Global Agricultural Machinery Market

Market Size in USD Billion

USD

171.80 Billion

USD

235.12 Billion

2024

2032

USD

171.80 Billion

USD

235.12 Billion

2024

2032

| 2025 - 2032 | |

| USD 171.80 Billion | |

| USD 235.12 Billion | |

| % | |

|

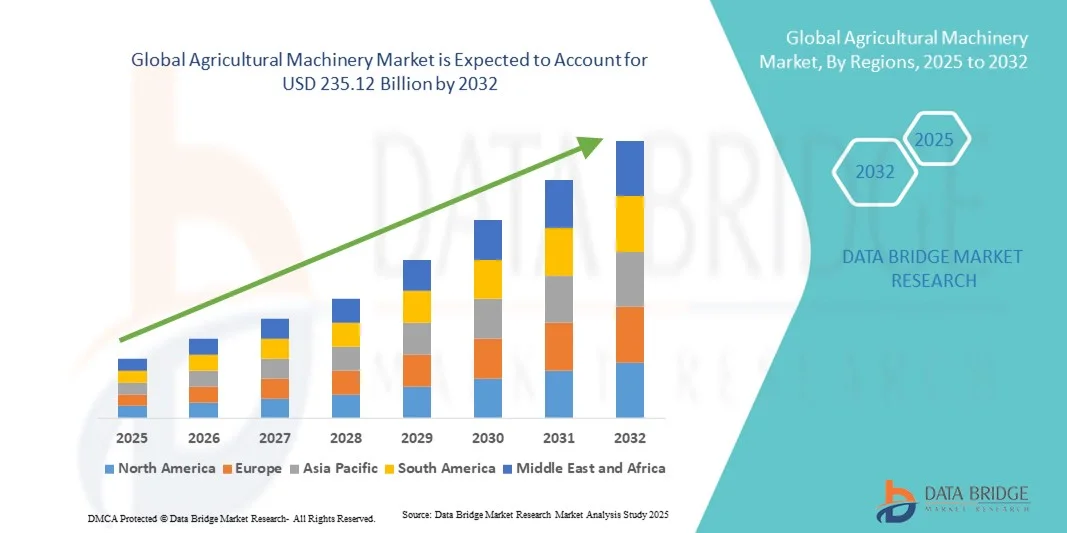

Global Agricultural Machinery Market Size

- The global Agricultural Machinery Market size was valued at USD 171.80 billion in 2024 and is expected to reach USD 235.12 billion by 2032, at a CAGR of 4.00% during the forecast period.

- The market growth is primarily driven by the increasing demand for mechanization in agriculture, coupled with advancements in precision farming technologies, automation, and smart farming equipment, which are enhancing efficiency and productivity.

- Additionally, rising global food demand, labor shortages, and government initiatives supporting modern farming practices are encouraging the adoption of advanced agricultural machinery, thereby significantly accelerating the growth of the industry.

Global Agricultural Machinery Market Analysis

- Agricultural machinery, encompassing equipment such as tractors, harvesters, plows, and seeders, is becoming increasingly essential in modern farming practices due to its ability to enhance efficiency, reduce labor requirements, and support large-scale food production across diverse agricultural settings.

- The rising adoption of agricultural machinery is primarily driven by the need for mechanization, precision farming technologies, and automation, along with growing global food demand and labor shortages in the farming sector.

- Asia-Pacific dominated the Global Agricultural Machinery Market with the largest revenue share of 31.5% in 2024, supported by advanced farming practices, high investment in agricultural technology, and strong presence of leading machinery manufacturers, with the U.S. witnessing substantial growth in machinery adoption for large-scale farms and specialized crop production.

- North America is expected to be the fastest-growing region in the Global Agricultural Machinery Market during the forecast period due to increasing agricultural mechanization, government initiatives promoting modern farming, and rising disposable incomes among rural populations.

- The tractors segment dominated the market with the largest revenue share of 36.5% in 2024, due to its multi-functional capabilities, widespread adoption across diverse farm sizes, and increasing integration with precision agriculture technologies such as GPS and automated steering.

Report Scope and Global Agricultural Machinery Market Segmentation

|

Attributes |

Agricultural Machinery Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

• John Deere (U.S.) |

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Global Agricultural Machinery Market Trends

Enhanced Efficiency Through AI and Automation Integration

- A significant and accelerating trend in the global Agricultural Machinery Market is the increasing integration of artificial intelligence (AI) and advanced automation technologies into farm equipment. This combination is significantly enhancing operational efficiency, crop management, and decision-making for modern farmers.

