Global Aerospace High Performance Alloys Market

Market Size in USD Billion

USD

14.59 Billion

USD

26.03 Billion

2025

2033

USD

14.59 Billion

USD

26.03 Billion

2025

2033

| 2026 - 2033 | |

| USD 14.59 Billion | |

| USD 26.03 Billion | |

| % | |

|

Aerospace High-Performance Alloys Market Size

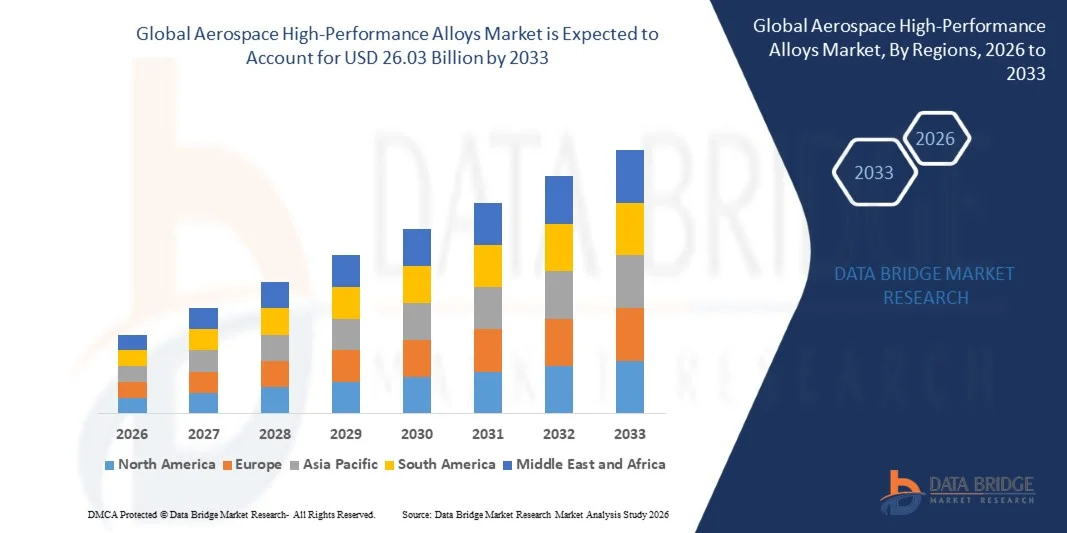

- The global aerospace high-performance alloys market size was valued at USD 14.59 billion in 2025 and is expected to reach USD 26.03 billion by 2033, at a CAGR of 7.50% during the forecast period

- The market growth is largely fuelled by increasing demand for lightweight, high-strength materials in commercial and military aircraft

- Rising adoption of advanced alloys in turbine engines, airframes, and structural components is further supporting market expansion

Aerospace High-Performance Alloys Market Analysis

- Aerospace high-performance alloys are increasingly utilized in aircraft, spacecraft, and defense applications due to their superior strength-to-weight ratio and thermal resistance

- The market is driven by growing aircraft production, modernization of defense fleets, and the need for fuel-efficient and high-performance aerospace components

- North America dominated the aerospace high-performance alloys market with the largest revenue share of 38.75% in 2025, driven by a strong presence of aerospace manufacturers, increased aircraft production, and advanced research in high-performance materials

- Asia-Pacific region is expected to witness the highest growth rate in the global aerospace high-performance alloys market, driven by rising commercial aircraft production, expansion of defense programs, government initiatives supporting aerospace manufacturing, and increasing adoption of advanced high-performance materials

- The Nickel Base segment held the largest market revenue share in 2025, driven by its exceptional high-temperature strength, corrosion resistance, and widespread application in jet engines, gas turbines, and structural components. Nickel-based alloys are preferred for critical aerospace applications where durability and performance under extreme conditions are paramount. In addition, ongoing R&D efforts are focused on enhancing creep resistance and oxidation performance, further strengthening the segment’s dominance. The growing demand for commercial and military aircraft is also supporting the sustained adoption of nickel-based alloys across the aerospace industry

Report Scope and Aerospace High-Performance Alloys Market Segmentation

|

Attributes |

Aerospace High-Performance Alloys Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

• Aperam (Luxembourg) |

|

Market Opportunities |

• Rising Demand For Lightweight And Fuel-Efficient Aircraft Components |

|

Value Added Data Infosets |

In addition to the market insights such as market value, growth rate, market segments, geographical coverage, market players, and market scenario, the market report curated by the Data Bridge Market Research team includes in-depth expert analysis, import/export analysis, pricing analysis, production consumption analysis, and pestle analysis. |

