Global Agriculture Sensor Market

Market Size in USD Billion

USD

2.60 Billion

USD

6.31 Billion

2025

2033

USD

2.60 Billion

USD

6.31 Billion

2025

2033

| 2026 - 2033 | |

| USD 2.60 Billion | |

| USD 6.31 Billion | |

| % | |

|

Agriculture Sensor Market Size

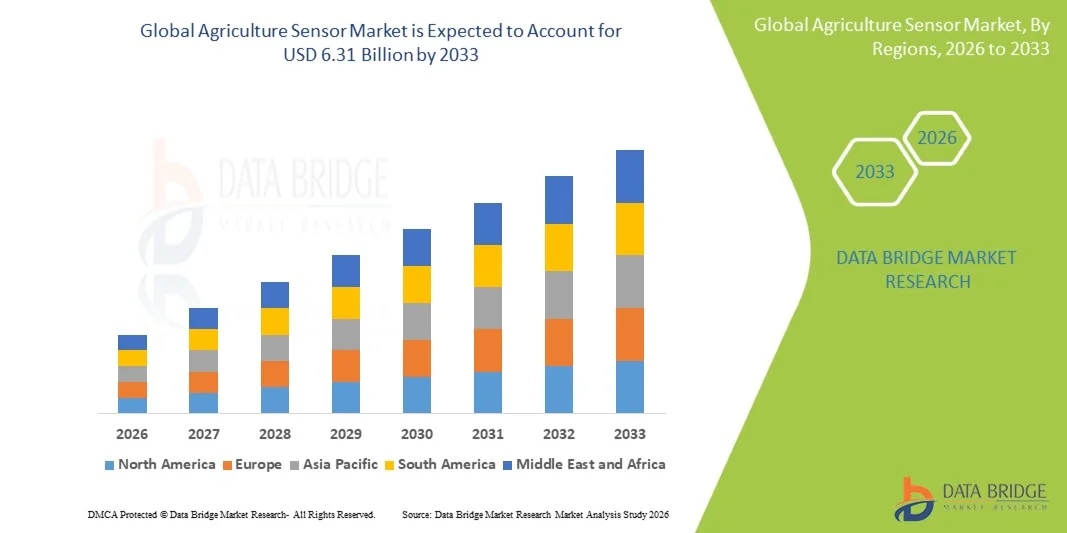

- The global agriculture sensor market size was valued at USD 2.60 billion in 2025 and is expected to reach USD 6.31 billion by 2033, at a CAGR of 11.73% during the forecast period

- The market growth is largely fueled by the increasing adoption of precision farming techniques and advancements in IoT, wireless connectivity, and smart monitoring technologies, leading to improved crop yield, soil health monitoring, and resource optimization in modern agriculture systems

- Furthermore, rising demand for sustainable farming practices, growing need for real-time field data, and increasing government support for smart agriculture initiatives are establishing agriculture sensors as a critical component of modern farming. These converging factors are accelerating the uptake of Agriculture Sensor solutions, thereby significantly boosting the industry's growth

Agriculture Sensor Market Analysis

- Agriculture sensors, which include soil sensors, crop sensors, climate sensors, and livestock monitoring devices, are increasingly vital in modern precision farming due to their ability to provide real-time data on soil moisture, temperature, nutrient levels, and crop health, enabling improved yield and resource efficiency

- The escalating demand for agriculture sensor solutions is primarily fueled by the growing adoption of precision agriculture practices, rising need for efficient water and fertilizer management, and increasing integration of IoT and AI-based smart farming technologies

- North America dominated the agriculture sensor market with the largest revenue share of approximately 37.8% in 2025, characterized by advanced agricultural infrastructure, high adoption of smart farming technologies, and strong presence of agri-tech companies, with the U.S. witnessing substantial growth driven by large-scale commercial farming and automation adoption

- Asia-Pacific is expected to be the fastest growing region in the agriculture sensor market during the forecast period, with a projected CAGR of around 10.6%, due to increasing food demand, government support for smart agriculture, rising mechanization, and expanding adoption of precision farming in countries such as India and China

