Global Agrivoltaics Market

Market Size in USD Billion

USD

4.20 Billion

USD

8.87 Billion

2025

2033

USD

4.20 Billion

USD

8.87 Billion

2025

2033

| 2026 - 2033 | |

| USD 4.20 Billion | |

| USD 8.87 Billion | |

| % | |

|

Agrivoltaics Market Size

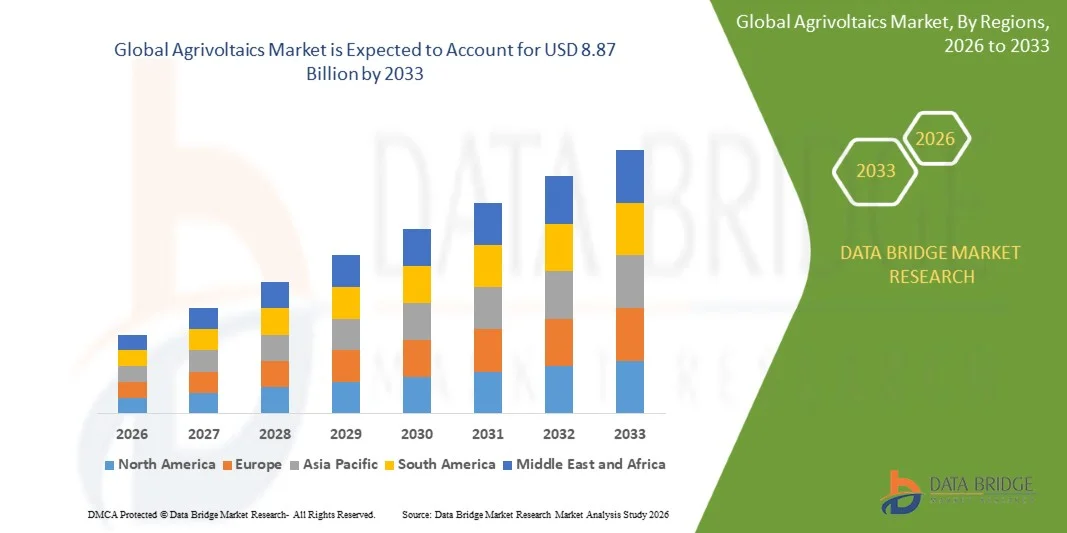

- The global agrivoltaics market size was valued at USD 4.2 billion in 2025 and is expected to reach USD 8.87 billion by 2033, at a CAGR of 9.80% during the forecast period

- The agrivoltaics market is primarily driven by the rising need to maximize land productivity by enabling the simultaneous use of farmland for both solar energy generation and agriculture, creating dual revenue streams for farmers and improving land-use efficiency

- In addition, increasing pressure to transition toward renewable energy, combined with the need for climate-resilient farming practices, is accelerating the adoption of agrivoltaic systems as they help reduce crop stress, enhance water retention, and improve overall farm sustainability

Agrivoltaics Market Analysis

- Agrivoltaics, which integrates photovoltaic systems with active agricultural production, is emerging as a transformative solution that supports clean-energy generation while maintaining or improving crop yields, making it a strategically valuable approach for addressing both energy and agricultural challenges

- The demand for agrivoltaics is gaining momentum due to the global push for decarbonization, supportive policy initiatives, and increasing recognition of the technology’s ability to enhance farm profitability, promote environmental sustainability, and strengthen food–energy security across diverse regions

- Europe dominated the agrivoltaics market with a share of 37.6% in 2025, due to strong renewable energy commitments, supportive regulatory frameworks, and widespread adoption of sustainable farming practices

- Asia-Pacific is expected to be the fastest growing region in the agrivoltaics market during the forecast period due to rapid urbanization, rising food demand, agricultural modernization, and government initiatives supporting dual-use agricultural models

- Fixed panel segment dominated the market with a market share of 68.7% in 2025, due to its lower installation complexity and cost-efficient structure suitable for large-scale agricultural fields. Farmers prefer fixed panel systems due to their reliability, as they provide stable shade distribution that improves soil moisture retention and crop resilience during high-temperature periods. These systems have a longer operational lifespan with minimal mechanical components, reducing maintenance requirements for rural users. Fixed panels also align well with government renewable energy projects that prioritize low-cost photovoltaic expansion. Their ability to integrate seamlessly with crops such as vegetables, berries, and leafy greens further strengthens their extensive market adoption

