Global Agricultural Tire Market

Market Size in USD Billion

USD

8.60 Billion

USD

18.70 Billion

2025

2033

USD

8.60 Billion

USD

18.70 Billion

2025

2033

| 2026 - 2033 | |

| USD 8.60 Billion | |

| USD 18.70 Billion | |

| % | |

|

Agricultural Tire Market Size

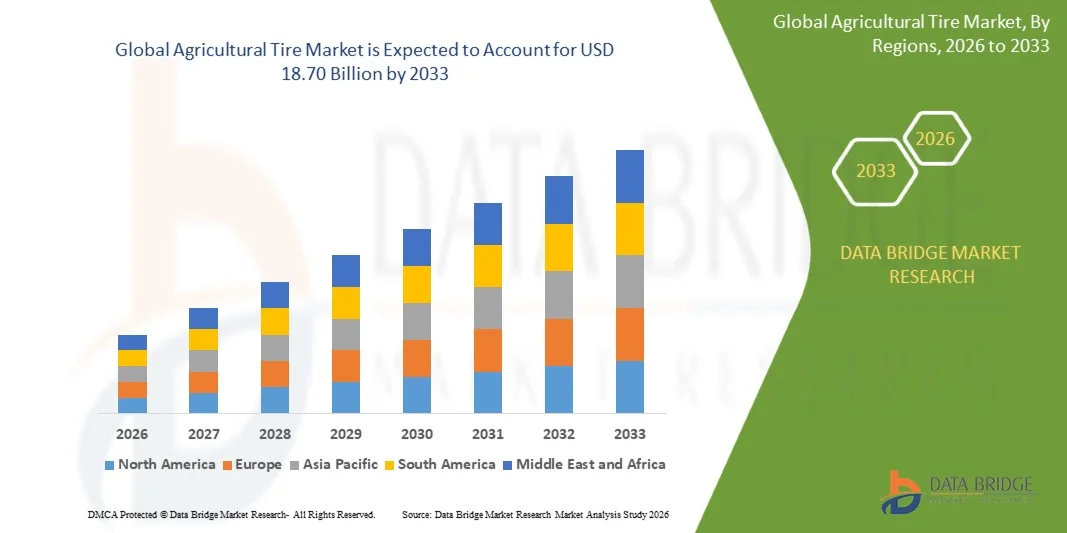

- The global agricultural tire market size was valued at USD 8.6 billion in 2025 and is expected to reach USD 18.70 billion by 2033, at a CAGR of 10.20% during the forecast period

- The agricultural tire market growth is largely fueled by the rising adoption of farm mechanization and continuous technological progress in tire engineering, which are improving efficiency, traction, and durability across various farming operations. In addition, increasing demand for high-performance tires that support precision agriculture, reduced soil compaction, and enhanced fuel efficiency is strengthening overall market expansion

- Furthermore, the shift toward advanced radial, IF, and VF tire technologies, along with the growing need for reliable tires for tractors, harvesters, and other farm machinery, is accelerating product upgrades among farmers. These converging factors are driving steady adoption of next-generation agricultural tires, thereby significantly boosting the industry's growth

Agricultural Tire Market Analysis

- Agricultural tires, designed to support tractors, harvesters, sprayers, and farm implements, are becoming essential components of modern mechanized farming due to their role in improving traction, load-carrying capacity, and field-to-road performance while minimizing soil disturbance

- The escalating demand for agricultural tires is primarily driven by expanding farm mechanization across emerging and developed regions, the need for higher productivity in large-scale farming, and increasing preference for advanced tire designs that enhance operational efficiency and maximize equipment performance

- Asia-Pacific dominated the agricultural tire market with a share of 38.33% in 2025, due to the high concentration of agricultural machinery usage, rising mechanization rates, and expanding cultivation areas across major farming economies

- North America is expected to be the fastest growing region in the agricultural tire market during the forecast period due to widespread adoption of advanced agricultural machinery, increasing sales of high-horsepower tractors and combines, and strong demand for premium radial and IF/VF tire technologies

- Tractors segment dominated the market with a market share of 57.23% in 2025, due to its widespread use across core farming operations that require consistent traction, load-bearing stability, and high durability in varying soil conditions. Tractors are the primary machinery used for plowing, tilling, seeding, hauling, and field preparation, which results in the highest tire utilization among all agricultural equipment. Their continuous year-round operation increases both OEM demand and replacement frequency, reinforcing the segment’s strong market contribution. The extensive global adoption of tractors across small, medium, and large farms further strengthens tire consumption in this category, supporting its clear dominance in the overall agricultural tire market