- The DNA microarrays segment dominated the largest market revenue share of 45.7% in 2025, driven by its extensive use in gene expression analysis and genetic research in agricultural biotechnology

Report Scope and Agriculture Sensor Market Segmentation

|

Attributes |

Agriculture Sensor Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Agriculture Sensor Market Trends

“Enhanced Precision and Farm Efficiency Through AI and Smart Data Integration”

- A significant and accelerating trend in the global Agriculture Sensor market is the integration of artificial intelligence (AI), IoT-based analytics, and advanced digital platforms that enable real-time monitoring of soil, crop, and environmental conditions. This convergence of technologies is significantly improving farm productivity, resource efficiency, and decision-making accuracy

- For instance, AI-enabled agriculture sensors are increasingly used to monitor soil moisture, temperature, humidity, and nutrient levels in real time, helping farmers optimize irrigation and fertilization strategies for improved crop yield

- AI integration in agriculture sensors enables predictive analytics, where systems can forecast weather impacts, pest attacks, and crop stress conditions based on historical and real-time data. For instance, smart irrigation sensors use AI algorithms to recommend optimal watering schedules based on soil and climate conditions

- Voice-enabled systems integrated with agriculture platforms allow farmers to access sensor data hands-free through smart devices, enabling quick updates on field conditions without manual system checks, improving operational efficiency in large farms

- The integration of agriculture sensors with centralized digital farming platforms enables unified monitoring of multiple farm parameters such as soil health, crop growth, irrigation levels, and equipment status, creating a fully connected smart farming ecosystem

- The increasing adoption of AI-driven and voice-assisted agriculture sensor systems is reshaping modern farming practices by enabling precision agriculture, reducing resource wastage, and improving overall crop productivity

Agriculture Sensor Market Dynamics

Driver

“Rising Demand for Precision Farming and Smart Agriculture Practices”

- The increasing need for higher agricultural productivity, combined with limited arable land and growing global food demand, is driving strong adoption of agriculture sensor technologies

- For instance, in April 2025, several agritech companies introduced AI-powered soil monitoring systems capable of providing real-time insights into nutrient levels and irrigation needs, improving farm efficiency

- Agriculture sensors help farmers make data-driven decisions by providing real-time monitoring of environmental and soil conditions, reducing dependency on traditional manual farming methods

- The rising adoption of precision farming techniques is further boosting demand for smart agriculture sensors that optimize water usage, fertilizer application, and crop management

- In addition, government initiatives promoting smart agriculture and digital farming practices are accelerating the deployment of sensor-based farming solutions globally

Restraint/Challenge

“High Installation Costs and Limited Digital Awareness Among Farmers”

- One of the key challenges in the Agriculture Sensor market is the high initial cost of advanced sensor systems, which limits adoption among small and medium-scale farmers

- For instance, deployment of large-scale sensor networks across farmland requires significant investment in hardware, connectivity infrastructure, and maintenance

- Limited digital literacy and lack of awareness about precision farming technologies in developing regions also restrict market penetration

- Many farmers still rely on traditional farming methods due to insufficient training and lack of technical support for sensor-based system

- In addition, connectivity issues in rural and remote agricultural areas further hinder real-time data transmission and effective sensor utilization

- Overcoming these challenges through affordable sensor solutions, government subsidies, and farmer education programs will be essential for long-term market growth

Agriculture Sensor Market Scope

The market is segmented on the basis of product type and technology.

• By Product Type

On the basis of product type, the Agriculture Sensor market is segmented into DNA microarrays, protein microarrays, tissue microarrays, and others. The DNA microarrays segment dominated the largest market revenue share of 45.7% in 2025, driven by its extensive use in gene expression analysis and genetic research in agricultural biotechnology. DNA microarrays enable high-throughput screening of genetic variations in crops, improving yield and disease resistance studies. Increasing demand for precision agriculture supports adoption. Growing applications in plant genomics research further strengthen demand. Advancements in bioinformatics enhance data interpretation capabilities. Rising investment in agricultural R&D boosts usage. Government initiatives promoting food security accelerate adoption. Expanding use in crop improvement programs supports growth. These factors collectively reinforce DNA microarrays dominance.

