Global Aerospace Sealant Market

Market Size in USD Billion

USD

1.54 Billion

USD

2.50 Billion

2024

2032

USD

1.54 Billion

USD

2.50 Billion

2024

2032

| 2025 - 2032 | |

| USD 1.54 Billion | |

| USD 2.50 Billion | |

| % | |

|

Aerospace Sealant Market Size

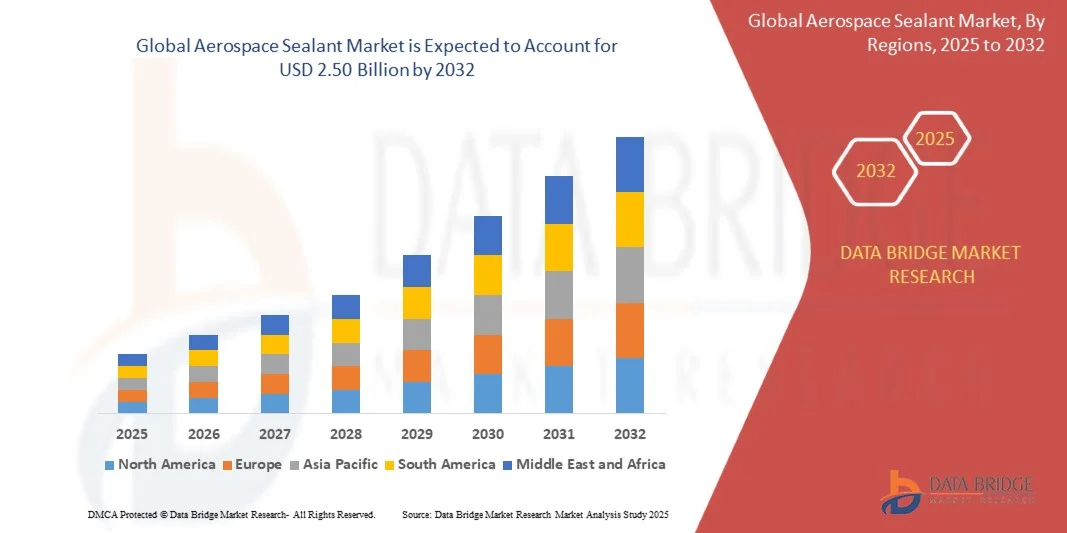

- The global aerospace sealant market size was valued at USD 1.54 billion in 2024 and is expected to reach USD 2.50 billion by 2032, at a CAGR of 6.25% during the forecast period

- The market growth is largely fuelled by the rising demand for corrosion-resistant and lightweight materials in commercial and military aircraft, as well as increasing aerospace manufacturing activities globally

- Growing emphasis on aircraft safety, durability, and maintenance efficiency is driving adoption of advanced sealants across airframes, fuselage panels, and critical joints

Aerospace Sealant Market Analysis

- The aerospace sealant market is witnessing significant innovation in sealant formulations, including high-temperature resistance, improved adhesion, and faster curing times

- Demand for environmentally friendly and low-VOC sealants is increasing, driven by stricter environmental regulations and sustainability initiatives in the aerospace industry

- North America dominated the aerospace sealant market with the largest revenue share of 38.50% in 2024, driven by a strong aerospace and defense industry, increasing aircraft production, and rising demand for maintenance, repair, and overhaul (MRO) services. The region’s well-established aviation ecosystem and advanced manufacturing infrastructure support the adoption of high-performance sealants

- Asia-Pacific region is expected to witness the highest growth rate in the global aerospace sealant market, driven by rapid urbanization, increasing aircraft deliveries, growth in low-cost carriers, and rising demand for MRO services in emerging economies

- The polysulfide segment held the largest market revenue share in 2024, driven by its excellent flexibility, chemical resistance, and long-term durability in high-stress aircraft applications. Polysulfide sealants are widely used in fuel tanks, fuselage joints, and wing assemblies, offering superior performance under extreme temperatures and environmental conditions

Report Scope and Aerospace Sealant Market Segmentation

|

Attributes |

Aerospace Sealant Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Aerospace Sealant Market Trends

“Increasing Adoption of Advanced Sealants in Aircraft Manufacturing and Maintenance”

- The growing shift toward advanced aerospace sealants is transforming the aviation landscape by providing superior corrosion protection, joint sealing, and thermal resistance. These sealants enable enhanced airframe durability and fuel efficiency, especially in commercial and military aircraft, reducing maintenance costs and improving operational performance. In addition, the use of high-performance sealants minimizes downtime during routine inspections and enhances aircraft reliability, supporting long-term operational efficiency