Report Scope and Agricultural Tire Market Segmentation

|

Attributes |

Agricultural Tire Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Agricultural Tire Market Trends

“Rising Adoption of IF/VF and Smart Tire Technologies”

- A significant trend in the agricultural tire market is the rapid shift toward IF, VF, and sensor-enabled smart tire technologies that improve traction, load capacity, and soil protection across modern farming operations. These advancements are strengthening the role of premium agricultural tires as essential components for precision agriculture, enhancing machine performance and enabling farmers to operate efficiently under varying field conditions

- For instance, Yokohama (ATG) and Trelleborg are introducing VF-grade flotation and traction-optimized tires that support heavier machinery while reducing soil compaction, improving fuel efficiency, and extending tire life. Such innovations are aligned with the growing adoption of high-horsepower tractors and implement equipment that require robust, technologically advanced tire solutions

- The use of advanced construction technologies is rising as farmers increasingly depend on tires that offer superior grip, lower slippage, and consistent performance in wet, dry, and uneven terrains. This trend is positioning IF/VF and smart tires as critical enablers of improved productivity and reduced operational downtime

- The growing emphasis on precision agriculture is accelerating demand for tires that support optimized load distribution and consistent pressure control, helping farmers protect soil health and maintain yield quality

- Large-scale farmers are adopting advanced radial tires to reduce rolling resistance and improve field-to-road efficiency, supporting faster transportation and reduced fuel consumption

- The market is experiencing strong growth in premium tire categories where enhanced durability, improved traction geometry, and digital monitoring capabilities are reinforcing the transition toward next-generation agricultural mobility systems

Agricultural Tire Market Dynamics

Driver

“Increasing Farm Mechanization and Demand for High-Performance Tires”

- Rising farm mechanization across global agricultural landscapes is driving strong demand for high-performance tires that enhance operational efficiency, field stability, and load-carrying capabilities. Farmers are investing in advanced tires to improve traction, support heavier machinery, and maintain consistent performance across diverse soil and weather conditions

- For instance, brands such as BKT supply IF/VF tires for high-horsepower tractors and harvesters, helping farmers manage heavier implements with reduced soil pressure and improved fuel efficiency. These tires support rigorous field operations and enable improved productivity in modern mechanized farming systems

- The expansion of large-scale farming is fueling the need for premium radial tires that offer longer service life and reduced maintenance costs under intensive usage. The adoption of precision farming techniques is pushing demand for tires with optimized pressure distribution and stronger carcass structures to support enhanced control and stability

- The rise in global food production requirements is encouraging farmers to upgrade their machinery with tires that can withstand extended working hours, harsh terrains, and fluctuating loads

- Increasing preference for premium tire technologies is reinforcing market growth as farmers focus on achieving greater output with minimal downtime while optimizing operating costs and fuel usage

Restraint/Challenge

“High Cost of Advanced Agricultural Tires and Replacement Expenses”

- The agricultural tire market faces challenges due to the high cost of advanced radial, IF, and VF tire technologies, which require specialized materials, reinforced structures, and precision manufacturing processes. These factors increase upfront purchase costs and pose affordability concerns for small and mid-scale farmers

- For instance, leading manufacturers such as Michelin integrate advanced tread compounds and reinforced sidewall technologies into premium agricultural tires, which improves durability but results in higher production and market prices. This elevated cost structure makes it difficult for cost-sensitive farmers to adopt next-generation solutions

- The need for frequent replacement in high-usage environments further adds to ownership expenses, making cost management a key concern for farmers operating under tight profitability margins

- Dependence on imported raw materials and fluctuating rubber prices contribute to unstable cost dynamics for manufacturers, affecting tire availability and pricing consistency. The complexity of producing high-performance agricultural tires limits economies of scale, keeping premium prices elevated across global markets

- These challenges collectively pressure farmers to balance performance needs with budget limitations, slowing adoption rates of advanced tire technologies despite their long-term productivity benefits

Agricultural Tire Market Scope

The market is segmented on the basis of sales channel, application, tire construction, rim-size, equipment horsepower class, and inflation-technology compatibility.

