Global Aerospace And Defense Elastomers Market

Market Size in USD Million

USD

80.24 Million

USD

125.02 Million

2024

2032

USD

80.24 Million

USD

125.02 Million

2024

2032

| 2025 - 2032 | |

| USD 80.24 Million | |

| USD 125.02 Million | |

| % | |

|

What is the Global Aerospace and Defense Elastomers Market Size and Growth Rate?

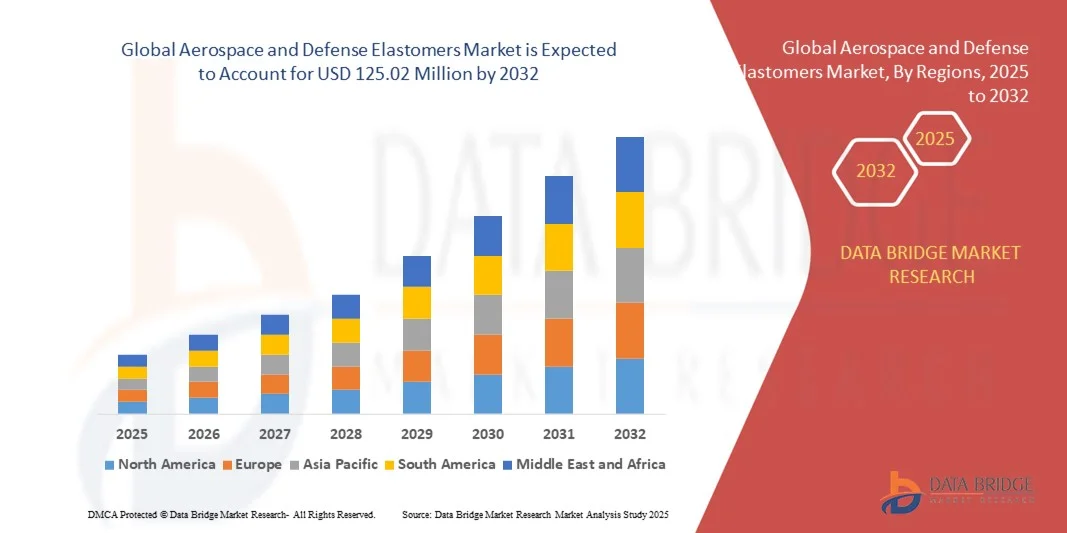

- The global aerospace and defense elastomers market size was valued at USD 80.24 million in 2024 and is expected to reach USD 125.02 million by 2032, at a CAGR of 5.70% during the forecast period

- The growing demand for region and defense elastomers is due to the trend of getting light-weight aircrafts which is able to facilitate impact the market growth

- The increasing focus of region and defense elastomers makers and different market players on enhancing the technologies offered with them is in addition expected to enhance the merchandise quality and offerings commercialized within the market

What are the Major Takeaways of Aerospace and Defense Elastomers Market?

- The high value of raw materials incorporates a negative impact on the expansion of the aerospace and defense elastomers market

- Whereas, rise in usage of private planes and emerging new markets will provide beneficial opportunities for the aerospace and defense elastomers market growth

- North America dominated the aerospace and defense elastomers market with the largest revenue share of 42.1% in 2024, driven by the growing demand for high-performance elastomers in aerospace, defense, and industrial applications

- The Asia-Pacific market is poised to grow at the fastest CAGR of 9.31% during 2025–2032, driven by rising aerospace manufacturing, increasing defense budgets, and rapid industrialization in China, Japan, India, and South Korea

- The EPDM segment dominated the market with the largest revenue share of 38.5% in 2024, driven by its excellent resistance to heat, ozone, and weathering, making it ideal for aerospace seals, gaskets, and insulation applications

Report Scope and Aerospace and Defense Elastomers Market Segmentation

|

Attributes |

Aerospace and Defense Elastomers Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

What is the Key Trend in the Aerospace and Defense Elastomers Market?

Rising Adoption of Lightweight, High-Performance Materials

- A prominent trend in the global aerospace and defense elastomers market is the increasing adoption of lightweight and high-performance elastomeric materials designed to improve fuel efficiency, reduce emissions, and enhance durability in extreme operational environments

- For instance, new fluorosilicone and fluoropolymer elastomers are being used in aircraft seals and gaskets to withstand high temperatures, aggressive chemicals, and harsh mechanical stress, ensuring longer service life and reduced maintenance requirements

- Advanced elastomers are also being tailored for noise, vibration, and harshness (NVH) reduction in aircraft and defense vehicles, helping improve passenger comfort and operational efficiency. High-performance thermoplastic elastomers, for instance, offer superior mechanical resilience while maintaining flexibility and weight savings

- The integration of these materials with additive manufacturing techniques and precision molding allows for customized, lightweight components that meet stringent aerospace and defense standards

- Companies such as Saint-Gobain Performance Plastics and Dow are investing heavily in R&D to develop elastomers that provide superior thermal, chemical, and mechanical resistance while reducing overall system weight

- The rising demand for fuel-efficient, durable, and lightweight elastomer solutions across aerospace and defense platforms is expected to drive innovation and growth in the sector over the forecast period

What are the Key Drivers of Aerospace and Defense Elastomers Market?