- Rising demand for lightweight and high-performance sealants is accelerating the adoption of silicone-based, polyurethane, and polysulfide formulations. These materials are particularly effective in high-stress areas such as fuselage joints, wing panels, and engine compartments, ensuring structural integrity and compliance with stringent aviation standards. The adoption of these sealants also contributes to extended service intervals and reduced environmental impact due to longer-lasting protective coatings

- The versatility and improved application methods of modern aerospace sealants are making them attractive for both OEMs and MRO (maintenance, repair, and overhaul) providers. Manufacturers benefit from easier application, faster curing times, and enhanced adhesion properties, which ultimately support production efficiency and aircraft longevity. Furthermore, these sealants can be applied in diverse operational environments, providing flexibility across different aircraft types and manufacturing processes

- For instance, in 2023, several North American and European aircraft manufacturers reported reduced corrosion-related maintenance incidents after implementing next-generation sealants across fuselage panels and wing assemblies, enhancing aircraft safety and lifecycle performance. The successful deployment of these sealants also improved overall operational efficiency, reduced repair costs, and contributed to higher fleet availability and reliability

- While advanced sealants are driving innovation and operational efficiency, their impact depends on continuous R&D, certification processes, and skilled application. Manufacturers must focus on material development, application training, and regulatory compliance to fully capitalize on market opportunities. In addition, collaboration with suppliers and testing facilities is essential to ensure sealants meet evolving industry standards and performance expectations

Aerospace Sealant Market Dynamics

Driver

“Increasing Demand for Corrosion-Resistant and Lightweight Materials in Aviation”

- The need for corrosion-resistant, lightweight materials is pushing both aircraft manufacturers and MRO providers to prioritize advanced sealants. Sealants such as silicone, polysulfide, and polyurethane ensure structural integrity while reducing aircraft weight, which improves fuel efficiency and operational cost savings. This demand is further reinforced by growing airline fleets and increasing pressure to meet environmental regulations and reduce carbon emissions

- Aircraft operators are increasingly aware of the long-term financial and safety implications of inferior sealing solutions, including premature component wear, leakage, and corrosion. This awareness is driving the adoption of high-performance sealants even in small and mid-sized aviation firms. Enhanced sealant performance also supports aircraft longevity, reduces unscheduled maintenance, and minimizes operational disruptions, adding value to fleet management strategies

- Regulatory compliance and industry standards such as FAA, EASA, and MIL-SPEC are reinforcing the importance of certified sealants in both new builds and retrofit projects. This trend is further supported by technological innovations in curing, adhesion, and material formulation. Manufacturers are leveraging these advancements to meet stringent quality and safety requirements, while ensuring faster certification cycles and improved acceptance in global markets

- For instance, in 2022, several European and North American aerospace OEMs adopted advanced polysulfide and polyurethane sealants in wing-to-fuselage joints, improving aircraft longevity and compliance with safety standards. These implementations also led to measurable reductions in corrosion incidents, improved operational efficiency, and enhanced customer satisfaction due to reliable performance

- While demand is strong, manufacturers must focus on material quality, performance validation, and application expertise to maintain competitiveness and long-term growth. In addition, investments in automated application systems and enhanced training programs for technicians are helping reduce application errors, improve efficiency, and maximize the benefits of advanced sealant solutions

Restraint/Challenge

“High Cost of Advanced Sealants and Specialized Application Requirements”

- The high price of advanced aerospace sealants, including silicone, polysulfide, and polyurethane types, limits adoption among smaller aircraft operators and low-budget MRO providers. Investment in certified materials and application equipment adds to operational expenses. These costs are often compounded by additional quality assurance testing, specialized storage requirements, and ongoing maintenance, creating financial barriers for some market participants

- Application of aerospace sealants often requires specialized training and controlled environments to ensure proper adhesion, curing, and structural performance. Lack of skilled personnel can result in inconsistent application and reduced effectiveness. Furthermore, incorrect application can compromise aircraft safety and lead to costly rework, underscoring the need for rigorous training and standardized procedures

- Supply chain challenges, including sourcing of high-performance raw materials and timely delivery, can delay production and maintenance schedules. These factors impact both OEMs and MRO providers with tight operational timelines. Limited availability of certified sealants in emerging markets can further exacerbate delays, increasing overall project lead times and operational risks