- By Sales Channel

On the basis of sales channel, the agricultural tire market is segmented into OEM and Replacement / Aftermarket. The OEM segment dominated the market in 2025 with the largest revenue share due to its integration into new tractors, harvesters, and implements purchased by farmers. OEM tires remain preferred for their guaranteed compatibility, factory-tested performance, and fitment efficiency during new equipment delivery. Major agricultural machinery manufacturers collaborate with tire suppliers to adopt durable radial and advanced tread designs supporting traction and soil protection. The expansion of new farm machinery sales, particularly in Asia and North America, strengthens the OEM segment’s lead. Farmers rely on OEM-fitted tires for initial operation cycles due to their reliability in heavy-duty farm applications, contributing to sustained dominance.

The Replacement / Aftermarket segment is anticipated to witness the fastest growth from 2026 to 2033, driven by frequent tire wear caused by continuous field usage and changing soil conditions. Farmers increasingly replace tires to maintain efficiency, reduce slippage, and sustain machine performance throughout seasonal operations. Higher adoption of high-horsepower equipment accelerates wear cycles, leading to rising demand for aftermarket upgrades. The availability of advanced radial and IF/VF tires in aftermarket channels encourages farmers to shift toward performance-focused replacements. Strengthening distribution networks and rural retail expansions further support the rapid rise of the aftermarket segment in the coming years.

- By Application

On the basis of application, the agricultural tire market is segmented into tractors, combine harvesters, sprayers, trailers, loaders & telehandlers, and other implements. The tractor segment dominated the market with the largest share of 57.23% in 2025 driven by its widespread use across core farming operations that require consistent traction, load-bearing stability, and high durability in varying soil conditions. Tractors are the primary machinery used for plowing, tilling, seeding, hauling, and field preparation, which results in the highest tire utilization among all agricultural equipment. Their continuous year-round operation increases both OEM demand and replacement frequency, reinforcing the segment’s strong market contribution. The extensive global adoption of tractors across small, medium, and large farms further strengthens tire consumption in this category, supporting its clear dominance in the overall agricultural tire market.

- By Tire Construction

On the basis of tire construction, the market is segmented into bias, radial, and IF/VF radial tires. The radial segment dominated the agricultural tire market in 2025 as farmers widely prefer radial construction for its improved traction, extended lifespan, and reduced fuel consumption. Radial tires distribute pressure uniformly, lowering soil compaction and supporting healthier crop growth. Their superior stability during transport and field operations makes them a standard choice for modern tractors and harvesters. The expansion of mechanized farming and higher adoption of performance-focused machinery further strengthens radial tire demand. Manufacturers continue enhancing radial designs with optimized lugs and flexible sidewalls, reinforcing market leadership.

The IF/VF radial segment is anticipated to witness the fastest growth from 2026 to 2033, fueled by the need for tires that carry heavier loads at significantly lower inflation pressures. IF/VF tires offer larger footprints, reducing compaction and enhancing traction efficiency in large-scale fields. These tires are strongly favored in precision farming systems where machine productivity and soil health are critical performance factors. Growing deployment of advanced, high-horsepower machinery increases reliance on IF/VF technologies. Farmers adopting sustainability-focused practices increasingly transition toward IF/VF tires for long-term operational benefits, boosting segment expansion.

- By Rim-Size

On the basis of rim-size, the agricultural tire market is segmented into less than 20 inch, 20–30 inch, 30–40 inch, and more than 40 inch. The 20–30 inch segment dominated the market in 2025 since this rim-size range is widely used in tractors, trailers, and mid-range farm equipment across global agricultural operations. These tires provide a balance between durability, load capacity, and maneuverability, making them suitable for major farm applications. High adoption of compact and medium-horsepower tractors contributes to consistent usage of this rim category. The segment benefits from strong aftermarket replacement cycles driven by routine field usage. Its compatibility with conventional and modern radial constructions ensures stable market leadership.

The more than 40 inch segment is expected to witness the fastest growth from 2026 to 2033, driven by rising deployment of large harvesters, sprayers, and high-horsepower tractors. Large-diameter tires offer superior flotation, reduced soil disturbance, and improved operational stability in wide-row and large-acreage farming. Expansion of commercial-scale farms in North America, Europe, and Brazil supports demand for these oversized tires. IF/VF radial developments increasingly target larger rim categories, accelerating growth. Farmers prioritizing higher efficiency and machine productivity increasingly shift toward large-diameter tire setups, strengthening segment momentum.

- By Equipment Horsepower Class

On the basis of horsepower class, the agricultural tire market is segmented into less than 30 HP, 30–70 HP, 71–150 HP, and more than 150 HP. The 71–150 HP segment dominated the market in 2025 as this class is the most widely used across mid-sized farms for tilling, planting, plowing, and transport operations. Equipment in this range requires tires with higher load-bearing stability and strong traction, supporting consistent demand. Medium-horsepower tractors represent the largest global fleet share, strengthening tire consumption across both OEM and aftermarket channels. Growing use of radial and IF/VF tires in this class enhances operational efficiency. These machines are central to mixed crop farming systems worldwide, ensuring segment leadership.

