader in AI computing and graphics technologies, announced the expansion of its NVIDIA DRIVE Sim platform built on Omniverse. The platform was designed to enable highly realistic, physics-based autonomous vehicle simulation using digital twins and AI-generated environments. It allowed automotive OEMs and technology companies to test perception systems, sensor fusion, and autonomous driving algorithms in large-scale virtual scenarios. This development significantly strengthened NVIDIA’s position in the autonomous vehicle simulation ecosystem and accelerated adoption of cloud-based driving simulation technologies

- In November 2021, Applied Intuition Inc., a leading U.S.-based autonomous vehicle simulation software company, announced a major Series D funding round of approximately USD 250 million. The funding was aimed at expanding its simulation and validation platforms used by global automotive OEMs and defense organizations. The company’s software enables large-scale virtual testing of autonomous systems across millions of driving scenarios, reducing dependency on real-world testing. This development highlighted growing investor confidence in simulation-based automotive validation technologies

- In June 2022, AB Dynamics PLC, a UK-based testing and simulation systems provider, completed the acquisition of Ansible Motion, a leading driving simulator manufacturer. The acquisition significantly expanded AB Dynamics’ capabilities in high-fidelity motion simulation systems used for automotive testing, ADAS validation, and motorsport applications. The combined portfolio enabled integration of advanced vehicle dynamics modeling with state-of-the-art simulator hardware. This strategic move strengthened consolidation trends within the global driving simulator market

- In October 2022, Dynisma Ltd., a UK-based high-performance simulation technology company, unveiled its DMG-1 motion simulator, designed for Formula 1 teams, automotive OEMs, and advanced vehicle development programs. The system featured ultra-low latency motion technology and high-fidelity vehicle dynamics replication, enabling extremely realistic driver feedback. The launch marked a major advancement in professional motorsport simulation and automotive R&D applications. This innovation positioned Dynisma as a key competitor in next-generation motion simulator technologies

- In March 2024, NVIDIA Corporation announced major advancements to its DRIVE Sim platform during its GTC conference, introducing enhanced generative AI capabilities and improved sensor simulation accuracy. The updates enabled faster scenario generation, improved perception training for autonomous vehicles, and more scalable simulation environments for OEMs and robotics developers. The integration of AI foundation models into simulation workflows significantly reduced development time for autonomous driving systems. This development reinforced NVIDIA’s leadership in AI-powered driving simulation ecosystems

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.