- For instance, in 2023, several aircraft maintenance firms in Asia-Pacific reported delays in fuselage assembly and wing sealing operations due to limited availability of certified sealants and trained applicators, affecting delivery schedules and cost efficiency. These disruptions also resulted in higher maintenance backlogs and delayed aircraft deployment, highlighting supply chain vulnerabilities

- While aerospace sealant technologies continue to advance, addressing cost, application complexity, and supply chain reliability remains crucial for sustained market growth and global adoption. Companies are investing in local manufacturing facilities, strategic sourcing agreements, and training programs to mitigate these challenges, ensuring that advanced sealants can meet growing industry demand efficiently and safely

Aerospace Sealant Market Scope

The aerospace sealant market is segmented on the basis of resin, application, end-use, and formulation technology.

• By Resin

On the basis of resin, the aerospace sealant market is segmented into polysulfide, silicone, fluorosilicone, polyacrylate, polyurethane, polythioether, and others. The polysulfide segment held the largest market revenue share in 2024, driven by its excellent flexibility, chemical resistance, and long-term durability in high-stress aircraft applications. Polysulfide sealants are widely used in fuel tanks, fuselage joints, and wing assemblies, offering superior performance under extreme temperatures and environmental conditions.

The silicone segment is expected to witness the fastest growth rate from 2025 to 2032, driven by its high-temperature resistance, ease of application, and ability to maintain adhesion on diverse substrates. Silicone-based sealants are increasingly preferred for airframe, windshield, and canopy applications due to their durability, UV resistance, and minimal maintenance requirements.

• By Application

On the basis of application, the market is segmented into fuel tank, airframe, flight line repair, aircraft windshield & canopy, fuselage, and others. The airframe segment held the largest market share in 2024, fueled by rising commercial and military aircraft production. Airframe sealants ensure structural integrity, corrosion protection, and improved fuel efficiency, which are critical for long-term aircraft performance.

The flight line repair segment is expected to witness the fastest growth from 2025 to 2032, driven by the increasing need for rapid maintenance and turnaround operations. Quick-curing sealants reduce aircraft downtime and enable efficient repair processes, supporting operational efficiency across airlines and MRO providers.

• By End-Use

On the basis of end-use, the market is segmented into commercial aviation, military aviation, and others. The commercial aviation segment held the largest revenue share in 2024 due to the expanding airline fleet and rising air travel demand. Sealants are extensively used in fuselage, wing, and engine components to enhance safety, fuel efficiency, and long-term durability.

The military aviation segment is expected to witness the fastest growth rate from 2025 to 2032, driven by increasing defense spending, modernization programs, and adoption of advanced aircraft. High-performance sealants are essential in military aircraft to withstand extreme operational conditions and ensure mission readiness.

• By Formulation Technology

On the basis of formulation technology, the market is segmented into solvent-based, water-based, and others. The solvent-based segment held the largest market share in 2024, driven by its excellent adhesion properties, chemical resistance, and proven performance in critical aerospace applications. These sealants are widely used for both OEM and MRO purposes across aircraft types.

The water-based segment is expected to witness the fastest growth from 2025 to 2032, fueled by increasing environmental regulations and demand for eco-friendly sealant solutions. Water-based sealants reduce VOC emissions, are easier to handle, and provide comparable performance, making them an attractive choice for modern aircraft manufacturing and maintenance.

Aerospace Sealant Market Regional Analysis

- North America dominated the aerospace sealant market with the largest revenue share of 38.50% in 2024, driven by a strong aerospace and defense industry, increasing aircraft production, and rising demand for maintenance, repair, and overhaul (MRO) services. The region’s well-established aviation ecosystem and advanced manufacturing infrastructure support the adoption of high-performance sealants

- Aircraft manufacturers and MRO providers in the region prioritize corrosion protection, joint sealing, and thermal resistance, which enhance airframe longevity, reduce maintenance costs, and improve operational efficiency. The use of certified sealants ensures compliance with stringent FAA and EASA regulations

- High technological capabilities, skilled workforce, and R&D investment further support widespread adoption, making North America a key market for both commercial and military aviation applications

U.S. Aerospace Sealant Market Insight

The U.S. aerospace sealant market captured the largest revenue share in 2024 within North America, fueled by increasing aircraft deliveries, growth in commercial aviation, and expanding MRO operations. Manufacturers are focusing on lightweight, corrosion-resistant sealants to improve fuel efficiency and structural durability. Integration of advanced polysulfide, silicone, and polyurethane sealants in fuselage, wing panels, and fuel tanks has enhanced safety and performance. In addition, government contracts and military aviation projects continue to drive demand for certified high-performance sealants.