The more than 150 HP segment is anticipated to witness the fastest growth from 2026 to 2033, driven by escalating adoption of high-horsepower machinery in mechanized and commercial farming. These large tractors and combines require advanced heavy-duty tires that offer superior load capacity and minimized compaction. Expanding cultivation of large acreage farms accelerates the shift toward high-power equipment. Farmers seeking improved productivity and reduced downtime increasingly invest in robust radial and IF/VF tire upgrades. The trend toward precision-based high-output operations further fuels rapid growth in this category.

- By Inflation-Technology Compatibility

On the basis of inflation-technology compatibility, the market is segmented into standard tires and CTIS-Ready / smart tires. The standard tires segment dominated in 2025 owing to their widespread availability, cost-effectiveness, and suitability across conventional farm machinery. Farmers continue to rely on standard tires for routine field tasks where traditional inflation practices are sufficient. Strong penetration in small and mid-sized tractors supports consistent demand. Manufacturers offer a wide range of standard bias and radial designs that align with varied soil conditions. The segment maintains leadership due to its affordability and broad use across global farming systems.

The CTIS-Ready / smart tires segment is expected to witness the fastest growth from 2026 to 2033, driven by rising adoption of digitally controlled inflation systems that enhance traction and reduce compaction. Smart tires support real-time pressure adjustments, improving equipment performance in diverse field conditions. Precision farming trends strengthen the uptake of CTIS-compatible designs offering fuel savings and improved durability. Large farms adopting advanced machinery increasingly prefer smart tire systems to optimize operational efficiency. Expanding availability of OEM-integrated CTIS solutions accelerates growth across this segment.

Agricultural Tire Market Regional Analysis

- Asia-Pacific dominated the agricultural tire market with the largest revenue share of 38.33% in 2025, driven by the high concentration of agricultural machinery usage, rising mechanization rates, and expanding cultivation areas across major farming economies

- The region’s large-scale production of tractors, harvesters, and implements, supported by cost-effective manufacturing and favorable equipment financing policies, is accelerating market expansion

- Growing demand for advanced radial and IF/VF tire technologies, increasing farm modernization initiatives, and a rapidly developing agricultural infrastructure contribute to sustained market growth across Asia-Pacific

China Agricultural Tire Market Insight

China held the largest share in the Asia-Pacific agricultural tire market in 2025 due to its strong agricultural equipment manufacturing base and extensive fleet of tractors and harvesters in active operation. The country benefits from high-volume tire production capabilities, integrated supply chains, and growing adoption of modern farming practices. Government support for agricultural modernization and rising demand for durable, high-performance tires across large farmlands further strengthens China’s leadership in the regional market.

India Agricultural Tire Market Insight

India is witnessing the fastest growth in the Asia-Pacific region, supported by rapid farm mechanization, rising tractor sales, and expansion of medium-horsepower equipment usage. Increasing government subsidies, improving rural infrastructure, and heightened focus on enhancing farm productivity are boosting agricultural tire demand. A growing replacement market, combined with increasing adoption of radialized tires across Indian farms, is contributing to the country’s robust growth momentum.

Europe Agricultural Tire Market Insight

The Europe agricultural tire market is expanding steadily, driven by advanced farm mechanization, high adoption of radial and IF/VF technologies, and a strong emphasis on soil conservation practices. The region’s focus on sustainable farming, precision-based equipment use, and compliance with environmental regulations supports demand for high-quality agricultural tires. Increasing deployment of large tractors, sprayers, and combines across Western and Central Europe further accelerates market growth, along with rising replacement needs in highly mechanized farms.

Germany Agricultural Tire Market Insight

Germany’s agricultural tire market is driven by its leadership in advanced farm machinery usage, high prevalence of large-acre commercial farms, and strong demand for high-performance radial and VF tire technologies. The country’s engineering expertise and widespread adoption of precision agriculture strengthen demand for tires offering improved traction, reduced compaction, and longer operational life. A mature replacement market and strong OEM integration further support Germany’s position in the European region.

U.K. Agricultural Tire Market Insight

The U.K. market is supported by a transition toward modern, efficient farm equipment, increasing investment in high-horsepower machinery, and rising focus on sustainable tire technologies. Growing adoption of radial and specialty flotation tires improves precision operations in diverse terrains. The country’s strong agricultural machinery rental ecosystem and active replacement cycles contribute to a steady rise in tire consumption across farming sectors.