- For instance, John Deere’s AutoTrac system uses AI and GPS-based guidance to enable tractors and harvesters to operate autonomously with high precision, reducing overlap and minimizing fuel consumption. Similarly, Kubota’s smart tractors integrate AI-assisted monitoring systems to optimize planting, irrigation, and fertilization schedules.

- AI integration in agricultural machinery enables features such as predictive maintenance, real-time crop monitoring, and adaptive task scheduling. For example, Claas’ telematics platform analyzes equipment performance and field data to suggest operational improvements, while Mahindra & Mahindra’s AI-driven tractors can adjust field operations based on soil conditions and crop requirements.

- The seamless integration of AI and automation with farm management platforms allows farmers to centralize control over multiple machines and agricultural operations. Through a single interface, users can monitor equipment, optimize resource use, and coordinate planting, harvesting, and maintenance schedules, creating a more efficient and data-driven farming ecosystem.

- This trend toward intelligent, automated, and interconnected machinery is fundamentally transforming expectations for modern agriculture. Consequently, companies such as AGCO are developing AI-enabled tractors and harvesters with features such as autonomous operation, real-time performance analytics, and adaptive control for diverse crop conditions.

- The demand for agricultural machinery with advanced AI and automation capabilities is growing rapidly across both large-scale and smallholder farms, as farmers increasingly prioritize productivity, resource efficiency, and precision farming solutions.

Global Agricultural Machinery Market Dynamics

Driver

Growing Need Due to Rising Food Demand and Labor Shortages

- The increasing global demand for food, coupled with labor shortages in the agricultural sector, is a significant driver for the heightened adoption of advanced agricultural machinery.

- For instance, in 2024, John Deere launched an upgraded autonomous tractor series equipped with AI-driven field optimization and precision planting capabilities, aimed at addressing labor constraints and improving farm productivity. Such innovations by key companies are expected to drive growth in the agricultural machinery market during the forecast period.

- As farmers face rising operational challenges, modern machinery offers advanced features such as precision planting, automated harvesting, soil monitoring, and crop health analytics, providing a compelling upgrade over traditional, manual farming methods.

- Furthermore, the growing adoption of smart farming technologies and connected equipment is making agricultural machinery an integral component of modern farm operations, offering seamless integration with farm management software, IoT sensors, and GPS-based systems.

- The benefits of automation, resource optimization, increased efficiency, and data-driven decision-making are key factors propelling the adoption of agricultural machinery across both large-scale commercial farms and smallholder operations. Government incentives, subsidies, and growing awareness of sustainable farming practices further contribute to market growth.

Restraint/Challenge

High Initial Investment Costs and Maintenance Complexity

- The high initial cost of advanced agricultural machinery, along with the complexity of operation and maintenance, poses a significant challenge to broader market penetration. Modern equipment often requires skilled operators and technical knowledge, which can be a barrier for small-scale or resource-limited farmers.

- For instance, the price of autonomous tractors or precision harvesters from companies such as John Deere and Kubota remains substantially higher than conventional machinery, limiting adoption among cost-sensitive farmers, particularly in developing regions.

- Ensuring affordability through financing options, government subsidies, and scalable solutions, alongside training programs for operators, is crucial for expanding market reach. Additionally, the need for regular maintenance, software updates, and technical support can create operational challenges and add to overall ownership costs.

- While leasing models and smaller, modular machinery options are gradually increasing accessibility, the perceived premium for advanced technology can still hinder widespread adoption, especially for farmers who do not immediately require full-scale automation or precision features.

- Overcoming these challenges through affordable financing, operator training, simplified maintenance, and local service networks will be vital for sustained growth in the global agricultural machinery market.

Global Agricultural Machinery Market Scope

Agricultural machinery market is segmented on the basis of type and application.

- By Type

On the basis of type, the Global Agricultural Machinery Market is segmented into tractors, ploughing and cultivating machinery, planting machinery, irrigation machinery, harvesting machinery, and other types. The tractors segment dominated the market with the largest revenue share of 36.5% in 2024, due to its multi-functional capabilities, widespread adoption across diverse farm sizes, and increasing integration with precision agriculture technologies such as GPS and automated steering. Tractors remain essential for plowing, hauling, and field preparation, making them a preferred choice for farmers globally. The harvesting machinery segment is projected to witness the fastest CAGR of 20.8% from 2025 to 2032, driven by labor shortages, rising demand for efficient crop collection, and the adoption of semi-automated and fully automated harvesting equipment such as combine harvesters and balers. Government incentives and technological advancements further accelerate the growth of this segment.