The protein microarrays segment is expected to witness the fastest CAGR of 9.6% from 2026 to 2033, driven by increasing demand for proteomic analysis in plant stress and disease studies. Protein microarrays help identify plant-pathogen interactions efficiently. Growing focus on crop protection and yield optimization supports adoption. Advancements in protein detection technologies enhance sensitivity. Rising research in agricultural biotechnology fuels demand. Expanding use in precision farming applications strengthens growth. Increasing funding for proteomics research boosts development. Improved assay techniques enhance accuracy and reliability. Growing awareness of plant health monitoring supports expansion. These factors position protein microarrays as the fastest-growing product segment.

• By Technology

On the basis of technology, the Agriculture Sensor market is segmented into optical-based arrays, electrochemical arrays, nanotechnology-based arrays, and others. The optical-based arrays segment held the largest market revenue share of 42.3% in 2025, driven by their high accuracy, rapid detection capabilities, and non-invasive nature in agricultural analysis. Optical systems are widely used for monitoring plant health and detecting biological changes. Increasing adoption in precision agriculture supports growth. Advancements in imaging technologies enhance performance. Rising demand for real-time crop monitoring strengthens usage. Expanding smart farming practices boost adoption. Government support for modern agriculture accelerates deployment. Integration with IoT systems improves efficiency. Continuous innovation in optical sensing improves reliability. These factors ensure dominance of optical-based arrays.

The nanotechnology-based arrays segment is expected to witness the fastest CAGR of 10.8% from 2026 to 2033, driven by increasing use of nanosensors for ultra-sensitive detection of biological and chemical signals. Nanotechnology enables early detection of crop diseases and nutrient deficiencies. Rising demand for precision farming supports adoption. Advancements in nano-biosensors enhance accuracy and efficiency. Expanding agricultural biotechnology research fuels growth. Increasing investment in smart farming technologies boosts development. Growing focus on sustainable agriculture supports usage. Integration with AI-driven analytics enhances decision-making. Improved cost-effectiveness of nanotech solutions accelerates adoption. These factors position nanotechnology-based arrays as the fastest-growing technology segment.

Agriculture Sensor Market Regional Analysis

- North America dominated the agriculture sensor market with the largest revenue share of approximately 37.8% in 2025, characterized by advanced agricultural infrastructure, high adoption of smart farming technologies, and a strong presence of leading agri-tech companies

- The region benefits from large-scale commercial farming practices, widespread use of IoT-enabled devices, and increasing integration of data-driven agriculture solutions

- Farmers in the region are increasingly adopting soil monitoring, climate sensing, and crop health tracking technologies to enhance productivity and optimize resource utilization. This widespread adoption is further supported by high investment capacity, technological awareness, and the growing focus on sustainable farming practices

U.S. Agriculture Sensor Market Insight

The U.S. agriculture sensor market captured the largest share within North America, driven by extensive adoption of precision agriculture technologies and strong government and private sector investments in agri-tech innovation. Large-scale farms are increasingly deploying advanced sensor systems for real-time monitoring of soil conditions, irrigation levels, and crop performance. In addition, the integration of AI and IoT in agriculture is enabling farmers to improve yield efficiency and reduce operational costs. The growing emphasis on automation and data-driven decision-making continues to propel the Agriculture Sensor industry in the U.S.

Europe Agriculture Sensor Market Insight

The Europe agriculture sensor market is projected to expand at a substantial CAGR during the forecast period, primarily driven by increasing focus on sustainable agriculture, strict environmental regulations, and rising adoption of precision farming technologies. Farmers across the region are increasingly utilizing sensor-based systems to optimize water usage, reduce chemical inputs, and improve crop productivity. The region is also witnessing strong growth in greenhouse farming and controlled environment agriculture, where sensors play a critical role in monitoring and maintaining optimal growing conditions.