- The growing focus on weight reduction and fuel efficiency in aircraft and defense vehicles is a primary driver for the increased demand for advanced elastomers. Lightweight elastomer components contribute directly to reduced operational costs and environmental impact

- For instance, in 2024, Saint-Gobain Performance Plastics introduced a range of elastomeric solutions optimized for high-temperature aircraft engine components, aimed at improving performance and reducing maintenance intervals

- Increasing adoption of next-generation military vehicles, unmanned aerial systems, and spacecraft requires elastomers that withstand extreme environmental conditions such as high heat, UV radiation, and chemical exposure

- The demand for longer lifecycle components and lower maintenance costs is pushing manufacturers to replace conventional materials with high-performance elastomers that offer superior durability and reliability

- The trend toward customized, application-specific elastomers, coupled with technological advancements in elastomer chemistry and processing, is further supporting market growth across aerospace and defense segments

Which Factor is Challenging the Growth of the Aerospace and Defense Elastomers Market?

- High development and material costs for advanced elastomers can limit adoption, especially for small- and medium-scale aerospace manufacturers. Premium materials such as fluorosilicones and fluoropolymers are significantly more expensive than traditional rubber or polymer alternatives

- Stringent regulatory and certification requirements for aerospace and defense components can extend development timelines and increase costs, deterring some manufacturers from switching to newer elastomer solutions

- Technical complexity in manufacturing and integration of high-performance elastomers may require specialized equipment, expertise, and testing, which increases operational and production costs

- Volatility in raw material prices can impact the overall cost structure for elastomer manufacturers, affecting pricing and adoption in cost-sensitive projects

- Overcoming these challenges requires enhanced R&D investment, material innovation, and collaboration with aerospace and defense OEMs to develop cost-effective, high-performance elastomer solutions that meet stringent performance and certification standards

How is the Aerospace and Defense Elastomers Market Segmented?

The market is segmented on the basis of type and application.

- By Type

On the basis of type, the aerospace and defense elastomers market is segmented into EPDM, fluoroelastomers, silicone elastomers, and others. The EPDM segment dominated the market with the largest revenue share of 38.5% in 2024, driven by its excellent resistance to heat, ozone, and weathering, making it ideal for aerospace seals, gaskets, and insulation applications. EPDM is widely used in aircraft and defense vehicles for its durability and cost-effectiveness, as well as its ability to maintain flexibility across a broad temperature range. The fluoroelastomers segment is anticipated to witness the fastest CAGR of 22.3% from 2025 to 2032, fueled by the growing demand for high-performance applications requiring superior chemical, fuel, and thermal resistance. Fluoroelastomers are increasingly adopted in advanced aerospace engines, fuel systems, and defense components, providing long-term reliability in harsh environments. The trend toward lightweight, high-performance materials is further supporting growth across both segments.

- By Application

On the basis of application, the aerospace and defense elastomers market is segmented into O-rings & gaskets, seals, profiles, hoses, and others. The O-rings & gaskets segment held the largest market revenue share of 41.7% in 2024, attributed to their critical role in ensuring airtight and fluid-tight sealing in aerospace engines, hydraulic systems, and fuel systems. The segment’s dominance is reinforced by stringent safety and reliability standards in both commercial and defense aircraft, making O-rings and gaskets essential components. The seals segment is expected to witness the fastest CAGR of 23.1% from 2025 to 2032, driven by the increasing use of high-performance elastomers in dynamic sealing applications such as landing gear, actuators, and aircraft doors. The rising demand for lightweight, durable, and chemically resistant sealing solutions across aerospace and defense platforms is propelling adoption, particularly in next-generation aircraft and military systems.

Which Region Holds the Largest Share of the Aerospace and Defense Elastomers Market?