Aerospace High-Performance Alloys Market Trends

“Rising Demand for Lightweight and Fuel-Efficient Aircraft Components”

• The growing focus on lightweight, high-strength, and corrosion-resistant materials is significantly shaping the aerospace high-performance alloys market, as manufacturers increasingly prefer alloys that improve aircraft performance, fuel efficiency, and durability. High-performance alloys are gaining traction due to their ability to withstand extreme temperatures, reduce structural weight, and maintain mechanical integrity, strengthening their adoption across commercial, military, and space applications

• Increasing awareness around environmental regulations, fuel efficiency, and aircraft longevity has accelerated the demand for high-performance alloys in turbine engines, airframes, landing gear, and structural components. Aerospace OEMs and defense manufacturers are actively seeking alloys that enhance operational efficiency, reduce maintenance costs, and extend product lifecycle, prompting collaborations between material suppliers and aerospace integrators

• Sustainability and performance standards are influencing procurement decisions, with manufacturers emphasizing material certifications, traceability, and compliance with aerospace regulations. These factors help aerospace companies differentiate products in a competitive market and ensure safety, while driving adoption of advanced metallurgical processes and alloy innovations

• For instance, in 2024, Boeing in the U.S. and Airbus in France expanded their aircraft production programs by incorporating titanium and nickel-based high-performance alloys in airframes and engine components. These deployments were introduced in response to growing demand for fuel-efficient, durable aircraft, with applications spanning commercial jets, military aircraft, and space launch vehicles. The alloys also contributed to weight reduction and improved operational efficiency

• While demand for aerospace high-performance alloys is rising, sustained market expansion depends on continuous R&D, cost-effective production, and meeting stringent performance and safety standards. Manufacturers are also focusing on improving supply chain resilience, alloy processing technologies, and developing innovative solutions that balance cost, performance, and regulatory compliance for broader adoption

Aerospace High-Performance Alloys Market Dynamics

Driver

“Rising Demand for Lightweight and Corrosion-Resistant Materials”

• The increasing demand for lightweight, high-strength materials is a major driver for the aerospace high-performance alloys market. Manufacturers are progressively replacing conventional metals with advanced titanium, nickel, and aluminum-based alloys to improve fuel efficiency, reduce aircraft weight, and meet stringent performance standards. This trend is also fostering research into novel alloy compositions and additive manufacturing processes

• Expanding applications in turbine engines, airframes, landing gear, and spacecraft structures are influencing market growth. High-performance alloys enhance strength, thermal stability, and corrosion resistance while maintaining structural integrity under extreme conditions, enabling aerospace companies to meet operational efficiency and safety requirements. The growing defense and space exploration programs globally further reinforce this trend

• Aerospace OEMs and component suppliers are actively promoting high-performance alloy-based solutions through engineering innovations, collaborative R&D, and compliance with aviation and defense standards. These efforts are supported by the growing focus on fuel efficiency, durability, and reduced maintenance costs, and they also encourage partnerships between material manufacturers and aircraft integrators

• For instance, in 2023, Lockheed Martin in the U.S. and Safran in France reported increased utilization of titanium and nickel alloys in military aircraft and helicopter programs. This adoption followed rising demand for lightweight, durable, and fuel-efficient aerospace components, driving product differentiation and operational advantages. Both companies also emphasized regulatory compliance and traceability in material sourcing to strengthen reliability and market credibility

• Although the rising demand for high-performance alloys supports growth, wider adoption depends on cost optimization, raw material availability, and scalable production processes. Investment in supply chain efficiency, sustainable extraction, and advanced metallurgical technologies will be critical for meeting global aerospace demand and maintaining competitive advantage

Restraint/Challenge

“High Production Costs and Complex Manufacturing Processes”

• The relatively high cost of aerospace high-performance alloys compared to conventional metals remains a key challenge, limiting adoption among cost-sensitive projects. High raw material costs, complex alloying, and intricate processing methods contribute to elevated pricing. In addition, fluctuations in the availability of titanium, nickel, and specialty aluminum alloys can affect supply stability and market penetration

• Awareness and technical expertise are uneven across emerging markets, where adoption of advanced alloys is still limited. Lack of understanding of alloy properties, processing requirements, and certification standards restricts usage in certain aerospace applications. This also slows innovation uptake in regions with limited access to metallurgical training and infrastructure