U.K. Agriculture Sensor Market Insight

The U.K. agriculture sensor market is anticipated to grow at a noteworthy CAGR, supported by increasing adoption of digital farming technologies and rising awareness regarding efficient resource utilization. Farmers are leveraging agriculture sensors for soil health monitoring, weather tracking, and crop management to enhance farm productivity. In addition, government initiatives promoting sustainable agriculture and smart farming practices are further accelerating the adoption of sensor-based technologies in the country.

Germany Agriculture Sensor Market Insight

The Germany agriculture sensor market is expected to expand at a considerable CAGR, driven by strong technological advancements, increasing focus on precision agriculture, and a well-established agricultural research ecosystem. German farmers are increasingly adopting sensor-based solutions to improve efficiency, reduce environmental impact, and ensure compliance with sustainability standards. The integration of smart farming equipment with sensor technologies is also becoming increasingly prevalent, supporting enhanced farm automation and productivity.

Asia-Pacific Agriculture Sensor Market Insight

The Asia-Pacific agriculture sensor market is expected to be the fastest growing region during the forecast period, with a projected CAGR of approximately 10.6%, driven by increasing food demand, government support for smart agriculture, rising mechanization, and expanding adoption of precision farming in countries such as China, India, and Japan. Rapid population growth and the need to enhance agricultural productivity are encouraging farmers to adopt advanced sensor technologies. In addition, improving rural infrastructure and increasing availability of affordable sensor solutions are further boosting market growth in the region.

Japan Agriculture Sensor Market Insight

The Japan agriculture sensor market is gaining momentum due to advanced farming technologies, increasing adoption of automation, and strong focus on improving agricultural efficiency. Farmers are utilizing sensor-based systems for monitoring soil conditions, crop health, and environmental factors to enhance yield quality. The country’s aging farming population is also driving demand for automated and easy-to-use smart agriculture solutions, further supporting the adoption of agriculture sensors.

China Agriculture Sensor Market Insight

The China agriculture sensor market accounted for the largest market share in Asia-Pacific in 2025, driven by rapid agricultural modernization, strong government initiatives supporting smart farming, and increasing adoption of precision agriculture technologies. Large-scale farming operations are increasingly integrating sensor-based systems to monitor crop conditions, optimize irrigation, and improve overall productivity. In addition, the country’s growing agri-tech industry and focus on food security are key factors propelling the demand for agriculture sensors.

Agriculture Sensor Market Share

The Agriculture Sensor industry is primarily led by well-established companies, including:

- Deere & Company (U.S.)

- Trimble Inc. (U.S.)

- Bosch (Germany)

- Siemens (Germany)

- Libelium (Spain)

- Pessl Instruments (Austria)

- CropX (Israel)

- Arable Labs (U.S.)

- Sentera (U.S.)

- Davis Instruments (U.S.)

- Campbell Scientific (U.S.)

- Acclima Inc. (U.S.)

- AquaSpy (U.S.)

- Teralytic (U.S.)

- Raven Industries (U.S.)

- CNH Industrial (U.K)

- Topcon Positioning Systems (U.S.)

- Ag Leader Technology (U.S.)

- Yara International (Norway)

Latest Developments in Global Agriculture Sensor Market

- In August 2025, OMRON Electronic Components announced the launch of its next-generation Weather Sensor designed to provide highly accurate and reliable environmental data for agriculture, meteorology, and smart farming applications — a key development supporting data-driven agricultural decision-making

- In October 2025, CropX launched a new Strato 1 field weather station, providing hyper-local weather data to complement soil monitoring systems and support more precise irrigation and planting decisions, enhancing precision agriculture capabilities

- In February 2025, John Deere introduced new planter technologies featuring seed level and fertilizer level sensing and active vacuum automation, enabling real-time data feedback and greater precision during planting and fertilization — a significant step forward in integrating sensor technology into core agricultural equipment

- In November 2025, Lindsay Corporation finalized its acquisition of Pessl Instruments, expanding its smart irrigation and environmental sensor portfolio under the METOS ecosystem — a strategic development broadening sensor offerings for precision agriculture and environmental monitoring

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.