- By Application

On the basis of application, the Global Agricultural Machinery Market is segmented into alloy production, agriculture, polishing, aerospace, and others. The agriculture segment accounted for the largest market revenue share of 52.8% in 2024, fueled by increasing global food demand, the adoption of mechanized farming, and precision agriculture solutions. Agricultural machinery enhances productivity, efficiency, and overall crop yield, driving consistent market growth. The alloy production segment is expected to witness the fastest CAGR of 19.5% from 2025 to 2032, driven by growing industrialization, rising demand for metal processing machinery, and automation in manufacturing facilities. Expanding investments in alloy production, polishing, and aerospace sectors are increasing demand for specialized machinery, allowing manufacturers to diversify their offerings and capture new industrial markets alongside traditional agriculture.

Global Agricultural Machinery Market Regional Analysis

- Asia Pacific dominated the Global Agricultural Machinery Market with the largest revenue share of 31.5% in 2024, driven by the high adoption of modern farming practices, large-scale commercial farms, and supportive government policies promoting mechanization and precision agriculture.

- Farmers in the region increasingly rely on advanced machinery such as tractors, harvesters, and irrigation systems to improve productivity, optimize resource use, and reduce labor dependency. The emphasis on precision farming, automation, and sustainable practices further fuels demand for technologically advanced agricultural equipment.

- This widespread adoption is supported by high capital availability, advanced infrastructure, and the presence of leading agricultural machinery manufacturers, establishing North America as a key market for both smallholder and large-scale commercial operations. The availability of financing options, subsidies, and training programs for machinery operators also contributes to sustained growth and positions the region as a frontrunner in the global agricultural machinery market.

U.S. Agricultural Machinery Market Insight

The U.S. agricultural machinery market captured the largest revenue share of 35% in 2024 within North America, fueled by the widespread adoption of advanced mechanization, precision farming, and smart agriculture technologies. Farmers are increasingly investing in tractors, harvesters, irrigation systems, and planting machinery to improve efficiency, reduce labor dependency, and optimize crop yields. The availability of government subsidies, financing options, and strong support infrastructure further propels market growth. Moreover, innovations such as AI-driven tractors, GPS-guided machinery, and automated harvesters are contributing significantly to the market expansion, particularly in large-scale commercial farming operations.

Europe Agricultural Machinery Market Insight

The European agricultural machinery market is projected to expand at a substantial CAGR during the forecast period, primarily driven by government incentives for modern farming practices, stringent agricultural regulations, and increasing awareness of sustainable farming. Countries such as Germany, France, and Italy are witnessing rising adoption of tractors, precision seeders, and automated irrigation systems. The trend toward smart and connected machinery is encouraging both new installations and upgrades of existing equipment, particularly in commercial and cooperative farming operations. Demand is also growing for energy-efficient, low-emission machinery aligned with environmental sustainability goals.

U.K. Agricultural Machinery Market Insight

The U.K. agricultural machinery market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by the modernization of farms, rising labor costs, and increased awareness of mechanized solutions to boost productivity. Farmers are increasingly adopting compact tractors, automated harvesters, and precision planting equipment to meet operational efficiency targets. Additionally, government initiatives supporting sustainable agriculture and farm mechanization, alongside rising investment in agri-tech startups, are further stimulating market growth.

Germany Agricultural Machinery Market Insight

The Germany agricultural machinery market is expected to expand at a considerable CAGR during the forecast period, fueled by advanced farm infrastructure, high technological adoption, and strong R&D in precision agriculture equipment. German farmers are increasingly relying on tractors, irrigation systems, and harvesting machinery with IoT-enabled monitoring and automation features. The demand for eco-friendly machinery, reduced emissions, and energy-efficient operations is further driving market adoption. Integration with farm management systems for real-time monitoring and data-driven decision-making is also a key growth driver.