• Manufacturing and supply chain challenges also impact market growth, as high-performance alloys require specialized equipment, precision machining, and strict quality control. Logistical complexities and long lead times increase operational costs. Companies must invest in skilled labor, advanced facilities, and quality management systems to maintain material integrity

• For instance, in 2024, aerospace suppliers in India and Brazil reported slower uptake of titanium and nickel-based alloys due to higher prices, limited local expertise, and infrastructure constraints. These factors also prompted some aircraft manufacturers to rely on imports for high-performance components, affecting production timelines and cost efficiency

• Overcoming these challenges will require cost-efficient alloy production, advanced manufacturing technologies, and focused technical training for engineers and manufacturers. Collaboration with certification bodies, aerospace OEMs, and suppliers can help unlock the long-term growth potential of the global aerospace high-performance alloys market. Developing cost-competitive alloy solutions while maintaining performance, safety, and regulatory compliance will be essential for widespread adoption

Aerospace High-Performance Alloys Market Scope

The market is segmented on the basis of product type, alloy type, and alloying element

• By Product Type

On the basis of product type, the global aerospace high-performance alloys market is segmented into Iron Base, Cobalt Base, and Nickel Base. The Nickel Base segment held the largest market revenue share in 2025, driven by its exceptional high-temperature strength, corrosion resistance, and widespread application in jet engines, gas turbines, and structural components. Nickel-based alloys are preferred for critical aerospace applications where durability and performance under extreme conditions are paramount. In addition, ongoing R&D efforts are focused on enhancing creep resistance and oxidation performance, further strengthening the segment’s dominance. The growing demand for commercial and military aircraft is also supporting the sustained adoption of nickel-based alloys across the aerospace industry.

The Cobalt Base segment is expected to witness the fastest growth rate from 2026 to 2033, driven by its superior wear resistance, thermal stability, and ability to maintain mechanical properties at elevated temperatures. Cobalt-based alloys are increasingly adopted in turbine blades, bearings, and other aerospace components that require both strength and longevity in demanding environments. In addition, advances in alloying techniques and powder metallurgy are enabling the production of complex cobalt-based components with improved performance. The rising focus on next-generation propulsion systems and high-performance jet engines is further fueling the adoption of cobalt alloys.

• By Alloy Type

On the basis of alloy type, the market is segmented into Wrought Alloy and Cast Alloy. The Wrought Alloy segment dominated the market in 2025 due to its enhanced mechanical properties, uniform microstructure, and versatility in fabrication processes, making it suitable for airframe components and high-stress applications. Wrought alloys also allow for precision shaping, improved toughness, and excellent fatigue resistance, which are critical for aerospace safety standards. The ongoing emphasis on lightweight yet strong materials in aircraft manufacturing further drives the preference for wrought alloys.

The Cast Alloy segment is expected to witness the fastest growth from 2026 to 2033, as casting allows for complex geometries and reduces manufacturing costs for intricate engine components, such as turbine blades and combustion chambers. Cast alloys are increasingly adopted for high-performance engine parts, enabling manufacturers to achieve designs that are difficult or uneconomical with wrought processing. In addition, advancements in precision casting and additive manufacturing techniques are enhancing material performance and component reliability.

• By Alloying Element

On the basis of alloying element, the market is segmented into Aluminum, Titanium, Magnesium, and Others. The Titanium segment held a major market share in 2025, owing to its high strength-to-weight ratio, corrosion resistance, and increasing use in structural components and engine parts to improve fuel efficiency and overall aircraft performance. Titanium alloys also offer superior fatigue resistance, which is essential for high-cycle aerospace components. Rising adoption in both commercial and military aircraft, coupled with cost reductions in titanium production, supports its continued dominance.

The Aluminum segment is expected to witness the fastest growth from 2026 to 2033, driven by its lightweight properties, ease of fabrication, and growing adoption in airframes and fuselage components to meet the demand for lighter, more fuel-efficient aircraft. Aluminum alloys are also increasingly integrated into hybrid material systems with composites to optimize performance. In addition, innovations in high-strength aluminum alloys are enabling aerospace manufacturers to reduce overall aircraft weight without compromising structural integrity.