- North America dominated the aerospace and defense elastomers market with the largest revenue share of 42.1% in 2024, driven by the growing demand for high-performance elastomers in aerospace, defense, and industrial applications

- Manufacturers and end-users in the region highly value the superior durability, chemical resistance, and thermal stability offered by aerospace-grade elastomers, which are critical for safety and reliability in aircraft, defense vehicles, and industrial systems

- This widespread adoption is further supported by the presence of major aerospace and defense companies, high investment in R&D, and stringent safety regulations, establishing North America as a leader in advanced elastomer consumption

U.S. Aerospace and Defense Elastomers Market Insight

The U.S. market captured the largest revenue share of 82% in 2024 within North America, fueled by the strong presence of aircraft manufacturers, defense contractors, and a focus on technologically advanced materials. The demand for lightweight, high-performance elastomers in seals, gaskets, hoses, and O-rings is expanding due to stringent regulatory standards and growing aerospace production. Moreover, government defense spending, coupled with modernization programs in military aircraft and vehicles, is significantly propelling market growth.

Europe Aerospace and Defense Elastomers Market Insight

The Europe market is projected to expand at a substantial CAGR during the forecast period, primarily driven by the adoption of high-performance elastomers in aerospace and defense sectors. The demand is supported by strict safety standards, increasing urbanization, and rising focus on eco-friendly, durable materials. Germany, France, and the U.K. are key contributors, with significant growth across aircraft production, industrial applications, and military systems.

U.K. Aerospace and Defense Elastomers Market Insight

The U.K. market is anticipated to grow at a noteworthy CAGR, fueled by ongoing investments in defense modernization and aircraft manufacturing. The country’s emphasis on innovation and regulatory compliance drives adoption, particularly in seals, hoses, and gaskets for both civil and military aviation applications.

Germany Aerospace and Defense Elastomers Market Insight

Germany’s market is expected to expand at a considerable CAGR, driven by the integration of high-performance elastomers in advanced industrial and aerospace systems. Strong infrastructure, focus on technological advancement, and sustainable manufacturing practices are accelerating demand in commercial and defense sectors.

Which Region is the Fastest Growing Region in the Aerospace and Defense Elastomers Market?

The Asia-Pacific market is poised to grow at the fastest CAGR of 9.31% during 2025–2032, driven by rising aerospace manufacturing, increasing defense budgets, and rapid industrialization in China, Japan, India, and South Korea. The growing adoption of high-performance elastomers in aircraft, defense vehicles, and industrial machinery, supported by local manufacturing hubs, is expanding market accessibility and affordability.

Japan Aerospace and Defense Elastomers Market Insight

Japan’s market is gaining momentum due to high-tech manufacturing, urbanization, and demand for durable, lightweight elastomers in civil and defense aircraft. Adoption is further supported by integration with advanced industrial systems and a focus on long-term reliability.

China Aerospace and Defense Elastomers Market Insight

China accounted for the largest revenue share in the APAC region in 2024, attributed to rapid industrial growth, expanding middle-class infrastructure, and increasing domestic aerospace and defense production. Government initiatives promoting high-quality, durable materials and smart industrial manufacturing are key factors propelling market growth.

Which are the Top Companies in Aerospace and Defense Elastomers Market?

The aerospace and defense elastomers industry is primarily led by well-established companies, including:

- Trelleborg (Sweden)

- Shin-Etsu Chemical Co., Ltd. (Japan)

- Dow (U.S.)

- The Chemours Company (U.S.)

- Momentive (U.S.)

- Saint-Gobain Performance Plastics (France)

- Solvay (Belgium)

- LANXESS (Germany)

- Esterline Technologies Corporation (U.S.)

- 3M (U.S.)

- Holland Shielding Systems BV (Netherlands)

- Jonal Laboratories Inc. (U.S.)

- PolyMod Technologies (U.S.)

- CHT R. Beitlich GmbH |CHT Group (Germany)

- Rogers Corporation (U.S.)

- Seal Science, Inc. (U.S.)

- Transdigm Group, Inc. (U.S.)

- TECHNETICS GROUP (U.S.)

- Zeon Chemicals L.P. (U.S.)

- PARKER HANNIFIN CORP (U.S.)

What are the Recent Developments in Global Aerospace and Defense Elastomers Market?

- In February 2025, DuPont and Rogers Corporation began exploring eco-friendly elastomer solutions, aligning with the growing trend toward sustainable manufacturing processes in the aerospace and defense industries, marking a significant step toward greener materials adoption

- In January 2025, Huntsman and Wacker Chemie entered into strategic alliances to expand their product portfolios and enhance market reach in the aerospace and defense elastomers sector, strengthening their position in the global market and enabling collaborative innovation

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Aerospace And Defense Elastomers Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Aerospace And Defense Elastomers Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Aerospace And Defense Elastomers Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.