Asia-Pacific Agricultural Machinery Market Insight

The Asia-Pacific agricultural machinery market is poised to grow at the fastest CAGR of 22% from 2025 to 2032, driven by increasing farm mechanization, rapid urbanization, and rising disposable incomes in countries such as China, India, and Japan. The region is witnessing growing adoption of tractors, irrigation machinery, and automated harvesters, supported by government initiatives promoting modern agriculture and digital farming. Additionally, the presence of local manufacturers producing cost-effective machinery and the expansion of contract farming are further accelerating market penetration across both smallholder and commercial farms.

Japan Agricultural Machinery Market Insight

The Japan agricultural machinery market is gaining momentum due to high technological adoption, labor shortages, and the country’s focus on precision and smart farming solutions. Farmers are increasingly leveraging automated tractors, robotic harvesters, and smart irrigation systems to enhance productivity and reduce dependency on manual labor. Integration with IoT-based farm monitoring platforms and data analytics systems is fueling growth. Additionally, the aging farming population in Japan is driving demand for user-friendly, automated equipment that minimizes physical effort while ensuring efficient farm management.

China Agricultural Machinery Market Insight

The China agricultural machinery market accounted for the largest market revenue share in Asia-Pacific in 2024, attributed to rapid urbanization, expansion of commercial farms, and increasing adoption of mechanized farming. Tractors, planting machinery, and irrigation equipment are witnessing high demand due to government initiatives promoting smart agriculture and precision farming. The push toward modernized agriculture, coupled with affordable domestic machinery options and the growth of large-scale farming operations, is significantly propelling market expansion. Additionally, China’s focus on improving crop yields and labor efficiency continues to drive machinery adoption across diverse agricultural segments.

Global Agricultural Machinery Market Share

The Agricultural Machinery industry is primarily led by well-established companies, including:

• John Deere (U.S.)

• AGCO Corporation (U.S.)

• CNH Industrial (Italy)

• Kubota Corporation (Japan)

• Same Deutz-Fahr (Germany)

• Claas (Germany)

• Mahindra & Mahindra (India)

• Argo Tractors (Italy)

• Kioti (South Korea)

• Fendt (Germany)

• Hyundai Heavy Industries (South Korea)

• Lovol Heavy Industry (China)

• Sonalika Tractors (India)

• Yanmar (Japan)

• Shandong YTO Group (China)

• Valtra (Finland)

• Case IH (U.S.)

• Doosan Infracore (South Korea)

• Zoomlion (China)

• Tafe (India)

What are the Recent Developments in Global Agricultural Machinery Market?

- In April 2023, CNH Industrial, a global leader in agricultural machinery, launched a strategic initiative in South Africa aimed at improving farm productivity through its advanced tractors and harvesting equipment. This program underscores the company’s dedication to providing innovative, reliable, and high-performance machinery tailored to the unique needs of regional farms. By leveraging its global expertise and cutting-edge product offerings, CNH Industrial is addressing local agricultural challenges while strengthening its presence in the rapidly growing global agricultural machinery market.

- In March 2023, Kubota Corporation, a leading Japanese manufacturer, introduced the latest precision planting and irrigation machinery designed specifically for large-scale commercial farms. The new systems enhance operational efficiency, reduce labor dependency, and optimize crop yields. This advancement highlights Kubota’s commitment to innovation in mechanized farming technologies and its focus on meeting evolving demands in both domestic and international agricultural markets.

- In March 2023, Mahindra & Mahindra, an Indian agritech giant, successfully deployed a smart tractor fleet program in Karnataka to support smallholder farmers with modern mechanization solutions. The initiative leverages GPS-enabled tractors and automated equipment to improve productivity, reduce fuel consumption, and provide actionable farm insights. The project emphasizes Mahindra’s focus on integrating technology with agriculture to create sustainable and efficient farming practices.

- In February 2023, Claas Group, a German agricultural machinery leader, announced a strategic partnership with European farming cooperatives to develop and distribute AI-powered harvesting systems. This collaboration aims to enhance operational efficiency, reduce crop losses, and facilitate sustainable farming practices. The initiative underscores Claas’ commitment to driving innovation and digital transformation in agriculture while improving productivity for cooperative members.

- In January 2023, Argo Tractors, an Italian manufacturer of high-performance tractors, unveiled the Tigre 120 Smart Tractor at the EIMA International Agricultural Exhibition. Equipped with telematics, IoT-enabled monitoring, and precision farming features, the tractor allows farmers to manage operations remotely and optimize field performance. The launch highlights Argo Tractors’ dedication to integrating advanced technology into agricultural machinery, offering farmers enhanced efficiency, control, and productivity.

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.