Aerospace High-Performance Alloys Market Regional Analysis

• North America dominated the aerospace high-performance alloys market with the largest revenue share of 38.75% in 2025, driven by a strong presence of aerospace manufacturers, increased aircraft production, and advanced research in high-performance materials

• The region’s aerospace industry extensively adopts nickel, titanium, and aluminum alloys in engines, airframes, and structural components due to their high strength-to-weight ratios and corrosion resistance

• High investment in R&D, coupled with technologically advanced manufacturing facilities and stringent safety standards, is further supporting the growth of aerospace high-performance alloys in both commercial and defense applications

U.S. Aerospace High-Performance Alloys Market Insight

The U.S. aerospace high-performance alloys market captured the largest revenue share in 2025 within North America, fueled by rising commercial aircraft production and a robust defense sector. Manufacturers are increasingly focusing on lightweight, high-strength alloys to enhance fuel efficiency and aircraft performance. The growing adoption of additive manufacturing and precision casting technologies, combined with demand for nickel-based and titanium alloys, is significantly propelling market growth. In addition, government initiatives promoting innovation in aerospace materials are further supporting market expansion.

Europe Aerospace High-Performance Alloys Market Insight

The Europe aerospace high-performance alloys market is expected to witness the fastest growth rate from 2026 to 2033, driven by increasing investments in next-generation aircraft and stringent environmental regulations. The rising emphasis on lightweight, fuel-efficient materials and the adoption of titanium and aluminum alloys are fostering market demand. Europe’s established aerospace manufacturers, coupled with research collaborations and sustainability initiatives, are boosting the integration of high-performance alloys in both civil and defense aircraft.

U.K. Aerospace High-Performance Alloys Market Insight

The U.K. aerospace high-performance alloys market is expected to witness rapid growth from 2026 to 2033, driven by strong defense programs, expansion of commercial aerospace manufacturing, and increased R&D in alloy technology. The demand for corrosion-resistant, high-strength alloys for airframes and engines is supporting market adoption. Furthermore, the U.K.’s strategic focus on lightweight materials and precision engineering is encouraging the use of wrought and cast high-performance alloys across multiple aerospace applications.

Germany Aerospace High-Performance Alloys Market Insight

The Germany aerospace high-performance alloys market is expected to witness considerable growth from 2026 to 2033, fueled by technological advancements, innovation in additive manufacturing, and the country’s emphasis on sustainability. Germany’s robust aerospace industry prioritizes the use of titanium and nickel-based alloys in critical engine components and structural applications. The increasing demand for fuel-efficient aircraft and adoption of hybrid material systems is further enhancing market penetration.

Asia-Pacific Aerospace High-Performance Alloys Market Insight

The Asia-Pacific aerospace high-performance alloys market is expected to witness significant growth from 2026 to 2033, driven by rapid expansion in aircraft production, urbanization, and rising investments in commercial and defense aerospace sectors in countries such as China, India, and Japan. The growing focus on lightweight, high-strength alloys, supported by government initiatives and domestic manufacturing capabilities, is boosting market adoption. In addition, increased collaborations with global aerospace companies and the rising demand for regional air travel are further fueling market growth.

Japan Aerospace High-Performance Alloys Market Insight

The Japan aerospace high-performance alloys market is expected to witness steady growth from 2026 to 2033 due to the country’s high-tech manufacturing capabilities, focus on precision engineering, and demand for lightweight, high-performance materials. The adoption of titanium and aluminum alloys in airframes and engine components is driving market expansion. Furthermore, Japan’s emphasis on advanced research and integration of alloys in smart manufacturing processes is supporting sustained growth in the aerospace sector.

China Aerospace High-Performance Alloys Market Insight

The China aerospace high-performance alloys market accounted for the largest revenue share in Asia-Pacific in 2025, attributed to the country’s rapidly expanding commercial aircraft production, growing defense programs, and high adoption of advanced materials. China’s investment in next-generation aerospace technologies and local manufacturing of nickel, titanium, and aluminum alloys are key factors driving market growth. In addition, government initiatives promoting self-reliance in aerospace materials and the rising middle-class demand for air travel are accelerating market expansion.

Aerospace High-Performance Alloys Market Share

The Aerospace High-Performance Alloys industry is primarily led by well-established companies, including:

• Aperam (Luxembourg)

• Alcoa Corporation (U.S.)

• CRS Holdings Inc. (U.S.)

• Outokumpu (Finland)

• Precision Castparts Corp. (U.S.)

• THE TIMKEN COMPANY (U.S.)

• VSMPO-AVISMA Corporation (Russia)

• Wall Colmonoy (U.S.)