Europe Aerospace Sealant Market Insight

The Europe aerospace sealant market is expected to witness the fastest growth rate from 2025 to 2032, driven by stringent safety and environmental regulations, growing defense expenditure, and modernization of fleets. The region is seeing increased adoption of eco-friendly, high-performance sealants in commercial and military aircraft. Technological advancements and urbanization in key aviation hubs are promoting new aircraft programs and retrofit projects, fostering market expansion.

U.K. Aerospace Sealant Market Insight

The U.K. aerospace sealant market is expected to witness significant growth from 2025 to 2032, supported by the country’s focus on aerospace innovation, aircraft production, and MRO services. Rising awareness of operational safety and structural efficiency encourages the adoption of advanced sealants across airframes, wings, and fuselage assemblies. Furthermore, the U.K.’s established aerospace ecosystem and regulatory compliance initiatives drive the market for certified, high-performance sealants.

Germany Aerospace Sealant Market Insight

The Germany aerospace sealant market is expected to witness strong growth from 2025 to 2032, fueled by the country’s industrial expertise, advanced manufacturing infrastructure, and focus on sustainable aviation solutions. Adoption of polysulfide, polyurethane, and silicone sealants in fuel tanks, airframes, and windshields is increasing due to regulatory compliance and high-quality standards. Germany’s emphasis on technological innovation and eco-conscious practices supports the growing demand for advanced aerospace sealants.

Asia-Pacific Aerospace Sealant Market Insight

The Asia-Pacific aerospace sealant market is expected to witness the fastest growth rate from 2025 to 2032, driven by rapid urbanization, rising aircraft production, and expanding commercial aviation sectors in countries such as China, Japan, and India. Government initiatives promoting aerospace manufacturing, smart cities, and defense programs are boosting sealant adoption. Availability of cost-effective sealants and skilled labor is enhancing market penetration across commercial and military aviation.

Japan Aerospace Sealant Market Insight

The Japan aerospace sealant market is expected to witness significant growth from 2025 to 2032, due to the country’s high-tech culture, rapid urbanization, and demand for advanced aerospace technologies. Japanese aircraft manufacturers increasingly integrate polysulfide, silicone, and polyurethane sealants for airframe protection, fuel tank sealing, and canopy applications. Aging aircraft fleets and growth in MRO activities further drive demand for durable and reliable sealant solutions.

China Aerospace Sealant Market Insight

The China aerospace sealant market accounted for the largest market revenue share in Asia Pacific in 2024, attributed to rapid aircraft production, increasing commercial and military aviation projects, and strong domestic manufacturing capabilities. The adoption of high-performance sealants in fuel tanks, fuselage joints, and wing assemblies is rising due to government aerospace initiatives and investments in new-generation aircraft programs. Affordable sealant options, local manufacturing, and expanding aerospace infrastructure are key factors propelling market growth.

Aerospace Sealant Market Share

The Aerospace Sealant industry is primarily led by well-established companies, including:

- 3M (U.S.)

- Solvay (Belgium)

- PPG Industries, Inc. (U.S.)

- Henkel Corporation (Germany)

- Beacon Adhesives, Inc. (U.S.)

- Master Bond Inc. (U.S.)

- H.B. Fuller Company (U.S.)

- Arkema (France)

- Flamemaster Corp. (U.S.)

- Aerospace Sealants (U.S.)

- Chemetall (Germany)

Latest Developments in Global Aerospace Sealant Market

- In September 2022, Solvay entered into a long-term agreement with Avio SpA to supply advanced composites and adhesive materials for aerospace applications. The supplied products are intended for multiple aerospace programs, including the Vega space program and European Space Agency satellite launch vehicles designed for low Earth orbit (LEO) missions. This partnership enables Solvay to strengthen its presence in high-performance aerospace materials, supporting innovation and reliability in space technology while enhancing its market share in the global aerospace sector

- In January 2022, H.B. Fuller completed the acquisition of Apollo, a U.K.-based manufacturer of liquid adhesives, sealants, coatings, and primers for roofing, industrial, and construction applications. Apollo will integrate into H.B. Fuller’s Construction Adhesives and Engineering Adhesives business units, enhancing the company’s capabilities in high-value, high-margin markets across the U.K. and Europe. This acquisition is expected to expand H.B. Fuller’s product portfolio, improve market penetration, and drive growth in key construction and industrial segments

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Aerospace Sealant Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Aerospace Sealant Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Aerospace Sealant Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.