Report Scope and Agrivoltaics Market Segmentation

|

Attributes |

Agrivoltaics Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Agrivoltaics Market Trends

“Growing Integration of Dual-Use Farming and Solar Energy Systems”

- A significant trend in the agrivoltaics market is the growing integration of solar power generation with active agricultural operations, driven by the rising emphasis on efficient land use and sustainable energy production. This trend is enabling farmlands to function as dual-purpose assets where crop cultivation and renewable energy generation operate in parallel to improve overall land productivity

- For instance, companies such as Enel Green Power deploy agrivoltaic installations that combine elevated solar structures with crop farming practices. These systems enhance land output by producing clean energy while supporting continued agricultural activity through controlled light distribution and microclimate benefits

- The adoption of agrivoltaics is expanding as solar panels mounted above crop fields improve shading conditions that support plant health and reduce heat stress. This integration is helping farmers adapt to climate variability and sustain yields in regions facing rising temperatures

- The market is experiencing increased interest in designs that optimize panel height and spacing to balance crop growth with peak solar generation. Such advancements are intensifying the focus on dual-use strategies that improve energy output without compromising agricultural productivity

- Agricultural researchers and solar developers are collaborating to refine system architectures that support diverse crop types. These initiatives are strengthening the value proposition of agrivoltaics as a long-term solution for improving land efficiency and renewable energy integration

- The agrivoltaics market is witnessing strong momentum due to rising demand for sustainable land practices that deliver both food security and clean energy generation. This trend continues to position dual-use solar systems as an essential component of modern agricultural development and climate-smart farming

Agrivoltaics Market Dynamics

Driver

“Rising Demand for Renewable Energy and Efficient Land Utilization”

- The rising focus on renewable energy adoption across rural and agricultural regions is driving the demand for agrivoltaic systems that combine food production with solar power generation. These systems support climate goals while enabling farmers to generate additional income through energy sales

- For instance, companies such as Next2Sun implement vertical agrivoltaic structures that maximize land utilization by enabling solar power generation without reducing usable farmland. These designs help landowners achieve higher productivity and diversify revenue sources

- Policies promoting renewable energy expansion are encouraging farmers to adopt solar-integrated agricultural solutions that optimize resource use. This demand is strengthening the market’s transition toward multifunctional land management

- The need for resilient energy infrastructure in agricultural regions is boosting investment in integrated farming–solar systems that provide reliable power generation. This driver continues to gain relevance as energy demands rise across rural economies

- The expanding recognition of agrivoltaics as a high-value land optimization strategy is reinforcing this driver. The alignment of renewable energy goals with agricultural productivity is shaping a stronger growth outlook for dual-use solar systems across global markets

Restraint/Challenge

“High Initial Installation Costs and System Complexity”

- The agrivoltaics market faces challenges due to the high upfront costs associated with designing and installing elevated or specifically engineered solar structures suitable for active farming environments. These tailored systems require durable materials and specialized engineering to ensure compatibility with agricultural operations

- For instance, companies such as BayWa r.e. integrate customized mounting systems and advanced tracking technologies to maintain balanced light distribution for crops. These complex configurations increase installation cost and require precise technical planning

- Engineering agrivoltaic projects involves careful evaluation of crop compatibility, shading impacts, and spatial design, which extends planning timelines and complicates system development. This complexity raises barriers for small-scale farmers

- Maintenance requirements become more intricate due to the coexistence of farming activity and solar infrastructure. Operators must manage equipment durability while supporting routine agricultural operations, increasing operational challenges

- The reliance on specialized system designs and precision engineering contributes to cost constraints that affect overall affordability. These challenges collectively limit market penetration among regions with budget-sensitive farming communities

Agrivoltaics Market Scope

The market is segmented on the basis of system design, technology, crop type, placement, and application.