• Materion Corporation (U.S.)

• Sandvik AB (Sweden)

• HAYNES INTERNATIONAL (U.S.)

• Hitachi Metals, Ltd. (Japan)

• Stanford Advanced Materials (U.S.)

• AMG Advanced Metallurgical Group N.V. (Netherlands)

• Arconic (U.S.)

• Nippon Yakin Kogyo Co. Ltd. (Japan)

• High Performance Alloys, Inc. (U.S.)

• eramet (France)

• Glencore (Switzerland)

• Constellium (France)

Latest Developments in Global Aerospace High-Performance Alloys Market

- In March 2025, Arconic, opened a new research and development center in Ohio, focused on lightweight, high-strength aerospace alloys. The center aims to accelerate product innovation, enhance collaboration with aerospace and defense customers, and develop next-generation materials. This initiative strengthens Arconic’s competitive position, enables faster adoption of advanced alloys, and supports growth in both commercial and military aircraft sectors

- In April 2025, VSMPO-AVISMA, signed a long-term titanium supply agreement with Embraer, securing a stable supply of high-performance titanium alloys for commercial and executive jets. The deal ensures continuity in aircraft production, supports Embraer’s expansion plans, and reinforces VSMPO-AVISMA’s presence in the global aerospace supply chain. It also positions the company to benefit from increasing demand for durable, lightweight materials

- In May 2025, Allegheny Technologies Incorporated (ATI), launched a new powder metallurgy-based alloy designed for hypersonic aerospace applications. The alloy provides superior thermal resistance and mechanical strength, enabling next-generation aerospace vehicles to withstand extreme conditions. This innovation enhances ATI’s market competitiveness and strengthens its role as a supplier of advanced, high-performance aerospace materials

- In June 2025, Safran, acquired a minority stake in a European startup developing recyclable aerospace alloys. This strategic investment promotes sustainability, accelerates the development of eco-friendly high-performance materials, and enhances Safran’s portfolio in the aerospace supply chain. The move aligns with industry trends toward greener aviation and positions Safran as a forward-looking innovator

- In August 2024, Spirit AeroSystems, expanded its Wichita, Kansas facility for advanced alloy component production. The expansion increases capacity for manufacturing high-performance components used in both commercial and military aircraft. It improves supply chain efficiency, meets growing industry demand, and reinforces Spirit AeroSystems’ role as a leading supplier of critical aerospace components

- In September 2024, Hexcel Corporation, introduced a new carbon fiber-reinforced high-performance alloy for aerospace structures. The material enhances strength-to-weight ratios, improves fuel efficiency, and is designed for adoption in primary airframe components. This launch supports Hexcel’s market growth and positions the company to meet rising demand for lightweight, high-performance materials

- In October 2024, GE Aerospace and Safran, extended their CFM International partnership with a focus on co-developing advanced high-performance alloys for next-generation LEAP and RISE engines. The collaboration aims to improve engine efficiency, durability, and overall performance, while strengthening innovation in alloy technology. The partnership reinforces both companies’ leadership in advanced aerospace propulsion systems

- In November 2024, Carpenter Technology Corporation, opened a state-of-the-art additive manufacturing facility in Pennsylvania dedicated to aerospace alloys. The facility enables production of complex, high-performance materials for next-generation aircraft, reduces lead times, and meets growing industry demand. This move enhances Carpenter Technology’s innovation capabilities and strengthens its market presence in aerospace materials

- In December 2024, Allegheny Technologies Incorporated (ATI), secured a multi-year contract with Boeing to supply high-performance titanium alloys for commercial and defense aircraft. The agreement reinforces ATI’s position as a key aerospace supplier, ensures long-term revenue stability, and supports Boeing’s aircraft production with reliable, advanced materials. It also highlights the growing demand for durable, lightweight alloys in aerospace

- In January 2024, Rolls-Royce, launched a proprietary high-temperature nickel alloy for jet engines. The alloy improves fuel efficiency, durability, and performance in the latest engine models. By enhancing engine longevity and reducing operational costs, this innovation strengthens Rolls-Royce’s competitive advantage and addresses market demand for high-performance propulsion materials

- In February 2024, Precision Castparts Corp., won a $300 million contract to supply superalloy turbine components for the Airbus A350 program. The contract expands the company’s presence in the European aerospace supply chain, supports large-scale aircraft production, and reinforces its reputation as a key supplier of critical high-performance components

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.