North America Agricultural Tire Market Insight

North America is projected to grow at the fastest CAGR from 2026 to 2033 due to widespread adoption of advanced agricultural machinery, increasing sales of high-horsepower tractors and combines, and strong demand for premium radial and IF/VF tire technologies. Expanding commercial farms, rising focus on productivity optimization, and rapid integration of precision agriculture systems are boosting tire upgrades and replacements. Strong partnerships between OEMs and tire manufacturers further reinforce the region’s accelerating growth.

U.S. Agricultural Tire Market Insight

The U.S. accounted for the largest share in the North America agricultural tire market in 2025, supported by extensive use of large-acre farming machinery and consistent demand for high-performance agricultural tires. The country’s advanced farming practices, emphasis on yield maximization, and significant penetration of precision technologies strengthen demand for radial and IF/VF tires. Strong OEM presence, a developed replacement market, and robust farm equipment sales solidify the U.S. as the leading contributor to regional growth.

Agricultural Tire Market Share

The agricultural tire industry is primarily led by well-established companies, including:

- Michelin (France)

- Apollo Tyres Ltd. (India)

- Goodyear Tire & Rubber Co. (U.S.)

- Nokian Tyres plc (Finland)

- Petlas Tire Industry (Türkiye)

- Continental AG (Germany)

- Balkrishna Industries Ltd. (India)

- Trelleborg AB (Sweden)

- Maxam Tire International (U.S./Europe)

- Hankook Tire & Technology (South Korea)

- Bridgestone Corporation (Japan)

- Prometeon Tyre Group (Italy)

- Mitas a.s. (Czech Republic)

- Specialty Tires of America (U.S.)

- Magna Tyres Group (Netherlands)

- Titan International Inc. (U.S.)

- CEAT Ltd. (India)

- Yokohama Rubber Co. Ltd. (Japan)

- GRI Tires (Sri Lanka)

Latest Developments in Global Agricultural Tire Market

- In March 2025, Yokohama launched the Alliance Agriflex+ 377 XT flotation tire, engineered with VF sidewalls and CFO technology, enabling up to 40% higher load capacity at the same pressure and 55% additional load in cyclical operations. The tire incorporates enhanced bead construction and optimized tread geometry to improve flotation, reduce ruts, and maintain better ground contact during heavy field tasks. This advancement strengthens the brand’s position in the premium flotation tire segment by supporting large implements and promoting reduced soil compaction, which is becoming a critical purchase criterion among modern farmers adopting high-yield cropping systems

- In March 2025, Mitas introduced the Agriterra ULTRA trailer tire featuring a reinforced carcass design aimed at minimizing heat generation and improving structural stability under heavy transport loads. The new structure enhances durability during long-distance hauling and provides stronger resistance against lateral stress when operating at higher speeds. This development enhances Mitas’s presence in the agricultural trailer tire category, meeting rising demand for durable tires suited for high-speed hauling and intensive field-to-road operations in large-scale farming environments

- In March 2025, Apollo expanded its Vredestein Traxion line for CLAAS tractors by adding new sizes tailored for the ARION series to boost traction efficiency and field durability. The expansion leverages the Traxion tread pattern’s self-cleaning design, reinforced shoulders, and specialized rubber compound to improve performance across mixed soil conditions. This expansion reinforces Apollo’s OEM alignment with global tractor manufacturers while catering to farmers seeking improved grip, lower slippage, and extended service life in multipurpose field conditions

- In February 2025, BKT unveiled its newly upgraded AGRIMAX V-FLECTO series with enhanced IF/VF compounding aimed at improving load performance and extending tread life for high-horsepower tractors. The updated construction elevates stability during heavy towing, supports consistent pressure distribution, and reduces rolling resistance for improved fuel economy. This update strengthens BKT’s share in the premium radial category as farmers increasingly prioritize fuel efficiency, operational stability, and lower soil impact in precision farming applications

- In January 2025, Trelleborg announced advancements to its TM1000 ProgressiveTraction line, integrating updated lug geometry to reduce vibration and enhance contact area for superior traction. The redesigned lugs generate higher torque transfer, minimize slip during deep tillage, and provide smoother on-road travel when moving between fields. This innovation supports the brand’s competitiveness in the advanced radial tire market by addressing the need for greater pulling power and optimized fuel use in heavy-duty agricultural operations

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.