• By System Design

On the basis of system design, the agrivoltaics market is segmented into dynamic panel and fixed panel systems. The fixed panel segment dominated the market with the largest share of 68.7% in 2025, supported by its lower installation complexity and cost-efficient structure suitable for large-scale agricultural fields. Farmers prefer fixed panel systems due to their reliability, as they provide stable shade distribution that improves soil moisture retention and crop resilience during high-temperature periods. These systems have a longer operational lifespan with minimal mechanical components, reducing maintenance requirements for rural users. Fixed panels also align well with government renewable energy projects that prioritize low-cost photovoltaic expansion. Their ability to integrate seamlessly with crops such as vegetables, berries, and leafy greens further strengthens their extensive market adoption.

The dynamic panel segment is expected to witness the fastest growth from 2026 to 2033, propelled by rising interest in adaptive solar tracking technology that boosts total energy yield. Dynamic panels adjust their tilt to maximize sunlight collection while optimizing the light available for crops, improving dual-use land productivity. These systems appeal to commercial farms aiming to increase energy revenue without compromising crop output. The enhanced microclimate control offered by dynamic designs supports sensitive crop varieties, creating new revenue opportunities. The surge in innovation around automated tracking systems and IoT-based control platforms further accelerates adoption. Their efficiency-driven design makes dynamic panels a preferred option for long-term agrivoltaic expansion.

• By Technology

On the basis of technology, the agrivoltaics market is segmented into monofacial, bifacial, and translucent modules. The monofacial segment dominated the market in 2025, favored for its lower installation cost and proven durability across diverse farming environments. Monofacial panels remain a popular choice for farmers seeking consistent energy production with simple maintenance. They perform effectively in traditional ground-mounted agrivoltaic layouts, where maximizing direct solar radiation is essential. The technology benefits from wide market availability and established supply chains, making deployment easier for rural agricultural regions. Their compatibility with crops requiring moderate shading enhances adoption across fruit and vegetable farming.

The bifacial segment is projected to record the fastest growth rate from 2026 to 2033, driven by its ability to generate electricity from both sides, improving energy efficiency in agrivoltaic settings. Bifacial modules capitalize on reflected light from soil, crops, or ground coverings, significantly increasing total output. Their adaptability to elevated and vertical installations makes them appealing for farms prioritizing shading uniformity and energy optimization. Commercial farms adopt bifacial panels to maximize land productivity under dual-use systems. The technology aligns with emerging agrivoltaic research that highlights improved crop performance under diffused light. Growing investment in high-efficiency solar technologies further strengthens market expansion for bifacial solutions.

• By Crop

On the basis of crop type, the agrivoltaics market is segmented into fruits, vegetables, and others. The vegetables segment dominated the market in 2025, driven by the high suitability of leafy greens, herbs, and shade-tolerant vegetables under agrivoltaic structures. Many vegetable species benefit from partial shading, which reduces heat stress and improves water efficiency during peak summer periods. Farms producing lettuce, spinach, cabbage, and similar crops achieve improved yields and quality under optimized light-sharing systems. Vegetable cultivation offers rapid harvest cycles, allowing farmers to quickly evaluate agrivoltaic productivity and economic return. The segment benefits from strong demand in local and global food supply chains. Its compatibility with fixed and dynamic solar structures strengthens continued dominance.

The fruits segment is projected to witness the fastest growth from 2026 to 2033, supported by increasing adoption of agrivoltaic systems for berries, grapes, and orchard crops. Fruit crops benefit from controlled microclimates created by elevated solar structures that protect against hail, excessive heat, and UV radiation. These advantages reduce weather-related losses and enhance overall yield stability. Research highlights improved fruit quality under partial shading, especially in berries and grapes, encouraging farm-level investment. Rising global demand for high-value crops accelerates deployment of agrivoltaic solutions among specialty fruit producers. The integration of solar structures with trellis-based farming models further strengthens market expansion.

• By Placement

On the basis of placement, the agrivoltaics market is segmented into greenhouses, ground-mounted systems, and shading nets. The ground-mounted segment dominated the market in 2025, backed by large-scale deployment across open agricultural fields. These systems offer flexible installation height, allowing sufficient clearance for farm machinery while providing uniform shade to crops. Their suitability for solar-electricity generation alongside commercial farming enhances operational revenue for landowners. Ground-mounted agrivoltaic layouts are favored in regions with wide agricultural land availability. Their structural stability and adaptability to different terrain types make them widely preferred among farmers. Supportive policies for solar land development further contribute to segment leadership.

The greenhouses segment is anticipated to grow at the fastest rate from 2026 to 2033, driven by rising adoption of solar-integrated greenhouse designs for horticulture and controlled-environment agriculture. Greenhouse agrivoltaics utilize translucent or semi-transparent PV panels that balance energy production with optimal light diffusion. These systems protect crops from extreme temperatures and unpredictable weather events, improving year-round productivity. Solar-powered greenhouses also reduce energy costs associated with heating, cooling, and irrigation. High-value crops grown under greenhouse conditions offer substantial profit margins, motivating farmers to adopt this model. Growing interest in sustainable greenhouse farming accelerates segment expansion.

• By Application

On the basis of application, the agrivoltaics market is divided into grassland farming, horticulture and arable farming, indoor farming, and more. The horticulture and arable farming segment dominated the market in 2025, supported by large-scale adoption of agrivoltaic systems for vegetables, fruits, cereals, and specialty crops. These farming categories benefit heavily from the microclimate regulation provided by elevated PV structures, which improves crop health and reduces irrigation needs. Farmers leverage agrivoltaic layouts to boost combined energy and crop output, enhancing overall land efficiency. The segment aligns strongly with dual-use land policies in multiple regions. Its compatibility with fixed and bifacial panel systems supports widespread deployment. The strong economic return from integrating solar revenue with mainstream crops ensures continued dominance.

The indoor farming segment is expected to be the fastest growing from 2026 to 2033, driven by rising interest in solar-powered controlled-environment agriculture. Agrivoltaics supports indoor farming by providing renewable electricity for climate control, irrigation pumps, LED lighting, and automation systems. Urban farming units and vertical farms increasingly depend on clean energy to reduce operational costs and carbon emissions. The integration of on-site solar generation enhances energy independence and reliability for indoor facilities. Growing demand for pesticide-free produce in metropolitan areas accelerates investment in agrivoltaic-enabled indoor farming structures. The segment’s alignment with sustainability goals drives rapid market expansion.

Agrivoltaics Market Regional Analysis

- Europe dominated the agrivoltaics market with the largest revenue share of 37.6% in 2025, driven by strong renewable energy commitments, supportive regulatory frameworks, and widespread adoption of sustainable farming practices

- Across the region, farmers and agricultural enterprises increasingly integrate solar installations with crop production to enhance land productivity and reduce energy dependence. European countries emphasize climate resilience and carbon reduction, which accelerates the uptake of agrivoltaic systems across vineyards, orchards, vegetable farms, and horticulture facilities

- The presence of advanced solar technologies, combined with well-established agricultural infrastructure, further strengthens regional adoption. This momentum is reinforced by government incentives, research collaborations, and pilot projects that demonstrate the dual benefits of agricultural output and clean power generation. Europe continues to lead in large-scale agrivoltaic deployment across both open-field and greenhouse applications

Germany Agrivoltaics Market Insight

The Germany agrivoltaics market held a substantial revenue share in 2025, driven by rising awareness of sustainable agricultural systems and strong national emphasis on renewable energy expansion. Farmers increasingly adopt elevated solar structures to protect crops from heat stress, maintain soil moisture, and stabilize yield quality. The country’s advanced research ecosystem, strong innovation culture, and extensive demonstration projects across vineyards, vegetable farms, and open fields continue to accelerate the adoption of agrivoltaics nationwide.

U.K. Agrivoltaics Market Insight

The U.K. agrivoltaics market is anticipated to grow at a notable CAGR during the forecast period, supported by rising interest in climate-resilient farming, expanding renewable energy initiatives, and the need to improve productivity on limited arable land. Farmers and estate owners increasingly recognize agrivoltaics as a strategic method to generate clean energy while creating moderated microclimates that enhance crop performance. The region’s evolving policy support and expanding focus on sustainable land management continue to drive market penetration.

Asia-Pacific Agrivoltaics Market Insight

The Asia-Pacific agrivoltaics market is projected to grow at the fastest CAGR during 2026 to 2033, driven by rapid urbanization, rising food demand, agricultural modernization, and government initiatives supporting dual-use agricultural models. Countries across the region increasingly adopt agrivoltaic systems to mitigate heat stress, enhance crop yield stability, and improve rural electrification. Strong solar manufacturing capabilities and expanding renewable energy policies further support widespread deployment across open farmland, horticultural zones, and greenhouse environments.

Japan Agrivoltaics Market Insight

The Japan agrivoltaics market is gaining momentum due to limited arable land, advanced technological capabilities, and the country’s focus on maximizing land productivity through integrated solar-agriculture systems. Farmers adopt agrivoltaics to balance energy production with enhanced crop quality under controlled shading environments. Japan’s strong inclination toward high-tech farming, IoT-enabled monitoring, and climate-adaptive agricultural practices continues to support market expansion across various regions.

China Agrivoltaics Market Insight

The China agrivoltaics market accounted for the largest revenue share in Asia-Pacific in 2025, supported by rapid rural development efforts, large-scale solar installations, and growing modernization of agricultural practices. Extensive government backing for renewable energy and dual-land-use programs encourages the deployment of agrivoltaics across vegetable farms, orchards, grasslands, and greenhouse clusters. China’s strong domestic solar manufacturing ecosystem and cost-efficient installation models further accelerate the expansion of agrivoltaic projects across multiple provinces.

Agrivoltaics Market Share

The agrivoltaics industry is primarily led by well-established companies, including:

- Sun’Agri (France)

- Enel Green Power (Italy)

- BayWa r.e. (Germany)

- Fraunhofer ISE (Germany)

- Next2Sun (Germany)

- Insolight (Switzerland)

- REM TEC (Italy)

- Kyocera Corporation (Japan)

- Acciona Energía (Spain)

- EDF Renewables (France)

- Zimmermann PV-Stahlbau (Germany)

- Scatec ASA (Norway)

- Arava Power Company (Israel)

- Ameresco (U.S.)

- ENGIE SA (France)

- R.Power Group (Poland)

- TNO (Netherlands)

- Hevel Solar (Russia)

Latest Developments in Global Agrivoltaics Market

- In June 2025, Cero Generation began operating its 48 MW agrivoltaic project in Italy, marking one of the most substantial operational deployments of agriPV infrastructure in Europe. The project showcases how large-scale solar assets can be effectively harmonized with agricultural production, demonstrating stable crop performance alongside renewable-energy output. Its success is expected to accelerate regulatory support, attract institutional investors, and encourage replication across Southern Europe, where land scarcity and high solar potential make dual-use systems particularly valuable for long-term market expansion

- In April 2025, Fraunhofer ISE introduced lightweight photovoltaic modules specifically engineered for crop-level mounting, addressing structural and agronomic constraints that previously limited deployment over delicate or shade-sensitive crops. By reducing weight and improving adaptability, these modules enable installations in fields where standard PV panels would restrict farming operations or damage soil quality. This advancement is likely to broaden technology compatibility across diverse crop categories, improve farmer acceptance, and stimulate demand for flexible agriPV designs that can integrate seamlessly with existing agricultural workflows

- In April 2025, JA Solar supplied its DeepBlue high-efficiency modules to the Suji Sandland agrivoltaic farm, reinforcing the importance of high-performance panels in maximizing energy generation under conditions of partial shading, variable terrain, and crop-driven spacing patterns. The deployment highlights rising adoption of advanced module technologies that enhance both photovoltaic output and the microclimate benefits essential for sustaining agricultural productivity. This integration is expected to promote deeper collaboration between solar manufacturers and agrivoltaic developers, driving the market toward higher-efficiency, crop-compatible module solutions

- In January 2025, Trinasolar US launched integrated solar-storage packages tailored for agricultural operations, responding to a critical need for reliable, stable, and cost-efficient on-farm energy supply. These packages combine photovoltaic generation with storage to mitigate grid fluctuations, support irrigation systems, and provide consistent power for farm equipment. By offering a unified solution rather than separate components, Trina is helping reduce project complexity and installation costs, which is likely to boost adoption among small and mid-scale farms and strengthen the commercial readiness of agrivoltaic systems across North America

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.